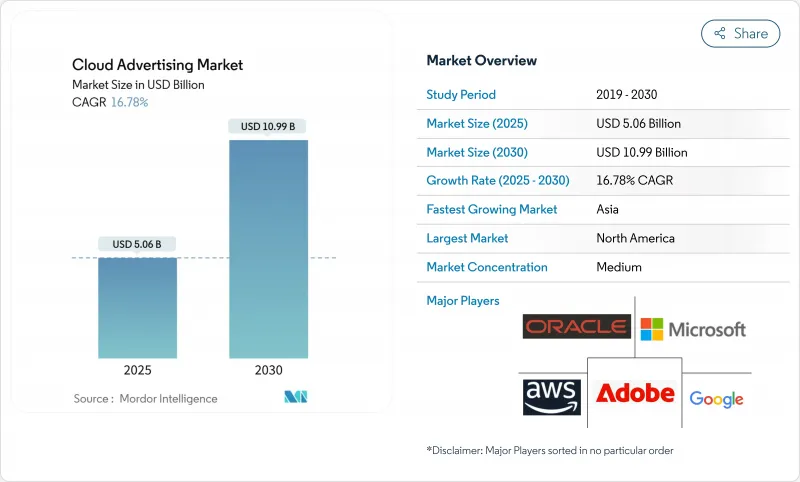

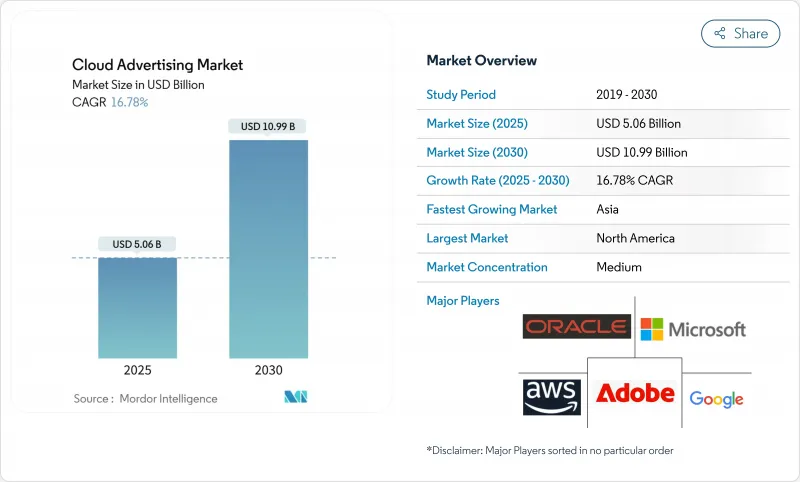

클라우드 광고 시장 규모는 2025년에 50억 6,000만 달러, 2030년에는 109억 9,000만 달러에 이르고, CAGR은 16.8%를 나타낼 전망입니다.

광고주가 On-Premise 스택을 밀리초 단위의 입찰, 실시간 분석, 통합된 개인정보 보호 제어를 제공하는 신축성 있는 AI 지원 클라우드 서비스로 전환함에 따라 수요가 가속화되고 있습니다. 클라우드 워크로드에 새로운 10억 달러가 유입될 때마다 관측 가능성, 암호화, GPU 풍부한 인스턴스에 대한 지출이 증가하고, 인프라가 직접적인 수익을 창출합니다. ID 그래프, 광고 소재 생성 및 캠페인 측정을 관리하는 워크로드는 종종 소블린 또는 논리적으로 분리된 리전에서 실행되며, 하이퍼스케일러는 클린룸 템플릿과 고객 관리 키를 예약 인스턴스 오퍼에 번들하도록 촉구합니다. 캠페인의 민첩성과 규제의 무결성이 하나의 협상에 수렴했기 때문에 조달주기에는 마케팅, 법무, IT가 동등하게 관여하게 되었습니다.

대규모 전자상거래 상점을 운영하는 소매업체는 2024년 광고 게재 코드를 퍼블릭 클라우드로 이전했습니다. 한 마켓플레이스에서는 서버리스 GPU 풀로 마이그레이션한 결과 플래시 캠페인의 기동 시간을 43% 단축하고 오프 피크시의 비용을 2자리 줄임으로써 몰입형 동영상 포맷의 예산을 확보할 수 있었다고 보고했습니다. 매시간 재고를 의식한 프로모션은 매주 업데이트 주기를 대신하여 클라우드의 경제성이 머천다이징 전략을 재구성하는 방법을 보여줍니다.

