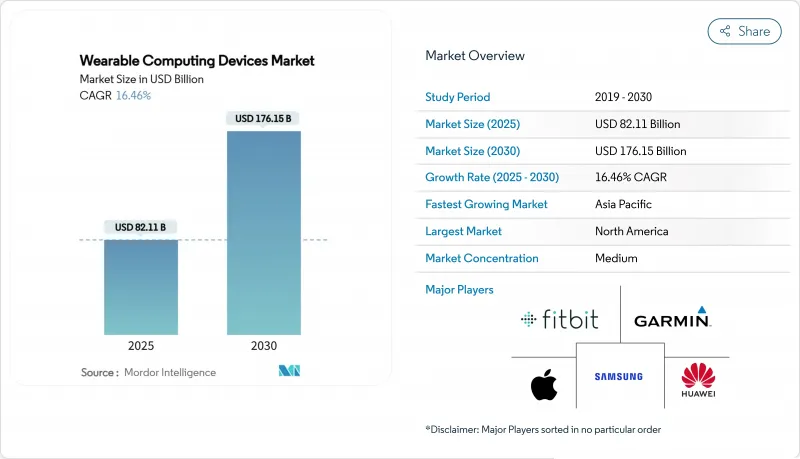

웨어러블 컴퓨팅 디바이스 시장은 2025년에 821억 1,000만 달러로 추정되고, 2030년에는 1,761억 5,000만 달러로 성장할 것으로 예측됩니다.

센서 소형화, 배터리 효율 칩셋, 스마트폰 에코시스템과의 긴밀한 통합으로 소비자와 기업 모두에게 매력이 퍼지고 있습니다. 비침습적인 대사 모니터링과 FDA를 통한 ISO 13485:2016 준수는 의료 등급 제품의 규제를 개선하고, 울트라 와이드 밴드로 구축된 정확한 위치 정보 기능은 산업 안전 이용 사례를 확대하고 있습니다. 공급망의 탄력성, 특히 마이크로 LED 컴포넌트 주변은 여전히 전략적 요건이며, 데이터 공유 규칙이 강화되는 동안 프라이버시 중심 설계가 전면에 나오고 있습니다. 이러한 요소를 종합하면 경쟁 요인은 높은 경쟁 압력을 유지하고 하드웨어, 소프트웨어 및 의료 서비스 계약을 융합시킨 생태계 중심 전략을 장려합니다.

TDK의 솔리드 스테이트 배터리는 1,000Wh/l의 에너지 밀도를 달성해, 히어러블이나 워치의 런타임을 연장하면서 소형화를 실현합니다. 칩 패키징의 진보에 의해 1장의 기판에 복수의 센서를 탑재할 수 있게 되어, 애플사의 특허에서는 사용자의 상황에 따라 전력과 열을 다이나믹하게 조정하는 것으로, 케이스를 두껍게 하지 않고 효율을 높여줍니다. 청화대학교에서 개발된 수성 암모늄 이온 마이크로 배터리는 피부에 접촉하는 장치에 적합한 보다 안전하고 유연한 화학을 입증합니다. 이러한 비약적인 진보로 상시 점등하는 건강 지표와 최소한의 전력만을 소비하는 생생한 마이크로 LED 디스플레이가 실현됩니다. 그 결과, 일상적인 액세서리에 지속적인 모니터링이 널리 받아들여집니다.

나중에 굳은살형 심근증으로 진단된 소비자의 시계가 심장의 이상을 보인 것으로 주목된 바와 같이, 웨어러블은 임상 수준의 사건을 검출하게 되어 왔습니다. 갤럭시 AI는 현재 수면, 스트레스, 활동을 문맥화하는 '에너지 점수' 인사이트를 제공하여 개인 코칭을 실현하고 있습니다. 홍콩 대학의 인센서 컴퓨팅 프로토타입은 생체 신호를 로컬로 처리하여 대기 시간을 단축하고 민감한 데이터의 온라인 노출을 줄입니다. MOTIVATE-T2D 연구의 증거는 트래커를 착용한 당뇨병 환자의 운동 요법에 대한 어드히어런스 향상을 나타내며, 정량화 가능한 건강 증진을 뒷받침합니다. 이러한 움직임은 소비자의 신뢰를 높이고 적극적인 셀프 케어를 정상화합니다.

한 조사에 따르면, 92%의 사용자가 웨어러블 데이터를 공유하는 방법에 대해 명확하지 않고 기밀성이 높은 메트릭을 공유하는 것을 망설이고 있습니다. 소비자용 장비에 대한 HIPAA의 적용 제외는 실시상의 격차를 남겨두고 있으며, 헬스케어 침해는 5년간 55% 증가하여 노출을 강조하고 있습니다. 호주 인권위원회는 어린이용 웨어러블 단말기의 신경 데이터 위험 증가를 경고하고 프라이버시법의 현대화를 요구하고 있습니다. 블록체인 프로토타입은 무단 액세스를 45% 절감하고 감지 시간을 10일 미만으로 단축하지만 비용과 확장성이 장벽으로 남습니다. 시장의 기세는 투명한 동의 흐름과 보안 바이 디자인 아키텍처에 달려 있습니다.

