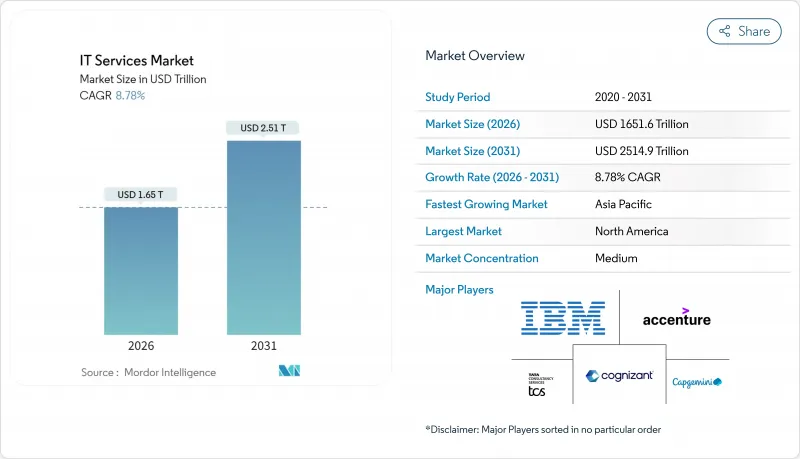

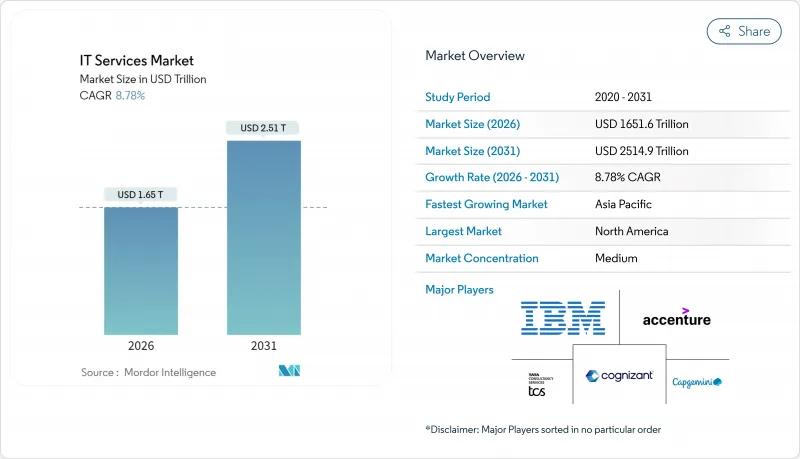

2026년 IT 서비스 시장의 규모는 1조 6,516억 달러로 추정되며, 2025년 1조 5,181억 달러에서 성장할 전망입니다.

2031년에는 2조 5,149억 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 8.78%로 확대될 전망입니다.

견고한 디지털 전환 계획, 기업의 인공지능 도입 증가, 클라우드 네이티브 마이그레이션 확대가 잠재적 수요를 확대하고 있습니다. 지출의 기세가 가장 강한 부문은 은행업과 의료 분야이며, 2024년에는 각 기관이 레거시 코어 시스템의 근대화를 진행하는 가운데 지출이 각각 8.7% 및 15% 증가했습니다. 하이브리드 클라우드 및 AI 워크로드를 기반으로 하는 컨설팅, 배포 및 관리 서비스를 종합적으로 제공할 수 있는 공급업체는 고부가가치 계약을 획득합니다. 한편, 가격에 민감한 아웃소싱 계약은 대규모 납품 파이프라인의 기반으로 계속 중요한 역할을 유지하고 있습니다. 수십억 달러 규모의 인수를 포함한 통합의 움직임이 활발해지고 있는 점은 규모, 수직 통합의 깊이, 지적 재산의 차별화가 기업용 계약의 업그레이드 획득에 있어서 결정적인 요소가 되고 있음을 나타냅니다.

멀티클라우드 배포는 기업의 87%를 넘어서고, 51%가 애플리케이션 리팩토링, AI 서비스, 데이터 플랫폼을 통합한 클라우드 네이티브 현대화 프로젝트에 자금을 투입하고 있습니다. 세계의 IT 서비스 시장에서는 단순한 리프트 앤 시프트 마이그레이션이 아닌 컨테이너 오케스트레이션, 마이크로서비스 및 DevOps를 보유한 공급자를 높이 평가하게 되었습니다. DXC 기술의 'Cloud Right' 접근 방식으로 오션 네트워크 익스프레스는 다운타임 제로 전환을 실현하고 공급업체가 인프라 관리에서 전략적 비즈니스 파트너로 진화하는 방법을 보여주었습니다. 수익원은 높은 기술 자격과 업계 인사이트를 모두 요구하는 권고 및 관리형 클라우드 운영 계층으로 전환하고 있습니다. 이러한 계약은 일반적으로 공유 서비스 수준 성과를 중심으로 구성되어 공급자의 고객 정착률과 단위 경제성을 향상시킵니다. Kubernetes, 사이트 신뢰성 엔지니어링 및 FinOps의 기술 부족은 서비스 요금을 더욱 밀어 올리고 있으며 클라우드 퍼스트 프로그램이 장기 성장에 가장 큰 플러스 효과를 가져오는 이유를 뒷받침합니다.

