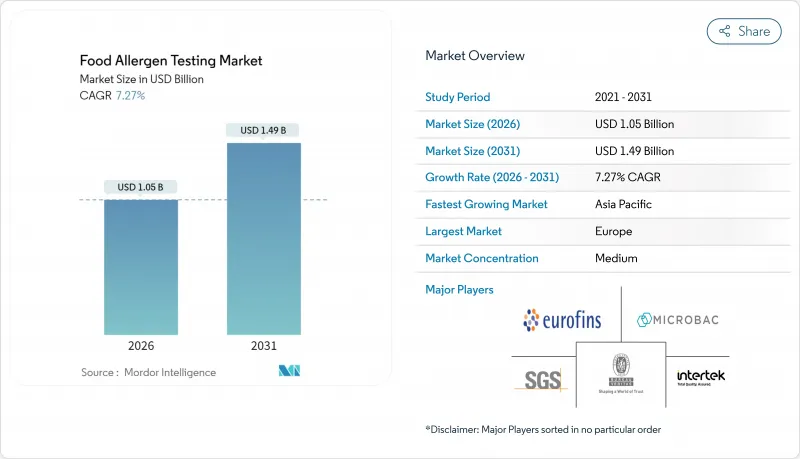

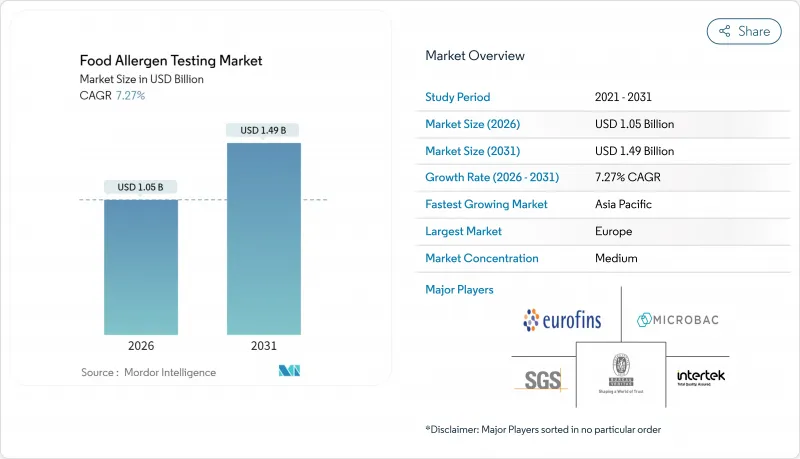

식품 알레르겐 검사 시장은 2025년 9억 8,000만 달러로 평가되었고, 2026년 10억 5,000만 달러에서 2031년까지 14억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 7.27%로 성장이 전망됩니다.

규제 모니터링 강화, 리콜 비용 증가, 통일된 기준 섭취량 규칙의 추진이 성장을 가속시키는 주요 요인입니다. 가공 식품의 월경 거래 증가 및 클린 라벨 제품에 대한 소비자 수요가 어우러져 공급망의 모든 단계에서 검사 범위가 확대되고 있습니다. 기술 도입은 검사 기관이 정량 하한값의 감소를 요구하는 가운데 다중 중합효소 연쇄반응(PCR) 및 질량 분석 플랫폼으로 이행하고 있습니다. 한편, 인공지능 툴은 검사 소요 시간의 단축과 위양성률의 저감을 실현하고 있습니다. 동시에 비싼 장비비용과 다알레르겐 프로토콜의 복잡성은 중소기업의 보급을 억제하고, 수탁검사기관 및 신속 검사 키트 벤더에게 미개척 시장 기회를 창출하고 있습니다.

알레르겐 관련 식품 리콜 빈도와 경제적 영향 증가는 식품 산업 전반에 걸쳐 위험 관리 우선순위를 변화시키고 있습니다. 미신고 알레르겐이 세계적으로 리콜의 주인이 되고 있는 가운데, 영국의 식품 안전 데이터에서는 2024년에 미신고 알레르겐에 의한 리콜이 53건 발생해, 10% 증가한 것이, 교차 오염 관리의 지속적인 과제를 부각하고 있습니다. 2026년 1월 미국 식품의약국(FDA)이 시행할 예정인 식품안전근대화법 섹션 204 추적가능성 요건은 디지털 추적 시스템의 도입을 의무화하여 알레르겐 관리 부족과 관련 법적 책임 위험의 시각화를 촉진합니다. 이 규제 변경으로 제조업체는 사후 대응 리콜 관리가 아닌 예방 검사 프로토콜에 대한 투자를 촉구하고 신속한 알레르겐 스크리닝 기술에 대한 지속적인 수요를 창출하고 있습니다. 위험 완화 및 규제 준수에 대한 우려는 외식 산업에서 특히 두드러집니다. 레스토랑에서는 가정에서의 소비에 이어 알레르기 반응의 발생률이 두 번째로 높아, 사용 현장에서의 검사 솔루션에 시장 기회를 창출하고 있습니다.

