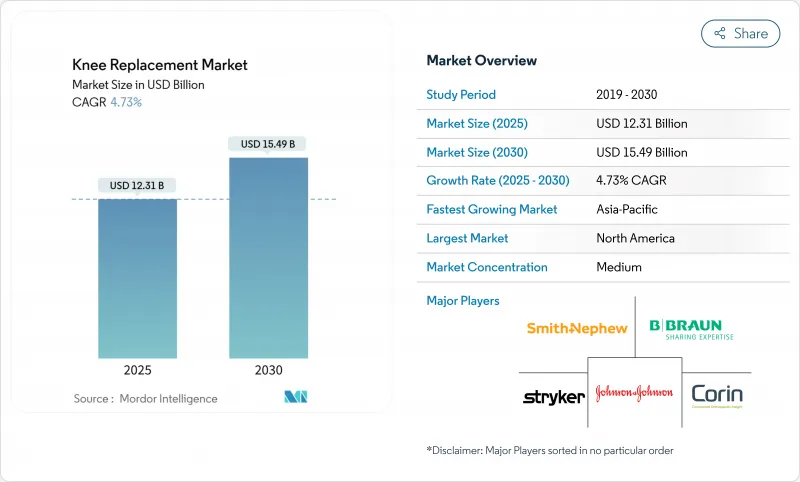

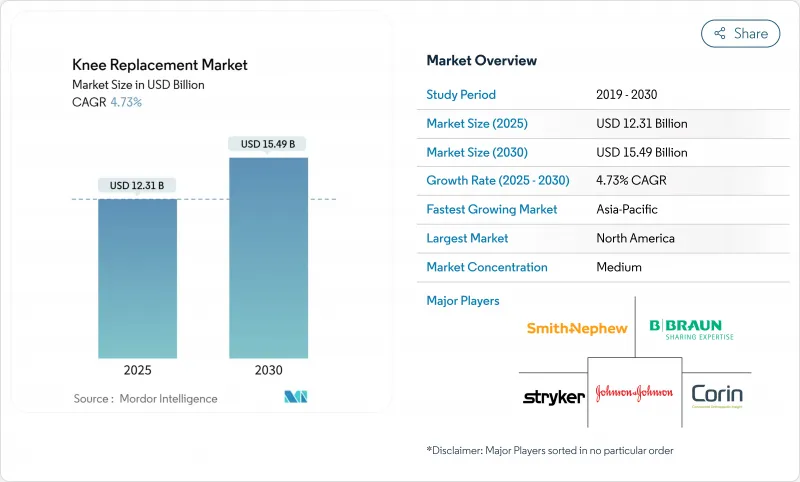

슬관절 치환술 시장 규모는 2025년에 123억 1,000만 달러로 평가되었고 예측 기간(2025-2030년)의 CAGR은 4.73%를 나타낼 것으로 예측되며 2030년에는 154억 9,000만 달러에 달할 전망입니다.

성장은 여러 요인의 복합적 작용에 기반합니다. 65세 이상 인구의 급속한 증가, 비만 유병률 상승, 임플란트 설계 및 수술 기법의 꾸준한 발전이 그것입니다. 기술 도입은 로봇 플랫폼이 대량 수술 병원과 외래 수술 센터 모두에서 주목받으며, 데이터 기반 정밀 수술로 분야를 전환시키고 있습니다. 병행되는 보험급여 개혁은 당일 퇴원 프로토콜을 장려하여 입원 및 외래 환경 간 경쟁을 심화시키고 있습니다. 제조사들은 제품 라인 확장, 플랫폼 인수, 지속가능성 약속 강화로 대응하고 있으며, 이러한 움직임은 주요 지역별 외과의 선호도와 구매 결정에 영향을 미치고 있습니다.

