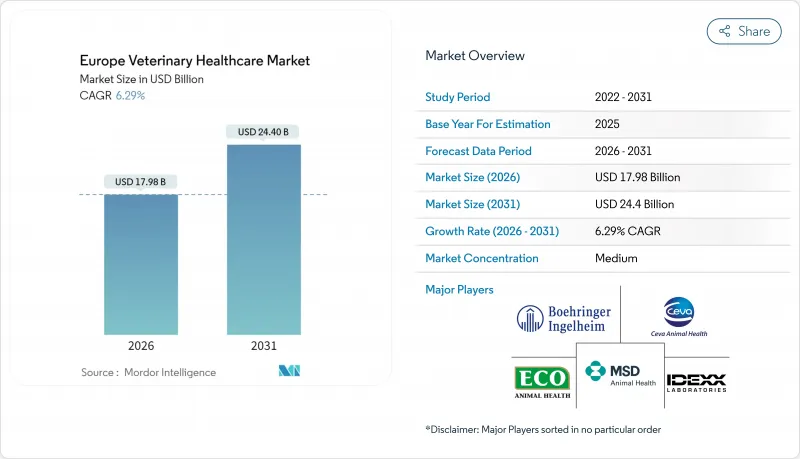

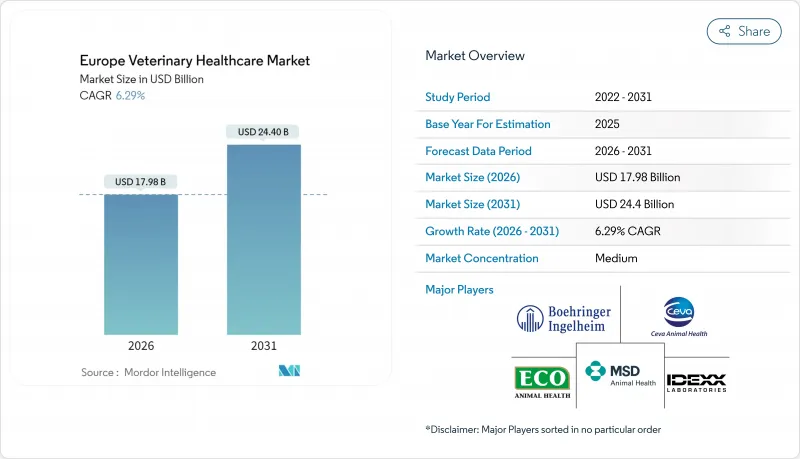

유럽의 동물용 헬스케어 시장은 2025년 169억 2,000만 달러에서 2026년에는 179억 8,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 6.29%를 나타낼 전망입니다. 2031년까지 244억 달러에 달할 것으로 예상됩니다.

이 확대는 반려동물의 인간화가 널리 진행되고 있으며, 제품 승인을 가속화하는 규제 개혁, 임상 인프라에 대한 기업 투자의 활성화에 의해 추진되고 있습니다. 가처분 소득 증가로 일상적인 치료와 고급 치료에 대한 자기 부담 지출이 증가하고 있는 반면, 디지털 플랫폼은 진료 효율성과 고객 참여도 향상에 기여하고 있습니다. 병원 체인 간의 통합은 진단 및 생물학적 제제의 구매력을 향상시키고, 단일클론항체의 상업적 성공은 정밀의료로의 전환을 보여줍니다. 동시에 축산농가는 항균제 내성을 억제하기 위해 바이오세이프 백신을 채용하고 있어 농장동물 전반에 걸친 수요를 지속시키고 있습니다.

유럽에서는 9,000만 가구 이상이 반려동물을 사육하고 있으며, 이는 수의학의 장기적인 수요를 지원하고 있습니다. 독일은 지역 톱으로, 45%의 가정에 반려동물이 있어, 보험 가입률의 가속에 의해 치료비에의 가격 감응도가 저하하고 있습니다. 이탈리아는 6,020만 마리의 동물 인구를 보유하고 있으며, 예방 의료에 대한 견조한 지출로 이어지고 있습니다. 도시의 주인은 가처분 소득을 건강 관리 플랜, 고급 푸드, 만성 질환 관리에 충당하고 있습니다. 북유럽 국가에서는 사육률과 보험 가입률의 연동성이 현저하고, 스웨덴에서는 2023년 시점에서 개의 83%, 고양이의 69%가 보험 가입했습니다. 반려동물의 수명이 연장됨에 따라 암 치료, 내분비학, 노년기 통증 관리 등 반려동물 건강 관리의 요구가 다양화하고 있습니다.

EU 규칙 2019/6은 제품 승인 절차를 표준화하고 예방 항생제의 사용을 제한하고 의약품의 추적 성을 향상시킵니다. 2026년 시행 예정인 새로운 복지 패키지로는 수송·과 축에의 감독이 확대되어 백신이나 진통제의 사용 촉진을 도모할 수 있습니다. 공공 지출은 특히 독일, 스페인, 영국에서 지방 수의사 부족에 대처하는 새로운 대학 프로그램을 지원합니다. 유럽 의약품청의 2025년 전략은 항균제 내성 대책으로서 원헬스 시책을 우선하여 비항생물질 요법 수요를 촉진했습니다. 이러한 정책은 종합적으로 제조업체와 서비스 제공업체에게 성장 지향적인 사업 환경을 키우고 있습니다.

