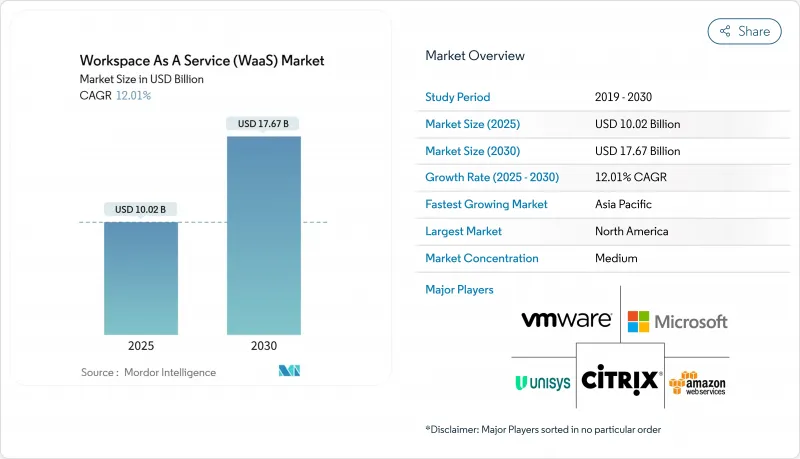

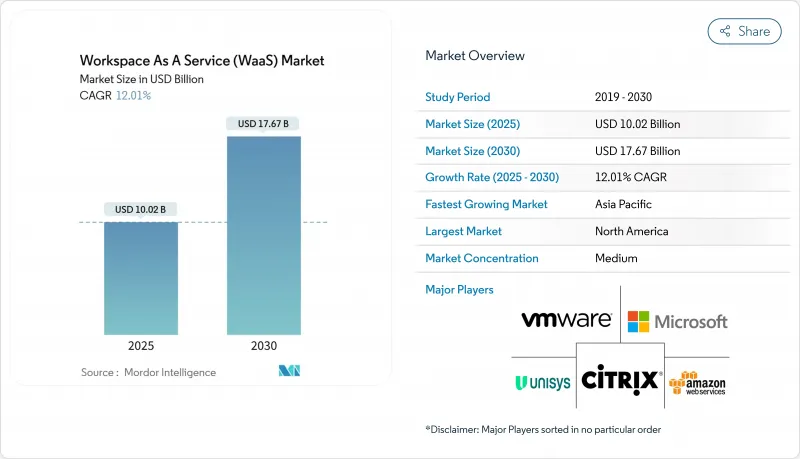

WaaS(Workspace As A Service) 시장 규모는 2025년에 100억 2,000만 달러에 이르고, 2030년에는 176억 7,000만 달러에 달할 것으로 예상됩니다.

기업은 보안, 컴플라이언스 및 생산성 도구를 단일 가상 환경에 통합하는 클라우드 퍼스트 디지털 워크플레이스 아키텍처로 전환하고 있다는 점에서 성장을 뒷받침하고 있습니다. Hyperscaler의 설비 투자액은 3,800억 달러를 넘어, AI 주도의 가상 데스크톱을 지원하는 세계 GPU 용량이 해방되었습니다. 제로 트러스트 프레임워크의 급속한 채용, 컴플라이언스에 대한 모니터링 증가, 보안 하이브리드 워크 요구 사항은 규제가 있는 산업 전체 수요를 지원합니다. 한편 시장의 집중은 완만하기 때문에 기존 벤더와 신흥 클라우드 네이티브 벤더 모두 그래픽 디자인, 금융 거래, 실시간 협업 등의 특수 워크로드를 중심으로 혁신을 진행하고 있습니다.

BYOD(Bring Your Own Device) 정책을 채택하는 기업은 데이터 보호와 통합된 보안을 철저히 하기 때문에 중앙 집중식 가상 데스크톱에 대한 의존도가 높아지고 있습니다. WaaS에 내장된 다중 요소 인증, 세분화된 조건부 액세스 및 세션 격리는 관리되지 않는 하드웨어와 관련된 위험을 줄입니다. 회계 사무소, 법률 사무소 및 설계 사무소에서는 가상 앱이 개인 노트북 및 태블릿에 즉시 전달되므로 계절 직원의 온보딩이 가속화되었다고 보고합니다. 또한 CIO는 IT 자산의 가시성이 향상되었음을 지적합니다. 이 기세로 BYOD는 성숙시장과 신흥 시장 전체에서 중기적인 촉진요인으로 자리매김하고 있습니다.

