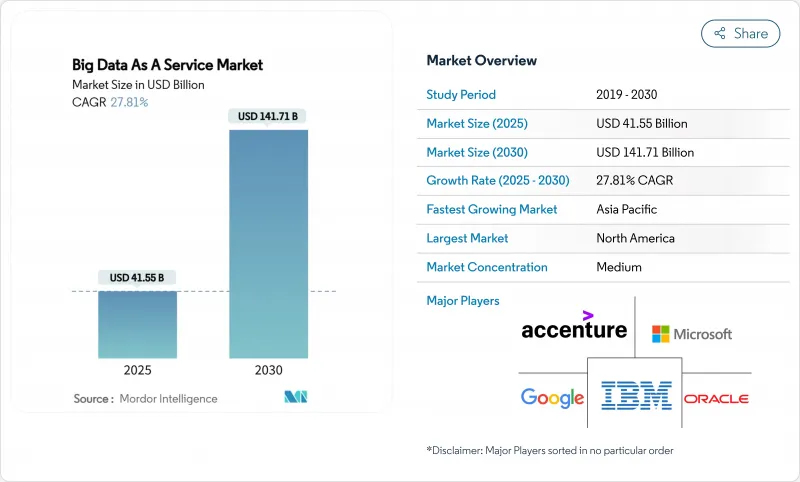

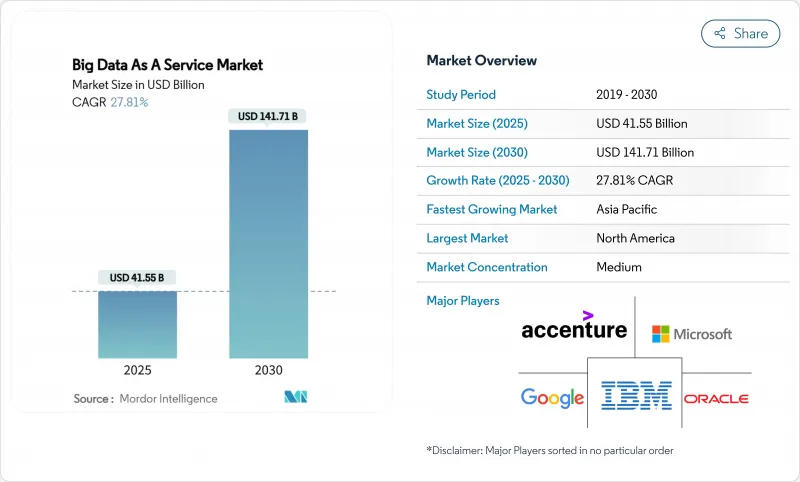

BDaaS(Big Data As A Service) 시장 규모는 2025년에 415억 5,000만 달러로 추정되고 예측 기간(2025-2030년)의 CAGR은 27.81%로, 2030년에는 1,417억 1,000만 달러에 달할 것으로 예상됩니다.

BDaaS(Big Data As A Service) 시장은 2025년에 415억 5,000만 달러에 이르고, 2030년에는 CAGR 27.81%로 1,417억 1,000만 달러에 달할 것으로 예상됩니다. 기업이 자본 집약적인 On-Premise 시스템을 인공지능 워크로드에 유연하게 대응하는 활용 기반 클라우드 분석으로 대체함에 따라 수요가 커지고 있습니다. 발전 AI 파일럿의 급증, 산업용 IoT의 전개 확대, 종량 과금으로의 세계적인 이동으로 도입 장벽이 좁아지고 있습니다. 따라서 하이퍼스케일 제공업체는 탄력적인 데이터 처리 요구를 충족시키기 위해 매년 1,050억 달러 이상을 새로운 용량에 투자하고 있습니다. 북미가 리더를 유지하고 있지만 제조업과 금융기관이 클라우드 전환을 가속화하고 있기 때문에 아시아태평양이 가장 가파른 경사를 보이고 있습니다. 이러한 요인들이 결합되어 BDaaS(Big Data As A Service) 시장은 10년 내내 견조한 전망을 유지하고 있습니다.

