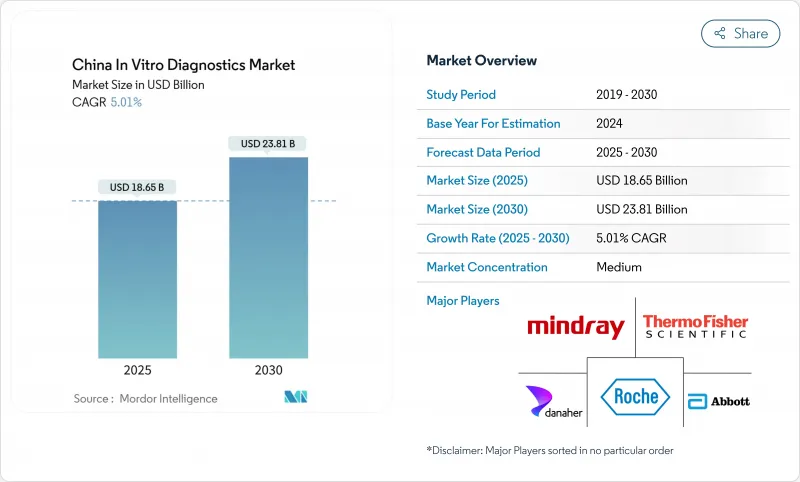

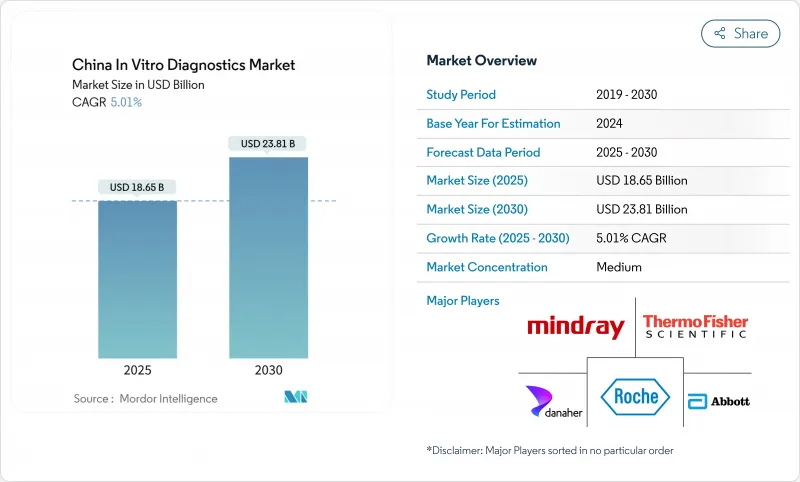

중국의 체외진단 시장은 2025년에 186억 5,000만 달러, 2030년에는 238억 1,000만 달러에 이를 것으로 예상되며, CAGR은 5.01%를 나타낼 전망입니다.

급속한 고령화, 만성 질환 부담의 무게, 1차 진료 진단에 대한 꾸준한 정책 지원이 수요를 뒷받침하고 있습니다. 합리화된 국가의약품관리국(NMPA) 패스웨이는 고가치검사의 심사기간이 단축되는 반면, 완성기반조달(VBP)에 의해 가격 투명성이 확보되어 하층환경에서의 폭넓은 채용이 촉진되고 있습니다. 현지 제조업체는 20%의 조달 가격의 우위를 활용해 점유율을 획득하고 Tier2/3의 병원에 내장된 인공지능(AI) 툴은 소요 시간을 30분에서 5분으로 단축합니다. 동시에, 감염 제어 프로토콜이 정착되고 POC(Point of Care) 솔루션이 지역 클리닉에 침투함에 따라 일회용 플랫폼이 견인력을 증가시키고 있습니다.

