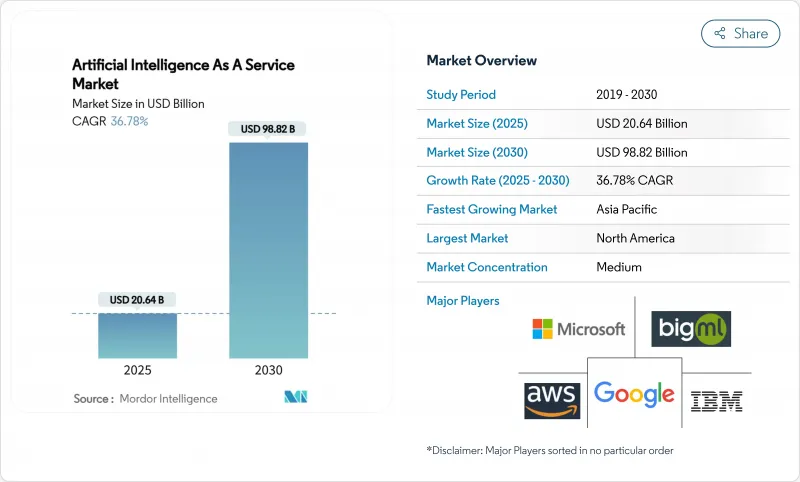

서비스형 AI 시장 규모는 2025년에 206억 4,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 36.78%를 나타낼 것으로 예측되며, 2030년에 988억 2,000만 달러에 달할 전망입니다.

파일럿 프로젝트에서 생산 워크로드로의 급속한 전환이 이러한 성장을 촉진하고 있으며, 기업들은 생성형 AI API를 고객 대응 시스템과 백오피스 시스템에 통합하고 있습니다. 구독형 가격 정책은 중소기업의 진입 장벽을 낮추는 한편, 맞춤형 AI 가속기는 추론 비용을 최대 80%까지 절감하여 공급업체의 마진을 확대하고 있습니다. 일본의 650억 달러 규모 AI 계획과 같은 정부 부양책이 추진력을 더하고, 하이퍼스케일 데이터센터 확장으로 단기 전력 제약에도 불구하고 컴퓨팅 용량이 지속적으로 확장되고 있습니다. 이러한 요인들이 합쳐져 서비스형 인공지능(AIaaS) 시장이 광범위한 산업 간 침투를 향해 나아가고 있습니다.

기업들은 이제 사후 분석보다 선견지명을 중시합니다. AI 기반 분석을 도입한 제조업체는 매출이 61% 증가했으며, 공급망 최적화로 물류 비용을 15% 절감했습니다. 의료 시스템은 방사선 워크플로우 자동화로 5년간 451%의 투자수익률(ROI)을 달성했습니다. 은행들은 사기 탐지 정확도를 높였으며, AI 예측을 통해 2028년까지 1,700억 달러의 추가 수익을 창출할 전망입니다. 실시간 데이터 수집과 에이전트형 AI 시스템이 이러한 추세를 지속시키며, 예측 분석을 AIaaS(Artificial Intelligence as a Service) 시장의 핵심 성장 동력으로 자리매김하고 있습니다.

낮은 진입 장벽을 해소하는 저비용 가격 정책 : 전 세계 중소기업의 생성형 AI 도구 도입률은 18%에 달했습니다. 미국에서는 직원 4명 규모의 기업에서 AI 사용률이 단 1년 만에 4.6%를 나타낼 것으로 예측되며, 5.8%로 증가했습니다. 소매업체는 실질적 성과를 보여줍니다. 타겟은 대규모 자본 지출 없이 생산성을 높이기 위해 400개 매장에 AI 직원 지원 도구를 도입했습니다. AI를 자본 지출(CapEx)에서 운영 지출(OpEx)로 전환함으로써 구독 플랫폼은 마이크로 기업 부문 전반에 걸쳐 AIaaS(Artificial Intelligence as a Service) 시장을 확대하고 있습니다.

AI 워크로드는 인프라 경제성을 압박합니다. 데이터 센터는 2030년까지 미국 전력 소비량의 9%를 차지할 수 있습니다. AI 에너지 수요는 2025년 23GW에 달해 비트코인 채굴을 넘어설 전망입니다. 현재 포춘 2000대 기업의 47%가 급증하는 비용을 통제하기 위해 생성형 AI를 온프레미스에서 개발 중입니다. 전력 가격 상승과 반도체 공급 부족으로 단기적 경제성이 저하되며 AIaaS 시장의 성장이 둔화될 전망입니다.

2024년 퍼블릭 클라우드 제공 방식은 78% 점유율을 유지하며 AIaaS 시장이 하이퍼스케일 인프라에 기반을 두도록 했습니다. 그러나 하이브리드 클라우드는 이사회가 비용 통제를 강화하고 규제 기관이 데이터 거주지 보호를 요구함에 따라 2025-2030년 연평균 32.1% 성장률을 기록하며 확실한 성장 동력으로 부상했습니다. 현재 포춘 2000대 기업 다수는 대규모 모델 훈련은 클라우드에서 수행하되 추론은 온프레미스에서 실행하며, 규모와 주권 사이의 균형을 맞추고 있습니다.