2022년부터 2023년까지 북유럽 시장에서 일반적인 치료의 중앙값 요금은 2-24% 상승했습니다. 기업체인은 독립계를 능가하는 연간 가격 상승률을 기록하고 있습니다. 스페인은 이러한 동향을 여실히 보여주며, 지출은 2022년 26억 1,300만 유로에서 2030년에는 38억 유로에 이를 것으로 예측되는 반면, 21%의 부가가치세(VAT)가 소비자의 부담을 더욱 증대시키고 있습니다. 기술 혁신, 임금 상승 압력, 개인 자금의 수익 목표가 인플레이션을 가속화하고 있습니다. 스웨덴의 "Vetpris"와 같은 가격 비교 포털 사이트가 등장하고 있지만 고급 의료기기 및 생물학적 제제로 인한 구조적 비용 하한을 상쇄 할 수는 없습니다. 예산에 제한이 있는 주인은 치료를 늦추고 동물 복지의 악화와 공중 보건에 영향을 미칠 위험이 있습니다.

2025년 치료제는 유럽의 동물용 헬스케어 시장 점유율의 61.88%를 차지했으며 백신, 구충제, 항감염제가 핵심을 이루었습니다. 헬스케어 분야의 유럽 시장 규모는 기업에 의한 집중구매를 활용한 고이익률 생물제제의 임베디드에 의해 꾸준히 확대. VAXXITEK 등의 백신은 2025년 초에 15.2%의 성장을 기록해 양계업체의 생물안전 대책 강화를 반영했습니다. NEXGARD등의 주력 브랜드에 의해 구충제는 견조를 유지한 한편, 항균약 적정 사용 정책에 의해 전신성 항균제의 유통량은 억제되었습니다. 진단약 시장은 규모가 작은 AI 구동형 화상 진단 장치나 시약 불필요한 혈액 검사 장치의 도입에 의해 검사 시간을 단축해 컴플라이언스를 향상시킨 것으로, CAGR 7.18%를 나타낼 전망입니다. 면역진단 키트가 최대 점유율을 유지하는 한편 보험상환제도의 정비와 기업백오피스 시스템과의 통합을 배경으로 분자진단검사와 디지털 X선 촬영이 가장 빠르게 성장하고 있습니다.

진단 분야의 기세는 클리닉의 수익성을 높이고, 사례 결과의 투명성을 향상시키고, 고객의 신뢰를 강화합니다. 유럽 의약청(EMA)의 2023년 승인 목록에는 9유형의 새로운 백신이 게재되어 유럽의 동물용 헬스케어 시장의 장기적인 지속을 지지하는 파이프라인의 활력을 나타냈습니다. 반려동물용 단일클론항체가 바이오마커로서도 기능함에 따라, 치료와 진단의 경계는 모호해지고 통합 케어 패키지의 도래를 예감하게 됩니다. 씹을 수 있는 제제와 복합 기생충 구제 백신·백신에 의한 제품 수명주기의 연장은 기업화된 진료 네트워크내에서의 크로스셀링 기회를 창출합니다.

유럽의 개 고양이용 헬스케어 시장 규모는 2025년 수익의 46.10%를 차지해, 보험의 확대, 도시형 라이프 스타일, 장수에 수반하는 질환 증가가 기반이 되었습니다. 독일 가구에서만 프리미엄 서비스에 대한 지출이 두드러지며, 반려동물은 유럽 의료 시장의 주도적 지위를 강화하고 있습니다. 가금 분야는 6.62%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 이루고 있으며, 고밀도·항생제 미사용 생산으로의 이행을 반영하고 있습니다. 말은 틈새면서 고부가가치 소비를 견인하고 있으며, 특히 프랑스와 독일에서는 말의 심장병학과 정형외과적 개입이 주목받고 있습니다. 돼지 및 반추동물 부문에서는 메타파락시스에 대한 규제적 제약을 충족시키기 위해 복합 백신이 채택됩니다. MSD의 아쿠아 사업 인수 후 DNA 기반 연어 백신을 통한 수산 양식 분야가 상승하고 성장 벡터의 다양화가 진행되고 있습니다.

반려동물 분야에서는 소형 동물 집중 치료실 기준에 따라 인간 등급의 시설 투자가 이익을 가져옵니다. 인간 내분비학으로부터 응용된 고양이용 당뇨병 치료제가 보여주는 바와 같이, 종간 제품 전용에 의해 파이프라인 효율이 가속. 축산 분야에서는 생산자 통합과 소매 가격 압력에 의한 이익률 압축에 직면하여 비용효과가 높은 광역 스펙트럼 생물제제와 뉴트라슈티컬에 대한 수요가 향하고 있습니다.

