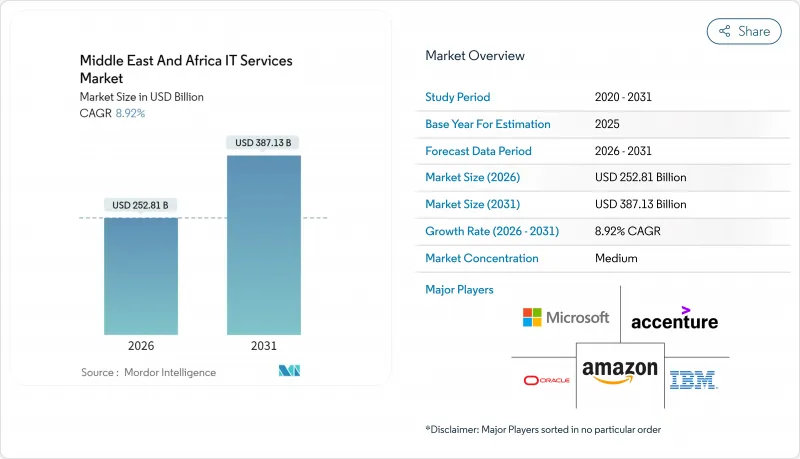

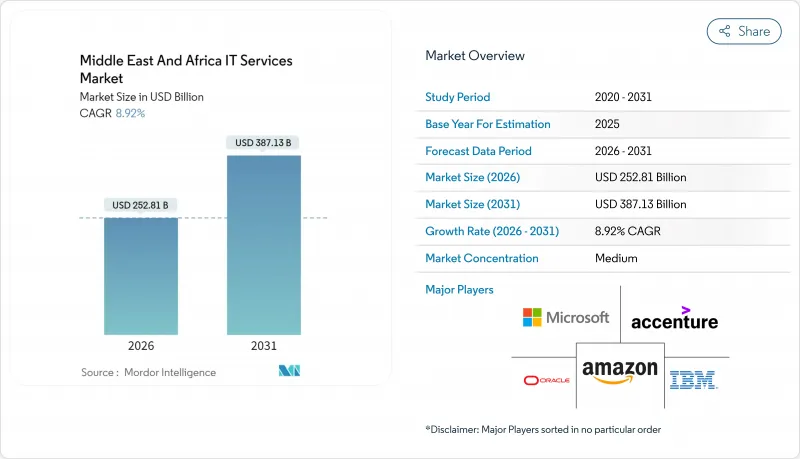

중동 및 아프리카의 IT 서비스 시장은 2025년에 2,321억 달러로 평가되었고, 2026년 2,528억 1,000만 달러에서 2031년까지 3,871억 3,000만 달러에 이를 것으로 예측되고 있으며, 예측기간(2026년부터 2031년)의 CAGR은 8.92%로 전망됩니다.

정부가 주도하는 디지털화 프로그램의 가속화, 국부펀드에 의한 기술 도입의 의무화, 5G의 보급으로 걸프협력회의(GCC) 회원국 및 아프리카의 주요 경제권에서 기업의 IT 지출 패턴이 변화하고 있습니다. 클라우드 도입 증가, 하이퍼스케일 데이터센터에 대한 투자 급증, 지역 전반의 핀테크 붐은 컨설팅, 도입, 관리 서비스에 대한 수요를 높이고 있습니다. 반면, 2개국에서 클라우드 네이티브 전문가가 만성적으로 부족하고 국경을 넘어서는 데이터에 관한 법률이 단편화되어 성장 전망은 희박하며 공급자는 제공 모델과 컴플라이언스 전략의 개선을 요구받고 있습니다. 세계의 통합업체는 규모와 기술의 깊이를 활용하고 지역 전문가들은 지역화 요구사항과 아랍어 능력을 활용하기 때문에 경쟁 역학은 균형을 유지하고 있습니다.

