ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

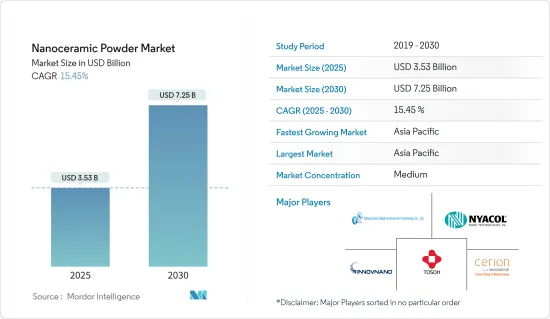

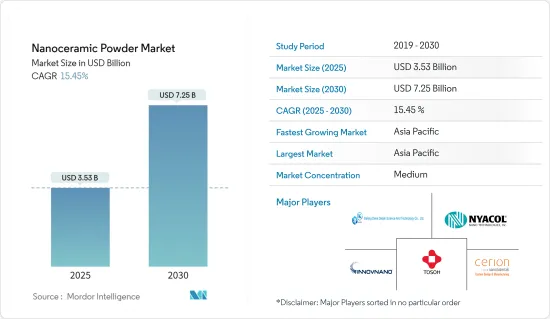

나노세라믹 파우더 시장 규모는 2025년에 35억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 15.45%로 성장하여 2030년에는 72억 5,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

COVID-19 팬데믹은 다양한 산업에 영향을 주었고, 나노세라믹 파우더 수요에 큰 영향을 미쳤습니다. 나노세라믹 파우더 수요는 운수, 화학, 공업 분야에서 감소세를 보이는 등 영향을 받았습니다. 그러나, 규제가 철폐된 이후 업계는 회복하고 있습니다.

시장 성장을 추진하는 중요한 요인은 일렉트로닉스 산업에서의 광범위한 사용입니다.

나노세라믹 파우더의 높은 가공 비용과 건강 및 안전성의 문제는 2024년부터 2029년 사이에 나노세라믹 파우더의 성장에 부정적인 영향을 미칠 것으로 예상됩니다.

탄화규소와 질화갈륨의 용도 증가와 우주탐사나 태양전지와 같은 첨단 기술에 있어서의 기회가 시장에 새로운 성장 기회를 가져올 것으로 예상됩니다.

2024년부터 2029년까지는 아시아태평양이 시장을 독점할 것으로 예상됩니다.

나노세라믹 파우더 시장 동향

전기 및 전자산업에서의 수요 증가

지난 20년간 나노세라믹에 관한 방대한 양의 연구가 이루어졌으며, 학술계와 산업계에 몇 가지 긍정적인 결과가 발생하였습니다.

유전성, 강자성, 압전성, 자기 저항, 초전도 등의 특성을 가지는 나노세라믹 파우더는 송전기기, 공업용 커패시터, 고에너지 저장 디바이스 등의 용도에 최적입니다.

나노세라믹 파우더는 전자 산업에서 사용되며 휴대폰, 휴대용 컴퓨팅 장치, 게임 시스템 및 기타 개인 전자기기의 고속 컴퓨팅 칩 제조 시 전통적으로 사용됩니다.

나노세라믹 알루미나는 더 높은 전압을 견딜 수 있기 때문에 장치의 크기에 따라 모양을 맞춤화할 수 있으며 전자 분야에서 가장 일반적으로 사용됩니다.

세계의 소비자 전자 산업은 휴대폰, 휴대용 컴퓨팅 장치, 게임 시스템 및 기타 개인 전자기기의 일관적인 수요 증가에 의해 오랜 세월에 걸쳐 세계에서 급성장을 이루고 있습니다.

국가통계국의 데이터에 따르면 중국의 집적 회로 생산량은 2023년 4월에 281억개에 달했습니다.

