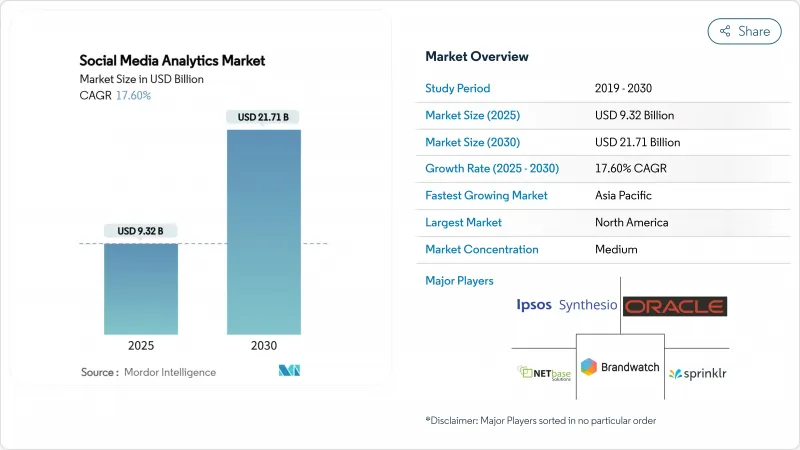

세계의 소셜 미디어 분석 시장 규모는 2025년 93억 2,000만 달러, 2030년에는 217억 1,000만 달러에 이르고, CAGR 17.6%를 보일 것으로 예측됩니다.

실시간 감정 검출, 행동 예측 모델링, 캠페인 ROI 측정에 대한 기업 수요의 급증이 이러한 확대를 지원합니다. 또한 독립형 브랜드 모니터링에서 텍스트, 이미지, 음성, 동영상을 대규모로 캡처하는 통합형 AI 주도형 인사이트 엔진으로의 결정적인 축족도 성장을 반영하고 있습니다. 클라우드 마이그레이션 가속화, 소셜 커머스 보급, 데이터 프라이버시에 대한 새로운 의무화는 솔루션 로드맵을 재구성하고 있습니다. 멀티모달 처리, 투명 모델 거버넌스 및 도메인별 데이터 커넥터를 결합할 수 있는 공급업체는 구매자가 포인트 도구를 통합 고객 경험 스택에 통합하는 동안 점유율을 얻습니다. 결과적으로 제품 로드맵은 지속적인 모델 재교육과 차별화를 유지하기 위한 내장형 GenAI 코파일럿에 중점을 둡니다.

2025년에는 52억 4,000만 명 이상이 소셜 채널에 참여하고 데이터 양이 확대되기 때문에 소셜 미디어 분석 시장은 수십억의 일상적인 상호작용을 분석하는 확장 가능한 클라우드 아키텍처로 전환하고 있습니다. TikTok의 평균 상호작용률이 2.50%인 반면 Instagram에서는 0.50%와 동영상 우선의 참여가 증가하고 있기 때문에 벤더는 이미지나 동영상의 분류자를 통합해야 하며 텍스트 전용 감정 도구를 구축하고 있습니다. 의료 제공자는 미국 성인의 90%가 소셜 플랫폼에서 건강 정보를 입수하고 있으며, 이 사용자의 급증을 이용하여 공중보건 신호를 추적하고 있습니다. 데이터 다양성은 독자적인 도메인 온톨로지와 언어 모델이 시간이 지남에 따라 정밀도를 향상시켜 공급업체의 록인을 강화합니다. 그러나 봇과 가짜 상호작용의 중복을 제거해야 하기 때문에 계산 비용이 증가하고 알고리즘의 지속적인 개선이 필요합니다.

북미 기업들은 수동 모니터링을 예측 지침으로 바꾸기 위해 GenAI에 많은 투자를 하고 있습니다. 이 지역의 마케팅 담당자의 69%가 컨텐츠 개인화에서 GenAI는 혁명적이라고 합니다. 고급 트랜스포머 모델은 99.68%의 정확도로 잘못된 정보를 감지하여 전반적인 데이터 충실도를 높입니다. 136,150개의 소셜 게시물에 Long Short-Term Memory 네트워크를 적용한 은행 파일럿은 91%의 고객 감정 분류 정밀도를 달성하여 마이크로부문화된 캠페인 제안을 가능하게 했습니다. 그러나 명확한 GenAI의 ROI를 보고하고 있는 기업은 불과 12%이며, 스킬 갭을 메울 수 있는 프로바이더에게 자문나 매니지드 서비스의 기회를 창출하고 있습니다. 로우 코드 모델 교육 인터페이스와 설명 가능성 대시보드를 배포하는 공급업체는 확대 수익을 얻기 위한 최상의 위치에 있습니다.

