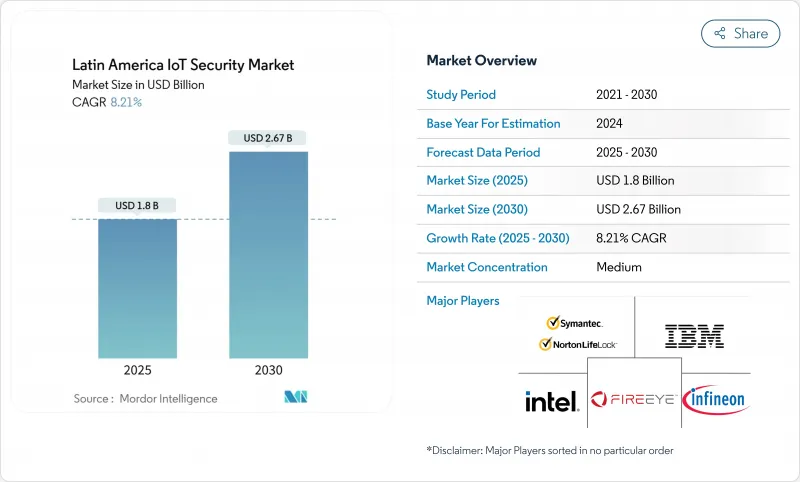

라틴아메리카의 IoT 보안 시장 규모는 2025년에 18억 달러, 2030년에는 26억 7,000만 달러에 이르고, CAGR 8.21%로 성장합니다.

브라질의 스마트 시티 모니터링 프로그램 확대, 칠레의 중요한 인프라에 대한 Zero-Trust 규칙의 의무화, 멕시코의 급속한 5G 배치가 연결 장치 보호에 대한 지출을 촉진합니다. 2024년에 1억 8,240만 명이 위험에 처한다는 기록적인 헬스케어 침해에 기업이 직면하는 가운데, 투자가 가속되는 한편, 반도체의 부족과 단편적인 프라이버시법이 당면의 전개 속도를 억제합니다. 이동통신사에 의한 NB-IoT 네트워크 강화 계약 증가는 연결성 업그레이드를 수익화하는 번들 보안 서비스로의 전략적 시프트를 반영합니다. 지역 제조업체는 하드웨어 수준의 암호화에 필요한 암호화 칩에 대한 제한된 액세스를 보완하기 위해 클라우드 기반 위협 감지 구독을 늘리고 있습니다.

브라질의 PAC 4.0 프로그램은 강력한 암호화, 마이크로 세분화, AI에 의한 비정상적인 감지에 의해 비디오 센서와 데이터 레이크를 보호하는 것이 지자체에 의무화되어 있습니다. 동시의 조달은 국제 규격에 준거하고 벤더는 ISO/IEC 27001 준거의 디바이스를 인증할 것을 요구되고 있습니다. 인근 수도는 조달 템플릿을 복제하여 엔드포인트와 네트워크 액세스 제어의 대응 가능한 기반을 확대하고 있습니다. 통합자의 보고에 따르면 모니터링 계약은 OT와 IT 이벤트를 실시간으로 상관시킬 수 있는 중앙 집중식 보안 운영 대시보드를 지정합니다. 또한 위조 방지 감사 추적 요구 사항은 세계 암호화 칩 부족으로 인해 여전히 부족한 보안 하드웨어 모듈에 대한 수요를 촉진합니다.

이동통신사는 현재 NB-IoT 회선의 각 활성화에 대해 악성 API, 보안 부트스트랩, SIM 수준의 암호화를 패키징하고 연결을 보안 강화 서비스로 바꾸고 있습니다. 멕시코의 4개 통신사는 2024년에 Open Gateway 보안 API를 공동으로 발표했으며, 조기 채택한 은행은 이러한 도구를 사용하여 SIM 스왑 사기 발생을 두 자리 줄였습니다. 5G 독립형 코어의 온라인화에 따라 콜롬비아와 칠레에서도 비슷한 서비스가 등장합니다. 계약 조건에는 종종 봇넷 형성을 차단하기 위해 시그널링 트래픽을 분석하는 AI 기반 위협 점수 엔진이 번들로 제공됩니다. 이동통신사의 경우 이러한 서비스를 통해 사용자 1인당 평균 수익을 높일 수 있지만 기업 고객을 여러 해에 걸쳐 포괄할 수 있습니다.

