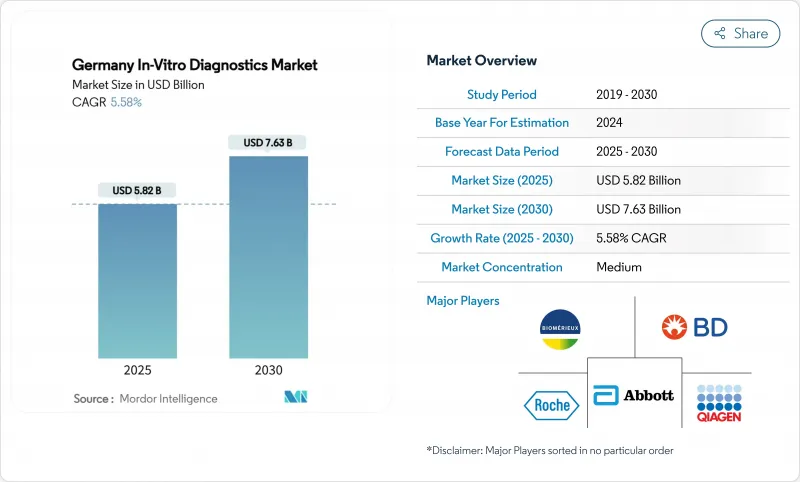

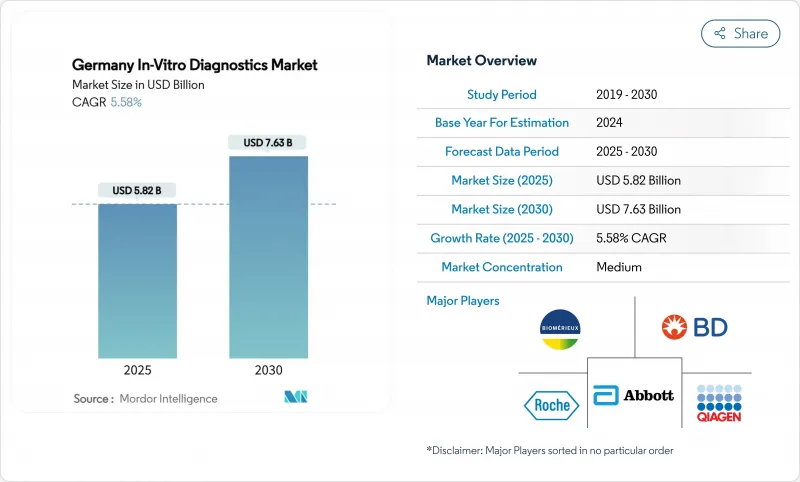

독일의 체외진단 시장 규모는 2025년에 58억 2,000만 달러, 2030년에는 76억 3,000만 달러에 이르고, CAGR은 5.58%를 나타낼 전망입니다.

이 지속적인 페이스는 국가의 의료 예산 4,740억 유로 중 진단이 전략적으로 중요하다는 것을 뒷받침합니다.

이 지속적인 속도는 국가의 의료 예산 4,740억 유로 중 진단이 전략적으로 중요한 위치를 차지하고 있음을 보여줍니다. 만성 질환 스크리닝, 정밀 종양학 프로그램, 신속한 감염증 감시가 수요의 원동력이 되는 한편, 병원 미래 기금이나 2025년 전자 환자 기록 의무화 등의 디지털 이니셔티브가 검사실의 자동화를 가속화합니다. EU의 IVDR 인증을 조기에 취득한 제조업체는 독일의 4개의 노티파이드 바디(NB)를 통해 시장 진입이 빨라져 적합 포트폴리오의 경쟁력을 높일 수 있습니다. NGS와 멀티플렉스 면역조직화학을 활용한 Precision On Collogy Assay는 가장 빠른 수익 확대 요인이며, 포인트 오브 케어 플랫폼은 응급 및 재택 환경에서의 분산 케어 모델의 확대로부터 혜택을 받습니다. 이러한 요인을 종합하면 독일의 체외진단 시장은 상환의 역풍에도 불구하고 명확한 성장 궤도를 유지하고 있습니다.

고령화가 진행되는 독일에서는 대사, 심장 및 신장 패널이 필요한 환자의 밑단이 퍼져 있습니다. 당뇨병의 유병률은 2025년 성인 930만명을 넘어 미국 당뇨병협회가 추진하는 개별 케어의 프로토콜에 따라 HbA1c와 마이크로알부민의 검사량이 증가합니다. 심혈관 위험 스크리닝도 마찬가지로 강화되었으며 Eurostat는 2024년 독일의 고혈압률을 24%로 지적하고 지질과 hs-트로포닌 사용에 박차를 가하고 있습니다. 이러한 역학적 현실은 임상 화학의 우위를 확고하게 하는 동시에 분자 패널을 일상적인 알고리즘으로 끌어 올려 독일의 체외진단 시장을 촉진합니다. 검사 시설은 시료 유입을 효율적으로 관리하기 위해 자동 코어 분석기와 고처리량 면역분석 라인을 확장하여 대응하고 있습니다.

