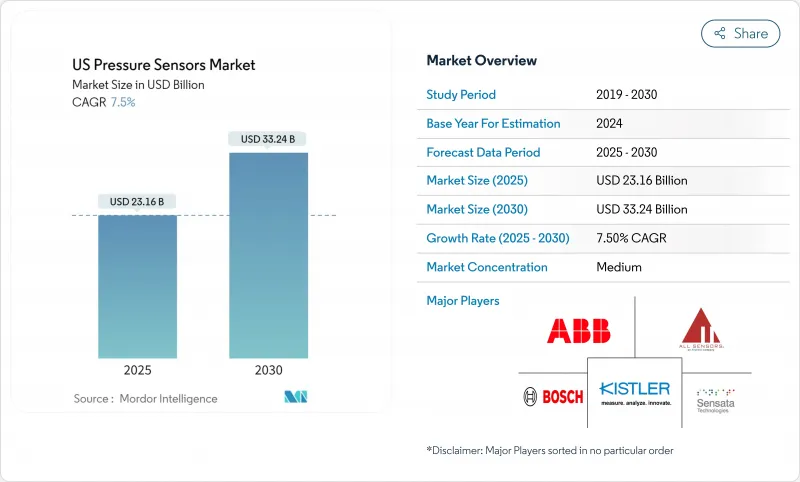

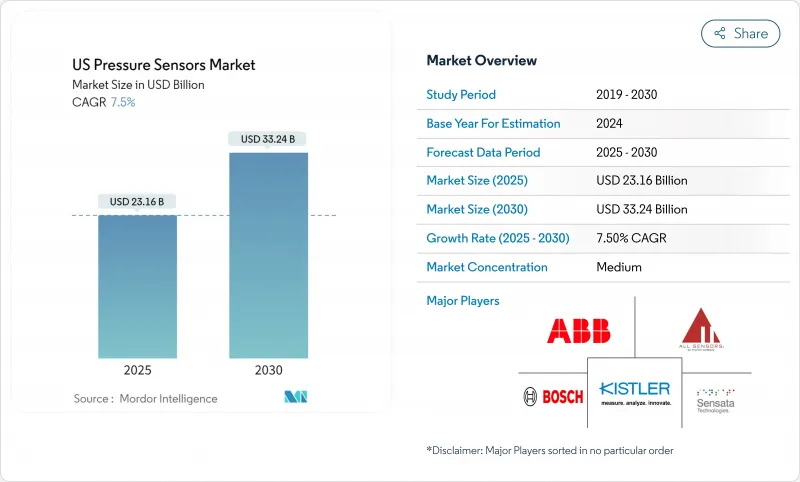

미국의 압력 센서 시장은 2025년에 231억 6,000만 달러로 평가되었고, 2030년에 332억 4,000만 달러에 이를 것으로 예측되며, CAGR은 7.50%를 나타낼 전망입니다.

반도체 제조업체들은 팹(fab)의 진공 및 가스 제어 허용 오차를 전체 범위의 ±0.05% 미만으로 강화하면서 이 확장의 상당 부분을 주도하고 있습니다. 자동차, 의료, LNG 인프라 분야의 강화된 안전 규정은 공급망이 압박을 받을 때에도 수요를 탄력적으로 유지합니다. MEMS와 NEMS 플랫폼의 융합은 비용 곡선을 재편하고 있으며, 나노스케일 장치는 새로운 정확도 기준을 설정하는 동시에 AI 지원 모듈로의 통합을 용이하게 합니다. 배터리 구동 IoT 시스템은 저전력과 온도 안정성을 결합한 정전용량 설계의 채택을 촉진하고 있습니다. 지역적으로는 남부 지역이 에너지 비용 우위로 신규 공장 유치를 이끌고 있는 반면, 헬륨 부족은 장기적 기밀성을 개선하는 패키징 혁신을 촉진하고 있습니다.

