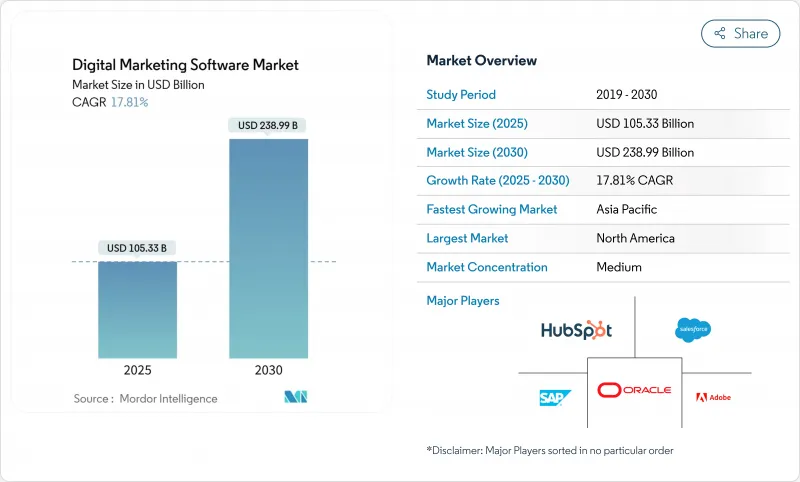

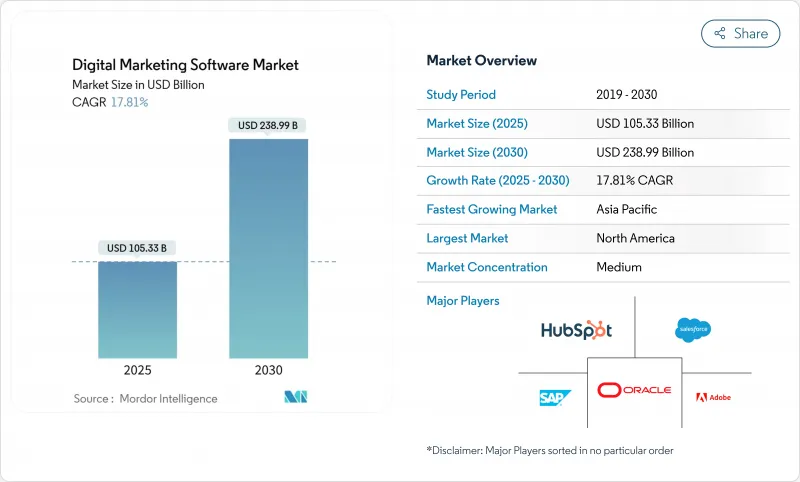

세계의 디지털 마케팅 소프트웨어 시장은 2025년에 1,053억 3,000만 달러로 평가되었고, 2030년에는 2,389억 9,000만 달러에 이를 것으로 예상되며, 기간 중 17.81%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

클라우드 네이티브 아키텍처로의 급속한 전환, AI 기반 자동화, 쿠키 없는 개인화 기술로 인해 마케팅 기술 지출은 전체 마케팅 예산의 25.4%를 유지하고 있습니다. 기업들은 이제 통합된 데이터, 콘텐츠, 실행 기능을 제공하는 통합 제품군을 선호하며, 통합 비용을 증가시키는 분산된 포인트 솔루션을 대체하고 있습니다. 사용량 기반 구독 가격 정책은 초기 자본 지출을 줄여 중견 기업의 도입을 촉진합니다. 플랫폼 벤더들이 생성형 AI 코파일럿을 내장하여 크리에이티브 사이클을 단축하고 셀프 서비스 분석을 확대함에 따라 경쟁 강도는 계속 높아지고 있습니다.

