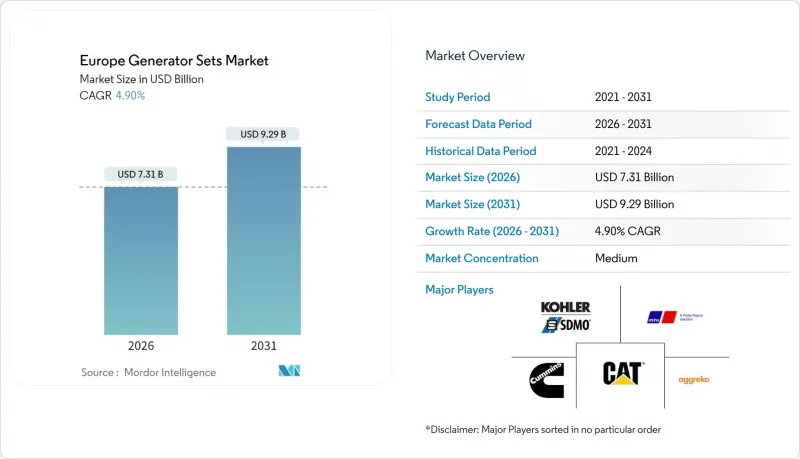

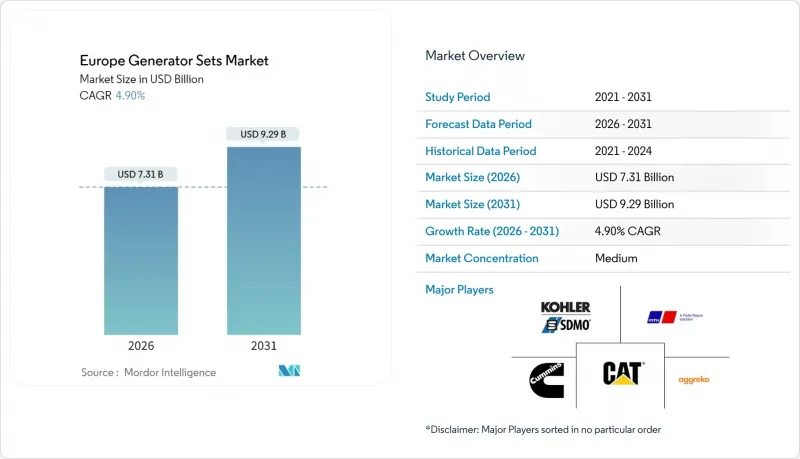

유럽의 발전기 시장 규모는 2026년에 73억 1,000만 달러로 추정되고 있습니다.

2025년 69억 7,000만 달러에서 성장하며, 2031년에는 92억 9,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 4.9%로 성장이 전망되고 있습니다.

데이터센터, 의료시설, 재생에너지 프로젝트가 저탄소 백업 전원을 요구하면서 디젤 전용 제품에서 이중 연료, 가스, 수소 지원 플랫폼으로 수요가 이동하고 있습니다. 기업의 지속가능성 프로그램, V단계 배출 규제, 대도시 지역의 전력망 혼잡이 이러한 전환을 가속화하고 있으며, 배터리와 발전기의 하이브리드 시스템 및 모듈식 구조가 조달 추세를 바꾸고 있습니다. 독일은 여전히 가장 큰 단일 국가 시장이지만, 스페인의 급속한 재생에너지 도입과 인프라 구축 계획이 가장 빠른 증가율을 보이고 있습니다. 용량 수준에서는 75kVA-375kVA 부문이 여전히 출하량을 주도하고 있지만, 하이퍼스케일 데이터센터가 750kVA-2,000kVA 유닛에 대한 수요 증가를 주도하고 있습니다. 경쟁 전략은 연료 독립형 엔진, 수소 파일럿 사업, 디지털 커넥티드 렌탈 차량에 초점을 맞추고 있으며, 마이크로그리드 도입, 고립형 전력 공급, 건설 현장의 새로운 기회를 개발하고 있습니다.

