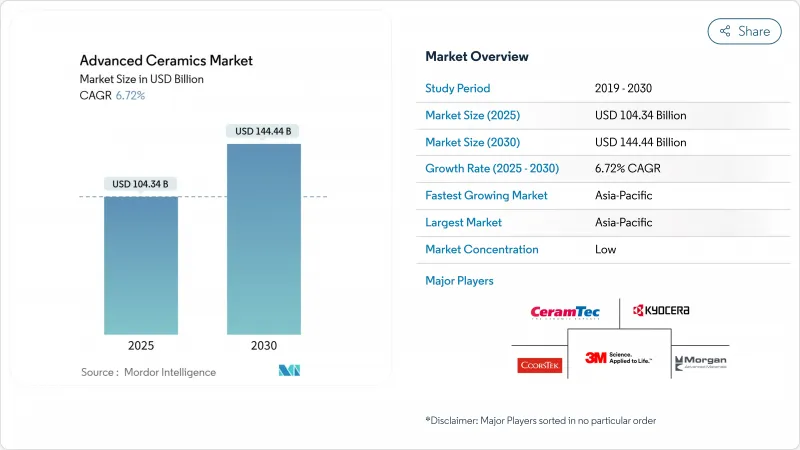

첨단 세라믹 시장의 2025년 시장 규모는 1,043억 4,000만 달러, 2030년에는 1,444억 4,000만 달러에 이르고 CAGR 6.72%로 성장할 것으로 예측되고 있습니다.

경량, 고경도, 내열성을 겸비한 재료에 대한 수요 증가는 항공우주, 일렉트로닉스, 에너지, 헬스케어 제조업체에 금속이나 고성능 폴리머로부터의 시프트를 촉진하고 있습니다. 특히 티타네이트 기반의 일렉트로 세라믹 및 세라믹 매트릭스 복합재료와 같은 재료 혁신이 공급업체에게 대응할 수있는 기회를 확대하고 있습니다. 아시아태평양은 왕성한 반도체 설비 투자로 주도적 지위를 유지하고 의료용도는 금속 임플란트를 대신해 바이오세라믹가 2자리 성장을 기록하고 있습니다. 생산 비용 상승과 복잡한 소결 경로는 여전히 역풍이지만, 자동화, 적층 성형 및 폐쇄 루프 재활용 노력으로 비용 곡선과 환경 발자국이 꾸준히 개선되었습니다.

첨단 세라믹은 금속에 없는 경도, 내마모성, 온도 안정성을 제공합니다. 제트 엔진 핫 섹션의 세라믹 매트릭스 복합재는 니켈 초합금에 비해 부품 중량을 30% 줄이고 연료 연소를 15% 개선합니다. 질화규소로 제조된 자동차용 터보차저 로터는 치수 정밀도를 유지하면서 1,000℃를 넘는 배기류를 견뎌냅니다. 알루미나나 지르코니아로 만들어진 산업용 펌프 하우징은 연마성이 높은 슬러리 중 스테인리스제보다 3-5배 오래 유지합니다.

알루미나 및 지르코니아와 같은 바이오 세라믹은 입증 된 생체 적합성과 최소한의 이온 방출을 나타내므로 임플란트의 수명이 연장되고 재 수술이 감소합니다. 외과의사는 환자의 해부학적 구조에 맞는 3D 프린팅 실리콘 질화물 척추 케이지를 점점 더 활용하고 있습니다. 정형외과 장비 제조업체는 또한 뼈 통합을 자극하는 생물학적 활성 유리 코팅과 국소 치료용 약물 용출성 다공성 세라믹을 시험하고 있습니다.

큰 하중 크기에 걸쳐 1,600°C에서 -5 °C의 균일성을 유지하는 것은 도전입니다. 약간의 온도 기울기조차도 기계적 강도를 낮추는 잔류 응력을 발생시키기 때문에 공급업체는 추가 검사 및 선별을 수행해야합니다. 완전 소결 부품의 정밀 연삭에서는 복잡한 형상으로 85% 이하의 수율을 기록하는 경우가 많습니다. 바인더 제트와 같은 적층 성형 기술은 최소한의 마무리로 끝나는 넷 모양에 가까운 부품을 만드는 것으로 유망시되고 있지만, 처리량과 표면 마감는 여전히 기존의 경로에 미치지 못합니다.

2024년의 첨단 세라믹 시장은 알루미나가 41%의 점유율을 차지했고 균형 잡힌 비용 성능 프로파일과 확립된 공급망에 의해 지원되고 있습니다. 이 재료는 기판, 절삭 공구, 생물 의학 헤드, 마모 부품에 널리 사용됩니다. 지속적인 공정 개량으로 파괴 인성을 6MPa*m1/2까지 높이는 서브 미크론의 결정 입경이 실현되어 성능을 희생하지 않고 부품의 박형화가 가능하게 되었습니다. 수요면에서 운송 및 송전망의 전기화는 알루미나를 많이 포함한 절연 하드웨어의 구입을 촉진하고 있습니다.