클라우드에서 호스팅되는 가상 데스크톱은 하드웨어의 대량 업데이트를 없애고 지출을 소비 기반 모델로 이동하여 총 소유 비용을 절감합니다. Amazon WorkSpaces Thin Client 기기는 195달러부터 사용 가능하며 클라우드에서 암호화된 픽셀을 스트리밍합니다. Microsoft Azure Virtual Desktop은 다중 세션 Windows 11을 추가하여 밀도를 극대화하고 세계 데이터센터의 실적를 통해 합병 및 프로젝트의 최고점에 즉시 확장할 수 있습니다. 이러한 효율성은 지금까지 엔터프라이즈급 인프라를 도입하기 위한 자금이 부족했던 아시아태평양의 중소기업에게 가장 강력하게 영향을 미칩니다.

가상 데스크톱은 왕복 지연의 영향을 받습니다. Citrix의 벤치마크 테스트에 따르면 지연이 150ms를 초과하면 사용자 경험이 급격히 떨어지고 300ms를 초과하면 허용되지 않습니다. 많은 지방과 신흥국들은 아직 일관성이 없는 광대역에 의존하고 있으며, 입력 지연, 음성 누락, 그래픽 불선명 등이 도입 의욕을 깎아내는 원인이 되고 있습니다. 하이퍼스케일러는 이웃 에지 영역과 적응형 UDP 전송에 의해 제약을 완화하지만, 마지막 마일의 인프라는 여전히 이질적입니다. 특히 고해상도 비디오 및 CAD 워크로드를 포함한 배포에서는 정부 중심의 광섬유 배포와 5G 고정 무선 테스트 운영이 매우 중요합니다.

2024년 WaaS(Workspace As A Service) 시장에서는 Desktop as a Service가 56.7%의 점유율을 확보했습니다. 이는 레거시 업무용 소프트웨어를 지원하는 풀 OS 이미지에 대한 근본적인 수요를 반영합니다. 패치 집중 적용, 황금 이미지 관리, 즉각적인 롤백은 개별 노트북에 비해 컴플라이언스를 단순화하기 때문에 기업은 이 모델을 선호합니다. 또한 DaaS의 채용은 시간 단위 요금으로 계약자와 계절 직원에게도 원활하게 확장할 수 있습니다. 이 부문의 리더십을 통해 플랫폼 공급업체는 정체성, 관측 가능성, 엔드포인트 분석과 같은 보완적인 기능을 통합 콘솔에 통합합니다.

통합 협업 스위트는 2030년까지 연평균 복합 성장률(CAGR)이 13.1%로 가장 빠르게 성장하는 카테고리입니다. 채팅, 통화, 문서 공동작업, 워크플로 자동화를 결합한 번들은 도구 난립을 줄이고 라이선스 통합을 촉구합니다. 기존 Office 365 계약 내에서 Microsoft Teams는 교육 기관과 신흥 기업에서 Google Workspace가 압도적인 점유율을 차지합니다. 공급업체는 현재 회의 기록 AI, 화이트보드 및 로우코드 프로세스 빌더를 통합하여 제품군을 보다 광범위한 디지털 경험 플랫폼의 런치패드로 자리잡고 있습니다. 이러한 흐름은 기업이 일관된 생태계를 지향함에 따라 단일 회의 및 스토리지 솔루션을 점차 희박하게 만들 것입니다.

2024년 WaaS(Workspace As A Service) 시장 규모의 67.5%는 On-Premise가 차지했습니다. 이러한 시설에서는 VDI 소프트웨어와 개인 데이터센터에서 실행되는 하이퍼 컨버지드 클러스터가 결합되는 경우가 많습니다. 그러나 엄격한 용량 계획, 하드웨어 업데이트 주기, 개별 재해 복구 사이트로 자본 비용이 높아지고 있습니다.

클라우드 도입은 2030년까지 연평균 복합 성장률(CAGR)이 13.8%로 가장 높을 전망입니다. 공급자는 엔터프라이즈급 GPU, 자동화된 탄력성, 세계 중복성을 초기 비용 없이 제공합니다. Microsoft의 Azure Virtual Desktop on Azure Stack HCI는 On-Premise에서 가상 세션 호스트를 호스팅하면서 클라우드에서 이를 제어하여 두 세계의 교량을 제공합니다. 유럽 기업들은 GDPR(EU 개인정보보호규정)과 Schrems II 데이터 전송 규정을 준수하는 소블린 클라우드 지역을 찾고 있습니다. 시간이 지남에 따라 엄격한 규제 기업에서도 퍼블릭 클라우드 운영 모델이 새로운 그린 필드 도입과 워크로드 확대를 지배하게 될 것입니다.