당뇨병은 1억 4,000만 명 이상의 성인을 앓고 있으며, 포도당 모니터링과 HbA1c 검사에 대한 수요가 지속되고 있습니다. HIV 감염자는 2023년까지 130만 명 가까이에 이르렀으며, 전통적인 위험 그룹 외에도 스크리닝 대상이 확산되고 있습니다. HIV 감염자의 결핵 스크리닝에 있어서의 CRP 검사의 감도는 72.23%이며, 멀티 마커 패널의 필요성을 강조하고 있습니다. POC(Point-of-Care)의 HbA1c 검사는 도시 지역에서는 500.06 USD/QALY, 농촌 지역에서는 185.10 USD/QALY의 비용 대 효용비를 실현하고, 국가의 지불 의사액(willingness-to-pay)의 임계치 내에 충분히 들어가 있습니다. 이러한 요인은 종합적으로, 특히 지방 분권적인 환경에서 분자 및 면역 측정법의 보급을 지원합니다.

중국에서는 60세 이상의 노인이 3억 1,000만 명에 달하고, 심혈관, 종양, 인지기능 검사에 대한 수요가 높아지고 있습니다. 조정조사에 따르면 2차 도시에서 노인들 수요와 진단 능력의 격차가 확대되고 있습니다. 정부 지출은 2030년까지 205조 위안(28조 2,000억 달러)에 이를 것으로 예상되며 진단제는 노인 의료에 충당됩니다. 해남성의 농촌네트워크에서는 건강 올인원 머신이 환자의 내원률을 37.85%, 클리닉 매출을 54.03% 밀어 올렸습니다. 이러한 인구동태의 변화는 자동화된 멀티 컨디션 검사 플랫폼의 밑바탕이 되고 있습니다.

수량 기준 조달은 확립된 기술에 유리하며 신흥 분자 및 AI 대응 검사의 지불 코드를 지연시킵니다. 71 도시에서 실시한 Diagnosis-Intervention Packet의 시험적 도입은 상환의 진화를 강조하지만, 보험 제도간의 불공평을 초래해, 신규 검사법의 도입을 지연시킬 위험도 있습니다.

분자진단제는 2024년에 39.37%의 점유율을 차지하고 중국의 체외진단 시장을 지원했습니다. 2030년까지 연평균 복합 성장률(CAGR)은 5.84%로 면역진단제가 가장 빠르고, 자동화와 감염 감시의 필요성이 배경으로 BGI Genomics의 Illumina에 대한 소송의 성공과 시퀀싱 기기의 매출 4% 증가는 자국의 기세를 나타냅니다. 임상 화학은 견고한 병원 네트워크를 통해 관련성을 유지하고 신속한 핵산 방법과 CRISPR 검출은 유행에 대한 대비를 강화합니다.

중국의 체외진단(IVD) 업계는 2차 병원에서 AI를 활용한 검사 메뉴 최적화로 처리량 향상의 혜택을 받습니다. COVID-19 이후 미생물 검사는 재주목받고 C 반응성 단백질 검사는 결핵 프로그램을 확대합니다. 소변 검사 및 틈새 패널은 처리 오류를 줄이는 통합 POC 장치로 점유율을 확대합니다. Microfluidics와 sample-to-answer 카트리지가 발전하고 분자진단은 혁신의 최전선에 있습니다.

시약 및 소모품은 2024년 매출의 62.29%를 차지하며 체외진단 시장의 경상수익의 기간이 되었습니다. 그러나 소프트웨어 및 서비스는 검사실의 디지털화에 따라 2030년까지의 CAGR이 6.35%를 나타낼 전망입니다. Mindray의 HyTest와 DiaSys 인수는 수직 통합을 강화하고 Chemclin의 자동 면역 검출 시스템은 국내 비용 우위와 수출 수준의 품질을 양립시킵니다.

실험실 정보 관리 시스템, AI 분석, 클라우드 대시보드는 워크플로우를 변화시키고 블록체인 툴은 개인정보보호법에 따른 데이터 보안 의무에 대응합니다. 장비 제조업체는 하드웨어, 소프트웨어 및 소모품을 번들로 구독 모델로 축발을 옮겨 VBP 가격 압력을 완화합니다. 중국의 체외진단(IVD) 산업은 이를 통해 제품 중심에서 플랫폼 중심 가치 창출로 전환합니다.

