인공 슬관절 치환술 시장 예측(-2030년) : 수술 유형별, 제품별, 용도별, 최종사용자별

Knee Replacement Surgery Market by Procedure Type, Product, Application, End User - Global Forecast to 2030

상품코드:1782035

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 270 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

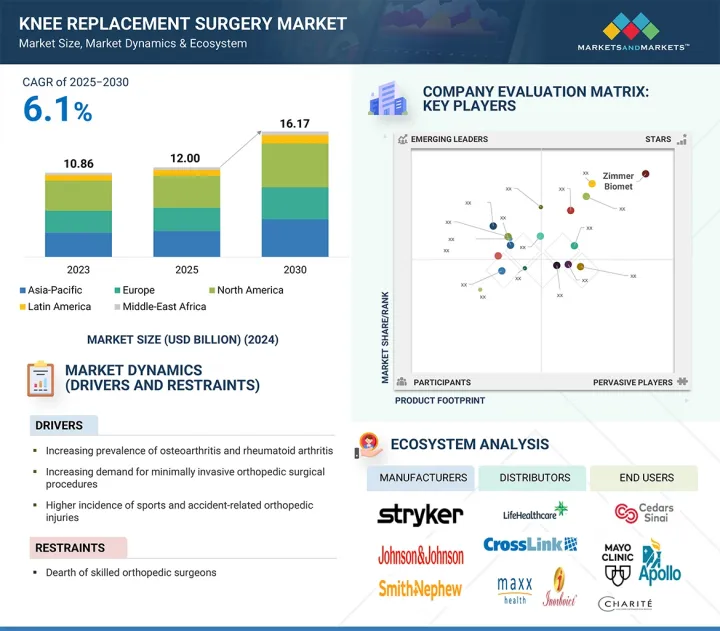

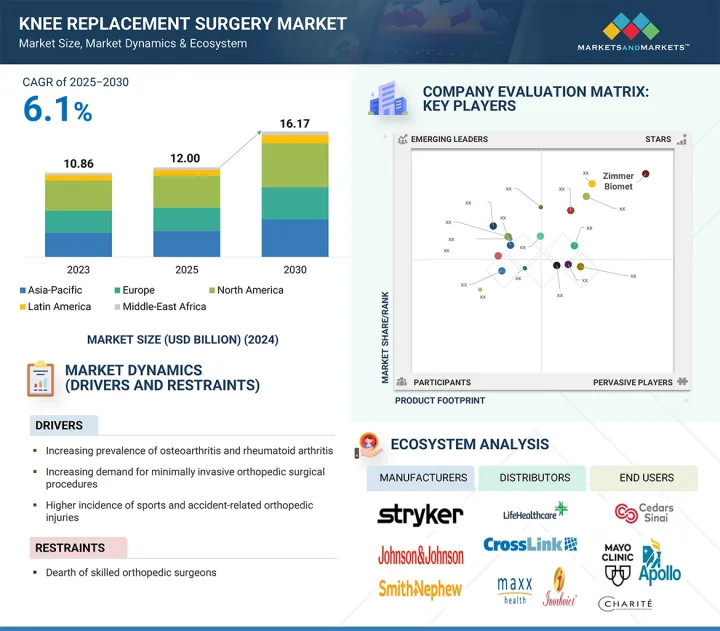

세계의 인공 슬관절 치환술 시장 규모는 2025년 120억 달러에서 2030년까지 161억 7,000만 달러에 달할 것으로 예측되며, 2025-2030년에 CAGR로 6.1%의 성장이 전망됩니다.

무릎 인공관절 치환술 시장은 여러 요인에 의해 큰 성장세를 보이고 있습니다. 다양한 치료법에 대한 인식이 높아지고 개발도상국의 의료 인프라가 개선되면서 외과수술 증가를 촉진하고 있습니다.

조사 범위

조사 대상연도

2023-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

제품, 수술 유형, 용도, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

또한 정부의 구상과 보험 개혁은 무릎 관절 수술의 가격 경제성과 접근성을 모두 강화하여 시장의 활동을 더욱 촉진하고 있습니다. 특히 젊은 층의 스포츠 손상 발병률 증가는 무릎 관절 질환의 조기 발병에 기여하고 있으며, 이로 인해 수술적 개입이 필요한 환자층이 확대되고 있습니다. 이러한 요인들은 세계 무릎 인공관절 수술 시장의 성장을 가속하고 있습니다.