ASEAN은 아시아태평양에서 가장 급성장하고 있는 소비자 전자 분야 지역입니다. 전기 및 전자기기 제조업은 ASEAN에서 가장 현저한 섹터 중 하나입니다.

북미 중에서도 특히 미국에서는 일렉트로닉스 산업은 완만한 성장이 예상되고 있습니다.

세계의 소비자 일렉트로닉스 시장은 최신 기술을 적용한 기기가 인기를 얻으면서 최근 몇 년간 현저한 성장을 이루고 있습니다.

일본 전자정보기술산업협회에 따르면 2023년 1-9월의 전자제품 생산액은 7조 8,917억 2,000만엔(-528억 6,490만 달러)에 달했습니다.

위의 요인으로 인해 2024년부터 2029년에 걸쳐 시장 수요가 증가할 가능성이 높습니다.

아시아태평양이 시장을 독점할 전망

세계 수요의 50% 이상을 차지하는 아시아태평양은 나노세라믹 파우더 재료의 가장 유망한 시장이며, 가까운 미래 시장을 독점할 가능성이 높습니다.

중국은 이 지역의 나노세라믹 파우더 수요의 33% 이상을 차지하고 있습니다.

중국은 세계 최대의 일렉트로닉스 생산국 중 하나이며, 한국, 싱가포르, 대만 등 기존의 상류 제조업체와 크게 경쟁하고 있습니다. 중국은 전자기기 시장에서 가장 높은 성장률을 나타내고 있습니다.

게다가 인도 브랜드 에퀴티 재단(IBEF)에 따르면 인도의 전자기기 제조업은 2025년까지 5,200억 달러에 달할 것으로 예상되고 있습니다. Make in India, National Policy of Electronics, Net Zero Imports in Electronics, Zero Defect Zero Effect 등 국내 제조업의 성장과 수입 의존도 저하, 수출의 활성화, 제조업에의 헌신을 보장하는 정책에 의한 정부의 대처에 의해 시장은 급속히 성장할 것으로 예상되고 있습니다.

이 지역은 또한 중국과 인도가 생산 능력 극대화에 기여하고 ASEAN 국가도 시장 확대에 참여하고 있기 때문에 최대의 자동차 제조국이기도 합니다. 2022년 중국의 자동차 생산 대수는 2,702만대에 이르렀으며, 전년(2,609만대)에 비해 3% 증가했습니다.

게다가 중국은 최대의 항공기 제조국 중 하나이며 국내 항공 여객의 최대 시장이기도 합니다.

나노세라믹 파우더의 사용은 군용기의 첨단 장비품과 부품, 엔진, 그리고 전투기에서 중요하기 때문에 나노세라믹 파우더 시장은 2024년부터 2029년까지 이 지역에서 유망시되고 있습니다.

중국 정부는 매년 국방비를 발표하고 있으며 2023년 3월에는 1조 5,500억 위안(2,248억 달러)의 국방 예산을 발표했습니다.

전체적으로, 중국과 인도의 일관적인 성장에 의해 나노세라믹 파우더 수요는 향후 수년간 지역 전체에서 보다 빠른 페이스로 증가할 것으로 예상됩니다.

나노세라믹 파우더 산업 개요

세계의 나노세라믹 파우더 시장은 과점적이고 부분적으로 통합되어 있으며, 소수의 기업이 시장을 독점하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

일렉트로닉스 산업에서의 보급

헬스케어 분야로부터 수요 증가

고성능 세라믹 코팅 수요 증가

억제요인

높은 가공 비용

기타 억제요인

업계 밸류체인 분석

Porter's Five Forces 분석

공급자의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

특허 분석

원재료 분석

제5장 시장 세분화

유형

산화물 분말

탄화물 분말

질화물 분말

붕소 분말

기타 유형

최종 사용자 산업

전기 및 전자

공업용

수송

의료

화학

방위

기타 최종 사용자 산업

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

유럽

독일

영국

프랑스

이탈리아

기타 유럽

북미

미국

캐나다

멕시코

세계 기타 지역

제6장 경쟁 구도

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

ABM Advance Ball Mill Inc.