2024년 웨어러블 컴퓨팅 디바이스 시장 점유율은 스마트 워치가 46%를 차지하였고, 종합적인 건강 대시보드와 일상적인 관련성을 확보하는 광범위한 타사 앱 에코시스템이 그 주역이 되고 있습니다. 스마트 워치로 인한 웨어러블 컴퓨팅 디바이스 시장 규모는 바이오 액티브 및 기타 멀티모달 센서가 심박수 이외의 대사 측정도 가능하게 함으로써 꾸준히 성장할 전망입니다. 2030년까지 연평균 복합 성장률(CAGR) 18.5%로 성장하는 귀걸이형 디바이스는 눈에 띄지 않는 폼 팩터 및 온도, 심박수, 음성 명령 기능의 추가에 의해 혜택을 받습니다. 산업용 헤드 마운트 디스플레이는 조선업과 현장 서비스에서 디지털 지시를 중첩하여 지보를 굳혀 측정 가능한 생산성 향상을 촉진합니다. 스마트 의류는 아직 발전 도상이지만, e-skin의 프로토타입에서 태어난 플렉서블 프린트 회로나 섬유 매립 전극이, 재활의 이용 사례를 전진시킵니다. 피트니스 트래커는 유사한 지표를 약간의 고도로 번들하는 엔트리 레벨 시계에서 가격 압력에 노출됩니다.

웨어러블 컴퓨팅 디바이스 업계에서는 신체 장착형 카메라와 외골격이 공공 안전이나 제조업의 피로 경감 등 전문 분야에 공헌하고 있습니다. 시장 진출기업은 오픈 API를 강조하고 있으며 비디오 스트림과 생체역학 데이터가 고용주 대시보드에 반영됩니다. 스마트 글라스는 창고 및 건강 관리 워크플로우에 축 발을 놓아 수동으로 스캔 시간과 오류율을 줄입니다. 공급업체는 초저전력 칩셋에 투자하여 도 렌즈의 변형이 광학 투명도와 배터리 목표를 충족하도록 합니다. 전반적으로, 제품의 다양화는 스마트 워치의 이점을 저하시키지 않으면서 어드레싱 가능한 전체 베이스를 확장하고 웨어러블 컴퓨팅 디바이스 시장 전체의 중층 성장을 지원합니다.

피트니스 및 웰니스는 2024년 웨어러블 컴퓨팅 디바이스 시장 규모의 39%를 차지했으며, 보수 카운트, 수면 스테이징, 온워치 코칭에 대한 소비자의 폭넓은 관심에 의해 지원되고 있습니다. 정액제 피트니스 컨텐츠와의 통합은 보존을 향상시킵니다. CAGR 성장률 19.2%로 예측되는 의료 및 헬스케어 용도에서는 원격 환자 모니터링 프로그램이 지속적인 생체 계측에 상환을 실시하기 때문에 디바이스는 웰니스 액세서리에서 상환 대상의 임상 툴로 이행합니다. 2형 당뇨병과 같은 만성 질환 코호트에서는 웨어러블로 생성된 경보와 원격 진단 프롬프트에 의해 유도되면 측정 가능한 혈당 조절이 개선됩니다. 병원은 수술 후 관리에 패치 기반 센서를 채택하여 침대 옆의 검사를 줄이고 직원의 시간을 확보합니다.

인포테인먼트는 몰입형 오디오로 기세를 유지하고 산업용 기업은 환경 모니터를 배치하여 위험 지역에서의 노출 사고를 줄입니다. 방위 용도로는 생체 인증이나 상황 인식 오버레이 등이 있습니다. 웨어러블 컴퓨팅 디바이스 산업은 교육 분야에도 진출하고 있으며, 여기에는 주의력 추적 헤드셋이 적응 커리큘럼에 정보를 제공합니다. 수요의 수렴을 통해 공급업체는 IEC의 의료 안전 표준 및 견고한 진입 정격을 모두 충족해야 하며 설계 및 품질 보증 의무를 더욱 전문화합니다.

웨어러블 컴퓨팅 장치 시장 보고서는 제품 유형별(스마트 워치, 스마트 웨어, 외골격 등), 최종 사용자별(피트니스 및 웰니스, 인포테인먼트 등), 운영 체제별(watchOS, Harmonyos 등), 연결 기술별(Bluetooth, 셀룰러(LTE, 5G), Wi-Fi 등), 지역별로 분류됩니다.

