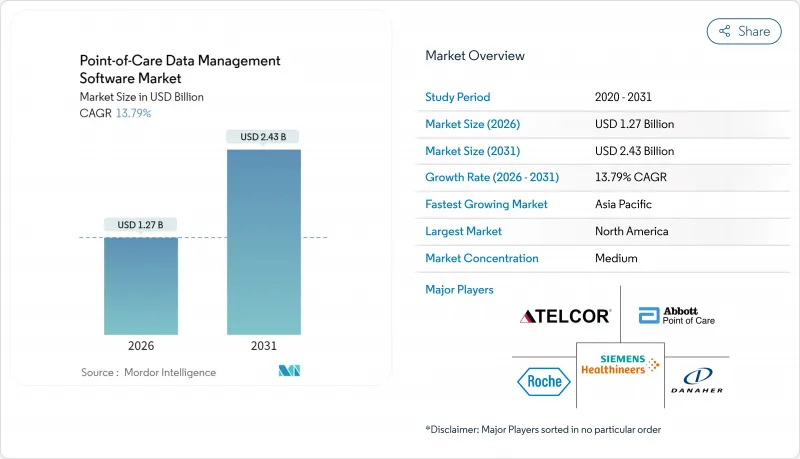

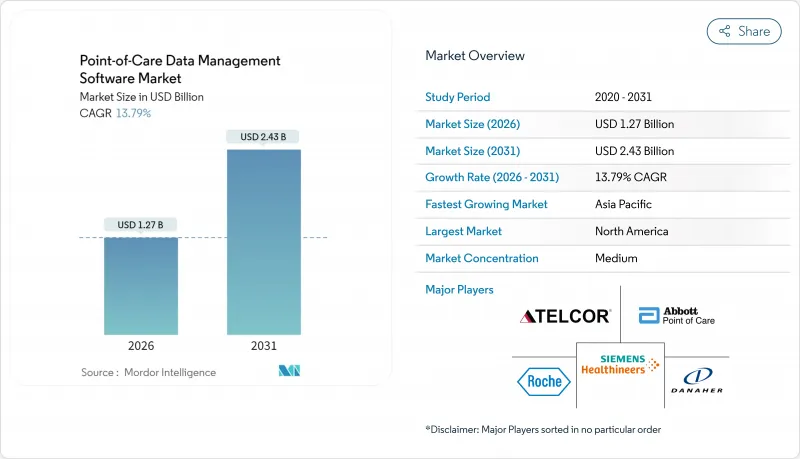

POC 데이터 관리 소프트웨어 시장은 2025년의 11억 2,000만 달러에서 2026년에는 12억 7,000만 달러로 성장하고 2026-2031년에 걸쳐 CAGR 13.79%로 성장을 지속하여, 2031년까지 24억 3,000만 달러에 이를 전망입니다.

이러한 급성장은 의료시스템의 실시간 진단으로의 전환, 유연한 연결성에 대한 정부자금의 확충, 성과연동형 보상제도에 대한 선호 증가에 기인하고 있습니다. 클라우드 마이그레이션, AI 기반 분석, 수백가지 유형의 장치를 함께 사용하는 미들웨어가 현재 주요 구매 기준이 되고 있습니다. 병원이 데이터 워크플로를 표준화하고 재택 치료 프로그램이 확대되는 가운데, 소프트웨어 서비스에 대한 사이버 보안 대책을 통합할 수 있는 벤더가 시장 점유율을 획득할 전망입니다. 대기업과 기존 기업 간의 통합과 틈새 혁신가가 공존하는 가운데 적당한 집중도를 유지한 시장 환경이 형성되어 안정적인 거래 활동이 예상됩니다.

