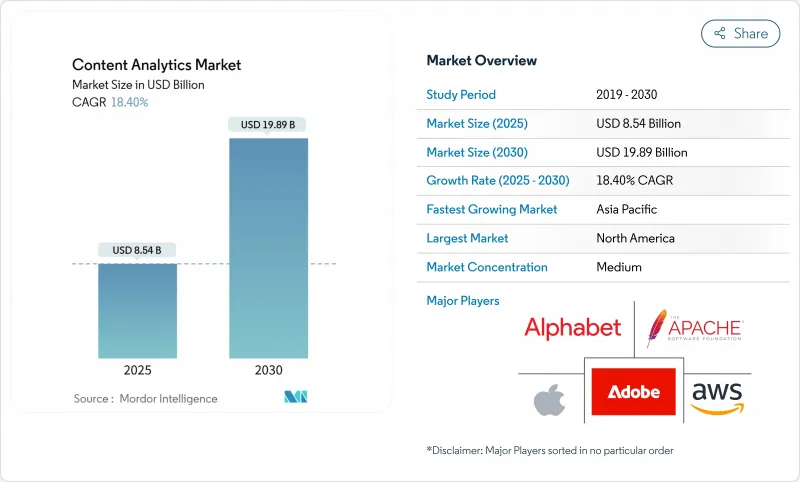

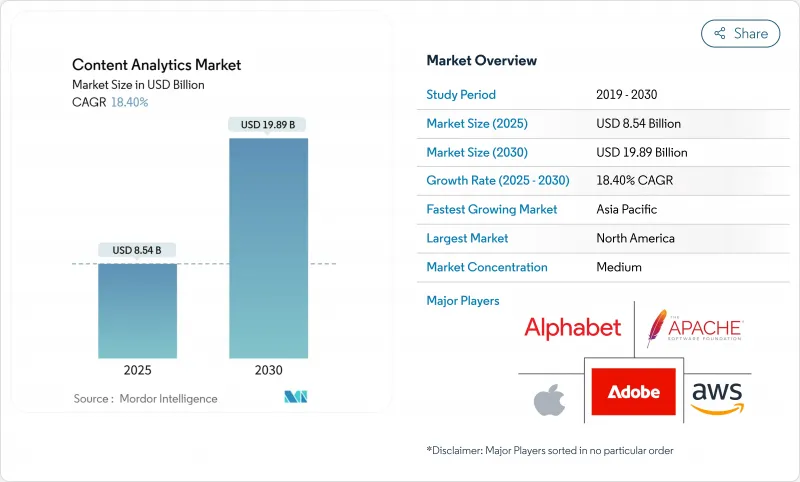

컨텐츠 분석 시장 규모는 2025년에 85억 4,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 18.40%로 성장할 전망이며, 2030년에는 198억 9,000만 달러에 달할 것으로 예측됩니다.

클라우드 마이그레이션 가속화, 멀티모달 AI의 급속한 채택, 벡터 검색 및 시맨틱 임베디드 기술의 융합이 기업이 비정형 정보에서 가치를 끌어내는 방식을 재구성하고 있습니다. 퍼블릭 클라우드 도입, 실시간 소셜 리스닝, 대규모 언어 모델을 활용한 '지식 마이닝' 파이프라인은 진입 장벽을 낮추고 실험을 촉진합니다. 동시에 데이터 주권과 하이퍼스케일 AI 플랫폼의 스케일 메리트를 밸런싱한 하이브리드 아키텍처에 대한 수요도 높아지고 있습니다. 소매, 미디어, BFSI의 기존 기업 간의 경쟁 격화는 보다 빠른 Time-to-Value와 측정 가능한 생산성 향상을 약속하는 수직화 솔루션으로 벤더를 밀어 올리고 있습니다. 이러한 요인들과 함께 컨텐츠 분석 시장은 예측 기간 동안 더 광범위한 기업용 소프트웨어 지출을 능가하는 것으로 나타났습니다.

비구조화 정보는 이미 기업 메모리의 대부분을 차지하고 있으며, 2025년에 예상되는 175제타바이트 중 80%는 관계형 시스템 이외에서 생성되고 있습니다. 예를 들어, 의료 제공업체는 수백만 개의 이미지와 다이어그램을 디지털화하고 실시간 임상 인사이트를 끌어내는 동시에 물리적 보관 비용을 절감합니다. 이러한 볼륨을 사용하면 지식 근로자가 문서, 채팅 로그 및 의료 검색에 대해 동일한 쿼리를 사용하여 의미 있는 질문을 할 수 있으며, 익숙한 SQL 엔진에 벡터 함수를 포함하는 레이크하우스 아키텍처로 기업을 밀어 올리고 있습니다.