파운드리은 생산 능력을 이익률이 높은 AI 가속기로 향하게 하고 하드웨어 수준에서 IoT 자격 증명을 보호하는 보안 요소의 출하를 제한합니다. 장치 제조업체는 40주가 넘는 리드 타임에 직면해 있으며, 많은 제조업체는 공격자가 바이패스할 수 있는 소프트웨어 전용 키 스토리지가 장착된 보드를 배송할 수밖에 없습니다. 신뢰할 수 있는 플랫폼 모듈의 최대 70% 인상은 재료비를 늘리고 지방 자치 단체 프로젝트에 공급하는 지역 OEM의 금리를 압박합니다. 일부 구매자는 공급이 안정될 때까지 배포를 연기하므로 공급업체에게 엔드포인트 보안 수익계상이 지연됩니다. 정부는 다른 지역의 신속한 조달을 촉진하기 위해 임시 수입 관세 면제를 고려하고 있습니다.

네트워크 보안은 경계 방화벽과 보안 게이트웨이가 확대되는 디바이스 그룹에 대한 기본적인 안전 가드로 계속 되었기 때문에 2024년에는 6억 8,400만 달러로 평가되었고, 라틴아메리카의 IoT 보안 시장 점유율의 38%에 해당합니다. 클라우드 보안 분야는 2030년까지 4억 3,800만 달러 시장 규모가 확대될 것으로 예측되며, CAGR은 11.20%로 추이할 전망입니다. 또한 하이브리드형 워크 모델은 On-Premise와 SaaS의 제어를 융합시킨 제로 트러스트 네트워크 액세스 솔루션 수요에도 박차를 가하고 있습니다.

클라우드 네이티브 플랫폼은 현재 자세 관리, 런타임 보호 및 소프트웨어 BOM 스캔을 하나의 구독으로 번들로 제공하여 도구 난립을 줄이고 있습니다. Microsoft의 펌웨어 분석 미리보기는 장치, 네트워크 및 클라우드의 각 레이어에 걸쳐 깊은 코드 가시성에 대한 전환을 강조합니다. 분석가들은 이러한 통합 제품이 성숙함에 따라 라틴아메리카의 IoT 보안 시장이 재조정될 것으로 예상하고 있지만, 네트워크 어플라이언스는 클라우드 도달범위가 제한된 브라운필드 산업 사이트에서 여전히 판매될 것으로 보입니다.

아이덴티티 액세스 관리 도구는 2024년 4억 3,200만 달러를 기록했고 라틴아메리카의 IoT 보안 시장 규모에 24%를 기여했습니다. 이러한 도구는 기업 클라우드에 연결하는 수백만 개의 센서의 인증 기반을 형성합니다. 보안 및 취약성 관리는 CAGR 12.50%로 가장 빠르게 성장하고 있습니다. 이는 주목을 받은 랜섬웨어 사건 이후 지속적인 노출 점수에 대한 이사회 수준의 관심 증가를 반영합니다. 자동화된 SBOM 생성은 조달 기준의 주류가 되고 EU의 사이버 레지리언스법(Cyber Resilience Act) 요건에 제품이 적합합니다.

침입 방어 시스템은 결정적인 대기 시간과 즉각적인 패킷 차단을 요구하는 제조 라인에 적합합니다. Data Loss Protection은 전자 의료 기록의 누출에 엄청난 벌금이 부과되는 건강 관리에서 규제 당국의 지원을 받고 있습니다. 통합 위협 관리 번들은 각 보호 레이어의 전문 팀을 구성할 수 없는 중견 기업에 의해 지원됩니다. 이러한 모듈에 텔레메트리를 통합하는 공급업체는 컴플라이언스 의무가 강화되는 동안 크로스셀에 의한 수익원을 획득할 수 있는 입장에 있습니다.

라틴아메리카의 IoT 보안 보안 유형(네트워크 보안, 엔드포인트 보안 등), 솔루션(아이덴티티 및 액세스 관리(IAM), 침입 방어 시스템(IPS) 등), 최종 사용자(헬스케어, 제조업 등), 배포 모델, 지역별로 세분화되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

The Latin America IoT security market size is valued at USD 1.8 billion in 2025 and will reach USD 2.67 billion by 2030, advancing at an 8.21% CAGR.