북미는 성숙한 클라우드 인프라, 높은 광대역 보급률, 기술, 금융, 미디어 분야에서의 조기 도입에 힘입어 2024년 WaaS(Workspace As A Service) 시장에서 35.6%의 점유율을 획득해 선두를 유지했습니다. 원격 근무의 데이터 관리에 대한 규제가 명확해짐에 따라 롤아웃이 가속화되었고, 여러 대도시 지역에서 하이퍼스케일러의 밀도가 대기 시간을 최적의 임계값 내로 억제했습니다. 아마존의 100억 달러를 투자한 노스캐롤라이나 캠퍼스 등 AI에 최적화된 데이터센터에 대한 지속적인 민간 투자는 이 지역공급 기반을 지속적으로 강화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 12.7%를 나타낼 것으로 예측됩니다. 인도, 인도네시아 및 베트남 정부는 광섬유 및 5G 커버리지를 확대하기 위한 보조금과 주파수 인센티브를 기록하여 중소기업과 공공기관이 On-Premise IT에서 클라우드 데스크톱으로 전환할 수 있도록 합니다. 아마존은 호주 데이터센터에 200억 호주 달러를 할당하고 새로운 태양광 발전소와 결합하여 지역의 녹색 인프라에 대한 의욕을 강조합니다. 일본과 한국의 국내 클라우드 제공업체도 언어 모델 개발과 3D 설계를 지원하는 GPU 리치 클러스터를 발표하고 있으며, 이웃 영역에서 제공되는 고성능 워크스테이션 수요에 박차를 가하고 있습니다.

유럽은 계속해서 소블린 클라우드의 틀을 축으로 한 성장의 축이 되고 있습니다. 유럽 데이터 법(European Data Act)과 분야별 의무화로 인해 워크로드는 지역 경계 내에 머물러야 하기 때문에 프랑스, 독일, 북유럽에서는 신뢰할 수 있는 클라우드 파트너 네트워크의 도입이 진행되고 있습니다. VMware의 소블린 클라우드 참조 아키텍처는 가상 데스크톱 인증을 신속하게 수행할 수 있는 표준화된 컴플라이언스 템플릿을 제공합니다. 하드웨어 업데이트 주기에 따라 많은 기업들이 On-Premise 랙을 축소하고 퍼블릭 클라우드의 공인 지역에 가입하고 있습니다. 중동 및 아프리카에서는 경제 다양화 프로그램과 관련된 새로운 도입이 보이지만, 라틴아메리카에서는 섬유 백본과 에지 노드가 역사적인 대역폭 갭을 해소하고 꾸준한 기세를 보이고 있습니다.

The Workspace As A Service (WaaS) Market size reached USD 10.02 billion in 2025 and is projected to climb to USD 17.67 billion by 2030, reflecting a steady 12% CAGR over the forecast period.

Growth is underpinned by enterprises shifting to cloud-first digital workplace architectures that converge security, compliance, and productivity tools into a single virtual experience. Hyperscaler capital spending exceeding USD 380 billion has unlocked global GPU capacity that supports AI-driven virtual desktops, while pay-as-you-go pricing keeps barriers low for small teams in every sector. Rapid adoption of zero-trust frameworks, rising compliance scrutiny, and secure hybrid-work requirements sustain demand across regulated verticals. Meanwhile, moderate market concentration encourages both incumbents and emerging cloud-native vendors to innovate around specialized workloads such as graphics design, financial trading, and real-time collaboration.

Organizations adopting Bring Your Own Device policies increasingly rely on centralized virtual desktops to protect data and enforce uniform security. Multi-factor authentication, granular conditional access, and session isolation embedded in WaaS reduce risks tied to unmanaged hardware. Accounting, legal, and design firms report faster onboarding of seasonal staff because virtual apps are delivered instantly to personal laptops and tablets. CIOs also cite improved IT asset visibility, since device-agnostic delivery keeps intellectual property inside the datacenter rather than on endpoints. This momentum positions BYOD as a mid-term driver across mature and emerging markets.

Cloud-hosted virtual desktops lower total cost of ownership by removing bulk hardware refreshes and shifting expenditure to consumption-based models. Amazon WorkSpaces Thin Client devices start at USD 195 and stream encrypted pixels from the cloud, illustrating how central management reduces desk-side support. Microsoft Azure Virtual Desktop adds multi-session Windows 11 to maximize density, while global datacenter footprints enable instant scaling during mergers or peak project phases. These efficiencies resonate most strongly with Asia-Pacific SMEs that previously lacked capital for enterprise-grade infrastructure.

