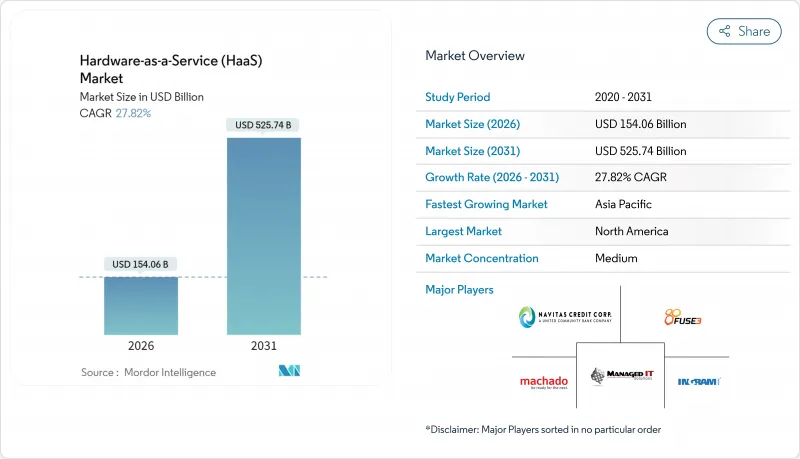

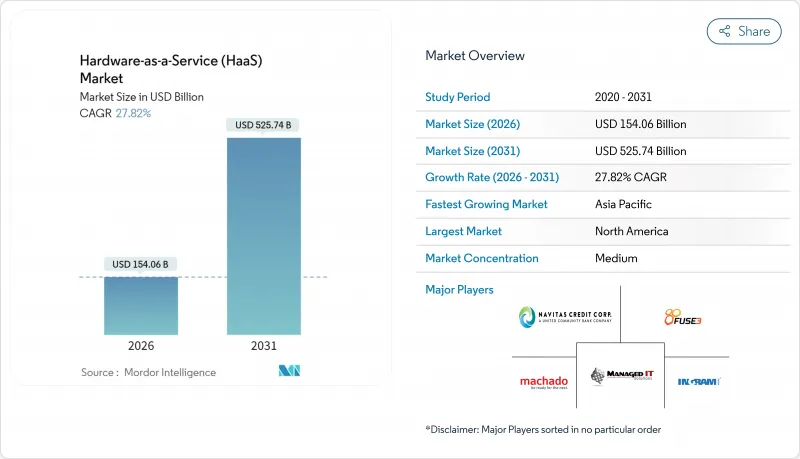

서비스형 하드웨어 시장은 2025년 1,205억 4,000만 달러로 평가되었으며, 2026년 1,540억 6,000만 달러에서 2031년까지 5,257억 4,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 27.82%로 전망됩니다.

이러한 급성장은 기업이 자본 집약적인 하드웨어 구매를 예측 가능한 구독 모델로 전환하고 있음을 반영하며 하이브리드 워크의 보안 요구사항과 CFO가 요구하는 운영 비용의 유연성에 대한 지향으로 가속화되고 있습니다. 캐나다의 국내 슈퍼컴퓨팅용 17억 캐나다 달러 예산 배분 등 국가 주도 AI 프로그램이 국내 인프라 수요를 자극하는 한편, 미국 CHIPS 및 과학법에 의한 500억 달러 인센티브는 현금을 고갈시키지 않고 공장을 근대화하기 위해 제조업체를 구독형 로보틱스로 이동시킵니다. 자산의 담보증권화는 서비스형 하드웨어 시장을 확대하고 있으며, DLL사는 2024년에 21억 5,000만 달러의 증권을 발행함으로써 공급자의 자금조달 비용이 저하되어 경쟁력 있는 가격 설정이 가능하게 되었습니다. EU의 순환형 경제 규제도 이러한 모델이 의무화된 내구성 및 수리 가능성 기준과 부합하기 때문에 추가적인 촉진요인이 되고 있습니다.

2024년 구독 모델은 미국 내 설비 취득의 54%를 차지하면서 임대가 구입을 상회했으며 운용 경비로의 전환이 현저합니다. 구독 계약은 전략적 프로젝트에 대한 자본을 해방하고 급속한 감가상각으로부터 구매자를 보호합니다. Dell APEX 고객은 고객센터 업무가 50% 절감되고 지원 비용이 30% 감소했다고 보고했으며, 성과 지향적인 파트너십이 일시적인 판매를 대체하고 있음을 보여줍니다. 이 장점은 진부화가 빠른 업계에서 더욱 증폭되고 서비스형 하드웨어 시장은 기술 리스크에 대한 전략적 헤지 수단이 되고 있습니다.

하이브리드 워크는 엔드포인트의 위협 노출을 증가시키고 업데이트 주기를 4년 미만으로 단축시킵니다. HP는 향후 디코딩 위험에 대항하기 위해 양자 내성 펌웨어를 도입할 예정이며 이는 장치 업데이트에 내장된 보안 프리미엄을 강조합니다(HP.COM). 중소기업의 70%가 영구적인 원격 근무 방침을 계획하고 있으며 이는 관리형 업데이트 서비스의 필요성을 높이고 있습니다.