북미는 보험사가 디바이스를 웰니스 인센티브에 통합하고 임상의가 원격 모니터링 등록을 수락했기 때문에 2024년 웨어러블 컴퓨팅 디바이스 시장에서 34.5%의 점유율을 유지했습니다. 애플, 삼성, 신흥 헬스텍 전문 기업들은 지속적인 바이탈 측정을 커버하는 상환 코드로부터 이익을 얻고 있으며, 소비자의 자기 부담 보험료 지불 의향을 강화하고 있습니다. 데이터 수집에 대한 감시의 눈이 엄격해지고, 벤더는 미국 HIPAA에 준거한 클라우드와 투명성이 높은 동의 플로우를 채용하게 됩니다. 커넥티드 패치를 장착한 심장병 환자의 재입원이 감소하고 있는 것이 의료 시스템의 파일럿 시험에서 실증되어 병원의 조달 의욕이 높아집니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 16.8%로 가장 급성장이 전망되고 있는 지역입니다. 인도의 현지 브랜드는 혈중 산소 농도와 심박수 경고를 포장한 30달러 이하의 스마트 시계를 제공하여 대응 가능한 소비자층을 확대하고 있습니다. 중국은 만성 질환의 원격 감시에 환불을 실시하는 통합 건강 디지털화 정책을 추구하고 의료 등급의 손목 밴드 병원 조달을 장려합니다. 일본은 습도가 높은 환경에서도 편안하게 작업할 수 있는 냉각 웨어러블을 도입하고, 한국의 부품 공급 클러스터는 세계 생산 확장성을 지원합니다. 수입 관세의 영향으로 OEM은 베트남과 인도네시아에 조립을 분산시키고 비용 변동을 완화하고 있습니다.

유럽은 보다 신중한 채용 곡선 하에서 꾸준한 성장을 이루고 있습니다. GDPR(EU 개인정보보호규정)과의 일치는 사용자의 신뢰를 높이지만 문서화 오버헤드를 증가시킵니다. 각국의 의료제도가 만성질환 환자에 대한 장비보조를 시험적으로 실시하더라도 상환 스케줄은 회원국간에 크게 다릅니다. 중동 및 아프리카에서는 사하라 사막 이남 지역에서 인프라 장애물이 높지만 피트니스 연결이 상태 상징이 되는 걸프 국가의 부유층 시장에 잠재력이 있습니다. 라틴아메리카에서는 체육관 문화 및 스마트폰의 보급률이 향상됨에 따라 브라질과 멕시코에 수요 포켓이 기록되고 있습니다. 웨어러블 컴퓨팅 장치 시장은 지역 전반에 걸쳐 의료 정책, 가처분 소득 및 통신 인프라의 성숙도에 의해 형성되고 있습니다.

The wearable computing devices market stands at USD 82.11 billion in 2025 and is projected to advance to USD 176.15 billion by 2030, reflecting a sturdy 16.46% CAGR through the period.

Sensor miniaturization breakthroughs, battery-efficient chipsets, and closer integration with smartphone ecosystems are widening both consumer and enterprise appeal. Non-invasive metabolic monitoring and FDA alignment with ISO 13485:2016 are improving the regulatory path for medical-grade products, while precise location capabilities built on ultra-wideband are expanding industrial safety use cases. Supply-chain resilience, especially around micro-LED components, remains a strategic requirement, and privacy-focused design is moving to the foreground as data sharing rules tighten. Collectively, these factors keep competitive pressure high and encourage ecosystem-centric strategies that blend hardware, software, and health-service subscriptions.

Solid-state batteries from TDK achieve 1,000 Wh/l energy density, cutting size while extending run-time for hearables and watches. Chip packaging advances allow multiple sensors on one substrate, and Apple patents show dynamic power and thermal adjustment based on user context, boosting efficiency without thicker casings. Aqueous ammonium-ion micro batteries developed at Tsinghua University demonstrate safer and flexible chemistry suitable for skin-contact devices. These leaps enable always-on health metrics plus vivid micro-LED displays that draw minimal power. The outcome is a broader acceptance of continuous monitoring in everyday accessories.

Wearables increasingly detect clinical-grade events, highlighted when a consumer's watch flagged cardiac abnormalities later diagnosed as takotsubo cardiomyopathy. Galaxy AI now delivers "Energy Score" insights that contextualize sleep, stress, and activity for personal coaching. In-sensor computing prototypes from the University of Hong Kong process bio-signals locally, lowering latency and reducing exposure of sensitive data online. Evidence from the MOTIVATE-T2D study shows enhanced adherence to exercise regimens among diabetes patients equipped with trackers, supporting quantifiable health gains. These developments deepen consumer trust and normalize proactive self-care.