워크로드의 이식성과 규정 준수를 추구하는 기업을 통해 세계의 클라우드 ERP 지출은 2022년에서 2027년에 걸쳐 거의 두 배가 될 전망입니다. 유럽의 기업은 2025년에 4,898억 유로(5,535억 달러)를 IT 서비스에 투입했으며, 그 45%가 클라우드 이니셔티브에 할당되었습니다. 멀티클라우드 전략은 벤더 종속 회피에 기여하지만 거버넌스의 복잡성을 초래하여 컨설팅 및 최적화 서비스에 대한 수요를 유발합니다. 데이터 주권 요건으로 지역 특화형 호스팅 기반의 필요성이 높아지고, 니어쇼어 및 온쇼어 계약이 확대되고 있습니다. 공인 클라우드 아키텍트 및 매니지드 FinOps 인력을 제공하는 공급자는 IT 서비스 시장 전반에 걸쳐 높은 수익 계약을 획득합니다.

자동화와 해외 규모의 확장으로 인해 일반적인 고객센터 업무 및 인프라 작업 진입 장벽이 사라지고 기존 아웃소싱 이익률이 압축됩니다. 고객은 성과 연동형 과금 방식을 점점 더 요구하고 있으며, 공급업체는 구체적인 비즈니스의 영향을 증명할 수밖에 없습니다. 소규모 경쟁업체가 가격을 낮추면서 프리미엄 컨설팅과 보안 서비스를 교차 판매할 수 있는 기존 기업 간의 통합이 가속화되고 있습니다. 이로 인해 발생하는 도태에 의해 향후 2년간 IT 서비스 시장 내 경쟁 질서가 재편될 전망입니다.

매니지드 보안 서비스는 CAGR 12.18%로 확대되었으며 IT 서비스 시장 전반에서 가장 높은 성장률을 보이고 있습니다. 기업은 위협 감지 및 사고 대응에서 전문 공급자가 내부 팀을 능가한다는 것을 인식하고 지속적인 컴플라이언스 모니터링을 포함한 장기 아웃소싱 계약을 체결하는 경향이 있습니다. IT 아웃소싱은 정착된 비용 최적화 요청으로 여전히 가장 높은 28.04%의 점유율을 유지하고 있습니다. 그러나 상품화된 비즈니스 흐름에서 수익률을 축소하면 공급업체가 아웃소싱 및 컨설팅을 패키징하고 가격 설정을 보호할 수 있습니다. 클라우드 및 플랫폼 서비스는 하이브리드 클라우드 배포 급증의 혜택을 누리고 있습니다. 프로젝트는 ERP의 현대화와 데이터 통합 레이어를 자주 결합하여 교차 판매의 기세를 지원합니다.

수요 동향은 비즈니스 프로세스 아웃소싱에도 유리하게 작용하고, 특히 재무, 인사 및 업계 특화형 백오피스 업무에서는 로봇 프로세스 자동화에 의한 효율화 효과가 현저히 높습니다. IT 컨설팅 수익은 복잡성 증대에 따라 확대되고 있습니다. 조직은 AI, 엣지 컴퓨팅, 수직 클라우드의 통합에 지침이 필요합니다. 레퍼런스 아키텍처, 마이그레이션 가속화 툴킷 및 도메인 전문 솔루션을 제공하는 공급업체는 IT 서비스 시장 전반에 걸쳐 고객의 지출 점유율을 확대하고 있습니다.

중소기업 시장은 2031년까지 연평균 복합 성장률(CAGR) 10.92%를 기록할 전망이며 클라우드 제공 ERP, CRM, 사이버 보안 통합 솔루션에 대한 민주화된 접근을 반영합니다. 종량 과금제에 의해 중소기업도 종래에는 대기업만이 이용할 수 있었던 기능을 도입할 수 있게 되어, 도입 기간이 수개월에서 수주로 단축됩니다. 의료 및 금융 서비스 분야의 컴플라이언스 부담은 중소기업이 사내 통제 체계를 구축하기보다 외부 전문가의 활용을 촉구하여 매니지드 서비스 파트너의 대응 가능 수익을 확대합니다.