기대수명 증가와 좌식생활 방식이 맞물려 골관절염 발생률을 높이고 무릎 인공관절 수술 수요를 가속화하고 있습니다. 65-74세 집단에서 이용률이 가장 높지만, 75-84세 그룹이 가장 빠른 성장률을 기록하고 있으며, 고소득 시장의 여성들은 남성보다 9배 높은 비율로 슬관절 치환술을 받고 있습니다. 임플란트 내구성 향상으로 50대 초반 환자 대상 시술이 가능해지면서 대상 환자군이 확대되고 재수술 부담이 더 먼 미래로 미뤄지고 있습니다.

임상 연구에 따르면 로봇 보조 기술은 인대 균형 조절 정밀도 향상, 정렬 이상 사례 감소, 초기 환자 보고 결과 점수 상승과 연관성이 확인되었습니다. 스트라이커의 마코 플랫폼은 누적 시술 건수 150만 건을 돌파했으며, 조사 대상 외과의의 95%가 수술 중 자신감 향상을 언급했습니다. 존슨앤드존슨의 VELYS 시스템은 2024년 CT 기반 계획 없이도 단일관절면 인공관절에 대한 FDA 승인을 획득하며 기존 시장의 지배력에 도전장을 내밀었고, 워크플로우 통합과 비용 효율성을 중심으로 한 기술 경쟁을 촉발시켰습니다.

중국의 물량 기반 조달 체계는 인공관절 평균 가격을 50% 인하했으며, 이로 인한 입원 환자 비용 절감액의 93.21%가 의료기기로 귀결되었습니다. 인도의 국가의약품가격관리위원회(NPPA)는 연구개발 비용과 부합하지 않는다고 판단되는 상한선을 부과하여 지속적인 무역 분쟁을 촉발했습니다. 제조사들은 이제 혁신 예산을 강제 할인으로부터 보호하기 위해 포트폴리오를 프리미엄과 가치 등급으로 세분화하고 있습니다.

2024년 전체 슬관절 치환술이 71.24%의 시장 점유율을 차지하며 동시에 2030년까지 연평균 5.83% 성장률을 기록해 주도적 부문이 시장 확대를 촉진하는 이례적인 역학 관계를 형성하고 있습니다. 이는 해당 시술이 다양한 병리를 해결하는 데 있어 다용도로 활용 가능하며, 임플란트 설계 및 수술 기법에서 지속적인 혁신이 이루어지고 있음을 반영합니다. 로봇 보조 기술의 정밀도 및 결과 개선으로 부분 슬관절 치환술이 주목받고 있으며, 존슨앤드존슨의 VELYS 시스템은 2024년 단일관절 치환술에 대한 FDA 승인을 획득하여 역사적으로 저조했던 골 보존 기술 활용도를 높이고 있습니다.

슬개대퇴 관절 치환술은 특히 고립성 전방 무릎 통증을 가진 젊은 환자를 대상으로 한 틈새 시장이지만 성장 중인 세그먼트입니다. 한편, 1차 임플란트 설치 기반의 노후화로 인해 재수술 및 복합 슬관절 치환술에 대한 수요가 증가하고 있습니다. 재수술 부문은 골소실 관리 및 구성품 호환성 문제 등 독특한 과제에 직면하여 모듈식 임플란트 시스템과 맞춤형 3D 프린팅 솔루션의 혁신을 촉진하고 있습니다. 2024년 미국에서 유일한 무시멘트 부분 무릎 임플란트로 FDA 승인을 받은 지머 바이오메트의 옥스포드 무시멘트 부분 무릎 임플란트는 10년 시점에서 94.1%의 임플란트 생존율을 보여 평균 부분 무릎 성능 지표를 크게 상회합니다.

북미는 2024년 41.11%의 매출로 슬관절 치환 시장을 주도했으며, 이는 미국 내 연간 79만 건 이상의 시술, 강력한 기술 도입, 그리고 견고한 민간 보험 적용 범위 덕분입니다. 캐나다의 공공 의료 시스템은 대기 시간 제약을 초래하여 미국 및 멕시코 의료 시설로의 해외 의료 여행(의료 관광)을 촉진합니다. 멕시코는 이러한 흐름을 활용하여 미국에서 훈련받은 외과 의사와 로봇 수술 패키지를 마케팅하는 민간 정형외과 기관을 확장하고 있습니다. 입원 기간 단축을 위한 보험사 압박은 가치 기반 구매(Value-Based Purchasing)에 대한 관심을 높이고 있으며, 의료기기 소비세는 여전히 입법 검토 중입니다.