의료 시스템은 CMS의 상호 운용성과 환자 접근성 제도에 의해 추진된 표준화된 FHIR R4 API를 통해 200가지 이상의 다른 POC 장비를 연결하는 상호 운용 가능한 미들웨어를 요구합니다. 각 공급업체는 데이터 사일로화를 피하고 임상 의사결정을 가속화하기 위해 추가 기능이 아닌 핵심 인프라로 연결성을 고려합니다. 5G와 엣지 컴퓨팅 노드의 출현으로 클라우드 네이티브 배포 지연이 줄어들어 여러 시설을 운영하는 사업자는 분산된 시설 간의 워크플로를 조화시킬 수 있게 되었습니다. FDA의 디지털 건강 소프트웨어 사전 인증 프로그램은 규제 심사에 연결성을 통합하여 연결성을 더욱 향상시키고 지속적인 성능 모니터링에 대한 인센티브를 창출합니다. 결과적으로 구매자는 계약을 진행할 때 미들웨어의 깊이와 미래를 예상하는 인터페이스의 로드맵을 선호합니다.

2024년 각국 정부는 의료 인프라 프로젝트에 2,000억 달러를 지출했으며 진료 현장 데이터 관리 소프트웨어를 포함한 디지털 플랫폼에 상당한 자금을 할당했습니다. 인도의 '국가 디지털 헬스 미션'이나 중국의 '건강 중국 2030' 등의 프로그램은 IT 근대화를 위한 예산을 투입해, 각국 고유의 데이터 현지화 제도를 충족하는 벤더에 시장을 개방하고 있습니다. 민관 연계 사업에서는 건설 입찰에 소프트웨어 조항을 통합하는 경우가 많아 부가적 기술이 필수 요소로 전환됩니다. 신설 병원과 진단센터에서는 가치 기반 의료 대시보드에 데이터를 공급하는 분석 제품군을 지정하여 소프트웨어 조달과 시설 건설 일정을 연동하고 있습니다. 이러한 지출 급증은 중소득 국가의 잠재 고객 기반을 확대하고 장기 유지보수 계약을 통해 공급업체의 수익 가시성을 높입니다.

종합적인 도입에는 시설당 50만-200만 달러의 비용이 소요되며, 이는 IT 직무의 40%가 공석인 소규모 및 지방병원에서는 도입의 장벽이 됩니다. 레거시 시스템의 이종 혼재는 인터페이스 코딩이나 워크플로 재설계의 부담을 증대시켜, 예산 사이클을 넘은 공사 기한 연장을 초래하는 경향이 있습니다. 연간 보수비, 직원 연수비, 업그레이드 계약비를 더하면 총소유비용이 더욱 높아집니다. 환자 수가 적은 시설에서는 투자 회수 모델이 여전히 취약하며 따라서 보조금을 통한 자금 조달과 단계적 과금 방식의 SaaS 옵션을 선택하는 경향이 있습니다. 모듈화된 클라우드 호스팅 서비스를 저렴한 가격으로 제공할 수 있는 공급업체는 잠재 수요를 획득하여 CAGR에 대한 이러한 억제요인에 대응할 수 있습니다.

2025년에도 온프레미스 도입은 매출의 51.62%를 차지했으며, 데이터 관리를 자사 서버에서 직접 수행하는 과거의 경향이 나타났습니다. 그러나 강력한 재해 복구 기능, 자동 패치 적용, 확장 가능한 스토리지 등의 이점을 바탕으로 클라우드 솔루션은 15.88%의 연평균 복합 성장률(CAGR)로 급성장하고 있습니다. 하이브리드 접근법은 마이그레이션의 가교 역할을 합니다. 많은 시스템은 대기 시간에 민감한 모듈을 현장에 유지하면서 분석 프로세스를 HIPAA 호환 클라우드로 마이그레이션합니다. 여러 거점을 보유한 체인 기업은 캠퍼스 간 성능 지표를 동기화하는 클라우드 중심 대시보드를 중시하여 중복 인프라를 줄입니다. FDA가 최근 발표한 지침에서는 검증된 클라우드 구성을 로컬 설치와 동등한 것으로 인정하고 있으며 이는 CIO의 우려를 더욱 완화하고 SaaS 모델에 대한 발주를 뒷받침하고 있습니다. 하드웨어 업데이트의 연기로 인한 절약분은 종종 사이버 보안 강화를 위해 투입되어 전환 곡선을 가속화합니다.

