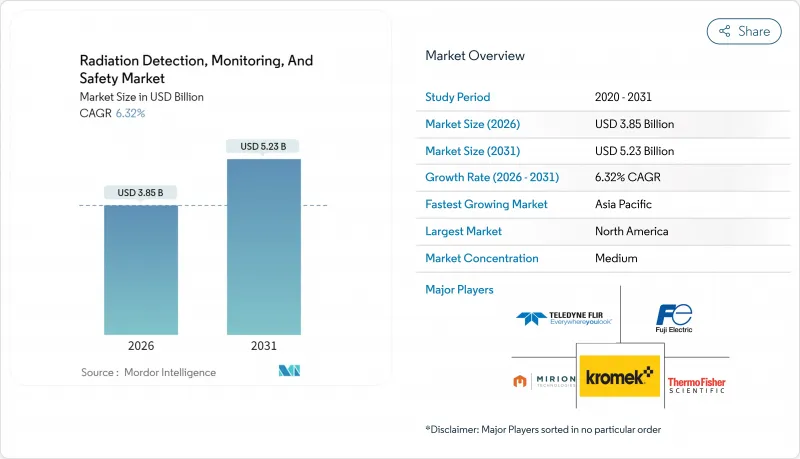

방사선 감지, 모니터링 및 안전 시장 규모는 2026년에는 38억 5,000만 달러로 평가되었고, 2025년 36억 2,000만 달러에서 성장이 예상됩니다.

2031년 예측은 52억 3,000만 달러에 이를 것으로 보이며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 6.32%로 성장할 전망입니다.

핵의학 시술 확대, 지속적인 환경 모니터링에 대한 규제 의무, 반도체 기반 검출기 성능의 급속한 발전이 이러한 성장세를 뒷받침합니다. 강화된 보안 우려는 국경 통제, 응급 대응, 핵심 인프라 부문 전반에 걸친 수요를 증대시키는 한편, 노후화된 원자로 군은 해체 관련 모니터링 구축 필요성을 촉진합니다. 방사선 감지, 모니터링 및 안전 시장은 민간 의료 투자와 국가 안보 지출을 연계하는 이중 활용 가치 제안을 통해 탄력적인 수익 기반을 구축합니다. 북미 유틸리티 기업, 유럽의 원자력 단계적 폐지 프로그램, 아시아태평양 지역의 신규 건설이 합쳐져 기존 감지 플랫폼의 교체 주기를 가속화하고 있습니다. 디지털 연결성, 예측 분석, 클라우드 네이티브 아키텍처는 이제 프리미엄 제품의 차별화 요소로 작용하며, 애프터마켓 소프트웨어 수익과 반복적 서비스 계약을 지원합니다.

2050년까지 전 세계 암 유병률이 3,500만 건으로 증가할 전망이며, 이는 정밀 선량계측 시스템의 잠재적 시장 규모를 확대합니다. 방사선 치료 부서는 이제 서브밀리초 단위의 빔 모니터링 정확도를 요구하며, 선량률의 고주파 변동을 포착하는 반도체 검출기를 선호합니다. 적응형 치료 계획 플랫폼은 데이터 생성량을 증대시키며, 임상의들은 분할 투여량을 조정하기 위해 실시간 피드백 루프에 점점 더 의존하고 있습니다. 이에 따라 의료 시스템은 다중 채널 선량 검증 랙, 중복 필드 교정기, 클라우드 호스팅 선량 등록 소프트웨어에 예산을 편성하며, 이는 방사선 감지, 모니터링 및 안전 시장을 확대하는 생태계를 형성합니다. 공급업체 전략은 선형 가속기 가동 시간을 향상시키는 모듈형 검출기 헤드와 AI 지원 QA 대시보드에 집중하고 있습니다.

핵의학 검사는 액티늄-225 및 루테튬-177과 같은 치료진단용 동위원소의 추진으로 2024년 전년 대비 12% 증가했습니다. 방사성 의약품 허브는 공기 중 알파 입자 모니터, 핫셀 감마 분광계, 시설 LIMS 데이터베이스와 자동 동기화되는 개인용 선량계가 필요합니다. 환자 집단에 더 가까운 분산형 사이클로트론 네트워크는 차폐 캐비닛, 오염 제거 포털, 누출 테스트 키트 등의 조달 노드를 증가시킵니다. 미국 FDA 21 CFR Part 361에 따른 표준화는 동위원소별 교정 프로토콜을 의무화하여 검출기 재교정 서비스 제공업체에게 지속적인 아웃소싱 기회를 보장합니다. 이러한 추세는 ASP(평균 판매 가격)를 상승시키고 애프터마켓 수익 가시성을 확대합니다.