"슬관절 전치환술 부문이 2024년 가장 큰 수술 유형 시장 점유율을 차지했습니다. "

무릎 인공관절 치환술 시장은 슬관절 전치환술, 슬관절 부분 치환술, 슬관절 재치환술, 기타 수술 유형으로 구분됩니다. 2024년에는 슬관절 전치환술(TKR) 부문이 시장을 장악할 것으로 예상되며, 특히 고령층에서 무릎 관절염의 유병률 증가가 주요 원인으로 작용할 것으로 보입니다. 이러한 추세는 TKR과 같은 내구성 있고 효과적인 치료 중재에 대한 수요 증가를 지원합니다. 또한 의료 인프라가 강화되고 치료 옵션에 대한 인식이 높아짐에 따라 선진국과 신흥 국가 모두에서 무릎 관절 임플란트에 대한 광범위한 접근이 촉진되고 있습니다.

"골관절염 및 류마티스 관절염 부문이 2024년 가장 큰 용도 시장 점유율을 차지할 것으로 예측됩니다. "

무릎 인공관절 시장은 골관절염 및 류마티스 관절염, 퇴행성 질환, 암, 기타 용도별로 분류됩니다. 2024년에는 골관절염 및 류마티스 관절염 부문이 가장 큰 점유율을 차지했습니다. 관절염과 같은 퇴행성 관절 질환이나 염증성 질환은 앉아서 생활하는 습관, 좋지 않은 자세, 일상적인 활동으로 인한 관절의 기계적 스트레스로 인해 초기 단계에서 악화될 수 있습니다.

"무릎 관절 임플란트 부문이 2024년 가장 큰 제품 시장 점유율을 차지했습니다. "

슬관절 임플란트 부문은 무릎 인공관절 시장에서 압도적인 점유율을 차지하고 있습니다. 이러한 임플란트는 장기간의 통증 완화 및 관절 가동범위 회복을 통해 환자의 삶의 질을 향상시키는데 매우 중요합니다. 성형외과 의사와 환자 모두 선호하는 이유는 성공률과 만족도가 높기 때문인 것으로 보입니다. 생체 적합성 합금 및 폴리머와 같은 재료의 끊임없는 발전과 혁신적인 디자인 강화 및 우수한 고정 기술로 인해 이러한 임플란트의 신뢰성과 수명이 향상되었습니다. 그 결과, 다양한 임상 현장에서 채택이 눈에 띄게 증가하고 있습니다.

"병원 부문이 2024년 가장 큰 최종사용자 시장 점유율을 차지했습니다. "

병원은 무릎 병리에 대한 고급 전문적 개입을 제공하는 데 있으며, 핵심적인 역할을 담당하고 있으므로 무릎 치료 수술 제품에서 가장 큰 시장 점유율을 차지하고 있습니다. 병원은 무릎 인공관절 전치환술과 같은 최첨단 수술을 시행할 수 있는 시설이 잘 갖추어져 있으며, 정형외과수술을 하기에 적합한 곳입니다. 또한 병원은 일반적으로 복잡한 사례를 처리하고, 최소 침습 수술을 수행하고, 종합적인 수술 후 관리를 제공하는 데 필요한 재정적 자원과 인프라를 갖추고 있으며, 이 모든 것이 무릎 치료 수술 장비에 대한 지속적인 수요에 기여하고 있습니다.

세계의 인공 슬관절 치환술 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요한 인사이트

인공 슬관절 치환술 시장 개요

북미의 인공 슬관절 치환술 시장 : 제품별

유럽의 인공 슬관절 치환술 시장 : 수술별

아시아태평양의 인공 슬관절 치환술 시장 : 최종사용자별

인공 슬관절 치환술 시장 : 지역별

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향/혼란

가격 분석

평균 판매 가격 : 제품별

평균 판매 가격 동향 : 주요 기업별

평균 판매 가격 동향 : 지역별

밸류체인 분석

연구·제품 개발

원재료 조달

마케팅·세일즈, 유통, 애프터서비스

공급망 분석

제조업체

최종사용자

에코시스템 분석

투자와 자금조달 시나리오

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

무역 분석

HS 코드 902110의 수입 데이터

HS 코드 902110의 수출 데이터

주요 컨퍼런스와 이벤트(2025-2026년)