Expanding smart-city surveillance programs in Brazil, mandatory Zero-Trust rules for Chilean critical infrastructure, and rapid 5G rollouts across Mexico propel spending on connected-device protection. Investments accelerate as enterprises confront record healthcare breaches that exposed 182.4 million people in 2024, while semiconductor shortages and fragmented privacy laws temper near-term deployment velocity. Rising NB-IoT network hardening contracts signed by mobile operators reflect a strategic shift toward bundled security services that monetize connectivity upgrades. Regional manufacturers also increase cloud-based threat-detection subscriptions to compensate for limited access to crypto-chips required for hardware-level encryption.

Brazil's PAC 4.0 program obliges municipalities to protect video sensors and data lakes with strong encryption, micro-segmentation, and AI-driven anomaly detection. City procurements reference international standards, prompting vendors to certify devices for ISO / IEC 27001 compliance. Neighbouring capitals replicate procurement templates, enlarging the addressable base for endpoint and network-access controls. Integrators report that surveillance contracts specify centralised security-operations dashboards able to correlate OT and IT events in real time. The requirement for tamper-proof audit trails also drives demand for secure hardware modules that remain scarce due to global crypto-chip shortages.

Mobile operators now package fraud-prevention APIs, secure bootstrapping, and SIM-level encryption with every NB-IoT line activation, turning connectivity into a security-enhanced service. Mexico's four carriers jointly unveiled Open Gateway security APIs in 2024, and early adopter banks use these tools to cut SIM-swap fraud incidents by double digits. Similar offerings appear in Colombia and Chile as 5G standalone cores come online. Contract terms increasingly bundle AI-based threat scoring engines that analyse signalling traffic to block botnet formation. For operators, these services raise average revenue per user while locking in enterprise customers for multiyear periods.

Foundries redirect capacity toward high-margin AI accelerators, limiting secure element shipments that protect IoT credentials at hardware level. Device makers face lead-times that exceed 40 weeks, forcing many to ship boards equipped with software-only key storage that attackers can bypass. Price hikes of up to 70% for trusted-platform modules inflate bill-of-materials costs, squeezing margins for local OEMs supplying municipal projects. Some buyers postpone rollouts until supply stabilises, translating into slower endpoint security revenue recognition for vendors. Governments consider temporary import-tariff waivers to encourage rapid sourcing from alternate geographies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Network Security generated USD 684 million in 2024, equal to 38% of the Latin America IoT security market share, as perimeter firewalls and secure gateways remained baseline safeguards for expanding device fleets. The Cloud Security segment is forecast to add USD 438 million by 2030, climbing at an 11.20% CAGR as enterprises migrate workloads and insist on policy consistency across multi-cloud tenancy. Hybrid work models also fuel demand for zero-trust network-access solutions that blend on-premises and SaaS controls.

Cloud-native platforms now bundle posture management, runtime protection, and software bill-of-materials scanning in one subscription, reducing tool sprawl. Microsoft's firmware analysis preview underscores a pivot toward deep code visibility that spans device, network, and cloud layers. As these converged offerings mature, analysts expect the Latin America IoT security market to rebalance, yet network appliances will still sell into brownfield industrial sites where cloud reach remains limited.

Identity and Access Management tools booked USD 432 million in 2024, translating to 24% contribution to the Latin America IoT security market size. They form the authentication backbone for millions of sensors plugging into corporate clouds. Security and Vulnerability Management grows fastest at a 12.50% CAGR, reflecting heightened board-level focus on continuous exposure scoring after high-profile ransomware incidents. Automated SBOM generation enters mainstream procurement criteria, aligning products with forthcoming EU Cyber Resilience Act requirements.

Intrusion Prevention Systems stay relevant for manufacturing lines that demand deterministic latency and immediate packet blocking. Data Loss Protection enjoys regulatory pull in healthcare where electronic patient-record breaches carry steep fines. Consolidated threat-management bundles gain traction among mid-tier firms that cannot staff specialist teams for each protection layer. Vendors that integrate telemetry across these modules position themselves to capture cross-sell revenue streams as compliance obligations tighten.

Latin America IoT Security Market Segmented by Type of Security (Network Security, Endpoint Security and More), Solutions (Identity and Access Management (IAM), Intrusion Prevention System (IPS) and More), End-User (Healthcare, Manufacturing and More), by Deployment Model and Geography. The Market Forecasts are Provided in Terms of Value (USD).