대기업 시장은 여전히 수익의 69.42%를 차지하고 있습니다. 이는 장기적인 혁신 로드맵이 필요한 광범위한 레거시 자산에 의해 지원됩니다. 사내의 전문센터와 외부 전문 지식을 융합한 하이브리드 모델이 주류가 되며 틈새 프로바이더에 있어서 고가치 계약의 획득 기회를 만들어 내고 있습니다. 기업 바이어는 RFP에서 지속가능성 인증 및 탄소 보고서 대응력을 점차 요구하는 경향이 있으며, IT 서비스 시장 전체에서 스코프 3 배출량을 추적하는 공급자에게 차별화의 길이 열리고 있습니다.

북미는 2025년 수익의 37.05%를 차지했으며 2조 7,000억 달러 규모의 기업용 기술 지출과 AI 및 클라우드 플랫폼의 조기 도입 추세가 이를 견인하고 있습니다. AI 거버넌스 위원회의 설치를 의무화하는 연방 정부의 지침에 의해 전략적 자문 및 도입 서비스에 대한 수요가 제도화되었습니다. 캐나다는 디지털 정부 프로그램과 천연 자원의 자동화를 추진하는 한편, 멕시코의 니어쇼어 제안은 문화적 친화성과 지적재산 보호를 요구하는 미국 기업을 유치하고 있습니다.

아시아태평양은 2031년까지 11.12%라는 가장 높은 CAGR을 기록할 전망입니다. 중국은 스마트시티 파일럿 사업과 그린 제조의 고도화를 추진하고, 인도는 배송거점으로서의 전통을 살리면서 국내 수요를 확대하며, ASEAN 국가들은 크로스보더 EC와 핀테크 성장을 지원하기 위해 인프라 격차 해소에 임하고 있습니다. 일본과 한국은 첨단 제조 및 통신 분야에 대한 투자를 집중시켜 5G와 엣지 컴퓨팅에 관한 전문 컨설팅을 촉진하고 있습니다. 호주 및 뉴질랜드는 IT 지출이 성숙했음에도 불구하고 은행과 정부 기관에서 사이버 보안과 클라우드 규정 준수를 지속적으로 선호하고 있습니다.

유럽에서는 2025년에 4,898억 유로(5,535억 달러)가 IT 서비스에 배분되었으며, 그 중 45%가 클라우드 프로그램에 할당되었습니다. GDPR(EU 개인정보보호규정), DORA, NIS2와 같은 규제 프레임워크는 보안 및 컴플라이언스 지출을 촉진하고 적합한 공급자에게 안정적인 기회 파이프라인을 보장합니다. 독일은 제조업의 디지털화를 주도하고 영국은 금융 서비스 변혁을 견인하며, 프랑스, 이탈리아, 스페인에서는 클라우드 ERP의 도입이 확대됩니다. 동유럽은 니어쇼어 제공 거점으로, 또한 근대화 서비스 수요처로 발전하여 IT 서비스 시장 전체의 생태계를 강화합니다.

IT services market size in 2026 is estimated at USD 1651.6 billion, growing from 2025 value of USD 1518.1 billion with 2031 projections showing USD 2514.9 billion, growing at 8.78% CAGR over 2026-2031.

Robust digital-transformation agendas, an upswing in enterprise artificial-intelligence adoption, and rising cloud-native migrations are expanding addressable demand. Spending momentum is strongest in banking and healthcare, where 2024 outlays jumped 8.7% and 15% respectively as institutions modernized legacy cores. Providers able to bundle consulting, implementation, and managed services around hybrid-cloud and AI workloads capture premium contracts, while price-sensitive outsourcing engagements continue to anchor large-scale delivery pipelines. Heightened consolidation-including multibillion-dollar acquisitions-shows that scale, vertical depth, and intellectual-property differentiation are now decisive in winning enterprise renewals.

Multi-cloud adoption has crossed 87% of enterprises, while 51% are funding cloud-native modernization tracks that bundle application refactoring, AI services and data platforms. The Global IT services market now rewards providers that master container orchestration, micro-services and DevOps over simple lift-and-shift migration. DXC Technology's "Cloud Right" approach enabled Ocean Network Express to achieve zero-downtime migration, showcasing how vendors move from infrastructure caretakers to strategic business partners. Revenue pools are shifting toward advisory and managed cloud operations layers that demand both deep technical credentials and sector insight. These engagements, typically structured around shared service-level outcomes, lift provider stickiness and unit economics. Skills scarcity in Kubernetes, site reliability engineering and FinOps is further buoying service rates, underscoring why cloud-first programmes add the highest positive delta to long-run growth.