주요 시장의 규제 조화는 전통적인 디스플레이 요구 사항을 넘어 제조 공정 및 공급망 검증 프로토콜에 이르는 전례없는 표준화 압력을 생성합니다. 미국 식품의약국(FDA)이 2024년에 발표한 제5판 알레르겐 관리 지침에서는 세척 절차 및 환경 모니터링에 대한 강화된 검증 요건이 도입되었습니다. 한편, 미국 농무부 식품안전검사국(FSIS)은 식육 및 가금 가공업자를 대상으로 한 종합적인 알레르겐 검증 프로그램을 시작했습니다. 네덜란드 식품 소비자 제품 안전청이 개정한 교차 오염방지 가이드라인은 구체적인 검사 빈도 및 분석 방법을 의무화하는 규범적인 제조 기준에 대한 경향을 상징하고 있습니다. 이러한 규제 동향은 관할 구역마다 다른 집행 강도에 대응해야 하는 다국적 식품 기업에 특히 큰 영향을 주고 유럽 시장에서는 가장 엄격한 컴플라이언스 틀이 유지되고 있습니다. 이 규제의 영향은 신흥 시장에도, 수출지향의 제조업자는 고급 시장에 접근하기 위해 국제적인 시험 기준을 채용할 필요가 있으며, 인증 시험 서비스에 대한 수요를 증폭시키는 시너지 효과를 창출하고 있습니다.

고급 알레르겐 검사 플랫폼은 상당한 자본이 필요하며 시장 진입의 큰 장벽이 되었습니다. 이것은 특히 세계 식품 생산 능력의 대부분을 차지하는 중소식품 제조업체에 영향을 미칩니다. 알레르겐 확인 분석을 위한 LC-MS/MS 시스템에는 50만 달러를 넘는 초기 투자가 필요하며, 연간 보수비와 소모품비는 1대당 10만 달러에 달할 전망입니다. 이 재정적 부담은 장비비용에 머무르지 않고 전문 인력 육성, 분석법 검증, 규제 준수를 위한 문서화 등에도 종합적인 알레르겐 검사 능력을 구축하기 위해서는 총액 100만 달러를 넘을 가능성이 있습니다. 이러한 비용 구조로 인해 시장은 양극화되고 있으며, 대규모 다국적 기업은 자체적으로 검사 시설을 유지하고 있지만, 중소 업체는 위탁 검사 서비스에 의존하지 않을 수 없으며 수요가 많을 때 지연이 발생할 수 있습니다. 이 비용 장벽은 신흥 시장에서 특히 두드러지며, 현지 검사 기관은 고급 분석 플랫폼을 도입하는 자금적 여유가 부족한 경우가 많으며, 국제 검사 공급자에 대한 의존과 안전 평가의 소요 시간의 장기화를 초래하고 있습니다.

면역 측정법 기반 기술은 2025년에 57.62%의 압도적인 시장 점유율을 차지했고, 신뢰성, 비용 효율성 및 세계 식품 안전 규정의 수용성으로 인해 57.62%를 차지했습니다. PCR 기반 방법은 높은 특이성과 여러 알레르겐을 동시에 검사할 수 있는 능력에 견인되어 2031년까지 연평균 복합 성장률(CAGR) 8.12%로 성장하고 있습니다. 질량 분석법은 특히 단백질 변형이 면역 측정 성능에 영향을 미치는 가공 식품에서 확인 검사 용도 분야에서 증가하고 있습니다. 분광법 및 이미징 기술은 특정 신속 스크리닝 용도에 활용되고 나노바이오센서 플랫폼은 스마트폰 통합 및 AI 분석을 통해 사용 현장에서 검사를 진화시키고 있습니다.