하이브리드 채택은 조달 방향을 전환시킵니다. 병원들은 클라우드 버스트 아키텍처를 도입하여 개인 식별 가능 건강 데이터를 로컬 서버 내에 유지하면서 모델 훈련을 위해 탄력적인 컴퓨팅을 활용함으로써, 가치 실현 시간을 잃지 않으면서 HIPAA 규정을 준수합니다. 제조업체들도 유사한 패턴을 따르며, 지연 시간에 민감한 비전 작업에는 엣지 노드를 활용하고 대량 분석은 지역 클라우드 존으로 이전합니다. 이처럼 규정 준수 및 예산 안정성이라는 두 가지 핵심 과제는 하이브리드 모델을 AIaaS(Artificial Intelligence as a Service) 시장 전망의 중심에 계속 위치시킵니다.

머신러닝 플랫폼이 2024년 매출의 42%를 차지했으나, AI 인프라 서비스는 44.5%의 CAGR로 더 빠르게 성장하고 있습니다. 이러한 변화는 백본 워크로드의 AIaaS 시장 규모 확장에서 컴퓨팅 최적화 클러스터와 네트워킹 패브릭을 핵심으로 자리매김하게 합니다. 맞춤형 칩 채택이 이 추세를 뒷받침합니다. 구글의 TPU와 아마존의 Trainium은 가격 대비 성능을 다중으로 향상시켜 고객이 이러한 실리콘을 제공하는 공급업체를 선호하도록 유도합니다.

소프트웨어 계층도 함께 진화합니다. 관리형 전개 번들은 이제 최적화된 커널과 오케스트레이션 툴링을 결합해 멀티클라우드 확장을 용이하게 합니다. 벤더들은 자체 복구 기능, 자동 패치 적용, 성능 대시보드를 내장해 운영 부담을 줄입니다. 이러한 개선 사항들은 원시 인프라와 개발자 생산성 간의 연결 고리를 강화하여 AIaaS 시장의 이 부문에서 수익 성장세를 공고히 합니다.

서비스형 AI 시장은 전개 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 서비스 유형(머신러닝 플랫폼 서비스, 인지 서비스(NLP, CV, 음성) 등), 조직 규모(중소기업, 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 제조업 등), 지역별로 세분화됩니다.

북미는 초대형 데이터 센터 기반과 깊은 스타트업 생태계에 힘입어 2024년 글로벌 매출의 38%를 차지했습니다. 주요 클라우드 기업들은 2025년 동안 2,500억 달러 이상의 신규 용량을 약속했으나, 2030년까지 미국 데이터 센터 전력 수요가 국가 공급량의 9%에 달할 수 있어 전력망 제약이 다가오고 있습니다. FTC의 클라우드-AI 협약 조사는 경쟁 경계를 재조정할 수도 있습니다.

아시아태평양 지역은 연평균 27.9% 성장률로 가장 빠른 상승세를 기록 중입니다. 일본은 AI 및 반도체 분야에 650억 달러를 배정했으며, 소프트뱅크는 생성형 AI 기반 기술에 9억 6,000만 달러를 투자했습니다. 중국의 알리바바는 클라우드 모델 서비스에 3,800억 위안을 할당했고, 바이트댄스의 볼케이노 엔진은 국내 공개 모델 호출량의 거의 절반을 처리했습니다. 기업 설문조사에 따르면 아시아태평양 지역 기업의 54%가 현재 장기적인 AI 수익 창출을 목표로 하고 있어 시범 운영을 넘어선 심층적 접근을 시사합니다.

유럽은 AI 규제 초안 하에서 혁신과 엄격한 감독을 균형 있게 조화시키며 꾸준히 성장 중입니다. 중동 및 아프리카는 주권적 AI 전략을 추진 : UAE는 2030년까지 해당 분야 가치 463억 3,000만 달러를 예상하며 마이크로소프트가 G42에 15억 달러를 투자합니다. 사우디아라비아의 1,000억 달러 규모 AI 펀드는 지역적 야망을 강조하며, GCC 기업 중 75%가 생성형 모델을 도입해 글로벌 평균을 상회합니다. 저렴한 에너지 접근성과 선제적 정책 프레임워크는 이 지역을 유럽, 아프리카, 남아시아를 연결하는 서비스형 인공지능 시장 진출의 가교 시장으로 자리매김하게 합니다.

The Artificial Intelligence As A Service Market size is estimated at USD 20.64 billion in 2025, and is expected to reach USD 98.82 billion by 2030, at a CAGR of 36.78% during the forecast period (2025-2030).