Global cloud-ERP outlays are on track to nearly double between 2022 and 2027 as enterprises pursue workload portability and regulatory compliance. European firms directed EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, with 45% tagged for cloud initiatives. Multi-cloud strategies help organizations avert vendor lock-in, yet they impose governance complexity that drives demand for advisory and optimization services. Data sovereignty mandates heighten the need for region-specific hosting footprints, bolstering nearshore and onshore engagements. Providers offering certified cloud architects and managed FinOps talent are capturing high-margin contracts across the IT services market.

Automation and offshore scale have erased entry barriers for common help-desk and infrastructure tasks, compressing margins in traditional outsourcing. Clients increasingly demand outcome-based billing, compelling vendors to prove tangible business impact. Smaller rivals undercut pricing, which accelerates consolidation among incumbents able to cross-sell premium consulting and security offerings. The resulting shake-out is likely to realign the competitive order within the IT services market over the next two years.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Managed Security Services is growing at a 12.18% CAGR, the steepest rate across the IT services market. Enterprises accept that specialized providers outperform internal teams in threat detection and incident response, prompting long-term outsourcing contracts that include continuous compliance monitoring. IT Outsourcing retains the largest 28.04% revenue position due to entrenched cost-optimization mandates. However, margin compression in commoditized workstreams is pushing vendors to package outsourcing with consulting to protect pricing. Cloud and Platform Services benefit from surging hybrid-cloud adoption; projects frequently bundle ERP modernization with data-integration layers, supporting cross-selling momentum.

Demand dynamics also favor Business Process Outsourcing, especially in finance, HR, and industry-specific back-office workflows where robotic process automation amplifies efficiency gains. IT Consulting revenues rise on complexity: organizations need guidance to harmonize AI, edge computing, and vertical clouds. Vendors that deliver reference architectures, accelerated migration toolkits, and domain-centric solutions increase wallet share across the IT services market.

Small and Medium Enterprises register an 10.92% CAGR through 2031, reflecting democratized access to cloud-delivered ERP, CRM, and cybersecurity bundles. Consumption-based pricing allows SMEs to deploy capabilities historically reserved for large corporations, compressing deployment timelines from months to weeks. Compliance burdens in healthcare and financial services incentivize SMEs to engage external specialists rather than build in-house controls, expanding addressable revenue for managed-service partners.

Large Enterprises still command 69.42% revenue, underpinned by sprawling legacy estates that demand long-duration transformation roadmaps. Hybrid models blending internal centers of excellence with targeted external expertise prevail, securing high-value contracts for niche providers. Enterprise buyers increasingly list sustainability credentials and carbon-reporting readiness in RFPs, offering differentiation avenues for providers that track Scope-3 emissions across the IT services market.

The IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, and More), End-User Enterprise Size (Small and Medium Enterprises, and More), Deployment Model (Onshore, Nearshore, and More), End-User Vertical (BFSI, Manufacturing, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America represents 37.05% of 2025 revenue, steered by USD 2.7 trillion in enterprise tech spending and early-adopter behavior toward AI and cloud platforms. Federal mandates requiring AI governance boards have institutionalized demand for strategic advisory and implementation services. Canada advances digital-government programs and natural-resource automation, whereas Mexico's nearshore proposition attracts U.S. firms seeking cultural affinity and IP protection.

Asia-Pacific records the highest 11.12% CAGR through 2031. China scales smart-city pilots and green-manufacturing upgrades, India leverages its delivery-hub heritage while expanding domestic demand, and ASEAN economies close infrastructure gaps to support cross-border e-commerce and fintech growth. Japan and South Korea funnel investments into advanced manufacturing and telecom, spurring niche consulting around 5G and edge computing. Australia and New Zealand, despite mature IT spend, continue prioritizing cybersecurity and cloud compliance in banking and government.

Europe allocates EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, 45% of which funds cloud programs. Regulatory frameworks-GDPR, DORA, and NIS2-propel security and compliance spend, ensuring consistent engagement pipelines for qualified providers. Germany spearheads manufacturing digitization, the United Kingdom leads in financial services transformation, and France, Italy, and Spain scale cloud-ERP rollouts. Eastern Europe develops as both a nearshore delivery basin and a consumer of modernization services, strengthening ecosystem depth across the IT services market.