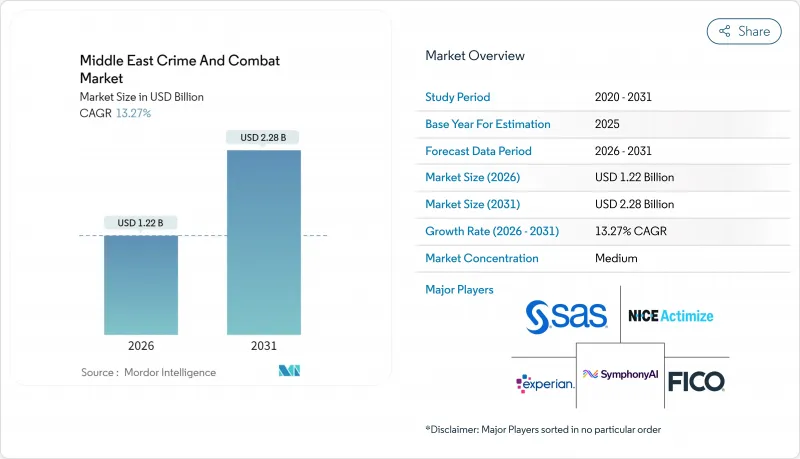

중동 범죄 및 전투 시장 규모는 2026년 12억 2,000만 달러에 이를 것으로 추정됩니다. 이는 2025년 10억 8,000만 달러에서 성장한 수치이며, 2031년에는 22억 8,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에 걸친 연평균 복합 성장률(CAGR)은 13.27%를 나타낼 전망입니다.

이 강력한 확대는 디지털 결제의 이용 증가, 아랍에미리트(UAE)과 사우디아라비아의 전자 KYC(본인 확인)의 의무화, 컴플라이언스 지출을 성장 촉매로 하는 '비전 2030' 연동의 금융 섹터 현대화를 반영하고 있습니다. 거래량 가속화, 지정학적 리스크 증가, 클라우드 도입의 급속한 진전이 함께 실시간 모니터링 툴, AI 구동형 이상 감지, 월경 데이터 공유 허브에 대한 안정적인 수요를 창출하고 있습니다. 경쟁의 심각성은 중간 정도로 유지됩니다. 이는 전문 아랍어 요구사항과 관할 구역별 요구사항이 신규 진입을 막기 때문이며, 지역 전문 기업이 세계 벤더와 공존할 수 있는 환경이 갖추어져 있기 때문입니다. 은행이 확장성이 높은 인프라를 추구하는 동안 클라우드 도입이 주류가 되고 있지만 데이터 주권이 의무화되는 부문에서는 On-Premise 시스템이 여전히 존재합니다. 지역 전체에서 AML(돈세탁 방지), 부정 방지, 테러 자금 대책, 보고 기능을 통합하는 플랫폼에 대한 투자 판단이 증가하고 있어, 벤더의 풋 프린트와 도입 스케줄을 효율화하고 있습니다.

걸프 국가에서는 모바일 결제와 비접촉 결제가 소매 지출의 주류가 되고, 일일 거래 건수는 수백만 건 규모에 달하고 있습니다. 사우디아라비아는 컴플라이언스에 11억 달러를 투자했음에도 불구하고 GDP의 5.74%를 금융 범죄로 잃을 위험이 있으며, 높은 처리량 모니터링 엔진의 필요성이 더욱 높아지고 있습니다. 아랍에미리트(UAE)에서 의무화된 전자 KYC(본인 확인)는 인근 국가도 도입을 진행하는 표준 온보딩 규칙을 확립하고, 본인 확인 시간을 단축함과 동시에 데이터 품질 기준을 인상하고 있습니다. 디지털 거래량 증가는 공격 대상 영역을 확대하고, 특히 합성 신분 사기나 게임 플랫폼을 이용한 자금 세정이 현저합니다. 이렇게 하면 은행은 알고리즘을 분기별로 업데이트해야 합니다. 클라우드 네이티브 툴은 계절적 지출 피크에 맞추어 확대 가능한 탄력적인 처리 능력을 제공해 클라우드 도입의 CAGR이 21.24%를 기록한 이유가 되고 있습니다. AI 스코어링 모델을 통합한 금융기관에서는 오감지율이 2자리 줄어들고 고객 승인 사이클이 대폭 단축되고 있습니다.

