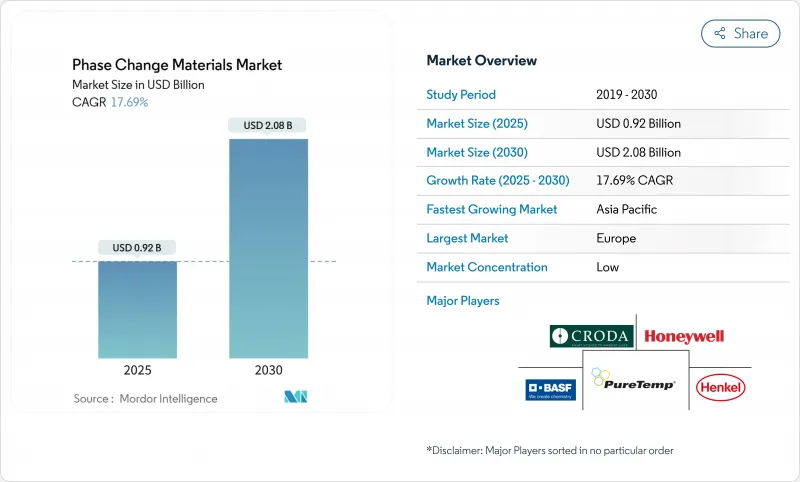

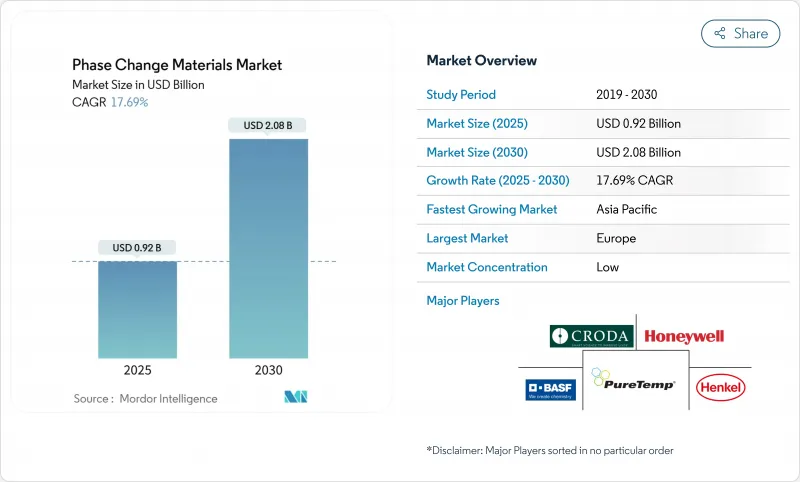

세계의 상변화물질 시장 규모는 2025년 9억 2,000만 달러로, 2030년에는 20억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 17.69%로 예상됩니다.

장기화하는 열파, 넷 제로 건설 목표, 운송의 급속한 전기화로 인해 잠열 축열은 현재 상업 에너지 전략의 중심에 자리 잡고 있습니다. 또한 콜드체인 물류 및 전기자동차 배터리 팩은 운송, 제약, 데이터센터 냉각 등 이 기술의 적용 범위를 확대하고 있습니다. 오랫동안 상분리와 과냉각 문제로 제약을 받은 솔트 하이드레이트는 최근 전도성의 돌파구를 받아 견인력을 늘리고 있습니다. 동시에, 농업 잔류물 유래의 바이오베이스 PCM은 열용량을 희생하지 않고 화재 안전성과 지속가능성 우려에 대처하고, 실험실의 호기심에서 확장 가능한 상업 제품으로 전환하고 있습니다. 아시아태평양에서는 제조업체가 고순도 염수화물과 관련된 공급망 위험을 헤지하기 위해 현지 생산 라인을 증설하고 생산 능력 증진의 지점으로 진화하고 있습니다.

성능에 따른 적합 기준을 통해 건축가는 단단한 단열재를 잠열 축열층으로 대체할 수 있게 되어 경량 벽 내의 피크 냉방 부하를 35-45% 삭감할 수 있게 되었습니다. 미네소타 주에서의 실측 결과는 실내 피크 온도가 5.49℃ 하락하고 부하가 77.8% 오프 피크 시간대로 이동한 것으로 보고되어 규제 당국에 HVAC 절약의 현실적인 증거를 제공합니다. 2027년 EU 리노베이션 목표를 위한 적합 기준치 상승으로 PCM이 들어간 석고 보드와 콘크리트 블록이 더욱 중시되고 상변화물질 시장 전체의 조달량이 증가할 것으로 예측됩니다.