프랑크푸르트, 암스테르담, 파리, 더블린의 데이터센터 운영사들은 그리드의 제약을 상쇄하고, Tier III 가동 시간을 충족하고, 주파수 응답 시장에서 용량을 수익화하기 위해 수 메가 와트 규모의 발전기를 추가 도입하고 있습니다. 병원은 EN 50172의 스위칭 규정과 24시간 연료 비축 요건을 충족하기 위해 모듈식 병렬 운전이 가능한 발전기로 업그레이드를 진행하고 있습니다. 커민스는 2024년 유럽 데이터센터 수주가 두 자릿수 성장을 기록하며 3,500kVA QSK95가 선호되는 플랫폼으로 부상했습니다. 대기 및 피크 쉐이빙의 역할을 위해 장비가 점점 더 많이 지정되어 평균 가동 시간이 연장되고 저 NOx 가스 장치에 대한 수요가 증가하고 있습니다. 의료 분야 구매자는 예방적 유지보수 및 ISO 22301 비즈니스 연속성 감사를 지원하는 원격 진단 기능을 갖춘 장치를 선호합니다.

스페인의 태양광 및 교통 인프라 확충, 폴란드의 철도망 개편, 이탈리아의 국가 재건 및 회복력 계획으로 인해 프로젝트 공사 기간이 길어지고 이동식 전원 대여 계약 기간이 연장되고 있습니다. 유럽 건설 산업은 2024년 1조 6,000억 유로의 생산액을 창출할 것으로 예상되며, 100kVA-500kVA의 이동식 발전기는 현장에 상설 전원이 없는 환경에서 여전히 필수적입니다. Aggreko는 2024년 유럽 임대 장비를 12% 확대하고, Stage V에 부합하는 디젤-배터리 하이브리드 장비를 통해 저부하 시간대 연료 소비를 30% 절감할 수 있도록 했습니다. 건설업체들은 가동 시간, 배출량, 연료 소비를 실시간으로 모니터링할 수 있는 텔레메트리 지원 장비를 점점 더 많이 요구하고 있으며, 발전기를 보다 광범위한 현장 관리 대시보드에 통합하는 추세가 증가하고 있습니다.

2024년부터 전면 시행되는 Stage V 규제에 따라 56kW 이상 디젤 발전기는 디젤 미립자 필터(DPF), 선택적 촉매 환원(SCR), 배기가스 재순환(EGR) 장착이 의무화되어 자본비용이 최대 18% 상승할 것으로 예측됩니다. 또한 DEF 보충 및 필터 재생을 위한 유지보수 비용으로 0.02-0.04유로/kWh가 추가됩니다. 75kVA-375kVA급 소규모 구매자들은 갱신을 연기하거나 가스 발전기로 전환하고 있으며, 아트라스콥코의 200kVA 미만 디젤 발전기 주문이 9% 감소한 반면, 가스 및 하이브리드 발전기 출하량은 14% 증가한 것이 이를 지원하고 있습니다. 제안된 Stage VI 규제에 따르면 2027년 이후 NOx 배출 기준은 30% 더 강화될 것으로 예측됩니다. 이로 인해 OEM 업체들은 암모니아 슬립 촉매를 채택할 수밖에 없었고, 이는 비용 상승과 연료 전환을 촉진하는 요인으로 작용했습니다.

2025년 기준 유럽 발전기 시장의 34.62%를 차지하는 75kVA-375kVA급은 표준화된 인클로저, 대량 생산, 경쟁력 있는 가격으로 지원되고 있습니다. 이 유닛들은 소매 체인 및 상업용 빌딩의 공조 설비, 냉동 설비, POS 시스템의 백업을 담당하고 있습니다. 배터리 스토리지가 소규모 계통연계 부하에 침투하면서 성장이 둔화되고 있지만, Stage V 규제에 따라 새로운 하드웨어가 필요하므로 교체 수요는 지속되고 있습니다.