유럽은 성숙하면서도 이질적인 양상을 보입니다. 독일은 여전히 가장 많은 시술량을 유지하지만, 프랑스의 보험급여 삭감으로 임플란트 가격이 25% 하락해 공급자 마진이 압박받고 프리미엄 제품 채택이 둔화되었습니다. 영국의 국민건강보험(NHS) 선택적 수술 대기열은 활동 목표 달성을 위해 민간 병원과의 계약을 촉진합니다. 남유럽 국가들은 유럽투자은행(EIB) 자금의 도움을 받아 수술실을 현대화하지만, 비용 통제를 위해 임플란트 처방 목록을 최소화합니다. 동유럽 시장은 낮은 기준선에서 출발하지만, EU 통합 기금과 기술 이전 파트너십이 정형외과 병동 업그레이드를 가속화하고 있습니다. 스칸디나비아에서 선구적으로 도입된 탄소 발자국 공개와 같은 환경 조달 기준이 국경을 넘어 확산되며 공급업체 자격 기준을 재편할 수 있습니다.

아시아태평양 지역은 15.08%의 연평균 성장률(CAGR)로 가장 높은 성장률을 기록하며 2030년까지 글로벌 무릎 인공관절 시장을 변화시킬 전망입니다. 중국의 물량 기반 조달은 기기 가격을 절반으로 낮췄으나 시술 증가에는 영향을 미치지 않았으며, 병원들은 오히려 낮은 마진을 상쇄하기 위해 처리량 증대를 추구합니다. 일본은 연간 82,304건의 1차 인공관절 수술을 기록하며, 금속 이온에 대한 문화적 거부감을 반영한 세라믹-온-세라믹 베어링이 사용됩니다. 한국의 시술률은 국민건강보험과 최소 침습적 방법의 적극적인 마케팅에 힘입어 지난 10년간 407% 증가했습니다. 인도는 급증하는 수요와 가격 상한선 사이에서 균형을 맞추며, 제한된 혁신 예산에도 불구하고 국내 임플란트 제조를 촉진하고 있습니다. 호주의 남성 10만 명당 83.9건의 부상 발생률은 스포츠 관련 무릎 외상 증가를 보여주며, 정부의 비용 통제가 강화되는 가운데도 파이프라인 수요를 부추기고 있습니다.

The Knee Replacement Market size is estimated at USD 12.31 billion in 2025, and is expected to reach USD 15.49 billion by 2030, at a CAGR of 4.73% during the forecast period (2025-2030).

Growth rests on a confluence of factors: the rapid expansion of the >=65-year population, escalating obesity prevalence, and steady improvements in implant design and surgical techniques. Technology adoption is shifting the field toward data-guided precision, with robotic platforms gaining traction among both high-volume hospitals and ambulatory surgical centers. Parallel reimbursement reforms now reward same-day discharge protocols, intensifying competition between inpatient and outpatient settings. Manufacturers are responding through product line extensions, platform acquisitions, and greater focus on sustainability commitments, moves that influence surgeon preferences and purchasing decisions in every major geography.

Rising life expectancy is intersecting with sedentary lifestyles to boost osteoarthritis incidence and accelerate knee arthroplasty demand. Utilization remains highest in the 65-74 cohort, yet the 75-84 group records the fastest growth, while women in high-income markets undergo total knee procedures at rates nine times higher than men. Increasing implant durability now supports interventions in patients in their early 50s, enlarging the addressable pool and shifting revision surgery burdens further into the future.