B2B 구매자의 70%가 이제 검색 엔진을 통해 조사를 시작함에 따라 기업들은 콘텐츠, 데이터, 커머스 전반에 걸친 참여 모델을 재설계해야 합니다. 제조 기업들은 마케팅 예산의 75%를 디지털 채널에 할당하며, 이는 과거 주기 대비 10% 포인트 증가한 수치입니다. 의료 서비스 제공자들은 웹 포털과 환자 앱 전반에 걸쳐 규정 준수 및 맞춤형 경험을 제공하기 위해 AI 오케스트레이션을 활용합니다. 유럽 기업들은 고객 경험을 주요 경쟁 우위로 인식하며, 디지털 전환 예산의 22.9%를 마케팅 기술에 투자합니다. 디지털 중심 참여로의 지속적인 전환은 획득, 전환, 유지 관리를 통합 관리하는 플랫폼에 대한 지속적인 수요를 뒷받침합니다.

Adobe GenStudio와 같은 생성형 AI 플랫폼은 대규모 동적 자산 변형을 가능하게 하여 제작 시간을 50% 단축하는 동시에 이메일 전환율을 두 배로 높입니다. HubSpot은 2024년 9월 출시한 Breeze AI에 80개 이상의 AI 기능을 내장하며 캠페인 디자인 자동화 경쟁을 강조했습니다. 아시아태평양 기업들은 투자를 가속화하고 있으며, 59%가 2025년 AI 예산 증액을 계획 중입니다. Salesforce Agentforce에서 볼 수 있듯 자율 에이전트의 기업 도입은 마케팅 워크플로우가 최소한의 인적 개입으로 운영될 수 있음을 입증합니다. AI 역량은 차별화 요소라기보다 기본 요건으로 빠르게 자리 잡고 있습니다.

기업 스택에는 평균 130개의 애플리케이션이 존재하지만, 완전히 통합된 것은 5분의 1 미만에 불과해 운영 비용을 증가시키고 투자 수익률(ROI)을 지연시킵니다. CMO들은 데이터 단절, 부실한 거버넌스, 제한된 구현 역량을 주요 장벽으로 꼽습니다. MACH(마이크로서비스, API 우선, 클라우드 네이티브, 헤드리스) 아키텍처로의 전환은 많은 중견 기업이 보유하지 못한 기술 전문성을 요구하여 일정을 연장하고 총소유비용을 증가시킵니다. 유럽 제조업체들은 이 격차를 보여주는데, 디지털 성숙도를 달성한 기업은 3분의 2에 불과한 반면 미국 동종 업계는 거의 4분의 3에 달합니다.

클라우드 제공 방식은 2024년 매출의 65.5%를 차지했으며, 디지털 마케팅 소프트웨어 시장 규모에서 차지하는 비중은 2030년까지 연평균 18.5%의 성장률로 확대될 전망입니다. 경제성은 여전히 매력적입니다. 탄력적인 인프라, 지속적인 업데이트, 낮은 유지보수 비용이 총소유비용을 낮추면서 확장성을 개선합니다. 데이터 거주지 및 맞춤형 통합이 여전히 중요한 규제 산업에서는 온프레미스 설치가 지속되지만, 클라우드 제공업체가 고급 보안 인증을 획득함에 따라 그 비중은 줄어들고 있습니다.

사용량에 따른 비용 조정은 중견 시장 진입을 촉진하며, AI 기능은 종종 클라우드 에디션에서 먼저 제공되어 선호도를 강화합니다. 벤더들은 전환을 용이하게 하기 위해 하이브리드 모델을 제공하지만, 기업들이 속도와 유연성을 우선시함에 따라 완전한 SaaS 전개로의 추세는 되돌릴 수 없는 것으로 보입니다.

소프트웨어 라이선스는 2024년 매출의 54.9%를 차지했으나, 기업들이 플랫폼 가치를 실현하기 위한 전문성을 추구함에 따라 서비스 매출은 연평균 19.2% 성장률로 더 빠르게 증가할 전망입니다. 시스템 통합, 데이터 정제, 변경 관리 프로젝트가 초기 사업을 주도하는 반면, 관리형 서비스는 장기적 최적화를 지속합니다. 모델 훈련, 거버넌스, 반복적 성능 튜닝이 필요한 AI 도입은 서비스 계약을 중심으로 한 디지털 마케팅 소프트웨어 시장 규모를 더욱 부양합니다.