Beijing DK Nano Technology Co. Ltd

Cerion LLC

Inframat Advanced Materials LLC

Innovnano-materiais Avancados SA

Nanophase Technologies Corporation

NYACOL Nano Technologies Inc.

Tosoh Corporation

Trunnano

제7장 시장 기회와 미래 동향

우주 탐사 및 태양전지와 같은 첨단 기술의 비즈니스 기회

탄화규소와 질화갈륨의 용도 확대

CSM

영문 목차

영문목차

The Nanoceramic Powder Market size is estimated at USD 3.53 billion in 2025, and is expected to reach USD 7.25 billion by 2030, at a CAGR of 15.45% during the forecast period (2025-2030).

Key Highlights

The COVID-19 pandemic had a diverse effect on different industries, significantly impacting the demand for nanoceramics powder. The demand fluctuations were due to disruption in supply chains, reduced economic activity, and changed consumer behavior. The demand for nanoceramics powder was affected as the transportation, chemical, and industrial sectors witnessed a decreasing trend. However, since restrictions were removed, the industry has been recovering.

A significant factor driving the market study is widespread use in the electronics industry. Additionally, increasing demand in the healthcare sector and high-performance ceramic coatings drive the nanoceramics powder market.

The high processing costs of nanoceramic powder and health and safety issues are expected to negatively affect the growth of the nanoceramic powder between 2024 and 2029.

Increasing applications of silicon carbide and gallium nitride and opportunities in advanced technologies, like space exploration and photovoltaic solar cells, are expected to provide new growth opportunities for the market.

Asia-Pacific is expected to dominate the market from 2024 to 2029. The electrical and electronics sector is supported by increasing investments and export opportunities, which drive this growth.

Nanoceramic Powder Market Trends

Increasing Demand from the Electrical and Electronics Industry

Over the last 20 years, there has been a huge amount of study into nanoceramics that has resulted in some positive outcomes for academia and industry. As a result, these advanced materials have a wide range of uses in electronics.

Nanoceramic powders with properties like dielectricity, ferromagnetism, piezoelectricity, magnetoresistance, and superconductivity make them a perfect fit for applications in power transmission devices, industrial capacitors, high-energy storage devices, and others.

Nanoceramic powders are used in the electronics industry, and they are traditionally used during the production of high-speed computing chips in cellular phones, portable computing devices, gaming systems, and other personal electronic devices.

Nanoceramic alumina is most commonly used in electronics, as it can withstand a much higher voltage, so its shape can be customized based on the device size.

The global consumer electronics industry has been growing rapidly across the world over the years due to the consistently increasing demand for cellular phones, portable computing devices, gaming systems, and other personal electronic devices. According to the Japan Electronics and Information Technology Industries Association, the total production of electronic products accounted for JPY 6,937,233 million in the first 8 months of 2023.

According to data from the National Bureau of Statistics, China's integrated circuit production volume reached 28.1 billion units in April 2023. The number of smartphone users in China is growing rapidly. The number of smartphone users in the country is expected to reach 868.2 million by the end of 2023.

ASEAN has the fastest-growing consumer electronics segment in Asia-Pacific. Electrical and electronics manufacturing is one of the most prominent sectors in ASEAN. The sector accounts for about 30-35% of the total exports from the region. Most global consumer electronic products, such as radio, computers, and cellular phones, are manufactured and assembled in ASEAN countries.

In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. An increase in the demand for new technological products is expected to help the market expansion in the future.

The global consumer electronics market has witnessed notable growth in the past few years as the latest technological gadgets are gaining popularity. Home automation and integrating devices with personal assistance have provided noteworthy growth to the market.

According to the Japan Electronics and Information Technology Industries Association, the production of electronic products accounted for JPY 7,891,720 million (~USD 52,864.9 million) in the first nine months (i.e., January- September) of 2023.