티타네이트 세라믹은 2030년까지 연평균 복합 성장률(CAGR)이 7.8%로 가장 급성장하고 있는 재료 그룹입니다. 티타네이트 바륨 적층 커패시터는 스마트폰과 전기자동차의 전력 관리 회로의 핵심으로 계속되고 있습니다. 동시에, 티타네이트지르콘산납을 대신하는 지속 가능한 재료로서, 무연의 니오브산칼륨·나트륨이 소나 변환기의 견인역이 되고 있습니다. 최근 연구는 ZnTiO3-ZnO 나노 복합 코팅이 접촉시 황색 포도상 구균을 97% 사멸시키는 것으로 입증되었으며 항균 표면에서 티타 네이트의 가능성을 확대했습니다.

단상 알루미나, 지르코니아, 질화규소는 잘 이해되고 있으며 규모가 크더라도 비용 효율이 높기 때문에 모놀리식 세라믹은 2024년의 첨단 세라믹 시장 규모의 78%를 차지했습니다. ISO 602 및 ASTM C1327 시험법의 표준화는 항공우주 및 의료 분야의 진입 자격을 단순화하고 판매량의 기세를 지속합니다. 생산자는 분말 형태 제어를 통해 신뢰성을 지속적으로 향상시켜 구조용 등급의 와이블 탄성률이 20을 넘어 부품 간의 편차를 줄였습니다.

세라믹 기반 복합재료는 금액 기준으로 작지만 중량과 강도의 절충점을 변경하기 때문에 CAGR은 8.12%를 나타냅니다. 배기 시스템 및 차세대 노즐의 가이드 베인은 현재 적극적인 냉각 없이 1,400℃의 가스 흐름을 견디는 실리콘 카바이드 섬유 강화 실리콘 카바이드 매트릭스를 사용하고 있습니다. 에어버스와 GE는 기체 보강재에 산화물 CMC를 사용하여 유지보수 비용을 줄이기 위한 비행 시험을 실시했습니다. 전기화학 에너지 기업은 탄소섬유 강화 알루미나를 고체 산화물 연료전지의 상호 연결에 적용하여 스택의 수명을 연장하고 있습니다. 실험실 개념이 급속히 상업 생산으로 전환되고 있다는 것은 복합재 클래스가 첨단 세라믹 산업의 주요 파괴력임을 뒷받침합니다.

아시아태평양은 2024년에 첨단 세라믹 시장의 54%를 차지했고, 밀집된 전자 클러스터, 확립된 분말 공급망 및 고가치 재료에 대한 정부의 우대 조치를 뒷받침하고 있습니다. 중국의 14차 5개년 계획에서는 첨단 세라믹을 전략적 부문으로 분류하고, 조종사에 대한 세금 공제 및 보조금 지급을 취소합니다.

북미에서는 항공우주, 방위, 의료 분야에서 소비가 증가하고 있습니다. 미국 공군 조사 연구소는 제트 엔진의 서비스 간격을 연장하기 위해 경량 CMC 연소기 라이너에 적극적으로 자금을 지원하고 있습니다. 인디애나와 테네시에 있는 정형외과 기기의 중심지에서는 고관절 부품용 지르코니아 강화 알루미나를 대량으로 조달하고 있으며, 이 지역 수요를 집중시키고 있습니다.

유럽은 독일 첨단 기계와 이탈리아 위생 도자기의 전문 지식을 통해 돌출 발자국을 유지하고 있습니다. 유럽 위원회의 '산업 리더십을 위한 첨단 재료' 이니셔티브는 지속가능성과 재활용성을 중시하고 있으며 연구예산이 저탄소 소결과 서큘러 이코노미의 파일럿 사업으로 흐르도록 하고 있습니다.

The advanced ceramics market is valued at USD 104.34 billion in 2025 and is forecast to expand to USD 144.44 billion by 2030, advancing at a 6.72% CAGR.

Rising demand for materials that combine lightweight, high hardness, and thermal resilience is pushing aerospace, electronics, energy, and healthcare manufacturers to shift away from metals and high-performance polymers. Material innovation, particularly around titanate-based electroceramics and ceramic matrix composites, enlarges the addressable opportunity set for suppliers. Asia-Pacific retains its leadership position due to strong semiconductor capital expenditure, while medical applications record double-digit growth as bioceramics replace metal implants. Although elevated production costs and complex sintering pathways remain headwinds, automation, additive manufacturing, and closed-loop recycling initiatives steadily improve cost curves and environmental footprints.