클라우드 벤더는 연방 정부와 학술 기관으로부터의 계약 획득을 위해 FedRAMP와 HITRUST 인증을 내세우며 기존 온프레미스 벤더의 선행 우위를 흡수하고 있습니다. 랜섬웨어의 위협 증가도 오프사이트 백업을 필요로 하며, 이는 많은 클라우드 계약에서 표준 기능이 되고 있습니다. 한편, 유전체 데이터를 다루는 연구 기관은 계산 처리량을 극대화하기 위해 여전히 로컬 클러스터에 의존하고 있습니다. 그러나 여기에서도 컨테이너화된 워크로드를 통해 수요 피크 시에는 클라우드에서 버스트 용량을 확보할 수 있으며, 이는 경계선이 모호한 하이브리드 아키텍처가 주류가 되는 미래상을 보여주고 있습니다. 시간이 지남에 따라 서비스 기반 가격 체계는 공급업체의 초점을 영구 라이선스에서 AI 모듈 및 API 시장을 풍부하게 갖춘 고객 유지 중심의 로드맵으로 전환하여 생태계 참여 수익 창출을 촉진합니다.

2025년에도 병원과 집중치료 부문은 46.15%라는 압도적인 점유율을 유지했습니다. 이는 응급 부문의 처리량 목표와 검사 결과의 신속한 제공 의무에 의해 뒷받침됩니다. 그러나, 재택 치료 프로그램은 14.71%의 연평균 복합 성장률(CAGR)을 기록하고 있으며, 메디케어의 재택 병원 서비스 확충이나 고령화 사회의 동향에 의해 추진되고 있습니다. 휴대용 분석기와 원격 의료 키트가 보급됨에 따라 간병인이 환자의 집에서 접속할 수 있는 경량 브라우저 기반 대시보드에 대한 수요가 증가하고 있습니다. 진단센터는 검체처리량의 급증에 대응하기 위해 자동검증제도을 통합하고, 클리닉에서는 정액 지불제도 하에서의 진찰주기 단축을 위해 POC 데이터를 활용하고 있습니다.

재택 관리 사업자는 불안정한 광대역 품질에 직면하면서 연결 회복시 동기화되는 '스토어 앤 포워드' 아키텍처에 대한 관심을 높이고 있습니다. 병원은 품질 관리의 편차를 감지하고 시약 재고 데이터를 통합하는 전사적 미들웨어에 대한 투자를 지속하여 공급망 효율을 향상시키고 있습니다. 외래 클리닉에서는 공유 서비스 모델을 도입하고, 집중형 분석 기능을 라이선싱하면서 현지의 기기 풀 관리는 자율적으로 유지하고 있습니다. 그리고 장기 요양 시설 및 산업 보건 시설을 포함한 '기타' 카테고리의 확대에 따라 병원 외 워크플로에 특화한 모듈형 UI 스킨에 대한 수요가 높아지면서 수익 기회가 확대되고 있습니다.

북미는 2025년에 38.21%의 점유율을 유지했으며 이는 NIH 보조금, BARDA의 DRIVe 프로그램, 성숙한 EHR 보급이 기반이 되고 있습니다. 미국 병원은 메디케어 어드밴티지의 품질 지표 달성을 위한 분석 도구를 도입하는 반면 캐나다 주립 시스템은 미들웨어 상호 운용성을 기반으로 한 지방의 접근성 향상에 자금을 투입하고 있습니다. 벤처 캐피탈의 유입과 예측 가능한 FDA 승인 프로세스를 통해 지역은 AI 집약형 모듈의 시험장이 되어 공급업체에게 조기 피드백 루프를 제공합니다.

아시아태평양은 세계에서 가장 높은 16.52%의 연평균 복합 성장률(CAGR)을 보일 것으로 전망됩니다. 중국의 150억 달러 규모 의료 디지털화 예산은 클라우드 기반 대시보드를 열망하는 공립 병원에 투입되고 있습니다. 인도의 "아유슈만 바라트 디지털 미션"은 상호 운용성을 의무화하여 구매자를 표준 준수 소프트웨어로 유도하고 있습니다. 일본은 Society 5.0을 활용해 재택 모니터링 키트와 집중 분석을 조합한 노인 케어 파일럿 사업을 뒷받침하고 있습니다. 싱가포르는 지역 전개의 거점으로서 기능해 동남아시아 전역에 전문 지식을 수출하고 있습니다. 다양한 규제 환경은 유연한 데이터 주권 전환 기능과 다국어 인터페이스를 갖춘 플랫폼을 높이 평가하고 있습니다.