All the aforementioned factors are likely to increase the demand for the market between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

With over 50% of the global demand, Asia-Pacific is the most promising market for nanoceramic powder materials, which is likely to dominate the market in the near future. This domination can be attributed to the rising demand from the electronics and medical industries in the region.

China accounts for over 33% of the demand for nanoceramic powder in this region. The country is also one of the major global markets for nanoceramic powder. Sustained demand for nanoceramic powder is witnessed here through its robust electronics, aerospace, and defense (A&D) sectors.

China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. According to the National Bureau of Statistics of China, retail sales of household appliances and consumer electronics in China amounted to almost CNY 61 billion (USD 8.52 billion) in April 2023.

Moreover, according to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect Zero Effect, which offer a commitment to growth in domestic manufacturing, lowering import dependence, energizing exports, and manufacturing.

The region is also the largest manufacturer of automobiles, with China and India contributing to maximum production capacity and ASEAN countries joining the expanding market. China is the largest automobile market globally and plays a pivotal role in the global automotive sector. In 2022, vehicle production in China reached a notable total of 27.02 million units, marking a 3% increase compared to the previous year (26.09 million units). The substantial production volume in China signifies a robust demand for automotive materials, including nanoceramic powder, to support this thriving industry.

Moreover, China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with the presence of over 200 small aircraft parts manufacturers.

Since the use of nanoceramic powder is important in high-grade military equipment and parts of military aircraft, engines, and fighter jets, the market for nanoceramic powder looks promising from 2024 to 2029 in the region.

The Chinese government announces defense expenditure information annually. China announced a defense budget of CNY 1.55 trillion (USD 224.8 billion) in March 2023. This represents a nominal 7.2% increase from the CNY 1.45 trillion (USD 229.6 billion) budget in 2022.

Overall, with the consistent growth in China and India, the demand for nanoceramics powder is expected to increase at a faster pace in the overall region in the coming years. The huge growth of Asia-Pacific is quite instrumental in the expansion of the global nanoceramics powder market.

Nanoceramic Powder Industry Overvview

The global nanoceramic powder market is oligopolistic and partially consolidated, with few players dominating the market. The major companies include Tosoh Corporation, Beijing DK Nano Technology Co. Ltd, NYACOL Nano Technologies Inc., Innovnano-Materiais Avancados SA, and Cerion LLC.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Widespread Use in the Electronics Industry

4.1.2 Increasing Demand from the Healthcare Sector

4.1.3 Increasing Demand for High-performance Ceramic Coatings

4.2 Restraints

4.2.1 High Processing Cost

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Patent Analysis

4.6 Raw Material Analysis

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Oxide Powder

5.1.2 Carbide Powder

5.1.3 Nitride Powder

5.1.4 Boron Powder

5.1.5 Other Types

5.2 End-user Industry

5.2.1 Electrical and Electronics

5.2.2 Industrial

5.2.3 Transportation

5.2.4 Medical

5.2.5 Chemical

5.2.6 Defense

5.2.7 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Rest of Europe

5.3.3 North America

5.3.3.1 United States

5.3.3.2 Canada

5.3.3.3 Mexico

5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

6.1 Market Ranking Analysis

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 ABM Advance Ball Mill Inc.

6.3.2 Beijing DK Nano Technology Co. Ltd

6.3.3 Cerion LLC

6.3.4 Inframat Advanced Materials LLC

6.3.5 Innovnano-materiais Avancados SA

6.3.6 Nanophase Technologies Corporation

6.3.7 NYACOL Nano Technologies Inc.

6.3.8 Tosoh Corporation

6.3.9 Trunnano

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Opportunities in Advanced Technologies, Like Space Exploration and Photovoltaic Solar Cell

7.2 Increasing Applications of Silicon Carbide and Gallium Nitride