43억 유로의 병원 미래 기금은 미들웨어, 트럭 자동화, 상호 운용가능한 LIS 업그레이드를 지원하여 실험실과 국가 ePA 백본 간의 양방향 데이터 흐름을 가능하게 합니다. 2025년의 DigitalRadar의 33/100 기준치는 미개발 효율성을 돋보이게 하고 적극적인 현대화 프로젝트를 촉진하고 있습니다. 하이델베르크에 있는 Siemens Health Innes의 자율적 로봇 코어 랩과 같은 조기 도입 기업은 수작업을 86% 줄이고 턴어라운드 시간을 37% 단축했다고 보고했습니다. 클라우드 네이티브 미들웨어와 AI를 활용한 품질 관리 모듈을 제공하는 벤더가 경쟁 시장을 견인해 독일의 체외진단 시장의 성장 레버로서의 소프트웨어가 강화되고 있습니다.

2024년 Association for Molecular Pathology의 조사에 따르면 독일 검사 시설의 73%는 IVDR 규정이 완전히 명확하지 않았으며, 41%는 이미 신규 검사의 시작을 연기하고 있습니다. 마감일은 2027-2029년까지 늘었으나 고위험 검사 자료는 여전히 비용이 많이 드는 성능 시험과 노티파이드 바디 감사를 요구합니다. 규칙 2024/1860은 추가로 6개월 동안 품절 경고를 부과하고 공급업체는 공급망을 강화해야 합니다. 컴플라이언스 투자는 R&D 예산을 우회하여 독일의 체외진단 시장 전체의 단기 혁신을 억제합니다.

임상 화학은 2024년 매출의 25%를 차지하며 독일의 체외진단 시장 규모에서 전해질, 간기능, 대사 패널의 요점이 되고 있습니다. 일상적인 검사가 플랫폼에 대한 투자를 지원하는 반면, 면역 진단은 감염과자가 면역 상태에 대한 통찰력을 넓힙니다. 또한 CleanNA사의 CE-IVD cfDNA 키트는 종양학 및 출생전 진단에의 응용을 확대하고 있습니다.

Roche의 125개 검사 파이프라인은 종양학, 신경학 및 심장 대사 패널에서 견인력을 강조합니다. Precision Medicine의 가이드라인이 성숙함에 따라 실험실은 종합적인 시퀀싱과 반사 면역조직화학을 통합하여 맞춤형 치료를 빠르게 진행하고 있습니다. 그 결과, 시장 역학은 안정적인 기준선 화학과 빠른 분자 부문의 역동적인 믹스를 즐길 수 있습니다.

Immunoassay는 2024년 매출의 34%를 차지했고, 풍부한 메뉴와 성숙한 분석기 그룹은 가격 압력에도 불구하고 예측 가능한 시약의 풀스루를 제공합니다. PCR의 다용도는 감염성 감시를 지원하고 등온 NAAT는 환자에 가까운 인플루엔자와 RSV의 조합으로 성장합니다. 차세대 시퀀서는 2자리 성장을 보여주고 복잡한 유전체 프로파일링의 독일 체외진단 시장 규모를 밀어 올립니다.

MGI Tech의 PrepALL 리퀴드 핸들러 및 Smart 8 피펫팅 스테이션과 같은 자동화 개발은 샘플 전처리 리드 타임을 최대 40% 단축하여 실험실 처리량을 향상시킵니다. 질량 분석은 탠덤 MS 스테로이드 패널에서 독성학에서 내분비학으로 진보하고 유동 세포 계측법은 면역 페노 타이핑 프로토콜을 표준화합니다. 이와 같이 수렴하는 기술은 독일의 체외진단 시장 전체에서 시약의 가동 시간을 지키면서 분석의 깊이를 높이고 있습니다.

시약 및 키트는 2024년 매출의 69%를 차지하고 독일의 체외진단 시장 점유율 속에서 벤더의 현금 흐름을 지원하는 경상 소비형 모델입니다. 장비 매출은 미들웨어 업그레이드와 연결성, 사이버 보안 레이어를 번들한 교환 사이클을 따릅니다.

소프트웨어 및 서비스는 실험실 워크플로우의 디지털화와 함께 CAGR 10.50%로 가속화되었습니다. 유나이트라보는 277만 유로의 시드권을 획득하고, 이종 기기를 단일의 운영 스택에 통합해, 바이오 테크놀로지 랩에서의 수동 데이터 전송을 삭감. 예측 유지보수 모듈은 예기치 않은 다운타임을 줄이고, 클라우드 기반 분석은 실용적인 집단 통찰력을 생성하고, 물리적 분석 전달을 넘어 독일의 체외진단 시장 가치를 증가시킵니다.

The Germany in-vitro diagnostics market size is USD 5.82 billion in 2025 and is forecast to reach USD 7.63 billion by 2030, advancing at a 5.58% CAGR; this sustained pace underscores the strategic weight of diagnostics within the nation's EUR 474 billion health-care budget.

