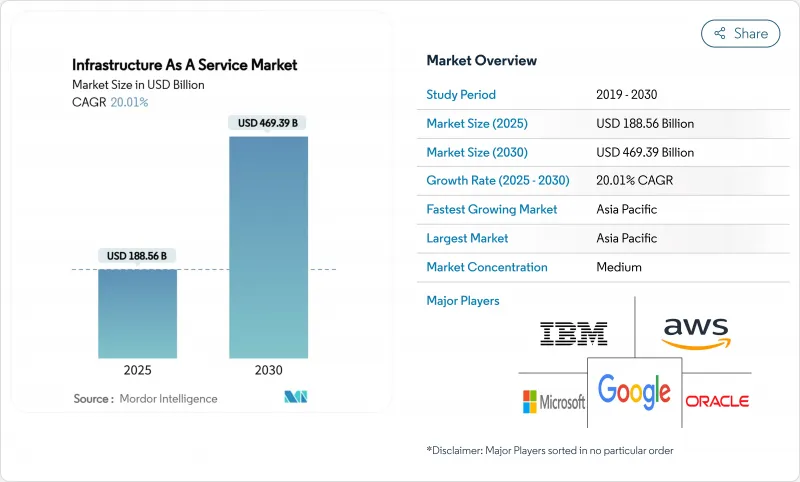

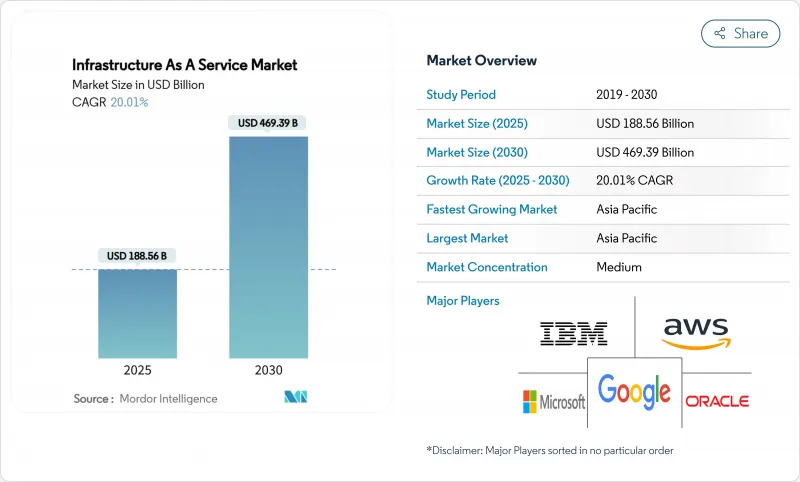

세계의 IaaS(Infrastructure As A Service) 시장 규모는 2025년 1,885억 6,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 20.01%로 확대되어, 2030년까지 4,693억 9,000만 달러에 이를 것으로 예측됩니다.

발전 AI 교육, 가속화된 기업의 하이브리드 전환, 연간 2,500억 달러 이상의 하이퍼스케일러 설비 투자에서의 수요가 이 궤도를 뒷받침합니다. 액체 냉각 데이터센터 설계, 5G 대기 시간을 지원하는 에지 배치, 주권 AI 이니셔티브가 결합되어 투자 수준이 높은 수준을 유지하고 있습니다. 하이퍼스케일러가 지역의 용량을 추구하는 한편, 국내 공급자는 데이터 거주 의무화를 활용하기 때문에 경쟁이 격화되고 있습니다. 사업자는 송전망의 제약을 완화하고 엄격한 지속가능성 목표를 달성할 필요가 있기 때문에 자연에너지 전력구매계약은 장기화되고 규모도 확대되고 있습니다. 클라우드 인프라 시장은 지리적으로 분산되어 AI에 대응한 성장이라는 다음 단계로 들어갑니다.