The Europe veterinary healthcare market is expected to grow from USD 16.92 billion in 2025 to USD 17.98 billion in 2026 and is forecast to reach USD 24.4 billion by 2031 at 6.29% CAGR over 2026-2031.

This expansion is propelled by widespread pet humanization, regulatory reforms that accelerate product approvals, and strong corporate investment in clinical infrastructure. Rising disposable incomes support higher out-of-pocket spending on routine and advanced treatments, while digital platforms enhance practice efficiency and client engagement. Consolidation among hospital chains unlocks purchasing power for diagnostics and biologics, and successful commercialization of monoclonal antibodies signals a shift toward precision therapeutics. Simultaneously, livestock producers adopt biosafe vaccines to curb antimicrobial resistance, sustaining demand across farm-animal lines.

More than 90 million European households keep pets, anchoring long-run demand for veterinary care. Germany tops the region, with pets in 45% of homes and accelerating insurance uptake that reduces treatment price sensitivity. Italy follows with a 60.2 million animal population, translating into robust preventive-care spending. Urban owners channel discretionary income toward wellness plans, premium foods, and chronic-disease management. Nordic nations illustrate the linkage between ownership and insurance: Sweden insured 83% of dogs and 69% of cats in 2023. As pets live longer, companion-animal healthcare needs diversify into oncology, endocrinology, and geriatric pain control.

Regulation (EU) 2019/6 standardizes product approval procedures, restricts prophylactic antibiotics, and improves medicine traceability. The forthcoming welfare package, expected in 2026, extends oversight to transport and slaughter, driving greater vaccine and analgesic uptake. Public spending supports new university programs that address rural veterinary shortages, especially in Germany, Spain, and the UK. The European Medicines Agency 2025 Strategy prioritizes One-Health measures against antimicrobial resistance, spurring demand for non-antibiotic therapies. These policies collectively nurture a growth-oriented operating climate for manufacturers and service providers.

Median fees for common procedures rose 2-24% across Nordic markets between 2022 and 2023; corporate chains posted annual price hikes outpacing independents. Spain illustrates the trend, with spend climbing from EUR 2.613 billion in 2022 to a projected EUR 3.800 billion in 2030 while a 21% VAT compounds consumer burden. Technology upgrades, higher wage expectations, and private-equity return targets fuel inflation. Price comparison portals such as Sweden's Vetpris emerge but cannot offset the structural cost floor set by advanced equipment and biologics. Budget-constrained owners delay care, risking welfare setbacks and public-health repercussions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Therapeutics represented 61.88% of Europe veterinary healthcare market share in 2025, anchored by vaccines, parasiticides, and anti-infectives. Europe veterinary healthcare market size for therapeutics grew steadily as corporates leveraged centralized buying to stock high-margin biologics. Vaccines such as VAXXITEK posted 15.2% expansion in early 2025, reflecting poultry producers' heightened biosecurity protocols. Parasiticides remained resilient through flagship brands like NEXGARD, although antibiotic stewardship capped systemic-antibacterial volumes. Diagnostics, while smaller, register a 7.18% CAGR as clinics adopt AI-driven imaging and reagent-free hematology devices that compress lab timelines and lift compliance. Immunodiagnostic kits retain the largest slice, yet molecular assays and digital radiography accelerate fastest, propelled by insurance reimbursement and corporate back-office integrations.

Diagnostic momentum elevates practice profitability and improves case-outcome transparency, reinforcing client trust. EMA's 2023 approval list, with nine new vaccines, signals sustained pipeline vitality that will sustain the Europe veterinary healthcare market long term. The line between therapy and diagnosis blurs as companion-animal monoclonal antibodies double as biomarkers, foreshadowing integrated care bundles. Product-life-cycle extensions through chewable formulations and combination parasiticide-vaccines create cross-selling opportunities within corporatized clinic networks.

Europe veterinary healthcare market size for dogs and cats equaled 46.10% of 2025 revenue, underpinned by expanding insurance, urban lifestyles, and longevity-linked morbidities. German households alone spent heavily on premium services, reinforcing the Europe veterinary healthcare market leadership of companion animals. Poultry edges ahead as fastest riser at 6.62% CAGR, mirroring the shift toward high-density, antibiotic-free production. Horses command niche but high-value consumption in equine cardiology and orthopedic interventions, particularly across France and Germany. Swine and ruminant segments adopt combination vaccines to satisfy regulatory curbs on metaphylaxis. Aquaculture emerges through DNA-based salmon vaccines following MSD's aqua acquisition, diversifying growth vectors.

The companion sector benefits from human-grade facility investments that mirror small-animal ICU standards. Cross-species product transfers accelerate pipeline efficiency, evidenced by feline diabetes solutions adapted from human endocrinology. Livestock categories confront margin compression from producer consolidation and retail price pressure, steering demand toward cost-effective broad-spectrum biologics and nutraceuticals.

The Europe Veterinary Healthcare Market Report is Segmented by Product (Therapeutics and Diagnostics), Animal Type (Dogs & Cats, Horses, Ruminants, Swine, Poultry, and Other Animal Types), Route of Administration (Oral, Parenteral, and More), End User (Veterinary Hospitals & Clinics, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).