스택이 더욱 복잡해짐에 따라 외부 파트너들은 특히 멀티클라우드 및 컴포저블 아키텍처 분야에서 역량 격차를 메우고 있습니다. 벤더들은 자문 및 관리형 서비스 제공을 구독형 플랜에 묶어 제공함으로써 지속적 반복 수익을 창출하고 고객 락인을 강화하고 있습니다. 고객사 팀의 역량을 강화하고 플랫폼 투자 수익률(ROI)을 가속화하기 위한 교육 아카데미 및 인증 프로그램이 확산되고 있습니다.

디지털 마케팅 소프트웨어 시장은 전개(클라우드 및 온프레미스), 구성 요소(소프트웨어 및 서비스), 최종 사용자 기업 규모(대기업 및 중소기업), 최종 사용자 업계별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 제조업 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 매출의 41.9%를 차지했으며, 이는 높은 클라우드 보급률, 숙련된 인력, Adobe, Salesforce, HubSpot과 같은 플랫폼 공급업체의 밀집된 분포에 힘입은 결과입니다. 벤처 캐피털은 AI 주도 마테크(martech) 스타트업을 지속적으로 선호하며 지역 혁신의 선순환을 강화하고 있습니다. 보급률이 성숙기에 접어들고 교체 주기가 길어지면서 성장은 안정적이지만 완만해지고 있습니다.

아시아태평양 지역은 2030년까지 연평균 20.6%의 성장률(CAGR)을 기록할 것으로 예상되며, 이는 전 세계에서 가장 빠른 속도입니다. 정부 차원의 디지털 전환 장려책과 함께 기업들은 언어적 및 문화적 특성을 고려한 현지화 AI 모델을 도입하고 있습니다. 제조업 및 금융 서비스 현대화 프로그램이 플랫폼 도입을 가속화하며, 규제 특성에 대응하기 위한 국내 공급업체들이 등장하고 있습니다. 따라서 아시아태평양 지역의 디지털 마케팅 소프트웨어 시장 규모는 경쟁이 심화되는 가운데서도 급속히 확대될 전망입니다.

유럽은 여전히 견고하지만 규제가 많은 도입 지역입니다. EU 제조업체 중 단 66%만이 종단간 디지털화를 달성했으나, 경영진의 56%는 2025년 기술 예산 증액을 계획 중입니다. GDPR은 프라이버시 우선 플랫폼 수요를 촉진하지만, 동시에 구현 일정과 비용 구조를 연장시킵니다. 설계 단계부터 규정 준수를 고려한 아키텍처를 보유한 공급업체들은 수용적인 구매자를 찾고 있으며, 유럽에서 개발된 전문성은 다른 관할권이 프라이버시 법규를 모방함에 따라 점차 수출되고 있습니다.

The global digital marketing software market posted USD 105.33 billion revenue in 2025 and is forecast to touch USD 238.99 billion by 2030, advancing at a 17.81% CAGR over the period.

Rapid migration to cloud-native architectures, AI-driven automation, and cookieless personalization keeps spending on marketing technology at 25.4% of overall marketing budgets. Enterprises now favor integrated suites that unify data, content, and activation functions, replacing fragmented point solutions that raise integration costs. Subscription pricing tied to usage reduces up-front capital outlays, encouraging adoption among mid-market firms. Competitive intensity continues to rise as platform vendors embed generative AI copilots that shorten creative cycles and expand self-service analytics.