1세대 의무 장착 타이어 공기압 모니터링 시스템(TPMS)이 수명 종료 단계에 접어들며 센서 공급업체에 반복적 비즈니스 기회를 창출하고 있습니다. 2007년 TREAD 법 이후 생산된 차량들은 두 번째 및 세 번째 교체 주기에 진입 중이며, 북동부 및 중서부 지역의 겨울철 도로 소금 노출로 배터리 소모가 가속화되고 있습니다. 테슬라 모델에 맞춤화된 바텍 오토 ID의 2025년형 라이트 센서블루(R)는 블루투스 진단 기능을 추가하고 서비스 주기를 연장하는 전기차 최적화 TPMS로의 전환을 보여줍니다. 이 장치에 내장된 예측 경고 기능은 애프터마켓을 사후 대응형 교체에서 정기 유지보수로 전환시켜 프리미엄 가격대를 뒷받침합니다.

확대된 메디케어 및 메디케이드 적용 범위는 자가 측정 혈압 장치에 대해 주별 플랜의 84%에 도달하여 고혈압 환자 약 140만 명의 접근성을 열었습니다. 미시간 주 프로그램은 장치당 최대 75달러를 지급하며 전국적 가격 기준을 설정했습니다. 이러한 환급 환경은 소형 팔 커프에 장착되면서 원격의료 플랫폼으로 데이터를 스트리밍하는 신뢰할 수 있는 저압 센서에 대한 수요를 급증시키고 있습니다.

중상위권 핸드셋 거의 모든 제품에 기압 센서가 탑재되면서 소비자 가전 시장의 물량 성장은 한계에 도달했습니다. 제조사들은 웨어러블용 초저전력 변형이나 드론용 고정밀 고도계 등 차별화된 성능으로 전환하며, 서부 해안 공급망에 집중된 성숙한 시장에서 틈새 시장을 개척하고 있습니다.

MEMS는 2024년 미국의 압력 센서 시장 점유율 31.05%를 차지하며 주류 자동차 및 산업 설계를 뒷받침합니다. 수율 최적화 실리콘 라인은 단위 비용을 낮게 유지하는 반면, 그래핀 멤브레인은 감도를 66 μV/V/kPa까지 끌어올려 고도계 및 의료용 웨어러블의 분해능을 향상시킵니다. 스트레인 게이지 장치는 실리콘 카바이드 변형이 600°C에서도 안정적으로 작동하는 상류 석유와 같은 가혹한 환경에서 여전히 선호됩니다. 광학 센서는 강한 전자기장이 존재하는 환경에서 점유율을 확대하고 있습니다.

파운드리 업체들이 공용 툴링을 도입함에 따라 생산 규모 확대는 MEMS와의 비용 격차를 좁혀 대량 생산 의료용 일회용품 분야에서 광범위한 채택을 가능케 할 것입니다. 이에 따라 미국의 압력 센서 시장은 AI 및 데이터 암호화를 내장한 혼합 기술 모듈에 마이크로 및 나노 형식이 점진적으로 융합되는 양상을 보일 것입니다.

피에조저항형 아키텍처는 제조사가 성숙한 CMOS 백엔드 공정을 재사용할 수 있어 2024년 매출 점유율 46.00%로 선두를 유지했습니다. 최근 실리콘 카바이드 개량으로 제로 출력 온도 계수가 섭씨 1도당 0.08%로 감소하여 가혹한 유전 또는 항공우주 환경 요구사항을 충족합니다. ASIC에 내장된 다항식 회귀 알고리즘은 잔류 오차를 0.008% FS로 줄여 정확도를 임무 핵심 기대치에 부합시킵니다.

10.20%의 연평균 성장률(CAGR)로 증가할 것으로 예상되는 정전용량식 감지 기술은 배터리 구동 IoT 노드에 필수적인 우수한 에너지 효율성을 제공합니다. ES Systems의 2024년 출시 제품은 I2C, SPI 및 아날로그 출력을 제공하면서 ±0.25% FS의 총 오차를 달성합니다. 공진 기술은 0.1 Pa 분해능으로 반도체 챔버 압력을 제어하는 특수 진공 게이지에 계속 적용됩니다. 미국의 압력 센서 시장은 공급업체들이 단일 패키지에 여러 기술을 통합하여 OEM이 애플리케이션별 한계값에 맞춰 성능을 조정할 수 있게 함에 따라 경쟁적 중첩 현상을 보일 것입니다.