GDPR(EU 개인정보보호규정)을 시행함으로써 EU의 게시자는 타사 추적 기능을 14.79% 절감했으며 플랫폼은 페더레이티드 학습과 같은 개인정보를 보호하는 애널리틱스를 고안할 수 밖에 없었습니다. 캘리포니아 소비자 개인정보 보호법은 유사한 제약을 미국 전체로 확대하고 있습니다. Meta의 "Pay or Okay" 정책은 동의 프레임워크가 데이터 가용성을 저하시키고 크로스 플랫폼 사용자 스티치를 복잡하게 만드는 방법을 보여줍니다. 개인의 프라이버시를 보호하면서 집계된 코호트 수준의 통찰력을 제공할 수 있는 공급업체는 규정을 준수하고 고객의 위험 노출을 줄일 수 있습니다.

솔루션은 2024년 매출의 65%를 차지했으며 소셜 미디어 분석 시장 입구 역할을 명확히 했습니다. 구독 라이선스는 예측 가능한 이점을 제공하지만 기업은 현재 서비스 계약을 선호하는 구현 체류에 직면하고 있습니다. 서비스의 CAGR은 23.3%로 예측되고 있으며, 모델 캘리브레이션, 택소노미 설계, 법규 맵핑 등이 요구되고 있습니다. 이 상승은 구현 및 최적화의 소셜 미디어 분석 시장 규모가 특히 GenAI 워크플로우가 맞춤형 프롬프트 엔지니어링을 요구하는 경우 기본 플랫폼 요금을 능가한다는 것을 보여줍니다. Sprinklr의 7억 9,640만 달러의 FY25 매출은 FY23의 6억 1,820만 달러에서 증가하여 소프트웨어 자문의 듀얼 스트림 모델을 보여줍니다.

전문 서비스의 기세는 수직 컴플라이언스 뉘앙스로 인해 발생합니다. 헬스케어 고객은 HIPAA와의 무결성을 추구하고 은행 고객은 신용위험 결정을 위한 모델 설명 가능성을 요구합니다. 전문 분야의 전문가와 데이터 사이언티스트가 협력하는 공급업체는 가치 실현 시간을 단축하고 월렛 공유를 확대할 수 있습니다. 그 결과, 권고 파트너는 전환수의 향상과 해지 감소로 이어진 성과 기반 가격을 공동 개발하고 인센티브를 조정하여 지속적인 수익을 창출하고 있습니다.

클라우드는 2024년에 소셜 미디어 분석 시장 점유율의 72%를 획득했으며, 자동 스케일링과 매니지드 보안을 강점으로 2030년까지 21.8%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예측되고 있습니다. 탄력적 GPU 클러스터는 대부분의 On-Premise 옵션보다 비용 효율적으로 비디오 스트림 및 변환기 모델을 처리합니다. 하이브리드 옵션은 데이터 거주 규칙에 속하는 섹터에서 지속되지만 지역 영역에 대한 하이퍼스케일러 투자는 주권 장벽을 낮춥니다. 따라서 클라우드 워크로드의 소셜 미디어 분석 시장 규모는 실시간 대시보드가 이사회 수준의 운영 도구가 됨에 따라 확대됩니다.

클라우드 네이티브 제공업체는 지속적인 배포를 활용하여 매일 봇 검색, 언어 적용 범위 및 컴플라이언스 템플릿을 개선하는 기능 릴리스를 푸시합니다. Snowflake 및 Databricks와 같은 광범위한 데이터 웨어하우스 에코시스템과의 통합으로 마케팅, 영업 및 서비스의 통합적인 시각화가 가능합니다. 반대로 레거시 On-Premise 설치에서는 모델의 버전 업이나 패치의 레이턴시에 고민되어 운용상의 리스크가 높아집니다.