걸프 지역의 물류 회랑은 아시아, 유럽, 아프리카 간의 다 통화 거래를 중개하고 무역 기반 자금 세척(TBML)을 체계적인 위험으로 전환하고 있습니다. 은행은 AI 분석을 도입하여 과대·과소청구서의 검출과 세관, 운송 및 결제 데이터의 거의 실시간으로 상관 분석을 실시했습니다. 무역 금융에서 블록체인의 검사 운영은 투명성을 가져오는 반면, 전용 분석 엔진을 필요로 하는 엄청난 데이터 세트도 생성하고 있습니다. 두바이와 리야드에 새롭게 설치된 정보 공유 센터는 위험 신호가 되는 지표를 배포하여 평균 감지 시간을 며칠에서 몇 시간으로 단축했습니다. 규제가 수렴하는 동안 다국어 대응 및 제재 스크리닝 대응 솔루션을 제공할 수 있는 벤더는 가격 프리미엄을 획득하고, 중소 금융기관은 진입 비용 절감을 위해 공유 서비스 모델을 채택하고 있습니다.

규제를 통해 수상한 거래 보고서를 작성하는 것은 아랍어로 의무화되지만, 경험이 풍부한 분석가 인력 풀은 수요를 따라 잡지 못했습니다. 영어만의 직무에 비해 급여 프리미엄이 40% 이상 웃도기 때문에 비용 기반이 부풀어 채택 사이클이 장기화하고 있습니다. 은행은 자동 번역 및 인공지능 요약 기술에 눈을 돌리고 있지만, 규제 당국은 고위험 안건에 대해서는 인간 모니터링을 요구하고 있으며, 병목 현상은 해소되지 않았습니다. 사우디아라비아의 대형 은행은 현재 대학 프로그램을 후원하고 있습니다만, 전문가에 의하면, 졸업생이 안건 처리의 숙련도를 달성하기까지는 3-5년의 성숙 기간이 필요합니다. 아랍어 인터페이스와 현지화된 워크플로우를 통합한 공급업체는 보다 신속한 도입 승인을 얻고 있습니다.

거래 모니터링 솔루션은 2025년 수익의 28.74%를 차지했으며 모든 AML 프로그램의 기반이 되는 규제 대응의 주력인 것이 부각되었습니다. 이 점유율은 중동 범죄 시장 규모에서 약 3억 1,000만 달러에 해당합니다. 클라우드 네이티브 엔진은 지연없이 매일 수백만 건의 마이크로 결제를 선별하여 Tier 1 은행에서 공급업체 잠금을 유지합니다. 사기 감지 및 사례 관리는 14.73%의 연평균 복합 성장률(CAGR)로 가장 급성장하는 부문이며, 합성 신분 정보의 악용과 깊은 가짜를 활용한 자금 세척 네트워크 증가로 혜택을 받고 있습니다. 공급업체는 이전에 분리된 모듈을 통합 제품군에 수렴하여 총 소유 비용을 절감하고 모델 리스크 거버넌스를 용이하게 합니다.

생성형 AI 컴포넌트는 현재 조사 시나리오 초안 작성, SAR 제출 처리 정책 제안, 에스컬레이션의 긴급 순위를 수행합니다. Oracle 에이전트는 경보를 강화하기 위해 타사 데이터베이스를 자율적으로 쿼리하는 진화의 궤적을 보여줍니다. 이스트넷과 같은 지역 진출 기업은 문화적 맥락을 유지하기 위해 아랍어 자연 언어 생성 기능을 통합하여 대응하고 있습니다. 공급업체를 통합한 기관은 모델 검증 감사의 원활화와 통합 오버헤드 감소를 보고합니다.

2025년 시점에서 클라우드 모델은 60.98%의 점유율을 차지하며 중동 범죄 및 전투 대책 시장에서 약 6억 6,000만 달러에 해당합니다. 아랍에미리트(UAE)과 사우디아라비아 규제 당국이 중요한 워크로드 오프프레미스 호스팅을 허가하는 동안 채택률은 CAGR 20.82%로 계속됩니다. SaaS 제공을 통해 중소 핀테크 기업도 엄청난 초기 투자 없이 엔터프라이즈급 분석 기능을 이용할 수 있습니다. 하이브리드 설계는 특정 개인 식별 정보를 국내에 보관하면서 지역 데이터센터에서 탄력적인 분석을 활용해야 하는 은행에 의해 지원됩니다.

On-Premise 도입은 물리적 데이터 분리를 선호하는 주권재부 기금과 방위관련 은행 간에 틈새 시장의 중요성을 유지합니다. 그러나 이러한 이해 관계자조차도 패치 관리주기를 줄이기 위해 컨테이너화 된 마이크로 서비스의 검사 운영을 수행하고 있습니다. 공급업체의 로드맵은 데이터 주권 관련 법률을 충족하면서 멀티 테넌트 릴리스와의 업그레이드 주기 무결성을 유지하는 단일 테넌트 클라우드 옵션을 강조합니다.

Middle East crime and combat market size in 2026 is estimated at USD 1.22 billion, growing from 2025 value of USD 1.08 billion with 2031 projections showing USD 2.28 billion, growing at 13.27% CAGR over 2026-2031.