백신, 첨단 생물학적 제제, 정밀 육류는 종종 -0.5℃의 편차를 3일 미만 허용하는 온도 범위를 필요로 합니다. PCM은 외부 전원 없이 이 기간을 72시간으로 연장하여 공항과 세관에서 지연 시 디젤 발전기에 대한 의존도를 줄입니다. 글리세린-물-NaCl 혼합물은 활성 냉각에 비해 이산화탄소 배출량을 30-40% 줄이고 의약품 보존 기간을 15-25% 연장하여 상변화물질 시장 전체에 2자리 수요를 가져오고 있습니다.

파라핀 왁스는 약 170° C 에서 발화하며, 비용을 증가시키고 건강 관련 표시 규제를 유발할 수 있는 브롬계 난연제가 필요합니다. LiNO3와 같은 무기 난연제는 독성 위험이 있습니다. 최근 in-situ 중합 고체-고체 PCM은 누출을 없애고 할로겐 없이 UL94 V-0의 연소성을 클리어하고 있습니다. 보다 광범위한 채택은 이러한 캡슐화의 발전을 확대하고 세계적인 화학 안전 기준을 조화시키는 데 달려 있습니다.

유기 파라핀 왁스는 상변화물질 시장의 수익의 기둥이어서 2024년 세계 매출의 44.19%를 차지합니다. 이점은 성숙한 공급망, 넓은 온도 범위, 건축 패널에 사용되는 매크로 캡슐화 슬래브와의 호환성을 반영합니다. 그러나 이해관계자가 라이프사이클 배출량의 삭감을 추구하는 가운데, 상변화물질 시장은 바이오 유래의 기름, 수지, 지방산 혼합물로 급선회하고 있습니다. 이 신흥 하위 부문은 2030년까지의 CAGR이 19.21% 이상이 될 것으로 예측되며, LEED 크레딧과 생물 유래 재료를 명확하게 추천하는 지자체의 녹색 조달 의무에 뒷받침되고 있습니다.

파라핀 기반 제제는 안정한 결정화와 0-90℃ 범위에서의 융점의 조정이 용이하기 때문에 2024년 상변화물질 시장 수익의 41.49%를 차지했습니다. 그럼에도 염수화물은 이 히에랄키를 붕괴시키는 기세이며, 2030년까지 CAGR은 18.04%로 확대됩니다. 높은 체적 열용량(최대 350kJ/L)과 탄소 첨가제에 의한 열전도율의 개선으로, 염수화물은 부품의 크기와 중량의 축소를 가능하게 하고 있습니다. 결과적인 밀도의 이점은 사용 가능한 설치 영역에 제한이 있는 전기자동차 배터리 슬리브 및 소형 데이터센터 랙에 특히 매력적입니다.

2024년 세계 매출의 32.86%는 유럽이 차지했니다. 이는 EU의 건축물 에너지 성능 지령에 의해 지원되며, 이 지령은 신축과 대규모 리노베이션 모두에 준 네트 제로 목표 달성을 의무화하고 있습니다. 독일과 북유럽에서는 PCM을 외벽 단열 시스템에 통합한 후 HVAC 에너지가 20-35% 절약된 것을 조기 채용 기업이 보여주고 있습니다. 탄소거래와 그린본드 적격성에 관한 규제의 명확화에 의해 PCM을 다용하는 건축재료에 대한 자금이 계속 끌려가고, 상변화물질 시장에서 유럽의 주도적 지위가 굳어지고 있습니다.

아시아태평양은 가장 급성장하고 있는 지역으로 2030년까지 매년 18.98%의 확대가 전망되고 있습니다. 중국의 적극적인 히트펌프 도입은 '히트펌프의 미래' 로드맵 하에서 장려되는 시너지 효과로 피크 전력 수요를 절약함으로써 PCM 축열을 보완합니다.

북미에서는 엄격한 에너지 규제 갱신과 폭발적으로 성장하는 전기자동차 부문이 결합되어 있습니다. 미국 데이터센터 사업자는 현장 에너지 저장에 대한 세액 공제를 목표로 PCM 기반 열 버퍼를 시험적으로 도입하고 서버의 열 스파이크를 흡수하여 냉동기의 시작을 연기하고 있습니다.

The Phase Change Materials Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 17.69% during the forecast period (2025-2030).