사례 연구 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

미충족 요구

AI/생성형 AI의 영향

서론

인공 슬관절 치환술 시장에서 AI 시장의 장래성

AI 사용 사례

AI를 도입하고 있는 주요 기업

2025년 미국 관세의 영향

서론

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종 용도 산업에 대한 영향

제6장 인공 슬관절 치환술 시장 : 제품별

서론

슬관절 임플란트

오소바이오로직스

무릎 브레이스·서포터 시스템

제7장 인공 슬관절 치환술 시장 : 수술별

서론

슬관절 전치환술

슬관절 부분 치환술 디바이스

인공 슬관절재 치환술

기타 인공 슬관절 치환술

제8장 인공 슬관절 치환술 시장 : 용도별

서론

류마티스 관절염·골관절염

변성 질환

암

기타 용도

제9장 인공 슬관절 치환술 시장 : 최종사용자별

서론

병원

외래 수술 센터

정형외과 클리닉

제10장 인공 슬관절 치환술 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

프랑스

영국

이탈리아

스페인

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

일본

중국

인도

호주

한국

기타 아시아태평양

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타 중동 및 아프리카

제11장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석(2021-2024년)

시장 점유율 분석(2024년)

기업의 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제12장 기업 개요

주요 기업

ZIMMER BIOMET

STRYKER

JOHNSON & JOHNSON MEDTECH

SMITH+NEPHEW

B. BRAUN SE

GLOBUS MEDICAL

ENOVIS

MICROPORT SCIENTIFIC CORPORATION

MEDACTA INTERNATIONAL

MAXX ORTHOPEDICS, INC.

MERIL LIFE SCIENCES PVT. LTD.

WALDEMAR LINK GMBH & CO. KG

EXACTECH, INC.

AMPLITUDE SURGICAL

RESTOR3D

기타 기업

BAUERFEIND

AK MEDICAL

DOUBLE MEDICAL TECHNOLOGY INC.

OLYMPUS CORPORATION

BIORAD MEDISYS PVT. LTD.

UNITED ORTHOPEDIC CORPORATION

ALLEGRA

TOTAL JOINT ORTHOPEDICS

THUASNE GROUP

EMBLA MEDICAL

제13장 부록

KSA

영문 목차

영문목차

The global knee replacement surgery market is expected to reach USD 16.17 billion by 2030 from USD 12.00 billion in 2025, at a CAGR of 6.1% from 2025 to 2030. The Knee replacement surgery market is witnessing substantial growth driven by several key factors. A heightened awareness of various treatment modalities, coupled with improved healthcare infrastructure in developing regions, is facilitating an increase in surgical procedures.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, Procedure Type, Application, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

Additionally, government initiatives and insurance reforms are enhancing both the affordability and accessibility of knee surgeries, further propelling market activity. Notably, the rising incidence of sports-related injuries among the younger population is contributing to the premature onset of knee conditions, thereby expanding the patient demographic that requires surgical intervention. Collectively, these factors are catalyzing the expansion of the global knee replacement surgery market.

"The total knee replacement segment held the largest procedure type market share in 2024."

The knee replacement surgery market is divided into total knee replacement, partial knee replacement, revision knee replacement, and other procedure types. In 2024, the total knee replacement (TKR) segment is projected to dominate the market, primarily driven by the rising prevalence of osteoarthritis, particularly within the geriatric population. This trend underscores the growing demand for durable and effective therapeutic interventions such as TKR. Furthermore, enhanced healthcare infrastructure and increasing awareness of treatment options have facilitated broader accessibility to knee implants in both developed and emerging economies.

"The osteoarthritis & rheumatoid arthritis segment commanded the largest applications market share in 2024."

The knee replacement surgery market is segmented by application: osteoarthritis & rheumatoid arthritis, degenerative disease, cancers, and other applications. In 2024, the osteoarthritis & rheumatoid arthritis segment held the major share. Degenerative joint diseases and inflammatory conditions, such as arthritis, can be exacerbated during their initial stages due to sedentary behavior, suboptimal postural alignment, and mechanical stress on the joints resulting from routine activities.

"The knee implants segment held the largest product market share in 2024."

The knee implants segment represents the predominant share of the knee replacement surgery market. These implants are pivotal in enhancing patients' quality of life by providing long-lasting analgesia and restoring joint mobility. Their preference among orthopedic surgeons and patients alike can be attributed to their high success and satisfaction rates. Continuous advancements in materials-such as biocompatible alloys and polymers-coupled with innovative design enhancements and superior fixation techniques, have increased the reliability and longevity of these implants. Consequently, there has been a notable uptick in their adoption across various clinical settings.

"The hospitals segment accounted for the largest end user market share in 2024."