유럽의 GDPR(EU 개인정보보호규정)은 아키텍처 결정에 계속 영향을 미칩니다. 2025년 봄, 다국적 방송사는 시청자 매칭을 암호화된 BigQuery 클린룸으로 이전했으며, 광고주는 원시 테이블에 액세스하지 않고 리프트를 측정할 수 있습니다. 현재 에이전시는 새로운 입찰에서 유사한 청사진을 요구하고 있으며, 클린룸이 프리미엄 애드온이 아닌 기본 요구사항이 되고 있음을 나타냅니다.

광고주는 2024년 노출 로그가 여러 클라우드를 건너면 데이터 출력 요금이 ROI를 악화시킬 수 있음을 발견했습니다. 유럽의 게임 퍼블리셔는 전용 섬유가 있는 공동 위치 시설로 트래픽을 전달하여 대기 시간 없이 7자리 비용을 절감했습니다. 재무 팀은 현재 네트워크 토폴로지를 예산의 핵심 변수로 취급하고 있습니다.

하이브리드 클라우드 광고 시장 규모는 2030년까지 24%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되고 있으며, 기밀성이 높은 ID 그래프를 포기하지 않고 탄력적인 컴퓨팅을 요구하는 브랜드의 요구가 부각되고 있습니다. 한 세계 항공사는 승객 목록 처리를 위해 Edge Kubernetes 클러스터를 실행하고 동시에 예측 작업을 공용 영역으로 버스트하여 GDPR(EU 개인정보보호규정) 준수 리타겟팅 및 실시간 수익 관리를 실현했습니다. Public-클라우드 광고는 스트리밍 서비스가 AV1 인코딩에 예약 GPU 블록을 사용하여 렌더링 비용을 반감시켜 2024년 64%의 클라우드 광고 시장 점유율을 유지. 프라이빗 클라우드의 도입은 금융 및 헬스케어에서 계속 중요하며, 유럽의 보험 회사는 세분화 모델을 OpenShift의 프라이빗 클러스터로 전환한 후 규제 시간을 20% 줄였습니다.

클라우드 광고 시장은 배포 유형(퍼블릭 클라우드 광고, 프라이빗 클라우드 광고, 하이브리드 클라우드 광고), 서비스 모델(SaaS(Software As A Service) 광고 플랫폼, 광고 게재용 IaaS(Infrastructure As A Service) 등), 최종 사용자 업계(소매, EC 상거래, 미디어 엔터테인먼트 등), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 매출의 38%를 차지했으며 입찰 요청의 라운드트립 중앙값을 120ms 미만으로 억제하는 고밀도 클라우드 간 연결에 지지되고 있습니다. 2025년에 도입된 주 수준의 개인정보보호법은 정책 애즈코드 도구에 대한 수요에 박차를 가하고 컴플라이언스를 선언형 템플릿으로 추상화하는 벤더에게 보상을 주고 있습니다.

아시아태평양은 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 20%로 가장 빠른 성장을 기록할 전망입니다. 데이터센터 건설에 대한 정부의 우대 조치, 광동성의 신재생에너지 프로젝트, 인도네시아 낙도의 저궤도 연결 등이 지금까지 도달할 수 없었던 잠재고객에 대한 모바일 광고 도달범위를 확대합니다.

유럽은 가장 엄격한 개인 정보 보호 시스템에 직면하고 있습니다. 유럽 전역에 퍼진 식료품 체인은 2025년에 소블린 클라우드를 통해 암호화된 충성도 ID를 페더레이션하여 약간의 대기 시간 오버헤드를 컴플라이언스 확실성으로 대체했습니다. 이 지역의 광고주는 규제 위험을 줄이기 위해 이러한 실적 절충을 수락합니다.

라틴아메리카에서는 물류 투자와 광고 수입의 선순환이 계속되고 있습니다. 브라질의 풀필먼트 전문 기업은 도시의 소비자의 55%로 당일 배송을 확대하여 스폰서가 있는 리스팅의 클릭 스루율을 높여 광고 수입이 GMV의 성장을 웃도는 것을 가능하게 했습니다.

