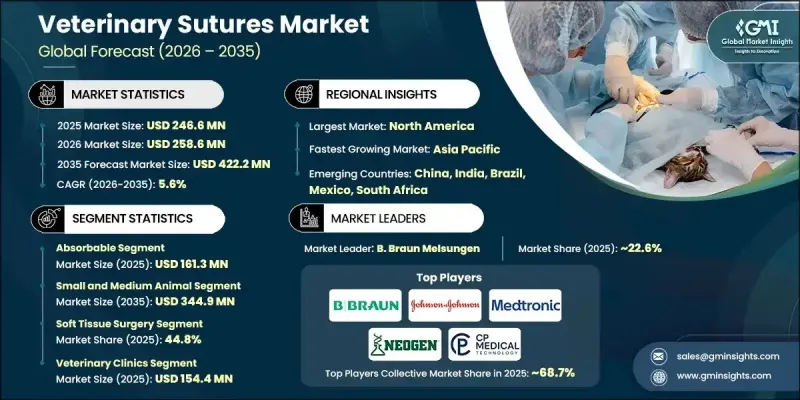

세계의 수의용 봉합사 시장은 2025년에 2억 4,660만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.6%로 성장하여 4억 2,220만 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 반려동물 수 증가와 동물의 만성질환 및 생활습관병의 확산으로 인해 성장하고 있습니다. 반려동물을 가족의 일원으로 인식하는 경향이 강해지면서 외과수술을 포함한 첨단 동물의료에 대한 수요가 급증하고 있습니다. 수의사 봉합사는 수의사가 상처를 닫고 외과적 절개 부위를 고정하여 적절한 치유를 보장하기 위해 사용하는 중요한 의료기기입니다. 감염 위험을 줄이고 조직 회복을 촉진하는 봉합 재료의 혁신은 임상 결과 향상에 기여하며 시장 발전의 원동력이 되고 있습니다. 선진국과 신흥국을 막론하고 동물병원 및 진료소의 확대로 외과적 치료에 대한 접근성이 개선되고 있습니다. 흡수성 및 비흡수성 봉합사는 생물학적 적합성, 내구성, 종을 초월한 안전성을 고려하여 설계되어 효과적인 상처 관리와 회복을 촉진합니다. 동물 건강관리에 대한 인식이 높아짐에 따라 전 세계적으로 첨단 수의학 봉합사의 채택이 지속적으로 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 2억 4,660만 달러 |

| 예측 금액 | 4억 2,220만 달러 |

| CAGR | 5.6% |

흡수성 봉합사 부문은 2025년 1억 6,130만 달러 규모로 65.4%의 점유율을 차지할 것으로 예측됩니다. 폴리글리콜산, 폴리글락틴 등을 포함한 흡수성 봉합사는 제거할 필요가 없어 편리하고, 통원 횟수를 줄일 수 있습니다. 연부조직 수술, 일상적인 상처 봉합, 내부 시술 등 폭넓은 적용성이 그 우위를 뒷받침하며 수의사와 반려동물 보호자들로부터 높은 지지를 받고 있습니다.

중소동물 분야는 2035년까지 3억 4,490만 달러 규모에 이를 것으로 예측됩니다. 이 분야의 성장은 개와 고양이를 비롯한 중-소형 반려동물 증가와 반려동물 보호자들의 고급 수의학에 대한 투자 의지가 높아지면서 성장세를 보이고 있습니다. 이들 동물은 일상적인 수술부터 복잡한 수술까지 다양한 외과적 시술을 받기 때문에 다양한 봉합사에 대한 안정적인 수요가 발생하고 있습니다.

북미 수의학 봉합사 시장은 2025년 39.7%로 가장 큰 점유율을 차지했습니다. 이 지역 시장 성장은 방대한 반려동물 수, 동물 건강에 대한 높은 인식, 잘 구축된 수의학 인프라에 의해 촉진되고 있습니다. 반려동물 보험의 보급 확대는 보호자들이 양질의 수술 치료에 더 많은 투자를 할 수 있게 해 시장 확대를 뒷받침하고 있습니다.

The Global Veterinary Sutures Market was valued at USD 246.6 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 422.2 million by 2035.

The market is driven by the rising pet population and the growing prevalence of chronic and lifestyle-related conditions among animals. With pets increasingly regarded as family members, demand for advanced veterinary care, including surgical procedures, has surged. Veterinary sutures are critical medical tools used by veterinarians to close wounds and secure surgical incisions, ensuring proper healing. The market benefits from innovations in suture materials that reduce infection risks and enhance tissue repair, improving clinical outcomes. Expansion of veterinary hospitals and clinics across both developed and emerging regions has improved access to surgical care. Sutures, available in absorbable and non-absorbable forms, are designed for biocompatibility, durability, and safety across species, ensuring effective wound management and faster recovery. As animal healthcare awareness grows, adoption of advanced veterinary sutures continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $246.6 Million |

| Forecast Value | $422.2 Million |

| CAGR | 5.6% |

The absorbable sutures segment held a 65.4% share, valued at USD 161.3 million in 2025. Absorbable sutures, including polyglycolic acid, polyglactin, and other types, are favored for convenience since they do not require removal, reducing the need for follow-up visits. Their broad applicability across soft tissue surgeries, routine wound closures, and internal procedures contributes to their dominance, making them highly preferred by veterinarians and pet owners.

The small and medium animal segment is projected to reach USD 344.9 million by 2035. Growth in this segment is fueled by the increasing population of dogs, cats, and other small to medium pets, along with pet owners' willingness to invest in advanced veterinary care. These animals undergo a variety of surgical procedures, from routine operations to complex interventions, creating consistent demand for diverse suture types.

North America Veterinary Sutures Market held the largest share of 39.7% in 2025. Market growth in the region is driven by a substantial pet population, strong awareness of animal health, and a well-established veterinary care infrastructure. The rising adoption of pet insurance also supports market expansion by enabling owners to invest more in quality surgical care.

Key companies active in the Global Veterinary Sutures Market include B. Braun Melsungen, Vetersut, CP Medical, Medtronic, Orion Sutures, AIP Medical, Vitrex Medical, SMI, DemeTECH Corporation, Dolphin Sutures, Johnson & Johnson, Cencora, Lotus Surgicals, and KATSAN. Companies in the Veterinary Sutures Market are leveraging multiple strategies to strengthen their market presence. They are focusing on research and development to create advanced, biocompatible, and infection-resistant suture materials. Strategic collaborations with veterinary hospitals and clinics enhance product adoption. Expanding distribution networks across emerging and developed regions ensures wider reach and accessibility. Many firms are also adopting digital marketing and e-commerce platforms to target pet owners and veterinary professionals directly. In addition, companies are investing in training programs for veterinarians to promote optimal suture usage, while mergers, acquisitions, and partnerships are employed to increase market share and accelerate entry into new regions.