OECD는 중소기업이 구독 제안을 평가하는 자금 조달 기술과 인적 자원이 부족하기 때문에 디지털 격차가 해소되지 않았다고 지적합니다. 이러한 불일치가 비용을 중시하는 지역에서의 도입을 늦추고 있지만, 프로바이더가 제공하는 평가 툴이나 정부 보조금에 의해 인식 격차는 축소되고 있습니다.

2025년 시점에서 서비스형 디바이스(DaaS)는 서비스형 하드웨어 시장에서 31.74%의 점유율을 차지했습니다. 한편 서비스형 로봇(RaaS)은 소규모 공장 자동화와 저가 협동 로봇의 보급을 배경으로 29.35%라는 가장 높은 CAGR을 기록하고 있습니다. 서비스형 GPU(GPU-as-a-Service)는 서비스형 하드웨어 시장에서 AI 워크로드의 확대에 따라 성장하고 있으며, GPU 구독 시장은 2025년 43억 1,000만 달러에서 2031년에는 498억 4,000만 달러에 이를 것으로 예측되고 있습니다. 전문 서비스는 가동률 향상을 도모하는 도입, 감시 및 최적화 기능으로 이러한 하드웨어 제공을 종합적으로 지원합니다.

구독 혁신은 플랫폼 수준의 서비스로도 확대되고 있습니다. Siemens사의 Senseye는 분당 100만 개 이상의 센서 포인트를 처리하고 예측 분석이 원시 하드웨어를 산업용 성능 보증으로 전환하는 방법을 제시합니다. 이러한 아키텍처의 전환은 가치를 소유에서 사용으로 전환하고 서비스형 하드웨어 시장은 성과 기반 경제에 뿌리를 두고 분석과 금융 전문 지식을 결합한 벤더에게 경쟁 우위가 기울고 있습니다.

2025년 시점에서는 온프레미스 도입이 44.85%의 점유율을 차지하였으며 이는 금융이나 의료 등 업계에서의 컴플라이언스나 레이턴시에 대한 민감성을 뒷받침하고 있습니다. 그러나 로컬 제어와 클라우드의 신축성을 융합하는 하이브리드 및 서비스형 네트워크(NaaS) 모델은 25.9%의 연평균 복합 성장률(CAGR)로 계속 성장하고 있습니다. Lenovo사의 ThinkAgile MX455 V3는 AI 추론을 가장자리에 배치하면서 트레이닝 워크로드를 Azure에 버스트함으로써 워크로드 이식성이 현대 조달을 정의하는 사례를 보여줍니다.

클라우드 관리 하드웨어 서비스는 용량 급증 대응 및 업데이트 단순화에 여전히 중요하지만 데이터 주권법은 특정 워크로드를 로컬로 유지할 것을 요구합니다. IBM사의 Power Virtual Server 온프레미스 포드는 퍼블릭 클라우드 벤더조차도 주권 요구사항을 충족하기 위해 현지화된 구독을 제공하고 있음을 나타냅니다. 따라서 서비스형 하드웨어 시장은 양자택일의 사고 방식에서 자산이 동적으로 이동할 수 있는 연속체로 전환하고 있습니다.

북미는 2025년 고도의 임대 생태계와 국내 생산을 장려하는 연방 정부의 인센티브에 힘입어 서비스형 하드웨어 시장에서 41.72%의 점유율을 유지했습니다. 미국 내 설비 조달의 절반 이상은 이미 임대를 통해 이루어지고 있으며, 이는 구독의 성숙도를 높이고 있습니다. 반도체 및 첨단 제조를 지원하는 정부 보조금은 유연한 로봇 및 엣지 디바이스에 대한 수요를 확대하고 있습니다.

아시아태평양은 19.15%의 연평균 복합 성장률(CAGR)을 나타내면서 가장 빠르게 성장할 것으로 예상되는 지역입니다. 2027년까지 자본재 지출을 25% 증가시키는 것을 목표로 하는 중국의 설비 업그레이드 계획과 디지털 결제를 지원하는 인도의 데이터센터 확장은 견조한 구독 파이프라인을 창출할 것입니다. 대만의 서버 제조에서의 장점은 서비스형 디바이스(DaaS) 플릿의 세계 물류 체인을 지원하고, 이 지역과 세계의 서비스형 하드웨어(HaaS) 시장의 확대를 더욱 연계하고 있습니다.

유럽의 동향은 조직을 서비스 기반 소유 형태로 이끄는 순환 경제 규제에 달려 있습니다. 2024년 7월 시행된 '지속가능한 제품을 위한 에코디자인 규제'는 장수명화, 수리가능성, 예비 부품의 가용성을 요구하며, 이는 유지보수를 포함한 서비스 계약과 직접적으로 일치합니다. 회수 루프 관리 및 재생품 제공에 뛰어난 공급자는 규제의 뒷받침을 받으며 유럽은 지속가능성이 주도하는 구독 혁신의 실험장으로 자리매김하고 있습니다.