3M과 같은 제조업은 생산 라인에 Azure SQL Edge를 도입한 후 이상 감지에 걸리는 시간을 40% 단축하고 탄성 처리의 운영에 미치는 영향을 보여줍니다. 전 세계 클라우드에 대한 연간 지출액은 2025년에 8,250억 달러를 초과하며, 기업의 85%가 애널리틱스 프로젝트를 지원하기 위해 멀티클라우드 환경을 사용하고 있습니다. 로컬 Hadoop 팜을 유지하는 데는 연간 200만 달러에서 500만 달러의 비용이 들지만, 사용 기반 BDaaS는 워크로드의 규모에 따라 엄격하게 확장됩니다. 네트워크 에지에서는 IoT 센서가 기존 파이프에서 처리할 수 없는 데이터를 생성하기 때문에 기업은 클라우드 분석 플랫폼과 동기화하면서 소스 근처에서 계산하는 분산 아키텍처를 채택해야 합니다.

대규모 언어 모델은 현재 대부분의 기업 로드맵에서 SQL 엔진 옆에 있습니다. 은행기관은 GenAI가 완전히 가동되면 연간 2,000억-3,400억 달러의 새로운 이익이 생길 것으로 추정하고 있으며, 비구조화 데이터 처리를 위한 BDaaS에 대한 대규모 투자를 촉진하고 있습니다. 눈송이는 2024년 매출액 26억 7,000만 달러의 38%를 AI 워크로드로 삼았으며 데이터 클라우드에 직접 AI 교육을 통합하기 위해 Anthropic, NVIDIA, Microsoft와 제휴했습니다. AWS는 이미 수십억 달러의 AI 가동률을 보고했으며, 단일 테넌트에서 데이터를 수집, 변환하고 ML 파이프라인에 제공할 수 있는 플랫폼에 대한 기세를 강조하고 있습니다. 검색을 통해 확장된 세대는 기업 문서를 더욱 수익화하고 잠자는 컨텐츠 라이브러리에서 새로운 수익원을 창출합니다.

클라우드 아키텍처를 분단하고 운영 비용을 증대시키는 현지화를 의무화하고 있는 국가는 75%에 이릅니다. GDPR(EU 개인정보보호규정), 중국의 CSL, 미국의 CLOUD법 등의 규칙이 중첩되어 다국적 기업은 복잡한 데이터 거버넌스 레이어를 구축할 수밖에 없어 총 소유 비용이 최대 25% 상승합니다. 금융기관은 또한 거래 데이터를 온쇼어에 저장해야 하며 공급업체의 선택이 제한되고 조달주기가 길어집니다. 이러한 장애물로 인해 전환이 지연되는 경우도 있지만 역행하는 것은 거의 없습니다. 공급자는 지역별 클러스터와 법적 차이에 대응하는 계약 조항을 제공하고 있으며, 역풍을 완화시킬 수는 있지만 해소할 수 없습니다.

Hadoop-as-a-Service는 2024년 BDaaS(Big Data As A Service) 시장의 42%를 차지하며 배치 처리와 데이터 레이크 아키텍처가 여전히 기존 기업의 가치를 유지하고 있음을 보여주었습니다. 그러나 Analytics-as-a-Service는 BI 대시보드, ML 노트북 및 벡터 검색을 클러스터 유지보수 없이 통합하는 관리형 환경이 기업에 지지되어 있기 때문에 CAGR 30.61%와 제공 제품 중 가장 빠른 속도로 성장할 것으로 예측되고 있습니다. 2025년 시장 세분화는 애널리틱스 분야가 지출 증가의 50%를 차지하고 2030년까지 리드를 확장할 것으로 예측됩니다. Data Platform-as-a-Service는 원시 인프라와 엔드 투 엔드 애널리틱스 제품군의 중간 위치를 차지하며 맞춤형 거버넌스 관리가 필요한 규제 대상 시나리오에서 계속 중요합니다.

