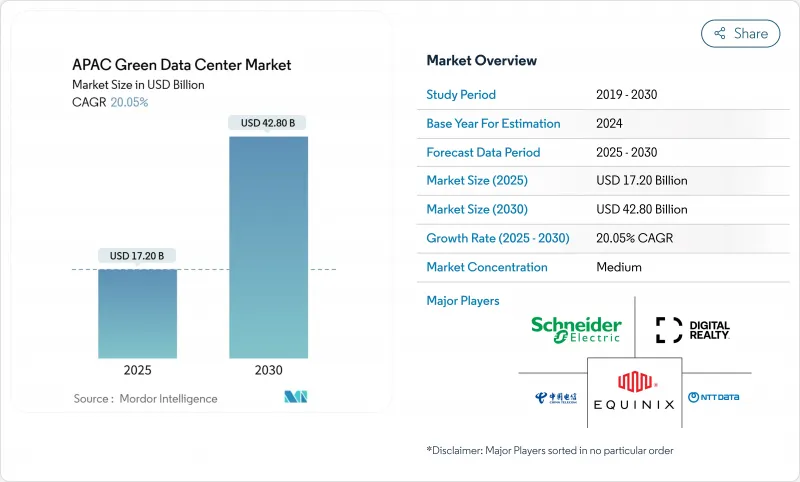

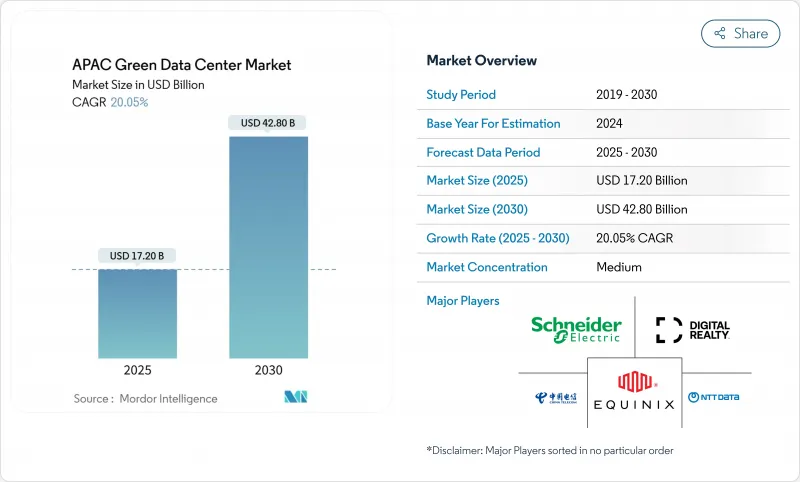

아시아태평양의 그린 데이터센터 시장은 2025년 현재 172억 달러로 추정되고, 2030년에는 428억 달러에 이를 전망이며, CAGR 20.05%로 성장할 것으로 예측됩니다.

하이퍼스케일 배치 증가, 엄격한 넷 제로 정책, 급속한 클라우드 도입으로 중국, 인도, 일본, 동남아시아 전역에서 에너지 효율적인 시설로 자본이 유도되고 있습니다. 액체 및 하이브리드 냉각 플랫폼, 기업의 전력 구매 계약 확대, 녹색 금융으로 인한 가중 평균 자본 비용의 감소가 프로젝트 파이프라인을 가속화하고 있습니다. 또한 기업은 100kW를 넘는 랙에 대응하기 위해 전원 아키텍처의 재구축을 진행하고 있으며, 정부는 재생에너지가 풍부한 2차 도시에 대한 입지 결정을 뒷받침하고 있습니다. 코로케이션 전문 기업, 클라우드 하이퍼스케일러, 인프라 부동산 투자 신탁이 희귀한 토지, 송전망에 대한 액세스, 숙련된 노동력을 둘러싸고 경쟁을 벌이고 있습니다.

GPU를 많이 사용하는 서버의 랙 밀도는 10kW에서 100kW를 초과할 때까지 부풀어 오르며 직접 냉각, 침지 냉각 및 정밀 액체 냉각 시스템으로의 이동을 촉진합니다. SK Telecom과 같은 사업자는 하드웨어 제조업체와 제휴하여 공기 냉각에 비해 에너지 사용량을 최대 30% 줄일 수 있는 차세대 열 솔루션을 상업화하고 있습니다. Equinix는 싱가포르를 포함한 100개 이상의 시설에서 액체 냉각을 도입하여 물 사용량을 줄이면서 AI 서비스 성능을 유지합니다. 랙 밀도를 높이면 바닥 면적이 줄어들고 평방 피트당 수익이 가속화되므로 조기 도입 기업은 비용면에서 우위를 차지할 수 있습니다.