사우디아라비아의 디지털 정부 정책은 248억 달러의 인프라 자금과 전국적인 5G 커버리지를 배경으로 2030년까지 공공 서비스의 90%를 클라우드로 마이그레이션하는 것을 목표로 하고 있습니다. UAE와 카타르에서도 비슷한 정책이 추진되고 있으며 대규모 통합, 사이버 보안 및 관리 서비스 지원이 필요하기 때문에 기존 아웃소싱에서 클라우드 네이티브 서비스 제공으로 수요 변화가 진행되고 있습니다. 민간 기업도 경쟁력을 유지하기 위해 이러한 공공 부문의 벤치마크를 모방하고 있으며, 하이브리드 클라우드 컨설팅과 플랫폼 서비스의 지속적인 도입을 촉진하고 있습니다.

사우디아라비아의 210억 달러 규모 데이터센터 건설 계획과 마이크로소프트, 블랙록, 테마섹이 주도하는 300억 달러 규모 지역 AI 인프라 협력이 현지 호스팅 경제를 변화시키고 있습니다. 지역의 신규 이용 가능 용량은 데이터 거주지 규정을 충족하고 지연에 민감한 워크로드를 지원하며 기존의 코로케이션 서비스보다 높은 서비스 마진을 제공하는 엣지 컴퓨팅 이용을 가능하게 합니다.

남아프리카는 세계 3위의 IT 인재 해외 유출지역이며, 전 구인건수의 2%가 국제적인 포지션을 차지하면서 현지 인재 기반을 소모시키고 있습니다. GCC 프로젝트는 아랍어와 영어에 능통한 전문가를 요구하기 때문에 인력 부족이 더욱 심각해지고 있으며, 공급자는 외국인 고용이나 분산형 해양 팀에 의존할 수밖에 없으며, 그 결과 제공 비용과 납기가 증가하고 있습니다.

2025년 시점에서 중동 및 아프리카의 IT 서비스 시장에서 34.83%의 점유율을 차지하였지만, 클라우드 및 플랫폼 서비스는 CAGR 10.72%로 확대될 것으로 전망되고 있으며 이는 기업이 AI 대응 아키텍처로 이행하고 있는 것을 반영하고 있습니다. 기존 아웃소싱은 레거시 워크로드에서 여전히 중요성을 유지하지만 클라우드 네이티브 서비스의 성숙과 함께 가격 압력에 직면하고 있습니다. 중요 인프라 전반에서 사이버 리스크가 심각해짐에 따라 매니지드 보안 서비스의 중동 및 아프리카의 IT 서비스 시장 내 규모가 확대되고 있습니다. AWS, Microsoft 및 Oracle을 통한 지역 하이퍼스케일 확장을 통해 공급업체는 실시간 분석 및 IoT 오케스트레이션과 같은 부가가치 서비스를 추가하여 낮은 마진의 인프라에 대한 지원을 대체합니다.

기업에 의한 핵심 용도의 재플랫폼화와 엣지 컴퓨팅 이용 사례를 통한 네트워크 재구축이 진행되고 있는 가운데, 컨설팅 및 도입 지원에 대한 수요는 견조하게 추이하고 있습니다. 비즈니스 프로세스 아웃소싱(BPO)은 문서 관리 및 민원 서비스 기능에 대해 공공 부문에서 안정적인 수요를 유지하고 있습니다. 컨설팅, 마이그레이션 지원 및 장기 관리 서비스를 패키징하는 공급업체는 고객과의 지속적인 관계를 구축하여 상품화 위험을 완화합니다.

2025년 지출액에서 대기업이 차지한 비율은 67.55%였지만, GCC 국가에서의 보조 클라우드 바우처와 기술 지원 제도의 뒷받침으로 중소기업(SME)은 10.18%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 전망되고 있습니다. 400억 달러 규모의 정부 자금이 중소기업의 디지털화 지원에 충당되어 ERP, CRM, 전자상거래 플랫폼 진입 장벽이 낮아지고 있습니다. 따라서 중동 및 아프리카에서 표준화된 SaaS 도입으로 IT 서비스 시장의 규모는 급격히 확대되고 있습니다.