750kVA-2,000kVA 부문은 무정전 전원 공급을 위해 N+1 레이아웃으로 모듈형 세트를 도입하는 데이터센터 캠퍼스 및 대규모 제조 시설에 힘입어 6.25%의 연평균 복합 성장률(CAGR)을 달성할 것으로 예측됩니다. 커민스의 3,500kVA QSK95는 배전반 재설계 없이 1 MW 블록을 추가할 수 있으며, 설치 기간을 단축할 수 있습니다. 2,000kVA 이상에서는 Wartsil 및 Caterpillar의 가스 또는 이중 연료 장치를 도입한 그리드 밸런싱 및 독립 전원 유틸리티를 예로 들 수 있습니다. 75kVA 이하에서는 정전 시간이 4시간 이하인 지역에서는 배터리와 인버터의 조합이 선호되고 있으며, 주거 및 소규모 상업시설 수요는 감소하는 추세입니다.

2025년 연료 구성에서 디젤은 52.88%를 차지합니다. 이는 주로 대규모 설치 기반과 연료의 보편적인 가용성 때문입니다. Stage V 규제 비용, 도심 저공해 구역, Scope 2 목표에 따라 CO2 배출량 30%, 미립자 물질 50%를 감축하는 듀얼 연료 유닛의 도입이 진행되고 있습니다. 천연가스 유닛은 독일, 네덜란드 등 파이프라인이 밀집된 지역에 집중되어 수요의 약 22%를 차지합니다. 반면, 바이오연료 대응 모델은 3% 미만에 불과하지만, Neste사의 HVO 공급량 증가에 따라 그 규모가 확대되고 있습니다.

커민스, 월실, 롤스로이스의 수소 지원 엔진은 2024년 상용 포트폴리오에 도입될 예정입니다. 그 채택률은 아직 1% 미만이지만, 전해장치의 건설과 파이프라인 인프라가 성숙해지면 상승할 것으로 예측됩니다. 프로판, 바이오가스, 매립지 가스 엔진은 보다 제한된 틈새 분야에서 사용되고 있습니다. 디젤의 점유율은 2031년까지 47.50% 이하로 떨어질 것으로 예상되지만, 이는 디젤이 완전히 대체되기 때문이 아니라 가스 및 하이브리드 제품의 성장이 더 빠르기 때문입니다.

유럽 발전기 시장 보고서는 용량별(75KVA 미만, 75-375KVA, 375-750KVA, 750-2,000KVA, 2,000KVA 이상), 연료 유형별(디젤, 천연가스, 이중연료/하이브리드, 신재생/바이오연료, 기타), 용도별(비상전원, 주전원/연속전원, 기타), 지역별(독일, 영국, 스페인, 미국, 프랑스, 이탈리아, 독일, 영국, 스페인) 주전원/연속전원, 기타), 최종사용자별(주택, 상업용 건물, 데이터센터, 기타), 지역별(독일, 영국, 스페인, 기타)로 분류되어 있습니다.

Europe Generator Sets market size in 2026 is estimated at USD 7.31 billion, growing from 2025 value of USD 6.97 billion with 2031 projections showing USD 9.29 billion, growing at 4.9% CAGR over 2026-2031.

Demand is shifting from diesel-only products to dual-fuel, gas and hydrogen-ready platforms as data centers, healthcare facilities, and renewable energy projects seek lower-carbon back-up power. Corporate sustainability programs, Stage V emissions rules, and grid congestion in metropolitan clusters are accelerating the transition, while battery-genset hybrids and modular architectures are reshaping procurement preferences. Germany remains the single-largest country market, but Spain's rapid renewable build-out and infrastructure programs are creating the fastest incremental growth. At the capacity level, the 75 kVA to 375 kVA segment still dominates shipments, yet hyperscale data centers are driving a swift rise in demand for 750 kVA to 2,000 kVA units. Competitive strategies center on fuel-agnostic engines, hydrogen pilots, and digitally connected rental fleets, which open up opportunities in microgrid deployments, island utilities, and construction sites.