고객은 하드웨어 사용률보다 분석에 소요되는 시간에 성공을 측정합니다. 눈송이가 Cortex AISQL을 발표했다는 것은 분석가가 평범한 단어로 LLM을 쿼리하고 트랜잭션 데이터를 저장하는 것과 동일한 유리 창에서 거버넌스가 효과적인 답변을받을 수있는 미래를 시사합니다. 이 수렴은 ETL, 웨어하우스 및 애널리틱스 간의 역사적인 격차를 모호하게 하고 공급업체에게 기능을 통합하도록 촉구합니다. 따라서 예측 기간 동안 BDaaS(Big Data As A Service) 시장은 인프라 우선의 브랜딩에서 의사결정 지원의 즉각성을 중시한 가치제안으로 축족을 옮길 것으로 보입니다.

퍼블릭 클라우드는 하이퍼스케일러 가격에 견인되어 2024년 매출의 63%를 차지했지만 하이브리드 클라우드의 CAGR은 29.51%로 가장 빠르게 상승했습니다. 기업은 민감한 기록을 비공개 영역에 유지하면서 수요가 급증할 때 퍼블릭 에지로 분석을 버스트할 수 있는 유연성을 요구하고 있습니다. 하이브리드 옵션은 또한 공급업체의 잠금을 완화하고 75% 사법 관할구가 데이터 거주 규칙을 부과하는 경우 규정 준수를 지원합니다. 그 결과, 하이브리드 솔루션의 BDaaS(Big Data As A Service) 시장 규모는 2025년부터 2030년에 걸쳐 3배 이상으로 확대될 것으로 예측되고 있습니다.

멀티클라우드 아키텍처는 이제 주류이며 85%의 기업이 빅데이터 업무에 최소한 두 개공급자를 채택하고 있습니다. Snowflake는 최근 AWS, Azure, Google Cloud에 걸쳐 있는 Apache Iceberg 파일과 통합되었습니다. IoT 게이트웨이가 있는 플랜트에서 하이브리드 레이아웃은 로컬 하드웨어에서 비정상적인 점수를 처리한 다음 과거의 동향 구축을 위해 클라우드 모델로 집계를 전송합니다. 이러한 패턴은 차세대 애널리틱스의 백본으로 하이브리드 도입을 정착시킬 것입니다.

BDaaS(Big Data As A Service) 시장 보고서는 서비스 모델(Hadoop-As-A-Service(HaaS), Analytics-As-A-Service(AaaS) 등), 배포(퍼블릭 클라우드, 프라이빗 클라우드 등), 최종 사용자 업계(은행, 금융서비스 및 보험(BFSI), 제조, IT 및 통신 등), 지역별로 분류됩니다.

북미는 2024년 BDaaS(Big Data As A Service) 시장의 39%를 차지했으며, 클라우드 제공업체의 정착, 벤처기업의 자금 조달, 데이터 중심의 비즈니스 문화가 뒷받침되었습니다. 미국과 캐나다의 기업은 조기 도입 기업으로 현재 AI 컴퓨팅 요금의 상승을 억제하기 위해 FinOps 프랙티스의 개선에 주력하고 있습니다. 유럽은 GDPR(EU 개인정보보호규정)의 의무에 힘입어 감사 가능성을 보장할 수 있는 매니지드 서비스를 지지하고 있습니다. 엄격한 개인정보보호 규정에도 불구하고 이 지역은 여전히 10% 대 중반의 성장률을 유지하고 있습니다.