Clinical studies now link robotic assistance to tighter ligament balancing, fewer alignment outliers, and higher early-stage patient-reported outcome scores. Stryker's Mako platform has surpassed 1.5 million cumulative procedures, with 95% of surveyed surgeons citing enhanced intra-operative confidence. Johnson & Johnson's VELYS system secured FDA clearance in 2024 for unicompartmental knees without CT-based planning, challenging incumbent dominance and spurring a technology race centered on workflow integration and cost-effectiveness.

China's volume-based procurement framework cut average knee implant prices by 50%, with devices accounting for 93.21% of total inpatient savings. India's National Pharmaceutical Pricing Authority imposed caps deemed misaligned with R&D costs, prompting ongoing trade disputes. Manufacturers now segment portfolios into premium and value tiers to shield innovation budgets against mandated markdowns.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Total knee replacement procedures command 71.24% market share in 2024 while simultaneously leading growth at 5.83% CAGR through 2030, creating a rare market dynamic where the dominant segment also drives expansion. This phenomenon reflects the procedure's versatility in addressing various pathologies and the continuous innovation in implant design and surgical techniques. Partial knee replacement procedures are gaining traction as robotic assistance improves precision and outcomes, with Johnson & Johnson's VELYS system receiving FDA clearance for unicompartmental procedures in 2024, addressing the historical underutilization of bone-preserving techniques.

Patellofemoral replacement represents a niche but growing segment, particularly for younger patients with isolated anterior knee pain, while revision and complex knee replacement procedures are experiencing increased demand as the installed base of primary implants ages. The revision segment faces unique challenges, including bone loss management and component compatibility issues, driving innovation in modular implant systems and custom 3D-printed solutions. Zimmer Biomet's Oxford Cementless Partial Knee, approved by the FDA in 2024 as the only cementless partial knee implant in the United States, demonstrates 94.1% implant survival at 10 years, significantly exceeding average partial knee performance metrics.

The Knee Replacement Market Report is Segmented by Product (Total Knee Replacement, Partial Knee Replacement, Patellofemoral Replacement, and More), Surgical Technology (Manual, Robotic-Assisted, and More), End User (Hospitals, Ambulatory Surgical Centres (ASC), and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led the knee replacement market with 41.11% revenue in 2024, driven by more than 790,000 annual procedures in the United States, strong technology adoption, and robust private-payer coverage. Canada's publicly funded system introduces wait-time constraints, prompting outbound medical travel to U.S. and Mexican facilities. Mexico capitalizes on that flow, expanding private orthopedic institutes that market US-trained surgeons and bundled robotics packages. Payer pressure to curtail inpatient lengths of stay is sharpening focus on value-based purchasing, while device excise taxes remain under legislative review.

Europe displays a mature yet heterogeneous profile. Germany retains the highest procedure volume, but reimbursement cuts in France trimmed implant prices by 25%, squeezing provider margins and slowing premium adoption. The United Kingdom's NHS elective backlog spurs contracting with private hospitals to reach activity targets. Southern European nations, helped by European Investment Bank funding, modernize operating theaters but run lean implant formularies to control costs. Eastern European markets start from lower baselines; EU cohesion funds and skill-transfer partnerships speed orthopedic ward upgrades. Environmental procurement criteria such as carbon-footprint disclosures, pioneered in Scandinavia, are gaining cross-border traction and could reshape vendor qualification standards.

Asia-Pacific contributes the highest growth at a 15.08% CAGR and is set to transform the global knee replacement market by 2030. China's volume-based procurement halved device prices yet did not dent procedure uptake; hospitals instead chase throughput to offset lower margins. Japan registers 82,304 annual primary knees, with ceramic-on-ceramic bearings reflecting cultural aversion to metal ions. South Korea's procedure rate grew 407% over the past decade, supported by national insurance and aggressive marketing of minimally invasive methods. India balances burgeoning demand against price caps, stimulating domestic implant manufacture albeit with constrained innovation budgets. Australia's injury incidence of 83.9 per 100,000 males illuminates rising sports-related knee trauma, feeding pipeline demand even as government cost-containment tightens.