Rapid migration from pilot projects to production workloads fuels this rise as enterprises embed generative-AI APIs in customer-facing and back-office systems. Subscription pricing lowers entry costs for small firms, while custom AI accelerators cut inference expenses by up to 80%, widening margins for providers. Government stimulus packages, such as Japan's USD 65 billion AI plan, add momentum, and hyperscale data-center build-outs keep compute capacity expanding despite near-term power constraints. Together, these forces push the Artificial Intelligence as a Service market toward broad, cross-industry penetration.

Enterprises now prize foresight over hindsight. Manufacturers using AI-driven analytics posted 61% revenue premiums, while supply-chain optimization shaved 15% off logistics costs. Healthcare systems gained 451% ROI over five years by automating radiology workflows. Banks boosted fraud-detection accuracy and see USD 170 billion additional profits by 2028 through AI forecasting. Real-time data ingestion plus agentic AI systems sustain this momentum, positioning predictive analytics as a core growth engine for the Artificial Intelligence as a Service market.

Low-commitment pricing dismantles historic entry barriers. Global SME adoption of generative-AI tools reached 18%. In the United States, AI usage among firms with four workers rose from 4.6% to 5.8% in a single year. Retailers illustrate practical returns: Target deployed AI employee-assistance tools across 400 stores to raise productivity without large capital outlays. By turning AI from capex to opex, subscription platforms broaden the Artificial Intelligence as a Service market across micro-enterprise segments.

AI workloads strain infrastructure economics. Data centers may draw 9% of the United States' electricity by 2030. AI energy needs are set to top Bitcoin mining in 2025, reaching 23 GW. Forty-seven percent of Fortune 2000 firms now develop generative AI on-premises to tame runaway bills. Rising power prices plus tight chip supply lower near-term affordability and clip growth in the Artificial Intelligence as a Service market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Public-cloud delivery retained 78% share in 2024, ensuring the Artificial Intelligence as a Service market remains anchored to hyperscale infrastructure. Hybrid cloud, however, is the clear growth engine, registering a 32.1% CAGR for 2025-2030 as boards demand tighter cost control and regulators press for data residency safeguards. Many Fortune 2000 firms now train large models in the cloud yet run inference on-premises, balancing scale with sovereignty.

Hybrid uptake redirects procurement. Hospitals adopt cloud-burst architectures to keep personally identifiable health data within local servers while exploiting elastic compute for model training, meeting HIPAA rules without losing time-to-value. Manufacturers mirror this pattern, reserving edge nodes for latency-sensitive vision tasks while pushing bulk analytics to regional cloud zones. The twin priorities of compliance and budget certainty thus keep hybrid models central to the Artificial Intelligence as a Service market outlook.

Machine-learning platforms supplied 42% of 2024 revenue, but AI infrastructure services are growing faster at 44.5% CAGR. This shift places compute-optimized clusters and networking fabrics at the heart of the Artificial Intelligence as a Service market size expansion for backbone workloads. Custom chip adoption underpins the trend: Google's TPUs and Amazon's Trainium deliver multi-fold price-performance gains, prompting clients to favor providers offering such silicon.

Software layers evolve in lockstep. Managed distribution bundles now pair optimized kernels with orchestration tooling to ease multi-cloud scaling. Vendors embed self-healing functions, automated patching, and performance dashboards to shrink operational toil. Together, these enhancements tighten the nexus between raw infrastructure and developer productivity, reinforcing the revenue trajectory in this segment of the Artificial Intelligence as a Service market.

The Artificial Intelligence As A Service Market is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Service Type (Machine-Learning Platform Services, Cognitive Services (NLP, CV, Speech) and More), Organisation Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (BFSI, Retail and E-Commerce, Manufacturing and More) and Geography

North America held 38% of global revenue in 2024, buoyed by an installed base of hyperscale data centers and a deep startup ecosystem. Cloud majors pledged more than USD 250 billion in fresh capacity during 2025, yet grid constraints loom as US data-center power draw may hit 9% of national supply by 2030. FTC probes into cloud-AI pacts could also recalibrate competitive boundaries.

Asia-Pacific charts the fastest ascent with a 27.9% CAGR. Japan earmarked USD 65 billion for AI and chips, and SoftBank invested USD 960 million in a generative-AI backbone. China's Alibaba allocated 380 billion yuan to cloud model services, while ByteDance's Volcano Engine processed nearly half of the country's public model calls. Corporate surveys show 54% of APAC firms now target long-term AI payouts, signalling depth beyond pilot activity.

Europe grows steadily, balancing innovation with strict oversight under draft AI regulations. The Middle East and Africa ride sovereign-AI strategies: the UAE expects USD 46.33 billion in sector value by 2030 as Microsoft injects USD 1.5 billion into G42. Saudi Arabia's USD 100 billion AI fund underscores regional ambition, and 75% of GCC enterprises deploy generative models, eclipsing global averages. Access to affordable energy and proactive policy frameworks position the region as a bridge market linking Europe, Africa, and South-Asia for Artificial Intelligence as a Service market rollouts.