검출기 OEM 업체는 FDA 510(k) 서류 심사를 통과하고, IEC 60601-2-45 성능 지표를 충족하며, CE 마킹 적합성을 획득해야 합니다. 각 단계마다 별도의 생체 적합성, 전자기호환성(EMC), 방사 패턴 테스트가 요구됩니다. 문서 작업만으로도 연구개발 예산이 증가하여 소규모 혁신 기업들은 라이선싱 계약이나 틈새 학술 시장으로 방향을 전환하게 됩니다. 병렬 인증 절차는 현장 배치된 기기가 다국적 영역으로 진입할 때 민첩한 펌웨어 업데이트를 방해하여 기능 출시를 지연시킵니다. 그 결과 설계 승인이 4년을 초과할 수 있는 장기화되어 신기술 투자 순현재가치(NPV)를 희석시키고 방사선 감지, 모니터링 및 안전 시장 내 단기 수익 가속화를 저해합니다.

감지, 모니터링 시스템은 2025년 매출의 50.74%를 차지하며, 지속적인 선량 조건 검증이 필요한 병원, 공공시설, 국방 기관의 조달 예산을 주도했습니다. 방사선 감지, 모니터링 및 안전 시장 규모 내에서 감지 플랫폼은 사전 유지보수 주기를 권고하는 예측 분석 모듈과 함께 성장할 것으로 전망됩니다. 납 방호복, 오염 제거 부스, 자동 격리 도어를 아우르는 안전 장비는 ISO 2919 보호 장치 표준의 조화로 7.55%의 연평균 성장률(CAGR)을 기록하며 기존 기준을 상회하고 있습니다. 실시간 감마선 프로브와 전동 차폐 커튼을 통합한 솔루션은 경보 발생부터 격리 조치까지의 시간을 단축하고 ALARA(합리적으로 달성 가능한 최저 수준) 준수를 개선합니다. 공급업체들은 교차 판매 시너지를 활용합니다. 병원은 신틸레이션 프로브 주문 시 배지 선량계 구독을 추가하는 경우가 많으며, 원자로 운영사는 경계 포털과 대피소 환기 시스템을 묶어 구매합니다. 규제 의무가 조달 시급성을 높여 프리미엄 SKU가 방사선 감지, 모니터링 및 안전 산업 전반에서 꾸준한 수요를 유지함에 따라 가격 탄력성은 여전히 미미합니다.

클라우드 대시보드의 확장된 기능, 지오태깅 경보 시각화, 역할 기반 접근, 자동화된 규정 준수 보고서 생성은 감지 장비를 단순 상품 수준을 넘어섭니다. SaaS 오버레이는 상당한 총마진을 창출하여 하드웨어 수익률을 능가하며 하드웨어 독립적 생태계를 촉진합니다. 결과적으로 채널 파트너들은 단일 감독용 HMI 아래 NaI(Tl), CZT, 중성자 모듈을 통합하는 다중 프로토콜 게이트웨이 재고를 선호합니다. 실시간 분석은 오경보 발생률을 추가로 감소시켜 비용이 많이 드는 대피 사고를 줄입니다. 이러한 부가가치 솔루션은 광범위한 방사선 감지, 모니터링 및 안전 시장 내에서 감지 솔루션의 리더십을 강화합니다.

북미는 2025년에도 30.05%의 매출 선두를 유지했으며, 이는 확고한 원자력 발전 설비, 광범위한 국토 안보 인프라, 그리고 조기 도입 의료 시스템을 반영한 것입니다. 미국 국립 연구소들은 CZT 검출기 소형화에 연구개발 보조금을 집중하고 있으며, 캐나다 NRCan 프레임워크는 연구용 원자로의 환경 모니터링 업그레이드에 보조금을 지원하고 있습니다. 멕시코의 방사성 의약품 수출 확대는 동위원소 생산용 핫셀 모니터의 추가 수요를 창출합니다. ANSI N42 기준에 따른 국경 간 표준화는 장비 상호운용성을 향상시켜 지역 방사선 감지, 모니터링 및 안전 시장 내 규모의 경제를 강화합니다.

아시아태평양 지역은 2060년까지 150기의 원자로 가동을 계획 중인 중국의 추진력에 힘입어 8.05%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장 궤적을 기록하고 있습니다. 중국의 ‘메이드 인 차이나 2025’ 정책에 포함된 현지화 의무는 CZT 웨이퍼 합작 생산 공장을 촉진하여 수입 관세를 낮추고 공급망 취약성을 완화하고 있습니다. 일본의 후쿠시마 사고 이후 규제 체제는 원자로 부지 주변 20km까지 확장된 경계 감마선 감시망을 지원하며, 인도의 원자력부는 2선 도시의 암 치료 병동을 위한 저비용 조사기를 지원합니다. 한국의 확장 중인 18MeV 사이클로트론 네트워크는 대상 병원 수를 더욱 확대하여, 방사선 감지, 모니터링 및 안전 시장의 글로벌 성장 엔진으로서 아시아태평양 지역의 지위를 공고히 하고 있습니다.