Advanced ceramics deliver hardness, wear resistance, and temperature stability that metals cannot match. Ceramic matrix composites in jet-engine hot sections cut component weight by 30% and improve fuel burn by 15% compared with nickel super-alloys. Automotive turbocharger rotors fabricated from silicon nitride withstand exhaust streams above 1,000 °C while maintaining dimensional accuracy. Industrial pump housings made from alumina and zirconia now last three to five times longer than stainless variants in abrasive slurries.

Bioceramics such as alumina and zirconia exhibit proven biocompatibility and minimal ion release, which lengthens implant lifespans and decreases revision surgeries. Surgeons increasingly rely on 3D-printed silicon-nitride spinal cages tailored to patient anatomy, an advance made possible by low-temperature stereolithography. Orthopedic device makers also experiment with bioactive glass coatings that stimulate osteointegration and with drug-eluting porous ceramics for localized therapeutics.

Maintaining +-5 °C uniformity at 1,600 °C across large load sizes is challenging. Even minor temperature gradients create residual stresses that downgrade mechanical strength, forcing suppliers to perform additional inspection and culling. Precision grinding of fully sintered parts often records yields below 85% on complicated geometries. Additive manufacturing technologies such as binder jetting show promise by building near-net-shape parts that need minimal finishing, but throughput and surface finish still trail conventional routes

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Alumina dominated the advanced ceramics market with a 41% share in 2024, supported by its balanced cost-performance profile and established supply chains. The material is entrenched in substrates, cutting tools, biomedical heads, and wear parts. Continuous process refinements now deliver sub-micron grain sizes that lift fracture toughness to 6 MPa*m1/2, enabling thinner components without performance trade-offs. On the demand side, electrification of transport and grid storage drives purchases of alumina-rich insulating hardware.

Titanate ceramics are the fastest-expanding material group at a 7.8% CAGR through 2030. Barium titanate multilayer capacitors remain the backbone of power-management circuits in smartphones and electric vehicles. Concurrently, lead-free potassium sodium niobate titanates gain traction in sonar transducers as a sustainable replacement for lead zirconate titanate. Recent research demonstrated ZnTiO3-ZnO nanocomposite coatings that kill 97% of Staphylococcus aureus on contact, widening titanate potential in antimicrobial surfaces.

Monolithic ceramics held 78% of the advanced ceramics market size in 2024 because single-phase alumina, zirconia, and silicon nitride are well understood and cost-efficient at scale. Standardization around ISO 602 and ASTM C1327 test methods simplifies qualification for aerospace or medical entry, sustaining volume momentum. Producers continue to improve reliability through powder morphology control, resulting in Weibull moduli above 20 for structural grades, which reduces part-to-part variability.

Although smaller in dollar terms, Ceramic matrix composites exhibit an 8.12% CAGR owing to their transformational weight-to-strength trade-off. Exhaust systems and next-generation nozzle guide vanes now use silicon-carbide fiber-reinforced silicon-carbide matrices that tolerate 1,400 °C gas streams without active cooling. Airbus and GE are flight-testing oxide-oxide CMCs in fuselage stiffeners to curb maintenance costs. Electrochemical energy companies apply carbon-fiber-reinforced alumina in solid-oxide fuel-cell interconnects to extend stack life. The rapid conversion of laboratory concepts into commercial runs underscores the composite class as a major disruptive force within the advanced ceramics industry.

The Advanced Ceramics Market Report Segments the Industry by Material Type (Alumina, Zirconia, Titanate, Silicon Carbide, and More), Class Type (Monolithic Ceramics, Ceramic Matrix Composites, and Ceramic Coatings), Application (Structural Ceramics, Bioceramics, Electroceramics, and More), End-User Industry (Electrical and Electronics, Transportation, Medical, and More), and Geography (Asia-Pacific, North America, and More).

Asia-Pacific possessed 54% of the advanced ceramics market in 2024, underpinned by dense electronics clusters, established powder supply chains, and government incentives for high-value materials. China's 14th Five-Year Plan classifies advanced ceramics as a strategic segment, unlocking tax credits and grant funding for pilot lines.

North America is witnessing a rise in consumption owing to robust aerospace, defense, and medical verticals. The United States Air Force Research Laboratory actively funds lightweight CMC combustor liners to extend jet-engine service intervals. Orthopedic device hubs in Indiana and Tennessee procure large volumes of zirconia-toughened alumina for hip components, driving concentrated regional demand.

Europe maintains a prominent footprint through Germany's advanced machinery and Italy's sanitary ware expertise. The European Commission's Advanced Materials for Industrial Leadership initiative emphasizes sustainability and recyclability, ensuring research budgets flow into low-carbon sintering and circular-economy pilots.