유럽에서는 규제 주도에 의한 꾸준한 보급이 진행되고 있습니다. 독일의 디지털 의료법은 병원 IT의 쇄신을 재정적으로 뒷받침하고 영국의 NHS 디지털 캠페인은 전급성기 병원을 공통 상호 운용성 기준으로 이행시키고 있습니다. 프랑스와 스페인은 EU 부흥 기금을 활용하여 원격 의료 및 검사실 IT의 현대화를 추진 중입니다. 엄격한 GDPR(EU 개인정보보호규정) 제도는 내재형 동의 관리 및 암호화를 요구하고 배포주기를 연장하여 신뢰성을 높입니다. 컴플라이언스 템플릿을 사전에 검증한 공급업체는 입찰에서 이점을 얻습니다. 남미, 중동, 아프리카는 점유율이 뒤떨어지고 있지만, 민관 연계에 의한 인프라 정비가 시작부터 디지털 키트를 규정하고 있기 때문에 15%대 중반의 성장률을 나타내고 있습니다.

The point-of-care data management software market is expected to grow from USD 1.12 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 2.43 billion by 2031 at 13.79% CAGR over 2026-2031.

This brisk expansion springs from health systems' pivot toward real-time diagnostics, wider government funding for flexible connectivity, and a rising preference for outcome-based reimbursement. Cloud migration, AI-driven analytics, and middleware that links hundreds of device types are now central buying criteria. Vendors able to bundle software, services, and cybersecurity safeguards stand to capture share as hospitals standardize data workflows and home-care programs scale. Consolidation among large incumbents coexists with niche innovators, creating a moderate-concentration landscape poised for steady deal activity.

Health systems are demanding interoperable middleware that links more than 200 distinct point-of-care devices through standardized FHIR R4 APIs, a capability spurred by CMS's Interoperability and Patient Access Rule. Vendors now treat connectivity as core infrastructure, not add-on code, to avoid data silos and accelerate clinical decision-making. The arrival of 5G and edge-computing nodes cuts latency for cloud-native deployments, letting multi-site operators harmonize workflows across dispersed facilities. FDA's Digital Health Software Precertification Program further elevates connectivity by embedding it in regulatory review, creating an incentive for continuous performance monitoring. As a result, buyers prioritize middleware depth and future-proof interface roadmaps when awarding contracts.

Governments spent USD 200 billion on health-infrastructure projects in 2024, earmarking sizable funds for digital platforms that include point-of-care data management software. Programs like India's National Digital Health Mission and China's Healthy China 2030 channel budget toward IT modernization, opening doors for vendors able to meet country-specific data-localization rules. Private-public partnerships often bundle software clauses into construction tenders, effectively converting optional tech into mandatory kit. As new hospitals and diagnostic centers go live, they specify analytics suites that feed value-based care dashboards, ensuring software procurement aligns with bricks-and-mortar schedules. This spends surge enlarges the addressable base in mid-income economies and smooths revenue visibility for suppliers through long-term maintenance deals.

Comprehensive rollouts cost USD 500,000-USD 2 million per facility, a hurdle that stalls adoption in smaller or rural hospitals where 40% of IT posts sit vacant. Legacy-system heterogeneity inflates interface coding and workflow redesign, often stretching timelines past budget cycles. Total cost of ownership widens when annual maintenance, staff training, and upgrade subscriptions enter the calculus. For facilities with thin patient volumes, payback models remain weak, nudging them toward grant funding or SaaS options with phased billing. Vendors able to package modular, cloud-hosted offerings at lower entry prices can unlock pent-up demand and counter this drag on CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