A study shows 92% of users lack clarity on how wearable data is shared, fueling hesitation about sharing sensitive metrics. HIPAA exclusions for consumer devices leave enforcement gaps, and healthcare breaches rose 55% over five years, underlining exposure. The Australian Human Rights Commission warns of heightened neural-data risk in child-oriented wearables, prompting calls for privacy law modernization. Blockchain prototypes reduce unauthorized access by 45% and cut detection time to under 10 days, but cost and scalability remain barriers. Market momentum hinges on transparent consent flows and security-by-design architectures.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Smartwatches accounted for 46% of wearable computing devices market share in 2024, anchored by comprehensive health dashboards and extensive third-party app ecosystems that secure daily relevance. The wearable computing devices market size attributed to smartwatches is poised to grow steadily as BioActive and other multi-modal sensors enable metabolic readings beyond heart rate. Ear-worn devices, advancing at 18.5% CAGR to 2030, benefit from discreet form factors and the addition of temperature, heart-rate and voice command functions. Industrial head-mounted displays gain ground in shipbuilding and field service by overlaying digital instructions, driving measurable productivity gains. Smart clothing remains nascent, though flexible printed circuits and textile-embedded electrodes from e-skin prototypes advance rehabilitation use cases. Fitness trackers feel price pressure from entry-level watches that bundle similar metrics at little premium.

The wearable computing devices industry sees body-worn cameras and exoskeletons serving specialist verticals such as public safety and manufacturing fatigue mitigation. Market entrants emphasize open APIs so video streams and biomechanical data feed into employer dashboards. Smart glasses pivot to warehouse and healthcare workflows, cutting manual scanning time and error rates. Vendors invest in ultra-low-power chipsets so prescription-lens variants meet optical clarity and battery objectives. Overall, product diversification expands the total addressable base without eroding smartwatch primacy, supporting layered growth across the wearable computing devices market.

Fitness and wellness accounted for 39% of the wearable computing devices market size in 2024, held up by broad consumer interest in step counts, sleep staging, and on-watch coaching. Integration with subscription fitness content strengthens retention. Medical and healthcare applications, forecast to grow 19.2% CAGR, transition devices from wellness accessories to reimbursable clinical tools as remote patient monitoring programs reimburse continuous vitals capture. Chronic-disease cohorts such as Type 2 diabetes show measurable blood-glucose control improvements when guided by wearable-generated alerts and tele-consultation prompts. Hospitals adopt patch-based sensors for post-operative care, reducing bedside checks and freeing staff time.

Infotainment keeps momentum through immersive audio, while industrial firms deploy environmental monitors to cut exposure incidents in hazardous zones. Defense uses include biometric authentication and situational awareness overlays. The wearable computing devices industry also touches education, where attention-tracking headsets inform adaptive curricula. Demand convergence pushes suppliers to meet both IEC medical safety norms and ruggedized ingress ratings, further professionalizing design and quality assurance obligations.

The Wearable Computing Devices Market Report is Segmented by Product Type (Smartwatches, Smart Clothing, Exoskeletons, and More), End User (Fitness and Wellness, Infotainment, and More), Operating System (watchOS, Harmonyos, and More), Connectivity Technology (Bluetooth, Cellular (LTE, 5G), Wi-Fi and More), and Geography.

North America retained 34.5% share of the wearable computing devices market in 2024 as insurers integrated devices into wellness incentives and clinicians embraced remote monitoring enrolment. Apple, Samsung and rising health-tech specialists benefit from reimbursement codes that cover continuous vitals capture, reinforcing consumer willingness to pay out-of-pocket premiums. Heightened scrutiny of data collection pushes vendors to adopt US-based HIPAA-aligned clouds and transparent consent flows. Health-system pilots demonstrate lower readmissions among cardiac patients equipped with connected patches, amplifying hospital procurement interest.

Asia Pacific is the fastest-growing region at 16.8% CAGR to 2030. Local brands in India offer sub-USD 30 smartwatches that still package blood-oxygen and heart-rate alerts, expanding addressable consumer segments. China pursues integrated health-digitization polices that reimburse remote monitoring for chronic diseases, encouraging hospital procurement of medical-grade wristbands. Japan showcases cooling wearables for workforce comfort in humid environments, while South Korea's component supply clusters underpin global production scalability. Import tariffs push OEMs to diversify assembly into Vietnam and Indonesia, mitigating cost swings.

Europe posts steady growth under a more cautious adoption curve. GDPR alignment delivers user trust yet adds documentation overhead. National health systems pilot device subsidies for chronic-care populations, but reimbursement schedules differ widely between member states. Middle East and Africa see potential in affluent Gulf markets where connected fitness is a status symbol, contrasted by infrastructure hurdles in sub-Saharan regions. Latin America records pockets of demand in Brazil and Mexico as gym culture and smartphone penetration improve. Across regions, the wearable computing devices market continues to be shaped by healthcare policy, disposable income and telecom infrastructure maturity.