The hardware as a service market was valued at USD 120.54 billion in 2025 and estimated to grow from USD 154.06 billion in 2026 to reach USD 525.74 billion by 2031, at a CAGR of 27.82% during the forecast period (2026-2031).

The leap reflects enterprises converting capital-intensive hardware purchases into predictable subscriptions, a shift accelerated by hybrid-work security mandates and CFO preference for operating-expense flexibility. Sovereign AI programs, such as Canada's CAD 1.7 billion allocation for domestic super-computing, are stimulating home-grown infrastructure demand, while the U.S. CHIPS and Science Act's USD 50 billion incentives are pushing manufacturers toward subscription robotics to modernize plants without depleting cash reserves. Asset-backed securitization is scaling the hardware as a service market, with DLL issuing USD 2.15 billion in notes during 2024, lowering providers' cost of funds and enabling competitive pricing. Circular-economy regulation in the EU is another catalyst because the model aligns with mandated durability and repairability standards.

Leasing overtook purchasing for 54% of U.S. equipment acquisitions in 2024, illustrating the pivot to operational expenses Subscription contracts free capital for strategic projects and shield buyers from rapid depreciation. Dell APEX customers report a 50% cut in help-desk load and 30% lower support costs, showing that outcome-oriented partnerships replace one-off sales. The benefit is amplified in sectors with fast obsolescence, making the hardware-as-a-service market a strategic hedge against technology risk.

Distributed work raises endpoint threat exposure, compressing refresh cycles below four years. HP introduced quantum-resistant firmware to counter future decryption risks, underscoring the security premium now baked into device turnover [HP.COM]. Seventy percent of SMEs plan permanent remote-work policies that intensify the need for managed refresh services.

OECD notes that digital gaps linger because SMEs lack the financing skills and staff capacity to evaluate subscription proposals. The mismatch slows adoption in cost-sensitive regions, though provider-run assessment tools and government grants are shrinking the knowledge gap.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Device-as-a-Service captured 31.74 of of % hardware as a service market share in 2025. Robot-as-a-Service, however, posts the fastest 29.35% CAGR, powered by small-factory automation and cheaper collaborative robots. The hardware as a service market size for GPU-as-a-Service is scaling alongside AI workloads; GPU subscriptions grew from USD 4.31 billion in 2025 to projections of USD 49.84 billion by 2031. Professional services wrap these hardware offerings with deployment, monitoring, and optimization that enhance uptime.

Subscription innovation extends to platform-level services. Siemens Senseye processes more than 1 million sensor points per minute, showing how predictive analytics converts raw hardware into industrial performance guarantees. The architecture shift elevates value from ownership to usage, anchoring the hardware as a service market in outcome-based economics and tilting competitive advantage toward vendors that bundle analytics and financing expertise.

On-premises deployments held a 44.85% share in 2025, a testament to compliance and latency sensitivities in industries such as finance and healthcare. Yet the hybrid/network-as-a-service model grows at 25.9% CAGR because it fuses local control with cloud elasticity. Lenovo's ThinkAgile MX455 V3 lets customers place AI inference at the edge while bursting training workloads to Azure, demonstrating how workload portability defines modern procurement.

Cloud-managed hardware services remain crucial for burst capacity and simplified updates, but data sovereignty law keeps certain workloads local. IBM's Power Virtual Server on-premise pod shows that even public-cloud vendors are packaging localized subscriptions to satisfy sovereignty mandates. The hardware as a service market is therefore shifting from an either-or mindset to a continuum where assets can relocate dynamically.

The Hardware As A Service Market Report is Segmented by Offering (Device-As-A-Service, Desktop/PC-as-a-Service, and More), Deployment Mode (On-Premises, Cloud-Managed, Hybrid/Network-as-a-Service), End-User Enterprise Size (Large Enterprises, Smes), End-User Industry (Retail and Wholesale, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 41.72% share of the hardware as a service market in 2025, sustained by sophisticated leasing ecosystems and federal incentives that reward domestic production. Over half of U.S. equipment procurement already flows through leases, reinforcing subscription maturity. Government grants supporting semiconductor and advanced manufacturing multiply demand for flexible robotics and edge devices.

Asia-Pacific is the fastest-growing region, posting a 19.15% CAGR. China's equipment renewal plan that aims for 25% growth in capital goods spending by 2027, and India's data-center expansion to support digital payments, will generate robust subscription pipelines. Taiwan's dominance in server manufacturing supplies the global logistics chain for device-as-a-service fleets, further entwining the region with global hardware as a service market expansion

Europe's trajectory hinges on circular-economy regulations that push organizations toward service-based ownership. The Ecodesign for Sustainable Products Regulation effective July 2024 requires long life, repairability, and spare-parts availability, aligning directly with service contracts that embed maintenance. Providers adept at managing take-back loops and refurbishment enjoy regulatory tailwinds, marking Europe as a laboratory for sustainability-driven subscription innovation.