유럽은 독일, 벨기에, 스페인의 해체 프로젝트가 공기 중 알파선 모니터 및 폐기물 드럼 분석 시스템에 대한 특수 수요를 창출하며 균형 잡힌 성장을 보이고 있습니다. 원자력 발전 비중이 높은 프랑스는 ASN의 엄격한 지진 위험 기준을 충족해야 하는 수명 연장 업그레이드에 주력합니다. 유라톰 조약은 조달 규격을 표준화하여 다년간 예산 주기를 활용한 국경 간 대량 계약을 가능케 합니다. 구소련 시대 연구용 원자로를 현대화하는 중동부 유럽 국가들은 교육 서비스가 포함된 턴키 방식의 감지 장비 패키지를 찾고 있습니다.

중동 및 아프리카 지역은 초기 단계이지만 전략적 항구에 중성자 화물 스캐너를 배치하고 사이클로트론 기반 방사성 의약품 연구소를 가동 중이며, 이는 신흥 지역에서 방사선 감지, 모니터링 및 안전 시장의 중기적 성장 동력을 예고합니다.

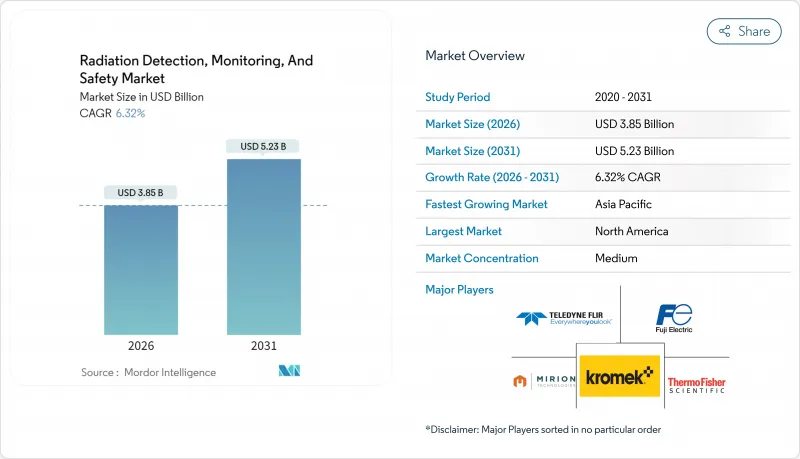

The radiation detection, monitoring, and safety market size in 2026 is estimated at USD 3.85 billion, growing from 2025 value of USD 3.62 billion with 2031 projections showing USD 5.23 billion, growing at 6.32% CAGR over 2026-2031.

The expansion of nuclear-medicine procedures, regulatory mandates for continuous environmental surveillance, and rapid advancements in semiconductor-based detector performance underpin this trajectory. Heightened security concerns reinforce demand across border control, first-responder, and critical infrastructure segments, while aging reactor fleets drive the need for decommissioning-linked monitoring deployments. The radiation detection, monitoring, and safety market benefits from a dual-use value proposition that aligns civilian healthcare investments with national-security spending, creating a resilient revenue base. North American utilities, European nuclear-phase-out programs, and Asia-Pacific build-outs collectively accelerate replacement cycles for legacy detection platforms. Digital connectivity, predictive analytics, and cloud-native architectures now distinguish premium offerings, supporting aftermarket software revenues and recurring service contracts.

Cancer prevalence is climbing toward 35 million global cases by 2050, enlarging the addressable base for precision dosimetry systems.Radiotherapy departments now specify sub-millisecond beam-monitoring accuracy, favoring semiconductor detectors that capture high-frequency fluctuations in dose rate. Adaptive treatment planning platforms amplify data-generation volumes, and clinicians increasingly rely on real-time feedback loops to tune fractionated doses. Health systems, therefore, budget for multi-channel dose-verification racks, redundant field calibrators, and cloud-hosted dose-registry software, an ecosystem that broadens the radiation detection, monitoring, and safety market. Vendor strategies focus on modular detector heads and AI-assisted QA dashboards that enhance linear-accelerator uptime.

Nuclear medicine examinations grew 12% year-over-year in 2024, propelled by theranostic isotopes such as actinium-225 and lutetium-177.Radiopharmaceutical hubs require air-borne alpha-particle monitors, hot-cell gamma spectrometers, and personal dosimeters that auto-synchronize with facility LIMS databases. Decentralized cyclotron networks, positioned closer to patient populations, multiply procurement nodes for shielding cabinets, de-contamination portals, and leak-testing kits. Standardization under U.S. FDA 21 CFR Part 361 obliges isotope-specific calibration protocols, ensuring recurring outsourcing opportunities for detector-recalibration service providers. These trends elevate ASPs (average selling prices) and extend aftermarket revenue visibility.

