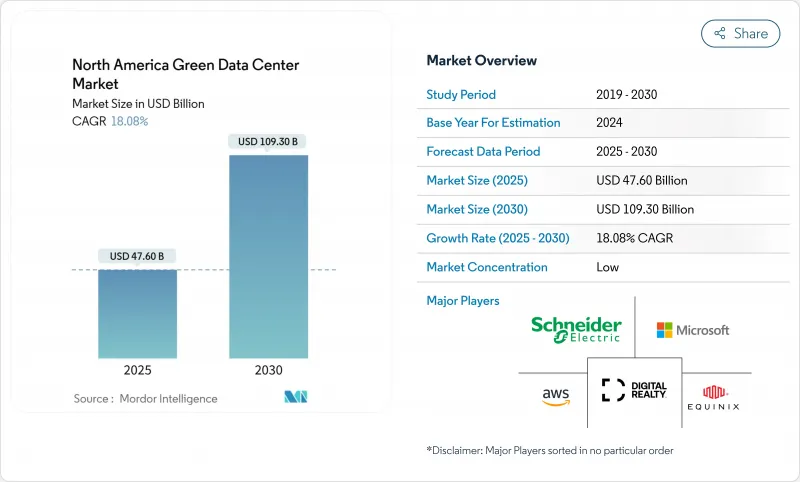

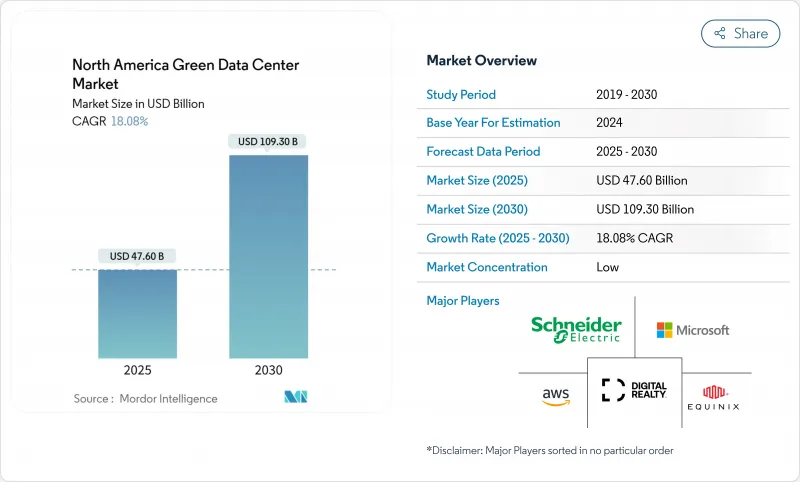

북미의 그린 데이터센터 시장 규모는 2025년 476억 달러로 평가되었고, 2030년에 1,093억 달러에 이를 것으로 예측되며, CAGR은 18.08%를 나타낼 전망입니다.

2023년 176TWh의 전력을 소비한 AI 워크로드 증가, 대규모 재생에너지 전력구매계약(PPA), 그리고 공격적인 하이퍼스케일 투자 계획이 이러한 진전을 뒷받침하고 있습니다. 하이퍼스케일 클라우드 플랫폼은 다중 기가와트 규모의 캠퍼스를 계속 건설하며 고밀도 액체 냉각 및 현장 청정 에너지 생산에 대한 수요를 앞당기고 있습니다. 코로케이션 사업자들은 기업의 탄소중립 의무를 충족시키기 위해 경쟁하며, 지속가능성 지표를 서비스 수준 계약(SLA)에 반영하고 있습니다. 이는 현재 북미 지역 제안 요청(RFP)의 대부분에 영향을 미치고 있습니다. 전력망 연결 지연과 숙련된 인력 부족은 여전히 걸림돌이지만, 경영진 수준의 정책 지원과 AI 기반 공기 흐름 최적화 기술의 혁신이 결합되어 시장 모멘텀을 10년 내내 유지할 것입니다.

하이퍼스케일 운영사들은 현장 태양광, 천연가스 피크 발전소, 원자력 에너지 할당을 통합한 기가와트급 캠퍼스에 자본을 쏟아붓고 있습니다. 애플은 텍사스, 캘리포니아, 노스캐롤라이나에 걸쳐 AI 준비 시설에 5,000억 달러를 투자하기로 했으며, 이는 마이크로소프트의 800억 달러 규모 북미 확장 계획을 반영합니다. 메타는 최대 4GW의 기저 부하 원자력 용량으로 지원되는 루이지애나 복합 시설에 100억 달러를 투입 중입니다. 인프라 메이슨스는 10GW 클러스터 수용이 가능한 청정 에너지 단지를 예측하며, 해당 지역을 지속 가능한 하이퍼스케일 개발의 글로벌 벤치마크로 자리매김할 것으로 전망합니다. 이러한 경쟁은 북미의 그린 데이터센터 시장 내 하이퍼스케일 용량의 24.4% CAGR(연평균 성장률)을 뒷받침합니다.

