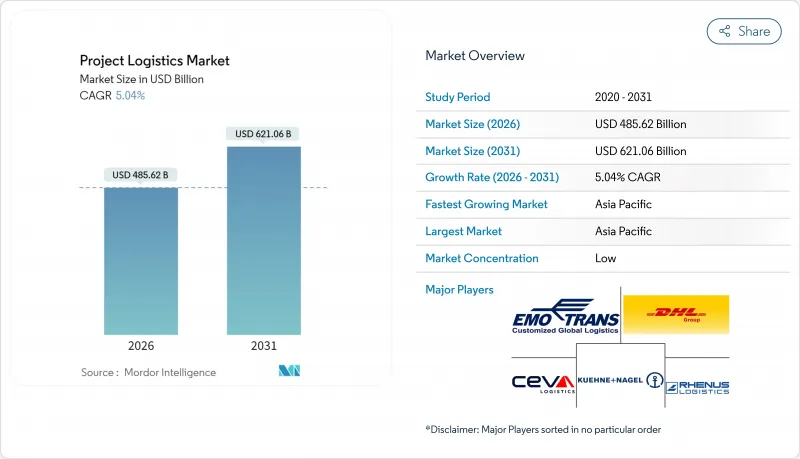

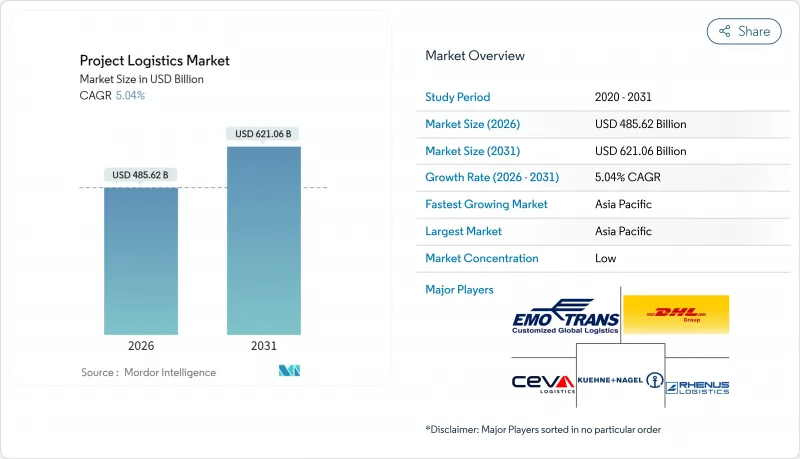

프로젝트 물류 시장의 규모는 2026년 4,856억 2,000만 달러로 추정되고 있으며, 2025년 4,623억 달러에서 성장할 것으로 전망됩니다.

2031년에는 6,210억 6,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.04%로 확대될 전망입니다.

신재생에너지 설비 증강, 신흥경제국에서 인프라 투자의 동시다발적 확대, 유라시아 횡단철도 회랑의 성숙화에 의해 서비스 범위가 확대됨과 동시에 운송 1건당 가치도 향상하고 있습니다. 중규모 LNG 터미널, 수소 파이프라인 전환, 모듈식 건설 프로젝트로 평균 부품 크기가 확대되어 특수 선박, 자주식 모듈 수송기, 온도 관리형 저장 시설에 대한 수요가 높아지고 있습니다. 동시에 AI를 활용한 루트 최적화 플랫폼은 엔드 투 엔드 비용을 10-15% 절감하여 납기를 단축함으로써 사업자는 제한된 자산을 보다 신속하게 재배치할 수 있게 되었습니다. 지역 전문업체와 기술 주도 신규 진출기업에 의한 경쟁 격화가 중견 기업의 통합을 가속화하고 있지만, 단독 사업자의 점유율이 8%를 초과하지 않기 때문에 시장 집중도는 여전히 낮은 수준입니다. 화물 운임 변동, 중량물 하역 작업자 부족, 만성 항만 혼잡 등의 지속적인 과제로 인해 운송 사업자는 디지털 시각화 도구, 멀티모달 허브, 시뮬레이션 훈련 프로그램에 대한 투자를 추진하고 있습니다.

해상 풍력 발전소와 그린 수소 회랑이 운송의 청사진을 다시 그리고 있습니다. 터빈 블레이드는 현재 100미터를 넘어 15-20MW 터빈용으로 설계된 잭업선이 필요합니다. 벤처 글로벌사의 플라커민즈 LNG 터미널 3단계 확장 프로젝트(총 180억 달러)는 구성 부품의 규모 확대를 상징하는 한편 독일에서 400킬로미터의 천연가스 파이프라인을 수소 수송용으로 전환하는 움직임은 -253°C 이하로 유지해야 하는 새로운 극저온화물의 등장을 보여줍니다. 이러한 변화에 대응하기 위해, 사업자는 루트 계획, 선박 선정, 재고 배치의 재검토를 요구받고 있습니다.