아시아태평양은 심박 조율기이며 CAGR 27.85%로 확대될 것으로 예측됩니다. 중국, 인도, 동남아시아 정부는 국가 클라우드 프로그램을 지지하고, 제조 디지털화는 BDaaS 파이프라인에 새로운 데이터를 쌓아 올립니다. Alibaba Cloud 및 Tencent Cloud와 같은 로컬 하이퍼스케일러는 지역 횡단 가용 영역에 투자하고 이전에 세계 제공업체에 묶여 있던 대기 시간 패널티를 제거합니다. IoT의 초기 도입국인 일본과 한국은 현재 지역 데이터 보호 프레임워크에 구축된 엔터프라이즈급 GenAI를 시도하고 있습니다.

라틴아메리카와 중동 및 아프리카는이 곡선의 초기 단계에있는 동안 유망한 절대 성장을 보여줍니다. 브라질 핀테크 기업과 멕시코 소매업체는 자본 예산이 대규모 셀프 호스트 클러스터를 지원할 수 없기 때문에 워크로드를 BDaaS로 이동합니다. 멕시코 걸프의 석유회사는 하이브리드 BDaaS 에지노드를 리그에서 가동시켜 예측 유지보수을 하고 있으며, 아프리카 통신사는 소비가격을 활용하여 자본을 앞당기지 않고 고객분석 프로그램을 시작하고 있습니다. 이러한 신흥 시장은 BDaaS(Big Data As A Service) 시장의 세계 실적를 확대하는 수익 증가에 기여하고 있습니다.

The Big Data As A Service Market size is estimated at USD 41.55 billion in 2025, and is expected to reach USD 141.71 billion by 2030, at a CAGR of 27.81% during the forecast period (2025-2030).

The big data as a service market reached USD 41.55 billion in 2025 and is forecast to climb to USD 141.71 billion by 2030, reflecting a compound annual growth rate of 27.81%. Demand escalates as enterprises replace capital-intensive on-premises systems with usage-based cloud analytics that flex with artificial-intelligence workloads. A surge in generative-AI pilots, wider industrial IoT rollouts, and a global shift toward pay-as-you-go pricing have narrowed adoption barriers. Hyperscale providers have therefore invested more than USD 105 billion each year in new capacity to meet elastic data-processing needs. North America retains leadership, yet Asia-Pacific shows the steepest trajectory as manufacturers and financial institutions accelerate cloud migrations. Together, these forces uphold a strong outlook for the big data as a service market through the decade.

Organizations now generate 2.5 quintillion bytes each day, volumes that exceed the practical limits of on-premises clusters.Manufacturers such as 3M cut anomaly-detection time by 40% after installing Azure SQL Edge on production lines, showing the operational impact of elastic processing. Annual global cloud spending topped USD 825 billion in 2025, and 85% of enterprises use multi-cloud environments to support analytics projects. Savings are evident: maintaining local Hadoop farms can cost USD 2-5 million per year, while usage-based BDaaS scales strictly with workload size. At the network edge, IoT sensors produce more data than traditional pipes can carry, forcing firms to adopt distributed architectures that keep compute near the source while synchronizing to cloud analytics platforms.

Large language models now sit beside SQL engines in most enterprise road maps. Banking institutions estimate USD 200-340 billion in new annual profit once GenAI is fully operational, driving heavy BDaaS investments for unstructured-data processing. Snowflake attributes 38% of its USD 2.67 billion fiscal-2024 revenue to AI workloads and has partnered with Anthropic, NVIDIA, and Microsoft to embed AI training directly in its data cloud. AWS already reports multi-billion-dollar AI run rates, underscoring the momentum toward platforms that can ingest, transform and serve data to ML pipelines in a single tenancy. Retrieval-augmented generation further monetizes enterprise documents, creating new revenue streams from dormant content libraries.