Seventy percent of B2B buyers now initiate research via search engines, forcing enterprises to re-engineer engagement models across content, data, and commerce. Manufacturing firms allocate 75% of marketing budgets to digital channels, up 10 percentage points versus past cycles. Healthcare providers use AI orchestration to deliver compliant, personalized journeys across web portals and patient apps. European organizations devote 22.9% of digital transformation budgets to marketing technology, recognizing customer experience as a primary competitive lever. The persistent shift toward digital-first engagement underpins sustained demand for unified platforms that manage acquisition, conversion, and retention.

Generative AI platforms such as Adobe GenStudio enable dynamic asset variation at scale, cutting production times by 50% while raising email conversion rates two-fold. HubSpot embedded more than 80 AI features in its Breeze AI release of September 2024, underscoring the race to automate campaign design. Asia-Pacific firms are accelerating investment, with 59% planning higher AI budgets in 2025. Enterprise deployments of autonomous agents, as seen in Salesforce Agentforce, prove marketing workflows can operate with minimal human intervention. AI capability is rapidly becoming a baseline requirement rather than a differentiator.

Enterprises average 130 applications in the stack, yet fewer than one-fifth are fully integrated, inflating operational costs and delaying ROI. CMOs cite disconnected data, poor governance, and limited implementation skills as top barriers. Moving to MACH (microservices, API-first, cloud-native, headless) architectures demands technical expertise that many mid-market firms lack, extending timelines and inflating total cost of ownership. European manufacturers illustrate the gap, with only two-thirds achieving digital maturity, compared with nearly four-fifths of US peers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud delivery controlled 65.5% of 2024 revenue, and its share of the digital marketing software market size is projected to expand at an 18.5% CAGR through 2030. The economics remain compelling: elastic infrastructure, continuous updates, and lower maintenance overheads drive total cost of ownership down while improving scalability. On-premise installations persist in regulated verticals where data residency and bespoke integration remain critical, but their share shrinks as cloud providers earn advanced security certifications.

Cost alignment with usage encourages mid-market entry, and AI functionality is often available first in cloud editions, reinforcing preference. Vendors offer hybrid models to ease transition, yet the momentum toward full SaaS deployment appears irreversible as enterprises prioritize speed and flexibility.

Software licenses represented 54.9% of 2024 revenue, yet services revenue is set to grow faster at 19.2% CAGR as firms seek expertise to unlock platform value. System integration, data hygiene, and change-management engagements dominate initial projects, while managed services sustain long-term optimization. The digital marketing software market size for service engagements is further buoyed by AI adoption, which requires model training, governance, and iterative performance tuning.

As stacks grow more complex, external partners fill capability gaps, particularly around multi-cloud and composable architectures. Vendors bundle advisory and managed-service offerings into subscription plans, generating sticky recurring revenue and deepening customer lock-in. Training academies and certification programs proliferate to upskill client teams and accelerate platform ROI.

Digital Marketing Software Market is Segmented by Deployment (Cloud and On-Premise), Component (Software and Services), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 41.9% revenue in 2024, driven by deep cloud penetration, a skilled workforce, and dense concentration of platform vendors such as Adobe, Salesforce, and HubSpot. Venture capital continues to favor AI-led martech startups, reinforcing the local innovation flywheel. Growth is steady but moderates as penetration approaches maturity and replacement cycles lengthen.

Asia-Pacific is projected to record a 20.6% CAGR to 2030, the fastest worldwide. Governments incentivize digital transformation, and enterprises are adopting localized AI models that respect linguistic and cultural nuances. Manufacturing and financial-services modernization programs accelerate platform uptake, and domestic vendors emerge to address regulatory specifics. The digital marketing software market size attributable to Asia-Pacific will therefore expand rapidly, even as competition intensifies.

Europe remains a solid but regulated adopter. While only 66% of EU manufacturers have achieved end-to-end digitalization, 56% of executives plan higher technology budgets in 2025. GDPR catalyzes demand for privacy-first platforms, yet also stretches implementation timelines and cost structures. Vendors with compliance-by-design architectures find receptive buyers, and expertise developed in Europe is increasingly exported as other jurisdictions replicate privacy statutes.