대기업은 AI, 예지보전, 멀티클라우드 거버넌스 프로젝트에 대해 수년간 수백만 달러 규모의 계약을 지속적으로 체결하고 있습니다. 그러나 가격 감응도가 높아지면서 성과 연동형 계약의 도입이 진행되고 있습니다. 하이터치형 대기업 프로젝트와 자동화된 중소기업 업무에 대해 딜리버리 팀을 구분하는 공급자는 자원 활용률과 이익률을 최적화합니다.

The Middle East and Africa IT services market was valued at USD 232.1 billion in 2025 and estimated to grow from USD 252.81 billion in 2026 to reach USD 387.13 billion by 2031, at a CAGR of 8.92% during the forecast period (2026-2031).

Accelerated government-backed digitization programs, sovereign-wealth-fund technology mandates, and widespread 5G coverage are reshaping enterprise IT spending patterns across the Gulf Cooperation Council (GCC) and key African economies. Rising cloud adoption, surging hyperscale data-center investments, and a region-wide fintech boom are intensifying demand for consultative, implementation, and managed-service offerings. Meanwhile, chronic shortages of bilingual cloud-native professionals and fragmented cross-border data laws temper growth prospects, prompting providers to refine delivery models and compliance strategies. Competitive dynamics remain balanced as global integrators leverage scale and technology depth while regional specialists capitalize on localization requirements and Arabic language capabilities.

Saudi Arabia's digital-government policy targets 90% cloud migration of public services by 2030, backed by USD 24.8 billion in infrastructure funding and nationwide 5G coverage. Comparable agendas in the UAE and Qatar require extensive integration, cybersecurity, and managed-service support, shifting demand from legacy outsourcing toward cloud-native delivery. Private enterprises mirror these public-sector benchmarks to sustain competitive parity, driving sustained uptake of hybrid-cloud consulting and platform services.

Saudi Arabia's USD 21 billion data-center pipeline and a USD 30 billion regional AI-infrastructure alliance anchored by Microsoft, BlackRock, and Temasek are transforming local hosting economics. Newly available in-region capacity satisfies data-residency statutes, supports latency-sensitive workloads, and enables edge-computing use cases that command higher service margins than traditional colocation offerings.

South Africa ranks third worldwide for outbound IT-talent recruitment, and 2% of all posted roles are international, draining local capacity. GCC projects intensify shortages by requiring Arabic-English fluent professionals, forcing providers to rely on expatriate hires or distributed offshore teams that increase delivery costs and timelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The segment accounted for 34.83% of the Middle East and Africa IT services market share in 2025, yet cloud and platform services are set to grow at 10.72% CAGR, reflecting enterprises' pivot toward AI-ready architectures. Traditional outsourcing retains relevance for legacy workloads but faces pricing pressure as cloud-native offerings mature. The Middle East and Africa IT services market size attributed to managed security services is expanding as cyber-risk escalates across critical infrastructure. Regional hyperscale expansions by AWS, Microsoft, and Oracle allow providers to layer value-added services such as real-time analytics and IoT orchestration, displacing low-margin infrastructure support.

Demand for consulting and implementation remains robust as enterprises re-platform core applications and re-architect networks for edge-computing use cases. Business-process outsourcing maintains steady public-sector demand for document-management and citizen-service functions. Providers that bundle consulting, migration, and long-term managed services create sticky client relationships, mitigating commoditization risk.

Large enterprises represented 67.55% of 2025 spend, but SMEs are forecast to post a 10.18% CAGR, buoyed by subsidized cloud vouchers and technical-support schemes across GCC economies. Government funds worth USD 40 billion are earmarked for SME digital-enablement, lower entry barriers to ERP, CRM, and e-commerce platforms. The Middle East and Africa IT services market size for standardized SaaS onboarding is therefore rising sharply.

Large enterprises continue to award multi-year, multi-million-dollar contracts for AI, predictive maintenance, and multi-cloud governance projects. However, price sensitivity has increased, prompting outcome-based contracts. Providers that segment delivery teams for high-touch enterprise projects and automated SME engagements optimize utilization and margin.

The Middle East and Africa IT Services Market is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, and More), End-User Enterprise Size (Small and Medium Enterprises and Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), Deployment Model (Onshore Delivery, Nearshore Delivery, and Offshore Delivery), and Country. The Market Forecasts are Provided in Terms of Value (USD).