Seventy-five percent of countries enforce localization mandates that fragment cloud architectures and inflate operating expenses. Overlapping rules from GDPR, China's CSL and the US CLOUD Act force multinational firms to build complex data-governance layers, lifting total ownership cost by up to 25%. Financial institutions must further store transactional data onshore, restricting vendor options and raising procurement cycles. These hurdles slow some migrations but rarely reverse them; providers increasingly offer region-specific clusters and contract clauses that address legal variance, tempering the headwind but not eliminating it.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hadoop-as-a-Service retained 42% of the big data as a service market in 2024, indicating that batch processing and data-lake architectures still hold value for established enterprises. However, Analytics-as-a-Service is forecast to grow at 30.61% CAGR, the quickest pace among offerings, as firms favor managed environments that merge BI dashboards, ML notebooks and vector search without cluster maintenance. In 2025, the analytics segment captured 50% share of the big data as a service market size for incremental spending and is projected to widen its lead through 2030. Data Platform-as-a-Service remains relevant in regulated scenarios that need custom governance controls, occupying a middle ground between raw infrastructure and end-to-end analytics suites.

Clients increasingly measure success by time-to-insight rather than hardware utilization. Snowflake's launch of Cortex AISQL signals a future where an analyst can query LLMs with plain language and receive governed answers from the same pane of glass that stores transactional data. This convergence blurs the historical divide between ETL, warehousing and analytics, pushing vendors to consolidate features. Over the forecast period, the big data as a service market will therefore pivot from infrastructure-first branding to value propositions built around immediacy of decision support.

Public cloud commanded 63% of revenue in 2024, driven by hyperscaler pricing, but hybrid cloud will rise fastest at 29.51% CAGR. Organizations seek the flexibility to keep sensitive records in private zones while bursting analytics to the public edge during demand spikes. Hybrid options also mitigate vendor lock-in and support compliance when 75% of jurisdictions impose data-residency rules. As a result, the big data as a service market size for hybrid solutions is projected to more than triple between 2025 and 2030.

Multi-cloud architectures are now mainstream: 85% of enterprises employ at least two providers for big-data tasks. Snowflake's recent integration with Apache Iceberg files across AWS, Azure and Google Cloud enables identical queries on any venue, encouraging workload portability. For plants with IoT gateways, hybrid layouts process anomaly scores on local hardware, then forward aggregates to cloud models for historical trend building. Such patterns will entrench hybrid deployments as the backbone of next-generation analytics.

The Big Data As A Service Market Report is Segmented by Service Model (Hadoop-As-A-Service (HaaS), Analytics-As-A-Service (AaaS), and More), Deployment (Public Cloud, Private Cloud, and More), End User Industry (BFSI, Manufacturing, IT and Telecom, and More), and Geography.

North America controlled 39% of the big data as a service market in 2024, buoyed by entrenched cloud providers, venture funding and data-driven business cultures. Enterprises in the United States and Canada were early adopters and now focus on refining FinOps practices to tame runaway AI compute bills. Europe follows, propelled by GDPR obligations that favor managed services able to guarantee auditability. Despite stringent privacy rules, the region still grows in mid-teens percentages because providers certify regional clusters and encryption-key sovereignty.

Asia-Pacific is the pacesetter, projected to expand at a 27.85% CAGR. Governments in China, India and Southeast Asia champion national cloud programs while manufacturing digitalization piles new data into BDaaS pipelines. Local hyperscalers such as Alibaba Cloud and Tencent Cloud invest in cross-regional availability zones, removing latency penalties once tied to global providers. Japan and South Korea, early IoT adopters, now experiment with enterprise-grade GenAI built on regional data guardianship frameworks.

Latin America and the Middle East and Africa are earlier in the curve yet show promising absolute growth. Brazilian fintech firms and Mexican retailers shift workloads to BDaaS because capital budgets cannot support large self-hosted clusters. Gulf oil producers run hybrid BDaaS edge nodes on rigs for predictive maintenance, while African telecoms leverage consumption pricing to launch customer-analytics programs without front-loading capital. Collectively, these emerging markets contribute incremental revenue that broadens the global footprint of the big data as a service market.