시장은 기술적 한계를 다루면서 일상 검사의 비용 효과를 유지하기 위해 여러 감지 방법을 통합한 하이브리드 플랫폼으로 전환하고 있습니다. 금 나노입자와 그래핀 기반 변환기를 이용한 첨단 바이오센서 기술은 펨토몰 수준의 검출 한계를 달성하여 기존 ELISA의 감도를 넘어 종래 검출 불가능했던 미량 알레르겐 오염의 검출을 가능하게 하고 있습니다. 그러나 신규 기술에 대한 규제 검증은 여전히 큰 과제이며, ISO 16140-2를 준수하기 위해서는 광범위한 검증 연구가 필요하며 일반적으로 시장 출시까지의 기간을 2-3년 연장하게 됩니다.

유럽은 2025년에 34.21%라는 압도적인 시장 점유율을 차지했으며, 정부 연구소와 민간 서비스 제공업체에 걸쳐 확립된 검사 인프라 및 종합적인 규제 프레임워크가 이를 지원하고 있습니다. 유럽 식품안전기관에 의한 알레르겐 평가 가이드라인의 정기적인 갱신 및 네덜란드 식품 소비자 제품 안전청의 교차 오염 방지 기준은 검사 수요를 지속시키는 이 지역의 엄격한 규제환경을 나타냅니다. 아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.86%로 가장 높은 성장률을 기록하고 있으며, 이 성장은 중국과 인도가 식품 수출 확대를 위해 국제 기준에 정합시키는 규제의 진화에 기인하고 있습니다. 일본의 식품 알레르기 유병률 배증은 인구 동태의 변화가 시장 성장을 견인하고 있음을 보여주며, 한국과 호주는 다국적 식품 기업에 있어 주요 검사 거점이 되고 있습니다.

북미는 확립된 FDA(미국 식품의약국) 및 USDA(미국 농무부)의 규제 프레임워크 하에서 운영되고 있으며, 시장 성장은 주로 규제의 확대가 아니라 기술 진보에 의해 견인되고 있습니다. 이 지역은 고급 검사 프로토콜과 인프라를 유지하면서 새로운 알레르겐 검출 기술 및 조사 방법에 적응을 계속하고 있습니다. 확립된 규제 환경은 시장 운영의 안정적인 기반을 제공하지만, 초점은 근본적인 규제 변경보다 최적화와 효율성 향상으로 전환하고 있습니다.

남미, 중동 및 아프리카에는 규제 정비 및 수출 시장 요건을 통한 성장 기회가 존재합니다. 그러나 현지 분석 능력의 한계와 국제 검사 기관에 대한 의존이 시장 발전을 제한하고 있습니다. 시장 분포는 규제의 진전과 시장 성장의 관계를 반영하고 있으며, 각 지역이 국내 식품 안전성과 국제 무역 경쟁력을 높이기 위해 검사 능력에 대한 투자를 추진하고 있습니다. 이러한 신흥 시장에서는 식품 안전 기준에 대한 인식이 높아지고 있으며, 국제 요건을 충족하기 위해 점검 인프라를 점차 정비하고 있습니다.

The food allergen testing market was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.05 billion in 2026 to reach USD 1.49 billion by 2031, at a CAGR of 7.27% during the forecast period (2026-2031).

Intensifying regulatory scrutiny, rising recall costs, and the push for harmonized reference-dose rules are the foremost forces accelerating growth. Heightened cross-border trade in processed foods, coupled with consumer demand for clean-label products, is broadening the testing footprint across every supply-chain tier. Technology adoption is shifting toward multiplex Polymerase Chain Reaction and mass-spectrometry platforms as laboratories seek lower limits of quantification, while artificial-intelligence tools shorten turnaround times and reduce false positives. At the same time, high instrument costs and the complexity of multi-allergen protocols restrain penetration among smaller manufacturers, creating white-space opportunities for contract laboratories and rapid test-kit vendors.

The increasing frequency and financial impact of allergen-related food recalls is transforming risk management priorities across the food industry, as undeclared allergens remain the primary cause of recalls globally. United Kingdom food safety data showed 53 cases of undeclared allergen recalls in 2024, a 10% increase that highlights the ongoing challenge of cross-contamination control. The FDA's implementation of Food Safety Modernization Act Section 204 traceability requirements, taking effect in January 2026, requires digital tracking systems that will increase the visibility of allergen control failures and associated liability exposure. This regulatory change is driving manufacturers to invest in preventive testing protocols instead of reactive recall management, generating consistent demand for rapid allergen screening technologies. Risk mitigation and regulatory compliance concerns are especially significant in the foodservice sector, where restaurants experience the second-highest incidence of allergic reactions after home consumption, creating market opportunities for point-of-use testing solutions.