The China in vitro diagnostics (IVD) market stands at USD 18.65 billion in 2025 and is forecast to reach USD 23.81 billion by 2030, registering a 5.01% CAGR.

Demand is buoyed by a rapidly ageing population, the country's high chronic-disease burden, and steady policy support for primary-care diagnostics. Streamlined National Medical Products Administration (NMPA) pathways shorten review timelines for high-value tests, while volume-based procurement (VBP) anchors price transparency and encourages wider adoption in lower-tier settings. Local manufacturers leverage 20% procurement price advantages to capture share, and artificial-intelligence (AI) tools embedded in tier-2/3 hospitals slash turnaround times from 30 minutes to five. Concurrently, disposable platforms gain traction as infection-control protocols persist and point-of-care (POC) solutions penetrate rural clinics.

Diabetes affects over 140 million adults, prompting sustained demand for glucose monitoring and HbA1c testing. HIV cases reached nearly 1.3 million by 2023, broadening screening beyond traditional risk groups. C-reactive protein testing shows 72.23% sensitivity for tuberculosis screening among HIV-infected persons, highlighting the need for multi-marker panels. Point-of-care HbA1c tests deliver cost-utility ratios of USD 500.06/QALY in cities and USD 185.10/QALY in rural areas, well within national willingness-to-pay thresholds. These factors collectively sustain molecular and immunoassay volumes, particularly in decentralised settings.

China counts 310 million citizens aged 60 and above, intensifying utilisation of cardiovascular, oncology and cognitive assays. Coordination studies point to widening gaps between elderly demand and diagnostic capacity in secondary cities. Government spending is projected to hit CNY 205 trillion (USD 28.2 trillion) by 2030, with diagnostics earmarked for geriatric care. Health All-in-One Machines boosted patient visits 37.85% and clinic revenue 54.03% in Hainan's rural network. The demographic shift therefore underpins automated, multi-condition test platforms.

Volume-based procurement favours established technologies, delaying payment codes for emerging molecular and AI-enabled tests. Diagnosis-Intervention Packet pilots in 71 cities underscore reimbursement evolution but also risk inequities across insurance schemes, slowing novel assay uptake.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Molecular diagnostics held 39.37% share in 2024, anchoring the China in vitro diagnostics (IVD) market. Immunodiagnostics rises fastest at 5.84% CAGR to 2030, backed by automation and infection-surveillance requirements. BGI Genomics' legal success against Illumina and a 4% uptick in sequencing-device sales illustrate home-grown momentum. Clinical chemistry remains relevant through entrenched hospital networks, while rapid nucleic-acid methods and CRISPR detection bolster pandemic preparedness.

The China in vitro diagnostics (IVD) industry benefits from AI-enhanced test-menu optimisation in secondary hospitals, improving throughput. Microbiology enjoys renewed focus after COVID-19, with C-reactive protein tests expanding tuberculosis programmes. Urinalysis and niche panels gain share through integrated POC devices that lower handling errors. Advances in microfluidics and sample-to-answer cartridges keep molecular diagnostics at the innovation frontier.

Reagents and consumables generated 62.29% revenue in 2024 and remain the backbone of recurring income for the China in vitro diagnostics (IVD) market. Yet software and services post a 6.35% CAGR to 2030 as laboratories digitise. Mindray's purchases of HyTest and DiaSys reinforce vertical integration, while Chemclin's automated immunodetection systems marry local cost advantages with export-level quality.

Laboratory-information management systems, AI analytics and cloud dashboards transform workflows, and blockchain tools address data-security mandates under the Personal Information Protection Law. Instrument makers pivot to subscription models bundling hardware, software and consumables, cushioning VBP price pressure. The China in vitro diagnostics (IVD) industry thereby transitions from product-centric to platform-centric value creation.

The China In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Microbiology, and More), Product (Instrument, Reagents & Consumables, and More), Usability (Disposable IVD Devices and Reusable IVD Devices), Application (Infectious Disease, Diabetes, Cardiology, and More), and End-User (Hospitals & Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).