북미는 정교한 디지털 광고 생태계와 GenAI의 조기 전개에 힘입어 2024년 매출 38%로 소셜 미디어 분석 시장을 선도했습니다. 미국 광고 지출의 75% 이상이 온라인이며 옴니채널 캠페인 오케스트레이션에서 소셜 리스닝 도구의 보급을 촉진하고 있습니다. 기업은 주 수준의 개인정보보호 법률에 따른 컴플라이언스 오버헤드 증가에 직면하고 있으며 정책 대응 분석 프레임워크에 대한 수요가 증가하고 있습니다. 성숙기에도 불구하고, 브랜드는 마케팅부터 위험, 투자자 홍보 활동, 직장 문화 평가에 이르기까지 이용 범위를 넓혀 성장이 계속되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 21.3%로 가장 높을 것으로 보이고, 모바일 퍼스트 사람들이 소셜 커머스를 대규모로 도입하고 있습니다. 이 지역의 2024년 소셜 미디어 광고비는 전년 대비 15% 증가한 770억 달러로 언어 횡단적인 센티먼트와 인플루언서의 부정 감지에 대한 투자를 지원합니다. Taobao의 라이브 스트림 판매 등 중국 생태계 혁신은 동남아시아에도 파급되어 그린필드의 애널리틱스 수요를 창출하고 있습니다. 인도의 다국어 다양성은 적응 가능한 온톨로지를 더욱 필요로 하며 현지어 모델의 개발 파트너십에 박차를 가하고 있습니다.

GDPR(EU 개인정보보호규정)과 디지털 서비스법은 기업이 통찰력 생성을 포기하는 것이 아니라 컴플라이언스를 준수하는 애널리틱스 옵션을 찾아야 합니다. 동의 관리, 온디바이스 처리 및 차등 개인정보 보호 보고서를 통합하는 공급업체는 신중한 구매자들 사이에서 파이프라인을 확장하고 있습니다. 한편, 라틴아메리카, 중동, 아프리카에서는 인터넷 보급률의 상승에 따라 기성품 클라우드 애널리틱스의 채용이 시작됩니다. 브라질과 걸프 국가의 도시 클러스터는 첨단 시장 행동을 반영하여 현지화에 많은 비용을 들이지 않고 소셜 미디어 분석 시장 채택을 가속화합니다.

The social media analytics market size stands at USD 9.32 billion in 2025 and is forecast to reach USD 21.71 billion by 2030, advancing at a 17.6% CAGR.

Surging enterprise demand for real-time sentiment detection, predictive behavioral modeling, and campaign ROI measurement underpins this expansion. Growth also reflects a decisive pivot from stand-alone brand monitoring toward unified, AI-driven insight engines that ingest text, image, audio, and video at scale. Accelerated cloud migration, the proliferation of social commerce, and fresh data-privacy mandates are reshaping solution roadmaps. Vendors able to combine multimodal processing, transparent model governance, and domain-specific data connectors are capturing share as buyers consolidate point tools into integrated customer-experience stacks. Competitive intensity remains high because switching costs are modest and proof-of-value cycles are short; as a result, product roadmaps emphasize continuous model retraining and embedded GenAI co-pilots to sustain differentiation.

More than 5.24 billion individuals engage on social channels in 2025, expanding data volumes and pushing the social media analytics market toward scalable cloud architectures that parse billions of daily interactions. Rising video-first engagement on TikTok, with 2.50% average interaction rates versus 0.50% on Instagram, forces vendors to embed image and video classifiers, displacing text-only sentiment tools. Healthcare providers leverage this user surge to track public health signals, with 90% of US adults sourcing health information on social platforms. Data diversity strengthens vendor lock-in because proprietary domain ontologies and language models improve accuracy over time. However, the need to de-duplicate bots and fake interactions escalates compute costs and necessitates continual algorithmic refinement.