Regulatory harmonization across major markets is creating unprecedented standardization pressure that extends beyond traditional labeling requirements to encompass manufacturing processes and supply chain verification protocols. The FDA's release of Edition 5 guidance for allergen controls in 2024 introduced enhanced validation requirements for cleaning procedures and environmental monitoring, while the United States Department of Agriculture's Food Safety and Inspection Service launched a comprehensive allergen verification program targeting meat and poultry processors. The Dutch Food and Consumer Product Safety Authority's updated cross-contact prevention guidelines exemplify the trend toward prescriptive manufacturing standards that mandate specific testing frequencies and analytical methods. These regulatory developments are particularly impactful for multinational food companies that must navigate varying enforcement intensities across jurisdictions, with European markets maintaining the most stringent compliance frameworks. The regulatory influence extends to emerging markets where export-oriented manufacturers must adopt international testing standards to access premium markets, creating a multiplier effect that amplifies demand for accredited testing services.

The high capital requirements for advanced allergen testing platforms create significant barriers to market entry, particularly affecting small and medium-sized food manufacturers that constitute the majority of global food production capacity. LC-MS/MS systems for confirmatory allergen analysis require initial investments exceeding USD 500,000, with annual maintenance and consumable costs reaching USD 100,000 per instrument. The financial burden extends beyond equipment costs to include specialized personnel training, method validation, and regulatory compliance documentation, which can collectively exceed USD 1 million for comprehensive allergen testing capabilities. This cost structure has created a divided market where large multinational corporations maintain in-house testing facilities while smaller manufacturers depend on contract testing services, potentially causing delays during peak demand periods. The cost barrier is especially significant in emerging markets, where local laboratories often lack the financial resources for advanced analytical platforms, resulting in dependence on international testing providers and longer turnaround times for safety assessments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Immunoassay-based technologies hold a dominant 57.62% market share in 2025, due to their reliability, cost-effectiveness, and acceptance within global food safety regulations. PCR-based methods are growing at an 8.12% CAGR through 2031, driven by their high specificity and ability to test multiple allergens simultaneously. Mass-spectrometry methods are increasing in confirmatory testing applications, particularly for processed foods where protein modifications can affect immunoassay performance. Spectroscopy and imaging technologies serve specific rapid screening applications, while nanobiosensor platforms are advancing point-of-use testing through smartphone integration and AI analysis.

The market is moving toward hybrid platforms that integrate multiple detection methods to address technical limitations while maintaining cost efficiency for routine testing. Advanced biosensor technologies using gold nanoparticles and graphene-based transducers achieve femtomolar detection limits, exceeding traditional ELISA sensitivity and enabling the detection of previously undetectable trace allergen contamination. However, regulatory validation remains a significant challenge for new technologies, as ISO 16140-2 compliance requires extensive validation studies that typically add 2-3 years to market entry timelines.

The Food Allergen Testing Market Report Segments the Industry Into Technology (Immunoassay-Based, PCR-Based, Mass-Spectrometry-Based, Spectroscopy and Imaging, Others), Application (Bakery and Confectionery, Dairy Products, Seafood and Meat Products, Beverages, Baby Food and Infant Formula, Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe holds a dominant market share of 34.21% in 2025, supported by comprehensive regulatory frameworks and well-established testing infrastructure across government laboratories and commercial service providers. The European Food Safety Authority's regular updates to allergen assessment guidelines and the Dutch Food and Consumer Product Safety Authority's standards for cross-contact prevention demonstrate the region's stringent regulatory environment that sustains testing demand. Asia-Pacific registers the highest growth rate at 9.86% CAGR through 2031, with this growth stemming from evolving regulations in China and India as they align with international standards to enhance food exports. Japan's doubled food allergy prevalence highlights demographic shifts driving market growth, while South Korea and Australia serve as key testing hubs for multinational food companies.

North America operates under established FDA and USDA regulatory frameworks, with market growth primarily driven by technological advancements rather than regulatory expansion. The region maintains sophisticated testing protocols and infrastructure, while continuing to adapt to emerging allergen detection technologies and methodologies. The established regulatory environment provides a stable foundation for market operations, though the focus has shifted towards optimization and efficiency improvements rather than fundamental regulatory changes.

South America and Middle East and Africa present growth opportunities through developing regulations and export market requirements. However, limited local analytical capabilities and reliance on international testing providers restrict market development. The market distribution reflects the relationship between regulatory advancement and market growth, as regions invest in testing capabilities to enhance domestic food safety and international trade competitiveness. These emerging markets demonstrate increasing awareness of food safety standards and are gradually developing their testing infrastructure to meet international requirements.