기업들은 이제 코로케이션 파트너 선정 시 지연 시간이나 가격보다 재생에너지 적합성을 우선시합니다. 아이언 마운틴은 2017년부터 데이터센터 전력 수요의 100%를 재생에너지로 충당해 왔으며, 북미 최초의 BREEAM 인증 사이트를 구축하여 새로운 조달 기준을 제시했습니다. 마이크로소프트의 2030 탄소 네거티브 약속과 2025년 100% 재생에너지 사용 요건은 공급망 전반에 파급되어 공급업체들이 지속가능성 연계 대출과 과학 기반 목표를 채택하도록 압박하고 있습니다. 검증 가능한 탄소 감축 실적을 입증한 공급업체는 우선 협상 대상자로 선정되며, 환경 성과가 결정적 경쟁 우위로 부상하고 있습니다.

저탄소 콘크리트, 대량 목재, 전기로강은 여전히 두 자릿수 프리미엄이 붙습니다. 마이크로소프트의 퀸시 시범 사업은 내재 탄소를 50% 감축했으나 소수 공급업체에서만 구할 수 있는 맞춤형 혼합물이 필요했습니다. 아마존은 43개 신규 센터에 저탄소 강재 사용으로 인한 추가 자본 지출을 공개했으며, 이는 대량 구매 할인 적용 후에도 발생한 비용입니다. 장기적인 에너지 및 브랜드 혜택이 이러한 비용을 상쇄하지만, 고가 대도시 개발사들은 그린본드 수익금이나 세제 혜택 없이는 프로젝트 수익성 확보에 어려움을 겪고 있습니다.

솔루션 부문은 2024년 북미의 그린 데이터센터 시장에서 63.1%의 매출 점유율을 유지하며 계속해서 우위를 점했습니다. 운영사들이 효율적인 전력 공급, 액체 냉각, AI 기반 관리 플랫폼에 투자했기 때문입니다. 이러한 우위는 규모의 경제를 실현하지만, 조달이 표준화되고 마진이 낮은 하드웨어로 전환되면서 성장세는 완화되고 있습니다. 반면 서비스 부문은 탄소중립 로드맵이 지속적인 최적화, 탄소 회계, 규정 준수 감사를 요구함에 따라 연평균 22.1% 성장할 것으로 전망됩니다. 관리형 지속가능성 서비스는 실시간 에너지 대시보드와 과학기반목표(SBT)에 부합하는 시설 운영을 지원하는 컨설팅을 결합합니다.

시스템 통합에 프리미엄 요금을 지불하는 운영사들은 가동 중단 없이 공랭식 홀에서 칩 직결 루프로의 원활한 전환을 기대합니다. 이러한 복잡한 개조 작업은 유체 네트워크 설계, 누출 감지 데이터 처리, 내재 배출량 최소화가 가능한 전문 기업에 의존합니다. 결과적으로 장비 가격은 디플레이션 압력을 받음에도 킬로와트당 서비스 수익이 증가하여 북미의 그린 데이터센터 시장의 장기적 혼합 구조를 견고하게 뒷받침하고 있습니다.

하이퍼스케일러 기업들은 AI 워크로드 집약도와 수직 통합형 청정 에너지 조달 덕분에 2024년 북미의 그린 데이터센터 시장 규모에서 36.1%를 차지했습니다. 이들의 2030년까지 24.4% CAGR(연평균 성장률)은 풍력, 태양광, 소형 모듈형 원자력, 가스 피크 발전 자산에 대한 대규모 선매 계약에 기반하며, 이는 중소 규모 업체들이 따라잡기 어려운 규모입니다. 이들 기업은 AI 제품 출시 시기를 맞추기 위해 전기실과 액체 냉각 매니폴드를 점점 더 사전 제작하여 건설 주기를 단축하고 있습니다.

코로케이션 제공업체들은 하이퍼스케일 업체들의 유입 수요를 확보하기 위해 캠퍼스 시설을 재편하고 있습니다. 신규 건설 시설은 무수 냉각 방식의 100MW 블록, 지속가능성 연계 임대 조항, 주요 클라우드 온램프 직결 광케이블을 특징으로 합니다. 에지 및 기업 사이트는 규모는 작지만 원격의료, 게임 등 지연 시간에 민감한 워크로드에 집중합니다. 재생에너지 마이크로그리드에 대한 투자는 분산형 사이트가 여전히 기업 평균 탄소 목표를 초과 달성할 수 있음을 보여주며, 북미의 그린 데이터센터 시장의 잠재적 대상 풀을 확대합니다.