Detector OEMs must clear FDA 510(k) dossiers, satisfy IEC 60601-2-45 performance metrics, and attain CE marking conformity, each requiring discrete biocompatibility, EMC, and radiation pattern tests. Documentation alone inflates research and development budgets, steering smaller innovators toward licensing deals or niche academic markets. Parallel certification tracks hinder agile firmware updates once fielded devices enter multi-country footprints, slowing feature rollouts. The result is elongated design-win cycles that can exceed four years, diluting NPV on new technology investments and tempering near-term revenue acceleration within the radiation detection, monitoring, and safety market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Detection and monitoring systems generated 50.74% of 2025 revenue, anchoring procurement budgets for hospitals, utilities, and defense agencies that must continuously validate dose conditions. Within the radiation detection, monitoring, and safety market size, detection platforms are projected to grow alongside predictive analytics modules that recommend proactive maintenance intervals. Safety equipment, encompassing lead-lined apparel, decontamination booths, and automated containment doors, is outpacing historical norms with a 7.55% CAGR, buoyed by harmonized ISO 2919 protective device standards. Integrated offerings that unite real-time g-ray probes with motorized shielding curtains shorten alarm-to-containment times and improve ALARA (as low as reasonably achievable) compliance. Vendors leverage cross-selling synergies: hospitals ordering scintillation probes often append badge-dosimetry subscriptions, while reactor operators bundle perimeter portals with shelter-in-place ventilation systems. Price elasticity remains modest, as regulatory obligations heighten procurement urgency, ensuring premium SKUs maintain a steady pull-through across the radiation detection, monitoring, and safety industry.

The expanded functionality of cloud dashboards, geo-tagged alarm visualization, role-based access, and automated compliance report generation pushes detection gear beyond commodity status. SaaS overlays carry significant gross margin, outstripping hardware rates and encouraging hardware-agnostic ecosystems. Consequently, channel partners favor stocking multi-protocol gateways that integrate NaI(Tl), CZT, and neutron modules under one supervisory HMI. Real-time analytics further reduces false-positive occurrences, trimming costly evacuation incidents. Such value-added solutions reinforce the leadership of detection solutions within the broader radiation detection, monitoring, and safety market.

The Radiation Detection, Monitoring and Safety Market Report is Segmented by Product Type (Detection and Monitoring and Safety), Detector Technology (Gas-Filled, Scintillation, and More), End-User Industry (Medical and Healthcare, Energy and Power, Homeland Security and Defence, Industrial, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 30.05% revenue lead in 2025, reflecting entrenched nuclear-power fleets, extensive homeland-security infrastructures, and early-adopter healthcare systems. U.S. national laboratories are funneling research and development grants into CZT detector miniaturization, while the Canadian NRCan framework is subsidizing environmental-monitoring upgrades at research reactors. Mexico's expanding radiopharmaceutical exports add incremental volume for isotope-production hot-cell monitors. Cross-border standardization under ANSI N42 enhances equipment interoperability, thereby reinforcing economies of scale within the regional radiation detection, monitoring, and safety market.

Asia-Pacific records the fastest trajectory at an 8.05% CAGR, underwritten by China's plan to commission 150 reactors before 2060. The localization mandate embedded in Beijing's Made-in-China 2025 policy promotes joint-venture fabrication plants for CZT wafers, reducing import tariffs and mitigating supply-chain fragility. Japan's post-Fukushima regulatory regime finances perimeter gamma-ray meshes extending 20 km around reactor sites, while India's Department of Atomic Energy funds low-cost survey meters for cancer-therapy wards in tier-two cities. South Korea's expanding 18-MeV cyclotron network further widens the addressable hospital count, reinforcing the Asia-Pacific region's status as the global growth engine for the radiation detection, monitoring, and safety market.

Europe exhibits balanced growth as decommissioning projects in Germany, Belgium, and Spain create specialized demand for alpha-in-air monitors and waste-drum assay systems. France, maintaining a strong nuclear-electricity share, focuses on life-extension upgrades that must meet ASN's stringent seismic-risk criteria. The Euratom treaty standardizes procurement specifications, enabling cross-border volume contracts that leverage multi-year budget cycles. Central and Eastern European nations, modernizing Soviet-era research reactors, seek turnkey detection suites bundled with training services.

The Middle East and Africa, although nascent, are deploying neutron-cargo scanners at strategic ports and commissioning cyclotron-based radiopharmacy labs, foreshadowing medium-term momentum for the radiation detection, monitoring, and safety market in emerging geographies.