On-premises deployments still commanded 51.62% revenue in 2025, showing the historical sway of in-house servers for direct data custody. Yet cloud solutions are sprinting at a 15.88% CAGR, fuelled by robust disaster-recovery, auto-patching, and elastic storage benefits. A hybrid approach acts as a transition bridge: many systems keep latency-sensitive modules on-site while pushing analytics to HIPAA-compliant clouds. Multi-site chains prize cloud-centric dashboards that synchronize performance metrics across campuses, trimming duplicated infrastructure. FDA's recent guidance equating validated cloud configurations with local installations further eases CIO concerns, nudging purchase orders toward SaaS models. Savings from hardware refresh deferral often finance cybersecurity upgrades, accelerating the migration curve.

Cloud vendors tout FedRAMP and HITRUST credentials to win federal and academic accounts, denting the head-start enjoyed by legacy on-premises incumbents. Rising ransomware threats also make off-site backups imperative, a default feature in many cloud contracts. Conversely, research institutes handling genomic data still lean on local clusters to maximize compute throughput. Even here, containerized workloads permit burst capacity in the cloud during peak demand, showcasing a future where line-blurring hybrid architectures dominate. Over time, service-based pricing shifts vendor focus from perpetual licenses to retention-driven roadmaps rich in AI modules and API marketplaces that monetize ecosystem participation.

Hospitals and critical-care units retained the lion's 46.15% share in 2025, supported by emergency-department throughput targets and lab turnaround mandates. Nevertheless, home-health programs are clocking a 14.71% CAGR, buoyed by Medicare's Hospital-at-Home expansion and aging-population dynamics. Portable analyzers and telehealth kits feed a need for lightweight, browser-based dashboards that caregiver's access from patient residences. Diagnostic centers integrate auto-verification rules to handle ballooning specimen loads while clinics lean on point-of-care data to shorten visit cycles under capitated payment plans.

Home-care operators grapple with variable broadband quality, propelling interest in store-and-forward architecture that syncs when connectivity resumes. Hospitals continue to invest in enterprise-wide middleware that flags quality-control drifts and consolidates reagent inventory data, improving supply chain efficiency. Outpatient clinics adopt shared-service models, licensing centralized analytics but maintaining autonomy over local device pools. The growing "other" category spanning long-term care and occupational-health sites creates opportunities for modular UI skins tailored to non-hospital workflows, widening addressable revenue.

The Point-Of-Care Data Management Software Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End User (Hospitals/Critical Care Units, Diagnostic Centers, Clinics/Outpatient, Home Healthcare, and More), Application (Infectious Disease Devices, Glucose Monitoring, and More), Component (Software Platform, and Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America maintained a 38.21% share in 2025, anchored by NIH grants, BARDA's DRIVe program, and mature EHR penetration. U.S. hospitals deploy analytics to satisfy Medicare Advantage quality metrics, whereas Canada's provincial systems fund rural-access upgrades that hinge on middleware interoperability. Venture capital flows and predictable FDA pathways make the region a test bed for AI-rich modules, giving suppliers early feedback loops.

Asia Pacific is set to compound at 16.52% CAGR, the fastest worldwide. China's USD 15 billion health-digitization budget funnels into county-level hospitals eager for cloud-hosted dashboards. India's Ayushman Bharat Digital Mission enforces interoperability, nudging buyers toward standards-compliant software. Japan leverages Society 5.0 to back aging-care pilots that marry home-monitoring kits with centralized analytics. Singapore acts as the regional deployment hub, exporting expertise across Southeast Asia. The mosaic of regulations rewards platforms sporting flexible data-sovereignty toggles and multilingual interfaces.

Europe exhibits steady, regulation-driven uptake. Germany's Digital Healthcare Act finances hospital IT overhauls, while the United Kingdom's NHS Digital campaign pushes all acute trusts onto a shared interoperability standard. France and Spain tap EU Recovery funds for telemedicine and lab IT modernization. Strict GDPR rules require baked-in consent management and encryption, extending deployment cycles but enhancing trust. Suppliers that pre-validate compliance templates gain bidding advantages. South America, the Middle East, and Africa trail in share but post mid-teens growth as public-private buildouts stipulates digital kits from the outset.