퍼블릭 클라우드의 AI 서비스를 통해 기업은 온디맨드로 트랜스포머 스케일 모델을 대여할 수 있으므로 전용 하드웨어에 대한 자본 지출을 피할 수 있습니다. 아마존 웹 서비스의 2025년 1분기 매출은 전년 동기 대비 17% 증가한 335억 달러를 기록했으며, 주로 애널리틱스 워크로드가 견인했습니다. 기업이 워크로드를 공급자 간에 분할하고 대기 시간, 비용, 관할 컴플라이언스를 최적화하는 하이브리드 패턴이 주류가 되고 있습니다. Google BigQuery와 Microsoft Knowledge Mining 파이프라인은 인프라를 추상화하는 한편 벡터 검색 API를 게시하여 이러한 전환을 지원합니다.

테크놀로지 리더의 37%만이 제네라티브 AI에 가치가 있다고 판단하고 있는데, 그 주된 이유는 기업이 프로토타입을 확장 가능한 워크플로우로 변환하는 데 어려움이 있기 때문입니다. 연방준비제도이사회(FRB)의 조사에 따르면 AI의 도입률은 기업에 따라 5%-40%의 폭이 있어 데이터 엔지니어링, 모델 거버넌스, 도메인 고유의 프롬프트 설계에 있어서 스킬의 편차가 부각되고 있습니다. 타겟팅된 재스킬업 프로그램이 없으면 공급업체가 풍부하게 제공하고 있음에도 불구하고 애널리틱스의 가치 실현이 정체될 위험이 있습니다.

기업이 트랜스포머 클래스 모델에 대한 마찰 없는 액세스를 요구하는 가운데 퍼블릭 클라우드 서비스는 2024년 56.2%의 매출을 획득했습니다. 이 점유율은 클라우드의 하이퍼스케일러가 계속 연마하는 비용 효율성과 탄력성의 이점을 뒷받침합니다. 퍼블릭 클라우드 워크로드용 컨텐츠 분석 시장 규모는 관리형 피처 스토어, 모델 허브 및 엔터프라이즈 프롬프트 라이브러리를 배경으로 급상승할 것으로 예측됩니다. 하이브리드 클라우드 및 멀티클라우드 이용 사례는 CAGR 21.3%로 추이하고 있습니다. 규제 부문에서 결정론적 처리량과 주권 제어가 필요한 워크로드에는 온프레미스 어플라이언스가 여전히 필수적입니다.

벡터 인덱스를 엣지에 배치하고 무거운 임베딩 생성을 클라우드 GPU에 오프로드함으로써 인사이트의 깊이를 희생하지 않고 정책 준수를 달성하는 기업이 늘고 있습니다. 공급업체는 현재 프라이빗 및 퍼블릭 엔드포인트에 걸쳐 파이프라인의 건전성을 점수화하는 관측 가능성 대시보드를 번들로 제공하며, 이는 단일 공급업체의 중단에 대한 컨텐츠 분석 시장의 내성을 강화하는 동향이 되었습니다.

소셜 미디어 모니터링은 브랜드 리스닝 스위트와 인플루언서 추적 모듈의 성숙한 채용을 반영하여 2024년 33.6%의 점유율을 유지했습니다. 그러나 컨택 센터의 자동화, 실시간 문자 발생 및 음성 생체 인식을 통해 음성 및 음성 분석의 CAGR은 20.5%가 되어 추적한 부문 중 가장 빠릅니다. 음성 중심 도구의 컨텐츠 분석 시장 규모는 은행, 여행, 헬스케어 키오스크 단말기에 음성 어시스턴트가 보급됨에 따라 확대되고 있습니다. 고품질의 자동 음성 인식을 통해 멀티 모달 대시보드를 만들고 톤, 감정 및 의도 점수가 에이전트 코칭 및 에스컬레이션 워크플로를 트리거합니다.

텍스트 분석은 계약 내용을 확인하고 컴플라이언스 플래그를 지정하는 데 필수적이며 비디오 중심 파이프라인은 손실 방지 및 스트리밍 컨텐츠 최적화에 도움이 됩니다. 소셜 비디오 클립, 콜센터 트랜스크립트, 사용자가 게시한 이미지가 같은 모델 정원으로 라우팅되어 컨버전스가 가속화되고 있습니다. 따라서 업계 시나리오는 사일로화된 제품에서 일관된 경험 엔진으로 이동하여 컨텐츠 분석 시장의 장기적인 성장 전망을 강화하고 있습니다.