Virtual desktops are highly sensitive to round-trip delay. Citrix benchmark testing shows user experience falls sharply once latency breaches 150 milliseconds and becomes unacceptable beyond 300 milliseconds. Many rural districts and emerging economies still rely on inconsistent broadband, leading to input lag, audio dropouts, and blurred graphics that discourage adoption. Hyperscalers mitigate constraints through nearby edge zones and adaptive UDP transport, yet last-mile infrastructure remains uneven. Government-sponsored fiber rollouts and 5G fixed-wireless pilots will be pivotal, especially for deployments involving high-definition video or CAD workloads.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Desktop as a Service secured 56.7% share of the Workspace as a Service market in 2024, reflecting persistent demand for full operating-system images that support legacy line-of-business software. Enterprises favor the model because centralized patching, golden-image management, and instant rollback simplify compliance compared with individual laptops. DaaS adoption also scales smoothly for contractors and seasonal staff thanks to hourly billing. The segment's leadership has prompted platform vendors to merge complementary functions such as identity, observability, and endpoint analytics into unified consoles.

Integrated Collaboration Suites represent the fastest-rising category at 13.1% CAGR through 2030. Bundles combining chat, calling, document co-authoring, and workflow automation reduce tool sprawl and encourage license consolidation. Microsoft Teams inside existing Office 365 agreements and Google Workspace in education and startup cohorts dominate volumes. Vendors now embed meeting-transcription AI, whiteboarding, and low-code process builders, positioning suites as a launchpad for broader digital experience platforms. This trajectory will gradually dilute standalone conferencing or storage solutions as firms gravitate toward cohesive ecosystems.

On-premise deployments controlled 67.5% of the Workspace as a Service market size in 2024 as enterprises leveraged sunk investments and asserted data sovereignty. Such estates often pair VDI software with hyperconverged clusters running in private datacenters. However, stringent capacity planning, hardware refresh cycles, and separate disaster-recovery sites keep capital costs high.

Cloud deployment is set to register the strongest 13.8% CAGR to 2030. Providers deliver enterprise-grade GPUs, automated elasticity, and global redundancy without upfront spend. Microsoft's Azure Virtual Desktop on Azure Stack HCI bridges both worlds by hosting virtual session hosts on-premise while controlling them from the cloud. European organizations gravitate toward sovereign cloud regions that address GDPR and Schrems II data transfer rulings. Over time, the public-cloud operating model will dominate new greenfield deployments and workload expansion even among highly regulated entities.

The Workspace As A Service (WaaS) Market Report is Segmented by Solution (Desktop As A Service (DaaS), Application As A Service (AaaS), and More), Deployment Model (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Education, Retail and E-Commerce, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained leadership with 35.6% share of the Workspace as a Service market in 2024, supported by mature cloud infrastructure, high broadband penetration, and early adoption across technology, finance, and media. Regulatory clarity around remote work data controls accelerated rollouts, while hyperscaler density in multiple metropolitan zones kept latency within optimal thresholds. Ongoing private-sector investments in AI-optimized datacenters, including Amazon's USD 10 billion North Carolina campus, continue to reinforce the regional supply base.

Asia-Pacific is projected to record the fastest 12.7% CAGR to 2030. Governments in India, Indonesia, and Vietnam earmark grants and spectrum incentives to extend fiber and 5G coverage, enabling SMEs and public agencies to leapfrog on-premise IT in favor of cloud desktops. Amazon's AU$20 billion allocation for Australian datacenters paired with new solar farms underscores regional appetite for green infrastructure. Domestic cloud providers in Japan and South Korea are also launching GPU-rich clusters to support language-model development and 3D design, fueling demand for high-performance workstations served from nearby zones.

Europe remains a growth pivot anchored on sovereign cloud frameworks. The European Data Act and sector-specific mandates force workloads to stay inside regional boundaries, prompting France, Germany, and the Nordics to adopt trusted cloud partner networks. VMware's sovereign-cloud reference architecture offers standardized compliance templates that expedite virtual desktop certification. As firms renew hardware cycles, many downsize on-premise racks and subscribe to sanctioned public-cloud regions, blending performance with legal assurance. The Middle East and Africa register nascent uptake tied to economic diversification programs, while Latin America sees steady momentum where fiber backbones and edge nodes close historic bandwidth gaps.