일반 AI 교육 클러스터는 칩당 700W의 GPU 랙을 필요로 하며, 2024년 데이터홀의 10%에서 2025년에는 20%로 액체 냉각 채택을 추진할 것으로 추정됩니다. 하이퍼스케일러는 현재 1MW 액체 냉각 랙을 중심으로 캠퍼스를 재설계하고 변환 손실을 줄이기 위해 400V DC 배전을 표준화하고 있다고 DataCenterFrontier는 말합니다. 데이터센터 사업자의 거의 40%가 AI 워크로드를 호스팅하기 위해 2026년까지 액체 냉각을 사용할 계획입니다. 이러한 기술적 변화는 시설 설계도를 재구성하고 클라우드 인프라 시장 전반에 걸쳐 AI 대응 설계가 기본 요건이 되었습니다.

기업은 현재 비용과 컴플라이언스의 균형을 맞추기 위해 워크로드를 여러 클라우드에 분산시키고 있습니다. 2024년 IBM에 의한 64억 달러 HashiCorp 인수는 멀티클라우드 오케스트레이션의 자동화를 심화시킵니다. Oracle과 Google의 멀티클라우드 제휴를 통해 Google 리전 내에서 Oracle 데이터베이스의 이그레스 비용이 필요하지 않아 워크로드의 이식성에 대한 오랜 장벽이 없어졌습니다. 은행의 도입은 특히 진행되고 있으며, 70%의 금융기관이 데이터 상주 규칙 및 운영 내결함성 테스트에 힘입어 시험적인 도입에서 전환하고 있습니다. 하이브리드 패턴이 확대됨에 따라 전문 서비스 제공업체는 거버넌스 및 보안 자문에서 새로운 수익을 얻어 클라우드 인프라 시장의 선순환을 강화하고 있습니다.

데이터센터는 2023년에 이미 미국 전력의 4.4%를 소비했습니다. 2028년에는 이 비율이 12%에 달할 가능성이 있어 기존의 송전망에 부담이 걸립니다. 한때 1대 허브였던 버지니아주 북부와 텍사스는 현재 메가와트의 할당을 제한하고 있으며, 사업자는 새로운 용량을 찾고 인디애나와 미시시피로 이동하고 있습니다. 아일랜드에서는 2030년까지 국가 전체 전력의 최대 70%가 디지털 부하로 향할 것으로 예상되며 일부 카운티에서는 모라토리엄이 시행되고 있습니다. 사업자는 시설의 전력 사용량을 95% 삭감하는 액침 냉각으로 대응하고 있지만, 이러한 개수에는 새로운 자본과 건설 스케줄의 연장이 필요합니다. 따라서 전력 부족은 클라우드 인프라 시장의 단기적인 확대를 늦추고 있습니다.

퍼블릭 클라우드는 2024년 매출의 71.0%를 차지했으며 10년에 걸친 On-Premise 스택의 전환을 반영합니다. 그러나 하이브리드층은 규제산업이 On-Premise 컨트롤과 오프프레미스 스케일을 결합하여 2030년까지 연평균 복합 성장률(CAGR)이 24.0%로 가장 빠른 속도를 기록합니다. 금융 서비스 리더는 하이브리드 설정이 규제 당국의 감사를 통과하면서 고객 경험 목표를 달성할 수 있다고 평가합니다. 하이브리드 구축의 클라우드 인프라 시장 규모는 2030년까지 1,420억 달러에 달할 것으로 예측되고 있으며, 지연에 영향을 받기 쉬운 워크로드와 컴플라이언스를 중시하는 워크로드의 균형을 잡는 데 있어서 하이브리드가 중요한 역할을 담당하고 있는 것이 부각되고 있습니다.

AWS Outposts 및 Azure Stack과 같은 프라이빗 연결 옵션의 급증은 이 하이브리드 흐름을 지원합니다. Aurora의 CME Group의 Google Cloud 비공개 리전은 미션 크리티컬 거래를 로컬로 유지하면서 퍼블릭 클라우드 도구를 활용하는 방법을 보여줍니다. IBM의 HashiCorp와 계약에 의해 강화된 다면적 오케스트레이션 소프트웨어는 복잡성의 장벽을 완화합니다. 성숙도가 높아짐에 따라 클라우드 인프라 업계에서는 도입 의사 결정을 두 가지 대안이 아닌 포트폴리오로 파악하는 경향이 커지고 있습니다.