컨텐츠 분석 시장은 전개 모드별(온프레미스, 퍼블릭 클라우드, 하이브리드 및 멀티클라우드), 용도별(텍스트 분석, 비디오 분석 등), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어, 생명 과학 등), 조직 규모별(대기업, 중소기업), 컨텐츠 유형별(텍스트, 이미지, 음성, 기타), 지역별로 세분화됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 클라우드의 조기 도입으로 성숙한 데이터 사이언스 인력 풀과 광범위한 타사 마켓플레이스 에코시스템이 구축되었기 때문에 2024년 매출 점유율은 38.1%에 달했습니다. AWS와 같은 주요 공급업체는 고급 벡터 검색 프리미티브를 서버리스 데이터베이스에 번들하여 2자리 성장률을 달성하여 지역 과제의 진입 장벽을 높였습니다. 임박한 유럽 ESG 보고서 의무화는 이미 수천 개의 미국 다국적 기업에 영향을 미치고 있으며 이에 따라 공개 파이프라인을 조정해야 하지만 기술 구매자는 안정적인 규제 배경에서 이익을 얻고 있습니다. 아시아태평양의 소비 믹스는 금융 서비스, 헬스텍, 소비자 직접 판매 소매에 이르렀으며 컨텐츠 분석 시장의 다양한 기세를 보장합니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 21.7%로 성장할 것으로 예측됩니다. 홍콩의 3,000페타플롭스 슈퍼컴퓨팅 센터와 인도의 13억 달러의 컴퓨팅 전략 등 정부가 지원하는 인프라 프로젝트는 멀티모달 및 대규모 언어 모델 워크로드에 필요한 GPU 밀도를 제공합니다. WeChat, LINE, Douyin과 같은 소셜 미디어의 보급은 미세 조정 사이클을 가속화하는 풍부한 현지 언어 데이터를 보장합니다. 각 지역의 클라우드 제공업체는 지역화 규칙을 충족하기 위해 소블린 AI 영역을 제공하기 위해 경쟁하고 있습니다.

유럽에서는 개인정보보호 체제가 분단되고 있음에도 불구하고 꾸준히 전진하고 있습니다. 전문가의 75%는 규제를 AI의 가장 큰 장애물로 꼽고 있지만, 이 지역은 연합 학습 등의 프라이버시 보호 분석에서 선도하고 있습니다. 자동차, 산업 및 에너지의 각 부문은 임베디드 하드웨어에서 작동하는 경량 멀티모달 모델의 상업화를 위해 학술 연구소와 협력하여 제조업의 경쟁력을 강화하고 있습니다. 민간투자는 여전히 북미와 중국의 수준을 밑돌고 있으며 전략적 인공지능 자율화에 관한 정책 논란의 동기 부여가 되고 있습니다.

중동 및 아프리카에서는 공공 부문의 디지털화 및 핀테크에 새로운 기세를 볼 수 있습니다. GPU를 이용할 수 있는 지역이 한정되어 있기 때문에 데이터 유출을 최소화하는 엣지 가속기에 대한 관심이 높아지고 있습니다. 라틴아메리카는 이러한 동향을 반영하고 있으며 소매 결제 디스 랩터와 도시 안전 기관이 SaaS 음성 분석을 채택하고 있습니다. 절대 규모는 작지만 이 지역은 공급업체의 수익원을 다양화하고, 세계의 컨텐츠 분석 시장에서 지리적 집중 위험을 줄이는 수요 증가에 기여하고 있습니다.

The Content Analytics Market size is estimated at USD 8.54 billion in 2025, and is expected to reach USD 19.89 billion by 2030, at a CAGR of 18.40% during the forecast period (2025-2030).

Accelerating cloud migration, rapid adoption of multimodal AI, and the convergence of vector search with semantic embedding technologies are reshaping how enterprises extract value from unstructured information. Public cloud deployments, real-time social listening, and large-language-model-powered "knowledge mining" pipelines are lowering entry barriers and encouraging experimentation. At the same time, demand is rising for hybrid architectures that balance data-sovereignty mandates with the scale advantages of hyperscale AI platforms. Intensifying competition among retail, media, and BFSI incumbents is pushing vendors toward verticalized solutions that promise faster time-to-value and measurable productivity gains. Together, these factors suggest that the content analytics market will keep outpacing broader enterprise-software spending through the forecast window.

Unstructured information already represents the majority of corporate memory, with 80% of the 175 zettabytes expected in 2025 originating outside relational systems. Health-care providers, for example, digitized millions of images and charts to unlock real-time clinical insight while eliminating physical storage costs. These volumes are pushing enterprises toward lakehouse architectures that embed vector functions inside familiar SQL engines, allowing knowledge workers to ask semantic questions against documents, chat logs, and medical scans in the same query.