Hospitals command the largest market share in knee treatment surgical products due to their central role in providing advanced and specialized interventions for knee pathologies. They are equipped to perform cutting-edge procedures, such as total knee arthroplasty, positioning themselves as the preferred venues for orthopedic surgeries. Furthermore, hospitals typically have the financial resources and infrastructure necessary to handle complex cases, execute minimally invasive techniques, and deliver comprehensive postoperative care, all of which contribute to sustained demand for knee treatment surgical devices.

"The Asia Pacific market is expected to register the highest growth rate during the forecast period."

The knee replacement surgery market covers five key geographies-North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2024, a significant market share for knee treatment surgery devices was held by the market in the North American region, comprising the US and Canada. On the other hand, the Asia Pacific market is estimated to register the highest growth rate during the forecast period. The Asia Pacific region is witnessing unprecedented expansion in the market for knee treatment surgical devices, driven by several key factors. The demographic shift towards an aging population is significant, with increased prevalence of musculoskeletal disorders such as arthritis and osteoporosis particularly evident in nations like Japan, China, and India. This demographic change is compounded by rising disposable incomes and improved access to healthcare services. The region's healthcare infrastructure is rapidly evolving, with investments in advanced technologies such as minimally invasive surgical techniques and robotic-assisted procedures, which are enhancing surgical outcomes and patient recovery times. Moreover, the surge in medical tourism, particularly in India and Thailand, along with proactive government initiatives aimed at bolstering healthcare infrastructure, further catalyzes market growth. These dynamics collectively position the Asia Pacific as a pivotal market for advancements in orthopedic treatment devices.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1- 30%, Tier 2- 42%, and Tier 3- 28%

By Designation: Directors- 10%, Managers- 14%, and Others- 76%

By Region: North America- 40%, Europe- 30%, Asia Pacific- 22%, Latin America- 6%, Middle East & Africa- 2%

The prominent players in the Knee replacement surgery market are Stryker (US), Johnson & Johnson Services, Inc. (US), Globus Medical, Inc. (US), Medacta International SA (Switzerland), Zimmer Biomet (US), Maxx Orthopedics (US), Enovis Corporation (US), Microport Scientific Corporation (China), B. Braun Melsungen AG (Germany), Meril Life Sciences Pvt. Ltd. (India), Smith & Nephew PLC (UK), and Exactech Inc. (US)

Research Coverage

This market research report analyzes the knee replacement surgery market along several different segments, such as procedure type, product, application, end user, and region. The report further sheds light on market growth-driving factors, mentions opportunities and threats, and presents an analysis of the competitive rivalry of leading companies. It further studies micro markets by focusing on growth tendencies and predicts revenues for industry segments for five leading geographies, along with corresponding countries.

Reasons to Buy the Report

The report would assist both small and new businesses in comprehending the market pattern, which can help them grow their market. Businesses procuring the report can implement any one or several of the approaches discussed to extend their market position.

This report provides insights on the following pointers:

Key drivers (increasing prevalence of osteoarthritis and rheumatoid arthritis, Increasing adoption of telemedicine and telesurgery, rising demand for minimally invasive procedures, increasing demand for minimally invasive knee surgical procedures, and higher incidence of sports and accident-related orthopedic injuries), restraints (risk and complications associated with knee surgery procedures, high cost of knee treatment surgery and treatments), opportunities (Growing focus on orthobiologics, increasing hospitals and trend towards outpatient care and innovations in robotic-assisted orthopedic surgeries and 3D printing), and challenges (dearth of orthopedic surgeons ) fueling the market growth of knee treatment surgery devices

Product Development/Innovation: In-depth study of emerging technologies, R&D programs, and new product & service launches in the knee replacement surgery market

Market Growth: In-depth insights into remunerative markets report analyze the knee replacement surgery market across varied geographies.

Market Diversification: Detailed analysis of new products, unexplored geographies, latest trends, and investments in the knee replacement surgery market

Competitive Analysis: In-depth analysis of market shares, growth strategies, and services of leading players, such as Zimmer Biomet (US), Stryker (US), Johnson & Johnson Services, Inc. (US), Smith+Nephew PLC (UK), and B. Braun (Germany).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DESIGN

2.2 RESEARCH DATA

2.2.1 SECONDARY RESEARCH

2.2.1.1 Key data from secondary sources

2.2.2 PRIMARY RESEARCH

2.2.2.1 Primary sources

2.2.2.2 Key industry insights

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.1.1 Approach 1: Company revenue estimation approach