IaaS(Infrastructure As A Service) 시장은 배포 형태(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 서비스 유형(Compute As A Service(CaaS), Storage As A Service(STaaS), Database/Analytics As A Service(DBaaS) 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 텔레콤, 헬스케어 및 생명과학), 지역으로 구분됩니다.

아시아태평양은 2024년 세계 매출의 43.2%를 차지했으며 중국, 일본, 인도 정부 AI 프로그램이 국내 클라우드에 보조금을 투입하고 있기 때문에 CAGR은 가장 빠른 21.4%를 유지하고 있습니다. 중국의 East Data-West 이니셔티브만으로도 매년 4,000억 위안이 8개의 메가 클러스터에 투입되어 컴퓨팅을 내륙부로 재분배하여 해안부의 혼잡을 완화하고 있습니다. 일본은 AWS의 150억 달러와 Oracle의 80억 달러의 서약을 통해 2030년까지 데이터센터의 가치로 2조엔(134억 달러)에 가까워집니다. 인도는 NTT에 의한 15억 달러의 확장과 디지털 인프라를 우대하는 현지 세제 우대 조치로부터 이익을 얻습니다.

북미는 여전히 2위의 거점이지만, 레거시 거점이 포화 상태에 있기 때문에 상대적인 성장은 둔화하고 있습니다. 에너지 제한으로 인해 프로젝트가 간과되는 주로 돌아갑니다. AWS는 인디애나 주에 110억 달러, 컴패스는 미시시피 주에 100억 달러의 캠퍼스 건설에 착공, STACK은 버지니아 주 북부에 1GW 이상의 투자를 수행합니다. 캐나다의 디지털 앰비션 프로그램이 연방 정부의 클라우드 도입을 가속합니다.

유럽에서는 수요와 탄소 중립 목표가 균형을 이룹니다. DORA와 같은 규제로 인해 금융기업은 공급업체의 다양화를 강요받는 반면, 더블린이나 암스테르담과 같은 전통적인 장소에서는 국가의 에너지 상한에 따라 용량이 제한됩니다. 베를린, 바르샤바, 오슬로, 취리히, 밀라노, 비엔나, 마르세유와 같은 대체 도시는 신재생 에너지에 의한 송전망과 지원적인 허가 제도 덕분에 대두하고 있습니다. EU는 2030년까지 제로카본 데이터센터를 목표로 하고 있으며, 열재이용 체계와 해상풍력발전과의 제휴에 투자에 박차를 가해 클라우드 인프라 시장의 다음 단계를 형성합니다.

The Infrastructure As A Service Market size is estimated at USD 188.56 billion in 2025, and is expected to reach USD 469.39 billion by 2030, at a CAGR of 20.01% during the forecast period (2025-2030).

Demand from generative-AI training, accelerating enterprise hybrid migrations, and hyperscaler capital expenditure above USD 250 billion per year underpin this trajectory. Liquid-cooled data-center designs, edge deployments supporting 5G latency, and sovereign AI initiatives together keep investment levels high. Competition intensifies as hyperscalers chase regional capacity while domestic providers leverage data-residency mandates. Power-purchase agreements for renewables are growing in length and scale because operators need to mitigate grid constraints and meet tightening sustainability targets. Collectively, these forces propel the cloud infrastructure market into its next phase of geographically distributed, AI-ready growth.

Generative-AI training clusters require GPU racks drawing 700 W per chip, pushing liquid cooling adoption from 10% of data halls in 2024 to an estimated 20% in 2025. Hyperscalers now redesign campuses around 1 MW liquid-cooled racks, standardizing 400 V DC power distribution to curtail conversion losses, DataCenterFrontier. Enterprises echo the trend: nearly 40% of data-center operators plan to use liquid cooling by 2026 to host AI workloads. These technical shifts reshape facility blueprints, making AI-ready designs a default requirement across the cloud infrastructure market.