중국의 '일대일로' 구상은 100억 달러 규모의 동아프리카 항만 계획과 운송 시간을 최대 50% 단축하는 철도망의 정비를 촉구했습니다. 동시에 국제 트랜스카스피해 운송 루트는 2024년에 27,000 TEU를 운송하여 전년 대비 25배의 비약적 성장을 이루었습니다. 프로젝트 물류 시장은 수십년에 걸친 예측 가능한 자본 파이프라인의 혜택을 받아 선대의 확대와 지역 저장소의 확장을 정당화하는 기반이 되고 있습니다.

1,000톤의 크롤러 크레인은 5,000만-1억 달러이며 풍력발전설비 설치선은 2억 달러를 넘는 비용이 듭니다. 이러한 거액 투자가 신규 진입을 막아 지역 전문업자의 고비용 장비 리스를 강화하기 때문에 프로젝트량이 증가해도 이익률의 향상이 억제되고 있습니다.

2025년 시점에서 프로젝트 물류 시장의 60.45%를 차지한 운송 부문은 특대화물에 대한 항로 설계, 중량물 운반선, 호위선의 필수적인 역할을 반영하고 있습니다. 창고 보관과 유통 및 재고 관리는 규모는 작지만, CAGR 5.18%로 가장 급속하게 확대하고 있는 분야입니다. 이 성장은 온도 관리된 임시 창고와 동기화된 스테이징을 필요로 하는 모듈식 건설의 증가를 반영합니다. 창고 보관 서비스의 프로젝트 물류 시장 내 규모는 통합 제공업체가 보관 및 라스트마일 조립을 설정함에 따라 확장이 예상됩니다. 자동 재고 관리 시스템을 도입하는 사업자는 부품의 체류 시간을 시각화할 수 있어 유휴 자본이나 지연 위약금을 억제할 수 있습니다.

서비스 내용의 다양화에 따라 현지 물류 조정, 통관 업무, 리스크 자문에 대한 수요도 높아지고 있습니다. 하이랜드 페어뷰사의 메가 물류센터는 원스톱 모델을 구현하여 복잡한 화물 흐름에 대응하는 4,000만 평방 피트의 시설을 제공합니다. 자산 소유자가 제조에서 설치까지의 책임을 외부로 위탁하는 가운데 프로젝트 물류 업계는 운송 중심의 계약에서 성과 중시의 파트너십으로 전환하여 고객 정착률과 수수료 수입 가능성을 높이고 있습니다.

프로젝트 물류 시장의 보고서는 서비스별(운송, 창고 보관, 유통 및 재고 관리, 기타 서비스), 화물 유형별(특대화물, 중량물, 개품산적화물, 기타), 최종 사용자별(석유 및 가스, 발전 및 송전, 건설 및 인프라 기타), 지역별(북미, 남미, 아시아태평양, 유럽, 중동 및 아프리카)로 구분되며 시장 예측은 금액 기준(달러)으로 제공됩니다.

아시아태평양은 중국의 '일대일로'를 따르는 항만, 인도의 고속도로망, 호주의 재생가능 광물자원의 급증에 힘입어 세계 수익의 38.60%를 차지하고 있습니다. 트랜스카스피해 항로의 취급량이 2024년에 27,000TEU로 25배로 급증한 사실은 수에즈 운하에 대한 의존도를 줄이는 대체 회랑의 중요성을 돋보이게 하고 있습니다. 지역 정부는 내륙 창고 및 디지털 통관 창구에 자금을 제공하여 운송업체가 자산의 회전을 가속화하고 체선료를 줄일 수 있습니다.

북미는 2위로 큰 시장이며 멕시코 걸프의 LNG 설비 확충, 40GW 규모의 재생에너지 파이프라인, 2025년 말 개통한 64억 달러 규모의 고디 하우 국제대교 등의 회랑 정비가 견인하고 있습니다. 캐나다의 북극 무역 회랑은 허드슨만 철도 개보수로 수송 시간을 단축하고 중요한 광물 수출 경로를 제공합니다. 허가절차의 개혁에 의해 스케줄의 확실성이 향상되어 물류기업이 장기 계약을 체결하는 뒷받침이 되고 있습니다.

유럽, 중동 및 아프리카는 성숙한 운송 경로와 신흥 경로의 모자이크 형태로 구성되어 있습니다. 독일의 400km 수소 파이프라인 전환은 새로운 화물 카테고리를 개척하고, 이집트의 항만 확장과 사우디아라비아의 랜드브리지 계획은 해안 중기 크레인 수요를 가속화하고 있습니다. 탄자니아의 바가모요항을 포함한 중국이 지원하는 동아프리카 항만은 무역 루트의 재편을 촉구하고 지역 전문업자에 의한 피더 서비스 설립을 유치하고 있습니다. 남미의 광업 회랑과 재생에너지 계획은 리스크 대응 능력이 있는 사업자에게 보상하는 선구적 기회를 개척하고 있습니다.