태국은 3개의 하이퍼스케일 캠퍼스를 위해 27억 달러를 기록했고, 인도네시아는 자카르타 확장을 위해 Digital Realty로부터 1억 달러를 받고 있습니다. 말레이시아는 구글에서 20억 달러를 기부하며, 구내 수처리 시설을 포함하고 있습니다. 싱가포르와 도쿄에서는 전력과 토지 부족에 직면한 하이퍼스케일러에게 있어서, 이러한 시장의 새로운 거점은 전개 스케줄을 단축하게 되지만, 개폐 장치나 변압기, 전문업체 공급망에는 부담이 걸립니다.

싱가포르는 2024년에 4년간의 모라토리엄을 해제했지만, 신규 용량은 불과 80MW에 머물렀으며, 개발 사업자는 엄격한 효율성 및 AI 대응 규칙을 충족할 필요가 있습니다. 도쿄도 같은 과제에 직면하고 있습니다. 송전망의 정비가 수요를 따라잡지 못하고, 프로젝트는 지바나 홋카이도로의 이전을 강요하고 있습니다. 제한된 허가가 지가를 상승시키고, 프로젝트 시작을 늦추며, 자본을 쿠알라룸푸르, 자카르타, 방콕으로 향하게 합니다.

AI 클러스터에 신속하게 도입할 수 있는 통합 전원, 냉각, 자동화 스택이 기업에 지지되어 있기 때문에 2024년 아시아태평양의 그린 데이터센터 시장에서는 솔루션이 62.1%의 점유율을 획득했습니다. 설비가 고밀도화를 위해 전기 백본의 배선을 변경하고 있기 때문에 전력 설비가 여전히 가장 큰 하위 부문인 반면, 액체 기술의 보급과 함께 고급 냉각 시스템은 2자리 성장을 기록하고 있습니다. 이 서비스는 설계 및 건설 엔지니어링, 재생에너지 통합 및 인증 컨설팅에 대한 수요에 힘입어 CAGR 22.1%와 현재는 소규모이지만 다른 모든 카테고리를 능가하고 있습니다. 아시아태평양의 그린 데이터센터 서비스 시장 규모는 복잡한 리노베이션과 함께 확대되고 2030년까지 154억 달러에 이를 것으로 예측됩니다. 소프트웨어 정의 에너지 관리 플랫폼과 액체 냉각 하드웨어를 번들링할 수 있는 공급업체는 하이퍼스케일러의 싱글-스로트-투-초크 파트너로서의 지위를 확립하고 있습니다.

기업은 또한 탄소회계감사, 그린본드 조성, 전력 구입 계약 협상 등 전문 서비스에도 눈길을 끕니다. 아마존 시멘트 대체와 같은 저탄소 소재는 도쿄 빌딩에서 64%의 부피 탄소를 줄이고 부품의 기술 혁신이 서비스 자문과 연동하고 있음을 강조합니다. 전기, 기계 및 IT 시스템을 통합하는 전문가는 시운전 위험을 줄이고 투자자의 수익 실현 주기를 단축합니다.

코로케이션 사업자의 2024년 점유율은 36.1%로 선행 투자 없이 확장 가능한 용량을 요구하는 기업에 필수적인 존재로 남아 있습니다. 그러나 AI 모델 훈련과 주권 클라우드 계약에 뒷받침된 하이퍼스케일러는 CAGR 24.4%로 성장을 지속하고 있으며 주요 성장 기관차가 되고 있습니다. 하이퍼스케일러와 관련된 아시아태평양의 그린 데이터센터 시장 규모는 2030년까지 3배 이상이 될 것으로 예측됩니다. TikTok 같은 기업이 태국 호스팅에 5년간 88억 달러의 투자를 약속했기 때문에 자카르타, 조호르, 바탐 섬의 토지 구획을 둘러싼 경쟁이 치열해지고 있습니다.

코로케이션 기업은 액체 대응 화이트 스페이스, 칩 직통 냉각 통로, 랙당 40kW를 넘는 고밀도 급전을 제공함으로써 대응하고 있습니다. 한편, 하이퍼스케일러는 자체 구축 스케줄이 수요를 상회하는 온램프 지역의 코로케이션 이용을 확대합니다. 이동 통신사의 엣지 전개는 실시간 분석을 지원하기 위해 5G 기지국 근처에 마이크로 사이트가 필요하며 다른 레이어가 추가됩니다.