Organizations now spread workloads across multiple clouds to balance cost and compliance. IBM's USD 6.4 billion HashiCorp acquisition in 2024 deepens automation for multi-cloud orchestration. Oracle's and Google's multicloud tie-up eliminates egress fees for Oracle Database inside Google regions, removing a long-standing barrier to workload portability. Banking adoption is especially strong: 70% of institutions have moved beyond pilots, spurred by data-residency rules and operational-resilience tests. As hybrid patterns scale, specialized service providers find new revenue in governance and security advisory, reinforcing a virtuous cycle for the cloud infrastructure market.

Data centers already drew 4.4% of US electricity in 2023; the share may hit 12% by 2028, stressing legacy grids. Northern Virginia and Texas, once prime hubs, now ration megawatt allocations, sending operators to Indiana or Mississippi for fresh capacity. Ireland anticipates up to 70% of national power heading to digital loads by 2030, prompting moratoriums in some counties. Operators respond with immersion cooling that cuts facility power use by 95%, yet those retrofits demand fresh capital and extended build timelines. Limited electricity, therefore, slows the near-term expansion of the cloud infrastructure market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Public cloud held 71.0% of revenue in 2024, a reflection of a decade-long migration away from on-premises stacks. The hybrid tier, however, records the fastest 24.0% CAGR through 2030 as regulated industries mesh on-prem control with off-prem scale. Financial-services leaders credit hybrid setups for meeting customer-experience targets while passing regulatory audits. The cloud infrastructure market size for hybrid deployments is projected to reach USD 142 billion by 2030, underscoring its role in balancing latency-sensitive and compliance-critical workloads.

A sharp increase in private connectivity options such as AWS Outposts and Azure Stack supports this hybrid wave. CME Group's private Google Cloud region in Aurora illustrates how mission-critical trading stays local yet leverages public-cloud tooling. Multifaceted orchestration software-boosted by IBM's HashiCorp deal-lowers complexity barriers. As maturity rises, the cloud infrastructure industry increasingly views deployment decisions as a portfolio exercise rather than a binary choice.

The Infrastructure As A Service Market is Segmented by Deployment Mode (Public Cloud, Private Cloud and Hybrid Cloud), Service Type(Compute As A Service (CaaS), Storage As A Service (STaaS), Database / Analytics As A Service (DBaaS) and More), End-User Industry(BFSI, IT and Telecom, Healthcare and Life Sciences) and Geography.

Asia Pacific owns 43.2% of global revenue in 2024 and sustains the fastest 21.4% CAGR as sovereign AI programs in China, Japan, and India funnel subsidies into domestic clouds. China's East Data-West initiative alone channels CNY 400 billion annually toward eight megaclusters, redistributing computing inland and lowering coastal congestion. Japan approaches JPY 2 trillion (USD 13.4 billion) in data-center value by 2030, buoyed by AWS's USD 15 billion and Oracle's USD 8 billion pledges. India gains from NTT's USD 1.5 billion expansion and local tax incentives favoring digital infrastructure.

North America remains the second-largest base but sees relative growth slow as legacy hubs saturate. Energy limitations redirect projects to overlooked states: AWS earmarks USD 11 billion for Indiana, Compass breaks ground on a USD 10 billion Mississippi campus, and STACK commits over 1 GW in Northern Virginia. Canada's Digital Ambition program accelerates federal cloud adoption, propelled by Shared Services Canada's brokerage role.

Europe balances demand with carbon-neutral targets. Regulations such as DORA compel financial firms to diversify providers while national energy caps limit capacity in traditional locations like Dublin and Amsterdam. Alternative metros-Berlin, Warsaw, Oslo, Zurich, Milan, Vienna, and Marseille-rise thanks to renewable grids and supportive permitting regimes. The EU's aim for zero-carbon data centers by 2030 spurs investment in heat-reuse schemes and offshore wind tie-ins, shaping the next phase of the cloud infrastructure market.