Public-cloud AI services let enterprises rent transformer-scale models on demand, avoiding capital expenditure on specialized hardware. Amazon Web Services recorded USD 33.5 billion in Q1 2025 sales, up 17% year on year, driven largely by analytics workloads. Hybrid patterns are now mainstream as firms split workloads across providers to optimize for latency, cost, and jurisdictional compliance. Google BigQuery and Microsoft Knowledge Mining pipelines are anchoring this shift by abstracting infrastructure while exposing vector search APIs.

Only 37% of technology leaders judge generative AI as valuable today, largely because firms struggle to translate prototypes into scaled workflows. Federal Reserve research shows AI uptake ranging from 5% to 40% across companies, highlighting the skills dispersion in data engineering, model governance, and domain-specific prompt design. Without targeted reskilling programs, analytics value realisation risks stalling despite abundant vendor offerings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Public-cloud services captured 56.2% revenue in 2024 as enterprises sought frictionless access to transformer-class models. This share underscores the cost-efficiency and elasticity advantages that cloud hyperscalers continue to refine. The content analytics market size for public-cloud workloads is projected to climb steeply on the back of managed feature stores, model hubs, and enterprise prompts libraries. Hybrid and multi-cloud deployments are on a 21.3% CAGR trajectory because firms must reconcile latency-sensitive use cases with data-residency statutes. In regulated sectors, on-premise appliances remain indispensable for workloads requiring deterministic throughput or sovereign control.

Enterprises increasingly position vector indexes at the edge while offloading heavy embedding generation to cloud GPUs, achieving policy compliance without sacrificing insight depth. Vendors now bundle observability dashboards that score pipeline health across private and public endpoints, a trend that strengthens the content analytics market's resilience to single-provider outages.

Social media monitoring retained a 33.6% share in 2024, reflecting mature adoption of brand-listening suites and influencer tracking modules. Yet contact-center automation, real-time transcription, and voice biometrics are pushing speech and audio analytics toward a 20.5% CAGR, the fastest among tracked segments. The content analytics market size for speech-centric tools is scaling as voice assistants proliferate across banking, travel, and healthcare kiosks. High-quality automatic speech recognition feeds multi-modal dashboards where tone, sentiment, and intent scores guide agent coaching or trigger escalation workflows.

Text analytics remains essential for contractual review and compliance flagging, while video-centric pipelines serve loss-prevention and streaming-content optimisation. Convergence is gaining speed as social-video clips, call-center transcriptions, and user-posted images are routed into the same model garden. The industry narrative, therefore, shifts away from siloed products toward cohesive experience engines, reinforcing long-term growth prospects for the content analytics market.

Content Analytics Market is Segmented by Deployment Type (On-Premise, Public Cloud, and Hybrid/Multi-Cloud), Application (Text Analytics, Video Analytics, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Organisation Size (Large Enterprises and Small and Medium-Sized Enterprises), Content Type (Text, Image, Audio, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 38.1% revenue share in 2024 because early cloud adoption produced mature data-science talent pools and extensive third-party marketplace ecosystems. Major providers like AWS drove double-digit percentage growth by bundling advanced vector search primitives into serverless databases, raising the entry barrier for regional challengers. Technology buyers benefit from a stable regulatory backdrop, although impending European ESG-reporting mandates already affect thousands of US multinationals that must align disclosure pipelines accordingly. The region's spend mix spans financial services, health-tech, and direct-to-consumer retail, ensuring diversified momentum for the content analytics market.

Asia-Pacific is the fastest-growing territory, expected to clock a 21.7% CAGR through 2030. Government-backed infrastructure projects, including Hong Kong's 3,000-petaflops supercomputing centre and India's USD 1.3 billion compute strategy, provision the GPU density required for multimodal and large-language model workloads. Social-media penetration across WeChat, LINE, and Douyin ensures abundant vernacular data that accelerates fine-tuning cycles. Regional cloud providers are racing to deliver sovereign AI zones to meet localisation rules, a move likely to preserve high services revenue inside domestic value chains.

Europe advances steadily despite fragmented privacy regimes. Seventy-five percent of professionals cite regulation as their biggest AI hurdle, yet the region leads in privacy-preserving analytics such as federated learning. Automotive, industrial, and energy sectors align with academic labs to commercialise lightweight multimodal models that run on embedded hardware, reinforcing manufacturing competitiveness. Private investment still trails North American and Chinese levels, motivating policy debate on strategic AI autonomy.

Middle East and Africa show emerging momentum in public-sector digitalisation and fintech. Limited local GPU availability has spurred interest in edge accelerators that minimise data egress. Latin America mirrors this trend, with retail payment disruptors and urban-safety agencies embracing SaaS voice analytics. Although smaller in absolute terms, these regions contribute incremental demand that diversifies vendor revenue streams and mitigates geographic concentration risk in the global content analytics market.