Project logistics market size in 2026 is estimated at USD 485.62 billion, growing from 2025 value of USD 462.30 billion with 2031 projections showing USD 621.06 billion, growing at 5.04% CAGR over 2026-2031.

Capacity additions in renewable energy, synchronized infrastructure super-cycles in emerging economies, and the maturation of trans-Eurasian rail corridors are broadening service scope while lifting value per shipment. Mid-scale LNG terminals, hydrogen pipeline conversions, and modular construction projects are enlarging average component dimensions, boosting demand for specialized vessels, self-propelled modular transporters, and climate-controlled storage. In parallel, AI-enabled route-optimization platforms are trimming end-to-end costs by 10-15% and shortening delivery windows, allowing operators to redeploy scarce assets faster. Heightened competition, driven by regional specialists and technology-first entrants, is accelerating consolidation among mid-tier firms, yet market concentration remains low because no single provider exceeds 8% share. Persistent headwinds volatile freight rates, certified heavy-lift labor shortages, and chronic port congestion are pushing carriers to invest in digital visibility tools, multi-modal hubs, and simulation-based training programs.

Offshore wind farms and green-hydrogen corridors are rewriting transport blueprints. Turbine blades now surpass 100 meters, necessitating jack-up vessels designed for 15-20 MW turbines. Venture Global's USD 18 billion phase-three expansion at Plaquemines LNG embodies the boom in component scale, while Germany's conversion of 400 kilometers of natural-gas pipeline to hydrogen service signals a new class of cryogenic cargo that must be kept below -253 °C. These shifts require operators to recalibrate route planning, vessel selection, and inventory staging.

China's Belt and Road Initiative has spawned a USD 10 billion East-African port program and rail links that cut transit times by up to 50%. Simultaneously, the Trans-Caspian International Transport Route moved 27,000 TEU in 2024, a 25-fold jump over the prior year. The project logistics market benefits from this predictable, multi-decade capital pipeline that justifies fleet expansion and regional depot build-outs.

A 1,000-tonne crawler crane can cost USD 50-100 million, and wind-installation vessels exceed USD 200 million. These sums deter new entrants and force regional specialists to lease gear at premiums, curbing margin upside even as project volumes rise.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Transportation captured 60.45% of the project logistics market in 2025, reflecting the indispensable role of route engineering, heavy-lift vessels, and escorts for oversized cargo. Warehousing, distribution, and inventory management, though smaller, is the fastest-expanding slice at a 5.18% CAGR. The uptick mirrors modular builds that need climate-controlled laydown yards and synchronized staging. The project logistics market size for warehousing services is set to climb as integrated providers bundle storage with last-mile assembly. Operators deploying automated inventory systems gain visibility over component dwell times, curbing idle capital and penalties.

A wider service mix also elevates demand for on-site logistics coordination, customs brokerage, and risk advisory. Highland Fairview's logistics megacenter embodies this one-stop model, offering 40 million square feet tailored for complex cargo streams. As asset owners outsource cradle-to-installation responsibility, the project logistics industry pivots from move-centric contracts to outcome-driven partnerships, raising stickiness and fee potential.

The Project Logistics Market Report is Segmented by Service (Transportation, Warehousing, Distribution & Inventory Management, Other Services), Cargo Type (Oversized, Heavy-Lift, Breakbulk, Others), End-User (Oil & Gas, Energy Generation/Transmission, Construction and Infrastructure, and More), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Asia-Pacific contributes 38.60% of global revenue, supported by China's Belt and Road ports, India's highways, and Australia's renewable-minerals surge. The Trans-Caspian route's 25-fold volume jump to 27 000 TEU in 2024 underscores alternate corridors that reduce reliance on Suez passages. Regional governments fund inland depots and digital customs windows, enabling carriers to rotate assets faster and clip demurrage fees.

North America ranks second, driven by LNG build-outs along the Gulf, 40-GW renewable-energy pipelines, and corridor upgrades such as the USD 6.4 billion Gordie Howe International Bridge that will open in late 2025. Canada's Arctic Trade Corridor advances through Hudson Bay Railway refurbishments that shave transit times and unlock critical-mineral exports. Favorable permitting reforms bolster schedule certainty, encouraging logistics firms to lock in long-term charter commitments.

Europe, the Middle East, and Africa compose a mosaic of mature and emerging lanes. Germany's 400-kilometer hydrogen-pipeline conversion pioneers a new cargo category, while Egypt's port expansions and Saudi Arabia's Landbridge escalate demand for coastal heavy-lift cranes. China-backed East-African ports, including Bagamoyo in Tanzania, redirect trade loops and invite regional specialists to establish feeder services. South America's mining corridor and renewable plans open frontier opportunities that reward risk-ready operators.