Demand is powered by chronic-disease screening, precision oncology programs and rapid infectious-disease surveillance, while digital initiatives such as the Hospital Future Fund and the 2025 electronic patient record mandate accelerate laboratory automation. Manufacturers that obtain early EU IVDR certification enjoy faster market access through Germany's four Notified Bodies, creating a competitive moat for compliant portfolios. Precision-oncology assays leveraging NGS and multiplex immunohistochemistry represent the quickest revenue escalators, while point-of-care platforms benefit from expanding decentralized-care models in emergency and home settings. Collectively, these factors keep the Germany in-vitro diagnostics market on a clear growth trajectory despite reimbursement headwinds.

Germany's aging population profile widens the base of patients requiring metabolic, cardiac and renal panels. Diabetes prevalence crossed 9.3 million adults in 2025, lifting HbA1c and microalbumin testing volumes as per individualized-care protocols promoted by the American Diabetes Association. Cardiovascular risk screening likewise intensifies, with Eurostat noting Germany's 2024 hypertension rate at 24%, spurring lipid and hs-troponin utilization. These epidemiological realities cement clinical chemistry dominance while pushing molecular panels into routine algorithms, thereby propelling the Germany in-vitro diagnostics market. Laboratories respond by expanding automated core analyzers and high-throughput immunoassay lines to manage specimen inflow efficiently.

The EUR 4.3 billion Hospital Future Fund subsidizes middleware, track automation and interoperable LIS upgrades, enabling bidirectional data flow between labs and the national ePA backbone. DigitalRadar's 33/100 baseline in 2025 highlights untapped efficiency, prompting aggressive modernization projects. Early adopters such as Siemens Healthineers' autonomous robotic core lab in Heidelberg reported 86% cuts in manual steps, trimming turnaround times by 37%. Vendors offering cloud-native middleware and AI-driven quality-control modules gain competitive traction, reinforcing software as a growth lever within the Germany in-vitro diagnostics market.

A 2024 Association for Molecular Pathology survey found 73% of German labs lacked full clarity on IVDR rules, and 41% had already deferred new-test launches. Although deadlines now stretch to 2027-2029, high-risk assay dossiers still demand costly performance studies and Notified-Body audits. Regulation 2024/1860 additionally imposes six-month stock-out alerts, compelling vendors to fortify supply chains. Compliance investments divert R&D budgets, tempering short-term innovation across the Germany in-vitro diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Clinical chemistry anchored 25% of 2024 revenue, a cornerstone for electrolyte, liver-function and metabolic panels within the Germany in-vitro diagnostics market size. Routine volumes sustain platform investments, whereas immuno-diagnostics extend insights into infectious and autoimmune states. Molecular diagnostics, propelled by rapid PCR and liquid-biopsy workflows, logs a 9.05% CAGR, and CleanNA's CE-IVD cfDNA kit broadens oncology and prenatal applications.

Roche's 125-test pipeline underscores traction in oncology, neurology and cardiometabolic panels. As precision-medicine guidelines mature, labs integrate comprehensive sequencing with reflex immunohistochemistry, fast-tracking personalized therapies. Consequently, the Germany in-vitro diagnostics market enjoys a dynamic mix: stabilized baseline chemistry plus high-velocity molecular segments.

Immunoassays delivered 34% of 2024 turnover, their extensive menu and mature analyzer fleet yielding predictable reagent pull-through despite pricing pressure. PCR's versatility anchors infectious-disease surveillance, while isothermal NAAT grows in near-patient flu-RSV combos. Next-generation sequencing propels double-digit gains and lifts the Germany in-vitro diagnostics market size for complex genomic profiling.

Automation developments, such as MGI Tech's PrepALL liquid handler and Smart 8 pipetting station, trim sample prep lead times by up to 40%, boosting laboratory throughput. Mass spectrometry progresses from toxicology into endocrinology with tandem-MS steroid panels, whereas flow cytometry standardizes immunophenotyping protocols. Converging technologies thus raise analytical depth while safeguarding reagent uptime across the Germany in-vitro diagnostics market.

Reagents and kits furnished 69% of 2024 revenue, the recurrent-consumable model sustaining vendor cash flow within the Germany in-vitro diagnostics market share. Instrument sales follow replacement cycles, with middleware upgrades bundling connectivity and cybersecurity layers.

Software and services accelerate at 10.50% CAGR as labs digitize workflows. UniteLabs secured EUR 2.77 million seed to integrate heterogeneous devices into a single operating stack, slashing manual data transfers in biotech labs. Predictive-maintenance modules lower unplanned downtime, and cloud-based analytics generate actionable population insights, increasing the Germany in-vitro diagnostics market value beyond physical assay delivery.

The Germany In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, and More), Technology (PCR, NGS, and More), Product (Instruments, and More), Usability (Disposable IVD Devices and More), Setting (Centralised Laboratories and More), Application (Infectious Disease, Diabetes, and More), and End-Users (Independent Diagnostic Laboratories and More). The Market Forecasts are Provided in Terms of Value (USD).