북미의 그린 데이터센터 시장 보고서는 업계를 서비스(시스템 통합, 모니터링 서비스, 전문 서비스, 기타 서비스), 솔루션(전력, 서버, 관리 소프트웨어 등), 사용자(코로케이션 공급자, 클라우드 서비스 공급자, 기업), 최종 사용자 업계(의료, 금융 서비스, 정부 등)로 분류합니다. 시장 예측은 금액(달러)으로 제공됩니다.

The North America green data center market size reached USD 47.6 billion in 2025 and is on track to hit USD 109.3 billion by 2030, expanding at an 18.08% CAGR.

Escalating AI workloads that consumed 176 TWh of electricity in 2023, wide-scale renewable power purchase agreements (PPAs), and aggressive hyperscale investment plans underpin this advance energy.gov. Hyperscale cloud platforms continue to build multi-gigawatt campuses, pulling forward demand for high-density liquid cooling and on-site clean energy generation. Colocation operators are racing to satisfy corporate net-zero mandates, weaving sustainability metrics into service-level agreements that now influence the majority of North American requests for proposal. Grid interconnection delays and skilled-labor gaps remain headwinds, yet executive-level policy support combined with technology breakthroughs in AI-driven airflow optimisation sustain the market's momentum through the decade.

Hyperscale operators are pouring capital into gigawatt-scale campuses that integrate on-site solar, natural-gas peaker plants, and nuclear energy allocations. Apple committed USD 500 billion for AI-ready facilities across Texas, California, and North Carolina, echoing Microsoft's USD 80 billion North American expansion plan. Meta is channeling USD 10 billion into a Louisiana complex supported by up to 4 GW of baseload nuclear capacity. Infrastructure Masons forecasts clean-energy parks capable of hosting 10 GW clusters, positioning the region as the global benchmark for sustainable hyperscale development. This arms race underwrites the 24.4% CAGR for hyperscale capacity within the North America green data center market.

Enterprises now rank renewable-energy alignment ahead of latency or price when choosing colocation partners. Iron Mountain has matched 100% of its data-center load with renewables since 2017 and built North America's first BREEAM-certified site, driving new procurement benchmarks. Microsoft's 2030 carbon-negative pledge and 2025 100% renewable coverage requirement cascade through supply chains, pushing vendors to adopt sustainability-linked loans and science-based targets. Providers demonstrating verifiable carbon reductions gain preferred-bidder status, elevating environmental performance to a decisive competitive lever.

Low-carbon concrete, mass timber, and electric-arc-furnace steel still price at double-digit premiums. Microsoft's pilot in Quincy cut embodied carbon by 50% but required bespoke mixes available from only a handful of suppliers. Amazon disclosed extra capex for lower-carbon steel across 43 new centres, even after accounting for volume discounts. While long-run energy and brand benefits offset these costs, developers in high-priced metros struggle to make projects pencil without green-bond proceeds or tax incentives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions continued to dominate the North America green data center market, holding 63.1% revenue in 2024 as operators invested in efficient power, liquid cooling, and AI-enabled management platforms. This dominance delivers scale economies, but growth moderates as procurement shifts toward standardised, lower-margin hardware. Services, by contrast, are forecast to expand at 22.1% CAGR because net-zero roadmaps require continuous optimisation, carbon accounting, and compliance audits. Managed sustainability offerings now bundle real-time energy dashboards with advisory support that aligns facilities with Science-Based Targets.

Operators paying premium rates for system integration expect seamless cut-over from air-cooled halls to direct-to-chip loops without downtime. These complex retrofits rely on specialist firms that can design fluid networks, process leak detection data, and minimise embodied emissions. As a result, services revenue per kilowatt is rising even as equipment pricing faces deflationary pressure, underpinning a resilient long-term mix within the North America green data center market.

Hyperscalers captured 36.1% of the North America green data center market size in 2024, thanks to AI workload intensity and vertically integrated clean-energy procurement. Their 24.4% CAGR to 2030 draws on massive forward contracts for wind, solar, small-modular nuclear, and gas-peaking assets that smaller peers cannot match. These players increasingly pre-fabricate electrical rooms and liquid-cooling manifolds, shrinking construction cycles to meet AI product-launch windows.

Colocation providers are retooling campuses to win hyperscale spill-over deals. New builds feature 100 MW blocks with waterless cooling, sustainability-linked lease clauses, and direct fibre to major cloud on-ramps. Edge and enterprise sites, while smaller, focus on latency-sensitive workloads such as telemedicine and gaming. Their investment in renewable micro-grids illustrates how decentralised sites can still exceed corporate-average carbon goals, broadening the addressable pool for the North America green data center market.

North America Green Data Center Market Report Segments the Industry Into Service (System Integration, Monitoring Services, Professional Services, Other Services), Solution (Power, Servers, Management Software, and More), User (Colocation Providers, Cloud Service Providers, Enterprises), and End-User Industry (Healthcare, Financial Services, Government, and More). The Market Forecasts are Provided in Terms of Value (USD).