중동 및 아프리카는 새로운 지상 광섬유 루트와 주권 클라우드 구축의 혜택을 누립니다. 한 걸프 항공사가 2025년 아부다비의 스택에서 시작한 아랍어 리타게팅 캠페인은 이전에는 디지털 지출에 대한 지수가 낮았던 시장에서 예약 증가를 창출했습니다.

The cloud advertising market size is estimated at USD 5.06 billion in 2025 and is forecast to reach USD 10.99 billion by 2030, reflecting a 16.8% CAGR.

Demand accelerates as advertisers trade on-premises stacks for elastic, AI-enabled cloud services that deliver millisecond bidding, real-time analytics, and integrated privacy controls. Each new billion flowing into cloud workloads lifts spending on observability, encryption, and GPU-rich instances, making infrastructure a direct revenue lever. Workloads that manage identity graphs, creative generation, and campaign measurement increasingly run in sovereign or logically isolated regions, pushing hyperscalers to bundle clean-room templates and customer-managed keys into reserved-instance offers. Procurement cycles now involve marketing, legal, and IT in equal measure because campaign agility and regulatory alignment have converged into one negotiation.

Retailers operating large e-commerce storefronts shifted ad-serving code to public clouds in 2024. One marketplace cut flash-campaign launch times by 43% after moving to serverless GPU pools and reported double-digit off-peak cost savings, freeing budget for immersive video formats. Hourly inventory-aware promotions have replaced weekly refresh cycles, demonstrating how cloud economics reshape merchandising strategy.

Europe's GDPR continues to steer architecture decisions. In spring 2025, a multinational broadcaster migrated audience-matching to an encrypted BigQuery clean room, enabling advertisers to measure lift without accessing raw tables . Agencies now request similar blueprints in new tenders, indicating that clean rooms are becoming a default requirement rather than a premium add-on.

Advertisers discovered in 2024 that data-out charges can erode ROI when impression logs traverse multiple clouds. A European gaming publisher cut seven-figure costs by repatriating traffic to a colocation facility with private fiber, without latency penalties. Finance teams now treat network topology as a core budget variable.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hybrid-cloud advertising market size is projected to grow at a 24% CAGR through 2030, underscoring brands' need for elastic compute without relinquishing sensitive identity graphs. A global airline ran edge Kubernetes clusters for passenger-list processing while bursting forecasting tasks to public zones, enabling GDPR-compliant retargeting and real-time yield management. Public-cloud advertising retained 64% cloud advertising market share in 2024 as a streaming service halved rendering costs by using reserved GPU blocks for AV1 encoding. Private-cloud deployments remain critical in finance and healthcare, with a European insurer cutting regulatory man-hours by 20% after migrating segmentation models to a private OpenShift cluster.

Cloud Advertising Market is Segmented by Deployment Type (Public Cloud Advertising, Private Cloud Advertising, Hybrid Cloud Advertising), Service Model (Software As A Service (SaaS) Advertising Platforms, Infrastructure As A Service (IaaS) for Ad Delivery, and More), End-User Industry (Retail and ECommerce, Media and Entertainment, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 38% of 2024 revenue, supported by dense inter-cloud connectivity that keeps median bid-request round-trip below 120 ms. State-level privacy laws introduced in 2025 spurred demand for policy-as-code tooling, rewarding vendors that abstract compliance into declarative templates.

Asia-Pacific is expected to record the fastest regional growth at 20% CAGR from 2025-2030. Government incentives for data-center construction, renewable energy projects in Guangdong, and low-earth-orbit connectivity across remote Indonesian islands together extend mobile-ad reach to previously unreachable audiences.

Europe faces the strictest privacy regime. A pan-European grocery chain federated encrypted loyalty IDs through sovereign clouds in 2025, trading minor latency overhead for compliance certainty. Advertisers across the region increasingly accept such performance tradeoffs to mitigate regulatory risk.

Latin America's virtuous cycle of logistics investment and advertising revenue continues. A Brazilian fulfilment specialist extended same-day delivery to 55% of urban consumers, boosting click-through rates on sponsored listings and enabling ad revenue to outpace GMV growth.

Middle East and Africa benefit from new terrestrial fiber routes and sovereign-cloud builds. A Gulf airline's Arabic-language retargeting campaign launched from an Abu Dhabi stack in 2025 generated incremental bookings in markets that previously under-indexed on digital spend.