North American enterprises invest heavily in GenAI to transform passive monitoring into predictive guidance. Sixty-nine percent of regional marketers call GenAI revolutionary for content personalization. Advanced transformer models now detect misinformation with 99.68% accuracy, lifting overall data fidelity. Banking pilots that applied Long Short-Term Memory networks across 136,150 social posts achieved 91% customer-sentiment classification accuracy, enabling micro-segmented campaign offers. Yet only 12% of firms report clear GenAI ROI, creating advisory and managed-service opportunities for providers that can bridge the skills gap. Vendors rolling out low-code model-training interfaces and explainability dashboards are best positioned to capture expansion revenue.

GDPR enforcement cut third-party tracking capability by 14.79% for EU publishers, compelling platforms to devise privacy-preserving analytics such as federated learning. The California Consumer Privacy Act extends similar constraints across the United States. Meta's "Pay or Okay" policy illustrates how consent frameworks reduce data availability and complicate cross-platform user stitching. Vendors able to deliver aggregated, cohort-level insights while preserving individual privacy comply with regulation and reduce client risk exposure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions contributed 65% of 2024 revenue, underlining their role as the entry point to the social media analytics market. Subscription licenses provide predictable margins, yet enterprises now confront implementation backlogs that favor service engagements. Services are forecast to rise at a 23.3% CAGR as firms seek model calibration, taxonomy design, and regulatory mapping. This uptick illustrates how the social media analytics market size for implementation and optimization eclipses basic platform fees, especially when GenAI workflows demand bespoke prompt engineering. Sprinklr's USD 796.4 million FY25 revenue, up from USD 618.2 million in FY23, showcases the dual-stream model of software plus advisory.

The momentum in professional services also stems from vertical compliance nuances. Healthcare clients require HIPAA alignment, while banking customers demand model explainability for credit-risk decisions. Providers that pool domain experts with data scientists reduce time-to-value and deepen wallet share. Consequently, advisory partners co-develop outcome-based pricing tied to conversion uplift or churn reduction, aligning incentives and boosting recurring revenue.

Cloud captured 72% of the social media analytics market share in 2024 and is projected to sustain a 21.8% CAGR through 2030 on the strength of auto-scaling and managed security. Elastic GPU clusters process video streams and transformer models more cost-effectively than most on-premise alternatives. Hybrid options persist in sectors bound by data-residency rules, yet hyperscaler investment in regional zones lowers sovereignty barriers. The social media analytics market size for cloud workloads will therefore expand as real-time dashboards become board-level operational tools.

Cloud-native providers leverage continuous deployment to push weekly feature releases that refine bot-detection, language coverage, and compliance templates. Integration with broader data-warehouse ecosystems such as Snowflake and Databricks enables unified marketing, sales, and service visibility. Conversely, legacy on-premise installations struggle with model-versioning and patch latency, increasing operational risk.

The Social Media Analytics Market Report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Module (Social Media Monitoring and Tracking, Social Media Measurement/Listening and Analytics), End-User Industry (Media and Entertainment, IT and Telecom, BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led the social media analytics market with 38% revenue in 2024, buoyed by sophisticated digital-ad ecosystems and early GenAI rollouts. More than 75% of US ad expenditure is online, driving pervasive use of social listening tools within omnichannel campaign orchestration. Enterprises face rising compliance overhead due to state-level privacy statutes, prompting demand for policy-aware analytics frameworks. Despite maturity, growth continues as brands extend usage from marketing into risk, investor relations, and workplace culture assessment.

Asia-Pacific posts the highest regional CAGR at 21.3% through 2030 as mobile-first populations adopt social commerce at scale. The region's USD 77 billion social-media ad spend in 2024, up 15% year over year, anchors investment in cross-language sentiment and influencer fraud detection. China's ecosystem innovation-such as Taobao's live-stream selling-spills over to Southeast Asia, creating green-field analytics demand. India's multilingual diversity further necessitates adaptable ontologies, spurring local-language model development partnerships.

Europe records steady growth because GDPR and the Digital Services Act force enterprises to seek compliant analytics alternatives rather than abandon insight generation. Vendors that embed consent management, on-device processing, and differential-privacy reporting expand pipeline among cautious buyers. Meanwhile, Latin America, Middle East, and Africa begin adopting off-the-shelf cloud analytics as internet penetration rises. Urban clusters in Brazil and the Gulf states mirror advanced market behaviors, accelerating social media analytics market adoption without incurring heavy localization expenditure.