Data-center operators in Frankfurt, Amsterdam, Paris, and Dublin are adding multi-megawatt generators to offset grid constraints, satisfy Tier III uptime, and monetize capacity in frequency-response markets. Hospitals are upgrading to modular, parallel-capable gensets to meet EN 50172 switchover rules and 24-hour fuel reserve requirements. Cummins logged a double-digit increase in European data-center orders in 2024, with its 3,500 kVA QSK95 emerging as a preferred platform. Equipment is increasingly specified for both standby and peak-shaving roles, lifting average runtime and driving demand for low-NOx gas units. Healthcare buyers favor units with remote diagnostics to support preventive maintenance and ISO 22301 business continuity audits.

Spain's solar and transport build-out, Poland's rail overhaul, and Italy's National Recovery and Resilience Plan are stretching project timelines and extending rental contracts for mobile power. The European construction sector generated EUR 1.6 trillion of output in 2024, and portable gensets between 100 kVA and 500 kVA remain essential where sites lack a permanent grid supply. Aggreko expanded its European rental fleet by 12% in 2024, with Stage V-compliant diesel-battery hybrids cutting fuel by 30% during low-load hours. Contractors increasingly demand telemetry-enabled sets to monitor runtime, emissions, and fuel use in real time, embedding gensets into broader site-management dashboards.

Stage V rules, fully effective from 2024, compel diesel gensets above 56 kW to add diesel particulate filters, SCR, and EGR, lifting capital cost by up to 18% and adding EUR 0.02-0.04 /kWh in maintenance for DEF replenishment and filter regeneration. Smaller buyers in the 75 kVA-375 kVA range are deferring replacements or shifting to gas units, evidenced by a 9% drop in diesel orders below 200 kVA at Atlas Copco and a 14% rise in gas and hybrid shipments. Proposed Stage VI limits would tighten NOx thresholds by an additional 30% after 2027, prompting OEMs to adopt ammonia-slip catalysts, which would drive further cost escalation and encourage fuel switching.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The 75 kVA-375 kVA bracket accounted for 34.62% of the European generator sets market share in 2025, supported by standardized enclosures, high-volume production, and competitive pricing. These units back up HVAC, refrigeration, and point-of-sale systems in retail chains and commercial buildings. Growth is flattening as battery storage penetrates small, grid-connected loads, yet replacement demand persists because Stage V compliance mandates newer hardware.

The 750 kVA-2,000 kVA segment is on track for a 6.25% CAGR, propelled by data-center campuses and large-scale manufacturing that implement modular sets in N+1 layouts to achieve uninterrupted power. Cummins' 3,500 kVA QSK95 enables operators to add 1 MW blocks without re-engineering switchgear, reducing installation timelines. Above 2,000 kVA, applications include grid-balancing and island utilities deploying gas or dual-fuel units from Wartsila and Caterpillar. Below 75 kVA, residential and small commercial demand is shrinking as battery-inverter combinations gain favor in regions with outage durations of four hours or less.

Diesel held 52.88% of the 2025 fuel mix, mostly due to a large installed base and universal fuel availability. Stage V costs, urban low-emission zones, and Scope 2 targets are prompting buyers to adopt dual-fuel sets that emit 30% less CO2 and 50% less particulates. Natural-gas units represent roughly 22% of demand, concentrated in pipeline-dense regions such as Germany and the Netherlands, while bio-fuel-ready models remain below 3% but are scaling with HVO supply increases from Neste.

Hydrogen-ready engines from Cummins, Wartsila, and Rolls-Royce entered commercial portfolios in 2024; adoption is still under 1% but is expected to climb once electrolyzer build-outs and pipeline infrastructure mature. Propane, biogas, and landfill-gas engines serve tighter, niche sectors. Diesel's share is forecast to drop below 47.50% by 2031, not due to outright displacement, but rather because of faster growth in gas and hybrid offerings.

The Europe Generator Sets Market Report is Segmented by Capacity (Below 75 KVA, 75 To 375 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Fuel Type (Diesel, Natural Gas, Dual-Fuel and Hybrid, Renewable/Bio-fuel, and Others), Application (Standby Power, Prime/Continuous Power, and More), End-User (Residential, Commercial Buildings, Data Centers, and More), and Geography (Germany, United Kingdom, Spain, and More).