The Asia-Pacific green data center market is currently valued at USD 17.2 billion in 2025 and is forecast to reach USD 42.8 billion by 2030, advancing at a 20.05% CAGR.

Rising hyperscale deployments, strict net-zero policies, and rapid cloud adoption are steering capital toward energy-efficient facilities across China, India, Japan, and Southeast Asia. Liquid and hybrid cooling platforms, wider corporate power-purchase agreements, and lower weighted-average cost of capital from green financing are accelerating project pipelines. Companies are also re-engineering power architectures to support racks that now exceed 100 kW, while governments push location decisions toward secondary cities with abundant renewable energy. Competitive intensity is mounting as colocation specialists, cloud hyperscalers, and infrastructure real-estate investment trusts compete for scarce land, grid access, and skilled labor.

Rack densities have ballooned from 10 kW to beyond 100 kW for GPU-rich servers, prompting a shift toward direct, immersion, and precision liquid cooling systems. Operators such as SK Telecom are partnering with hardware manufacturers to commercialize next-generation thermal solutions that can trim energy use by up to 30% compared with air cooling. Equinix is rolling out liquid cooling in more than 100 facilities, including Singapore, to maintain performance for AI services while curbing water usage. Early adopters gain a cost advantage because higher rack density reduces floor space requirements and accelerates revenue per square foot.

Thailand has earmarked USD 2.7 billion for three hyperscale campuses, while Indonesia is receiving USD 100 million from Digital Realty for a Jakarta expansion. Malaysia has attracted a USD 2 billion pledge from Google that includes on-site water-treatment plants. New sites in these markets shorten deployment timelines for hyperscalers facing power and land caps in Singapore and Tokyo, though they strain regional supply chains for switchgear, transformers, and specialist contractors.

Singapore lifted its four-year moratorium in 2024 but released only 80 MW of new capacity, pushing developers to meet strict efficiency and AI-readiness rules. Tokyo faces similar challenges as grid upgrades lag demand, forcing projects to relocate to Chiba or Hokkaido. Limited permits inflate land prices and slow project starts, redirecting capital toward Kuala Lumpur, Jakarta, and Bangkok.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions captured 62.1% share of the Asia-Pacific green data center market in 2024 as enterprises favor integrated power, cooling, and automation stacks that can be deployed quickly for AI clusters. Power equipment remains the largest subsegment because facilities are re-wiring electrical backbones for higher density, while advanced cooling systems record double-digit growth as liquid technologies spread. Services are smaller today yet outpace all other categories with a 22.1% CAGR, fueled by demand for design-build engineering, renewable-energy integration, and certification consulting. The Asia-Pacific green data center market size for Services is projected to reach USD 15.4 billion by 2030, expanding alongside complex retrofits. Vendors able to bundle software-defined energy-management platforms with liquid cooling hardware position themselves as single-throat-to-choke partners for hyperscalers.

Enterprises also turn to professional services for carbon-accounting audits, green-bond structuring, and power-purchase agreement negotiations. Low-carbon materials, such as Amazon's cement replacements that cut embodied carbon by 64% in Tokyo builds, underscore how component innovation dovetails with service advisory. Integration specialists who can orchestrate electrical, mechanical, and IT systems reduce commissioning risk, shortening revenue realization cycles for investors.

Colocation operators held a 36.1% share in 2024 and remain vital for enterprises seeking scalable capacity without upfront capital. Yet hyperscalers, propelled by AI model training and sovereign-cloud contracts, are registering a 24.4% CAGR, making them the primary growth locomotive. The Asia-Pacific green data center market size tied to hyperscalers is projected to more than triple by 2030. Competition for land bank parcels in Jakarta, Johor, and Batam is intensifying as companies like TikTok pledge USD 8.8 billion over five years for Thailand hosting.

Colocation firms respond by offering liquid-ready white space, direct-to-chip cooling corridors, and high-density power feeds exceeding 40 kW per rack. Hyperscalers, in turn, expand colocation usage for on-ramp regions where self-build timelines exceed demand. Edge deployments by telecom operators add another layer, requiring micro-sites near 5G base stations to support real-time analytics.

Asia Pacific Green Data Center Market Report is Segmented by Services (System Integration, Monitoring Services, and More), Solutions (Power, Servers, Management Software, and More), Users (Colocation Providers, Cloud Service Providers, Enterprises), End-User Industries (Healthcare, Financial Services, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).