미국의 압력 센서 시장 보고서는 센서 유형별(MEMS, 스트레인 게이지, 기타), 기술별(피에조 저항, 정전 용량, 기타), 출력 인터페이스별, 압력 범위별, 용도별(자동차, 의료, 산업, 가전, 기타), 미국 지역별(북동부, 중서부, 기타)로 분류됩니다.

The US pressure sensors market is valued at USD 23.16 billion in 2025 and is projected to climb to USD 33.24 billion by 2030, advancing at a 7.50% CAGR.

Semiconductor manufacturers are driving a large share of this expansion as fabs tighten vacuum and gas control tolerances below +-0.05% full scale. Heightened safety rules in automotive, medical, and LNG infrastructure keep demand resilient even when supply chains face stress. The convergence of MEMS and NEMS platforms is reshaping cost curves, with nanoscale devices setting new accuracy benchmarks while easing integration into AI-ready modules. Battery-powered IoT systems are pushing adoption of capacitive designs that combine low power with temperature stability. Regionally, the South benefits from energy-cost advantages that attract new plants, while helium scarcity is forcing packaging innovation that improves long-term hermeticity.

First-generation mandatory Tire Pressure Monitoring Systems are now reaching end-of-life, creating repeat business for sensor suppliers. Vehicles built after the 2007 TREAD Act are entering second and third replacement cycles, and winter road-salt exposure in the Northeast and Midwest quickens battery depletion. Bartec Auto ID's 2025 Rite-SensorBlue(R), tailored for Tesla models, illustrates the shift toward EV-optimized TPMS that adds Bluetooth diagnostics and extends service intervals. Predictive alerts embedded in these units move the aftermarket from reactive swaps to scheduled maintenance, supporting premium price points.

Expanded Medicare and Medicaid coverage now reaches 84% of state plans for self-measured blood pressure devices, opening access for about 1.4 million beneficiaries with hypertension. Michigan's program pays up to USD 75 per device, setting a national pricing anchor. This reimbursement landscape fuels rapid demand for reliable low-pressure sensors that fit in compact arm-cuffs while streaming data into telehealth platforms.

Nearly every mid-to-high-tier handset now ships with a barometric sensor, capping volume growth in consumer electronics. Manufacturers pivot toward differentiated performance such as ultra-low-power variants for wearables or high-precision altimeters for drones, carving niche gains in an otherwise mature space concentrated in West Coast supply chains.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

MEMS held 31.05% of the US pressure sensors market share in 2024 and underpin mainstream automotive and industrial designs. Yield-optimized silicon lines keep unit costs low, while graphene membranes now lift sensitivity to 66 µV/V/kPa, enhancing resolution for altimeters and medical wearables. Strain-gauge devices remain favored in harsh settings such as upstream oil where silicon carbide variants work reliably at 600 °C. Optical sensors gain ground in environments with strong electromagnetic fields.

As foundries deploy shared tooling, production scale will narrow cost gaps with MEMS, opening broader adoption in high-volume medical disposables. The US pressure sensors market will therefore see a gradual blend of micro and nano formats in mixed-technology modules that embed AI and data encryption.

Piezoresistive architectures led with 46.00% revenue share in 2024 because manufacturers can reuse mature CMOS back-end steps. Recent silicon-carbide revisions cut the temperature coefficient of zero output to 0.08% per °C, fitting harsh oilfield or aerospace needs. Polynomial-regression algorithms embedded in ASICs trim residual errors to 0.008% FS, aligning accuracy with mission-critical expectations.

Capacitive sensing, projected to rise at a 10.20% CAGR, provides superior energy efficiency vital for battery-powered IoT nodes. ES Systems' 2024 release achieves +-0.25% FS total error while offering I2C, SPI, and analog outputs. Resonant techniques stay in specialty vacuum gauges where 0.1 Pa resolution guides semiconductor chamber pressure. The US pressure sensors market will see competitive overlap as vendors integrate multiple technologies into single packages that let OEMs dial performance to application-specific thresholds.

The United States Pressure Sensors Market Report is Segmented by Sensor Type (MEMS, Strain-Gauge and More), Technology (Piezoresistive, Capacitive and More), Output Interface, Pressure Range, Application (Automotive, Medical, Industrial, Consumer Electronics and More), US Region (Northeast, Midwest and More)