This vigorous expansion reflects rising digital-payments usage, mandatory e-KYC rules in the UAE and Saudi Arabia, and Vision 2030-linked financial-sector modernization that turns compliance spending into a growth catalyst. Transaction-volume acceleration, heightened geopolitical risk, and rapid cloud adoption jointly create steady demand for real-time monitoring tools, AI-driven anomaly detection, and cross-border data-sharing hubs. Competitive intensity stays moderate because specialized Arabic-language and jurisdiction-specific requirements deter new entrants, allowing regional specialists to coexist with global vendors. Cloud deployment dominates as banks pursue scalable infrastructure, yet on-premise systems persist where data-sovereignty mandates apply. Across the region, investment decisions increasingly favor integrated platforms that unify AML, fraud, CTF, and reporting functions, streamlining vendor footprints and implementation timelines.

Mobile and contactless payments now dominate retail spending across the Gulf, pushing daily transaction counts into the multi-million range. Saudi Arabia risks losing 5.74% of GDP to financial crime despite allocating USD 1.10 billion to compliance, reinforcing the need for high-throughput monitoring engines. Mandatory e-KYC in the UAE standardizes onboarding rules that neighboring states are replicating, trimming verification times, and raising baseline data quality. Higher digital volumes enlarge attack surfaces, especially for synthetic-identity fraud and gaming-platform laundering, compelling banks to refresh algorithms quarterly. Cloud-native tools offer elastic processing that scales with seasonal spending peaks, explaining the 21.24% CAGR logged by cloud deployments. Institutions that integrate AI-scoring models report double-digit drops in false positives and materially faster customer-acceptance cycles.

The Gulf's logistics corridors channel multi-currency trade between Asia, Europe, and Africa, turning trade-based money-laundering (TBML) into a systemic risk. Banks deploy AI analytics to flag over- or under-invoices and to correlate customs, shipping, and payment data in near real time. Blockchain pilots in trade finance introduce transparency but also generate vast datasets that require purpose-built analytics engines. Newly formed intelligence-sharing centers in Dubai and Riyadh distribute red-flag indicators, cutting the average detection window from days to hours. As regulations converge, vendors capable of delivering multilingual, sanctions-screening-ready solutions gain a price premium, and smaller institutions adopt shared-service models to lower entry costs.

Regulations require suspicious-activity reports to be prepared in Arabic, yet the talent pool of experienced analysts lags demand. Salary premiums exceed 40% compared with English-only roles, inflating cost bases and prolonging hiring cycles. Banks turn to automated translation and AI summarization, but regulators insist on human oversight for high-risk cases, preserving the bottleneck. Large Saudi banks now sponsor university programs, yet experts note a 3-5-year maturation window before graduates achieve case-handling proficiency. Vendors that embed Arabic interfaces and localized workflows gain faster deployment approvals.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Transaction Monitoring solutions generated 28.74% of 2025 revenue, underscoring their status as the regulatory workhorse anchoring every AML program. That share equates to roughly USD 0.31 billion of the Middle East crime and combat market size. Cloud-native engines that screen millions of daily micro-payments without latency maintain vendor lock-in across Tier-1 banks. Fraud Detection and Case Management, the fastest-growing line at 14.73% CAGR, benefits from rising synthetic-identity abuse and deepfake-enabled mule networks. Vendors are converging these once-separate modules into unified suites, lowering the total cost of ownership and easing model-risk governance.

Generative-AI components now draft investigation narratives, recommend SAR filing dispositions, and rank escalation urgency. Oracle's agents exemplify the trajectory, autonomously querying third-party databases to enrich alerts. Regional players such as EastNets respond by embedding Arabic natural-language generation to preserve cultural context. Institutions that consolidate vendors report smoother model-validation audits and reduced integration overhead.

Cloud models held a 60.98% share in 2025, equivalent to roughly USD 0.66 billion of the Middle East crime and combat market share. Adoption will continue at 20.82% CAGR as regulators in the UAE and Saudi Arabia ratify off-premise hosting for critical workloads. SaaS offerings allow smaller fintechs to access enterprise-grade analytics without large upfront capital outlays. Hybrid designs appeal to banks that must keep certain personally identifiable data on domestic soil yet still harness elastic analytics in regional data centers.

On-premise deployments retain niche relevance among sovereign-wealth entities and defense-linked banks that prioritize physical data segregation. Yet even these stakeholders pilot containerized micro-services to slash patch-management cycles. Vendor roadmaps emphasize single-tenant cloud options that satisfy data-sovereignty statutes while preserving upgrade cadence parity with multi-tenant releases.

The Middle East Crime and Combat Market is Segmented by Solutions (KYC Systems, Compliance Reporting Suites, and More), Deployment Mode (Cloud, On-Premises), End-User Vertical(BFSI, Fintechs and Payment Service Providers, and More), Application (Anti-Money Laundering, Counter-Terrorist Financing, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).