Lengthening heat waves, net-zero construction goals, and rapid electrification in transport now place latent-heat storage at the center of commercial energy strategies. Mandatory building-energy codes in Europe and North America are accelerating integration, while cold-chain logistics and electric-vehicle battery packs expand the technology's reach into transportation, pharmaceuticals, and data-center cooling. Longly constrained by phase-separation and supercooling issues, salt hydrates are gaining traction after recent conductivity breakthroughs. At the same time, bio-based PCMs derived from agricultural residues have moved from laboratory curiosity to scalable commercial products, addressing fire safety and sustainability concerns without sacrificing thermal capacity. Regionally, Asia-Pacific is evolving into the fulcrum for capacity additions as manufacturers add local production lines to hedge supply-chain risk linked to high-purity salt hydrates.

Performance-based compliance criteria now allow architects to substitute rigid insulation with latent-heat storage layers, unlocking a 35-45% reduction in peak cooling loads within lightweight walls. Measured field results in Minnesota reported a 5.49 °C drop in peak indoor temperature plus a 77.8% load shift toward off-peak hours, providing regulators with real-world evidence of HVAC savings. Rising compliance thresholds for 2027 EU renovation targets are expected to place additional emphasis on PCM-infused gypsum boards and concrete blocks, thereby lifting procurement volumes across the Phase Change Material market.

Vaccines, advanced biologics, and precision meats require temperature bands that often tolerate a +-0.5 °C deviation for less than three days. PCMs extend that holdover to 72 hours without external power, cutting diesel-generator reliance during airport or customs delays. Glycerol-water-NaCl blends slash carbon footprints 30-40% versus active cooling and lift pharmaceutical shelf life by 15-25%, feeding double-digit demand across the Phase Change Material market.

Paraffin waxes ignite at roughly 170 °C and require brominated flame retardants that add cost and can trigger health-labeling restrictions. Inorganic candidates such as LiNO3 present toxicity risks. Recent in-situ polymerized solid-solid PCMs eliminate leakage, passing UL94 V-0 flammability without halogens. Broader adoption hinges on scaling these encapsulation advances and harmonizing global chemical safety standards.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Organic paraffin waxes remain the revenue anchor for the Phase Change Material market, accounting for 44.19% of global sales in 2024. Their dominance reflects mature supply chains, broad temperature coverage, and compatibility with macro-encapsulation slabs used in building panels. Yet the Phase Change Material market is witnessing a sharp pivot toward bio-derived oils, tallow, and fatty-acid blends as stakeholders chase lower life-cycle emissions. The emergent sub-segment is forecast to outpace all others at 19.21% CAGR to 2030, buoyed by LEED credits and municipal green-procurement mandates that explicitly endorse biogenic materials.

Paraffin-based formulations captured 41.49% of the Phase Change Material market revenue in 2024 due to their stable crystallization and ease of tailoring melting points across the 0-90 °C spectrum. Even so, salt hydrates are on course to disrupt that hierarchy, expanding at an 18.04% CAGR through 2030. High volumetric heat capacity (up to 350 kJ/L) and thermal conductivity improvements via carbon additives are allowing salt hydrates to shrink component size and weight. The resulting density advantage is especially attractive for electric-vehicle battery sleeves and compact data-center racks, where available footprint is constrained.

The Phase Change Material Market Report Segments the Industry by Product Type (Organic, Inorganic, and Bio-Based), Chemical Composition (Paraffin, Non-Paraffin Hydrocarbons, and More), Encapsulation Technology (Macro-Encapsulation, and More), End-User Industry (Building and Construction, Packaging, Textiles, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Europe held 32.86% of global sales in 2024, underpinned by the EU's Energy Performance of Buildings Directive, which compels both new construction and deep-renovation projects to hit quasi-net-zero targets. Early adopters in Germany and the Nordics have shown 20-35% HVAC energy savings after embedding PCMs into external wall insulation systems. Regulatory clarity around carbon trading and green-bond eligibility continues to draw capital toward PCM-rich building materials, consolidating Europe's leadership position in the Phase Change Material market.

Asia-Pacific is the fastest-growing region, anticipated to expand 18.98% annually through 2030. China's aggressive heat-pump rollout complements PCM thermal storage by shaving peak electricity demand, a synergy encouraged under the "Future of Heat Pumps" roadmap.

North America combines stringent energy-code updates with an exploding electric-vehicle sector. Data-center operators in the United States, drawn by tax credits for on-site energy storage, pilot PCM-based thermal buffers to absorb server heat spikes and postpone chiller start-up.