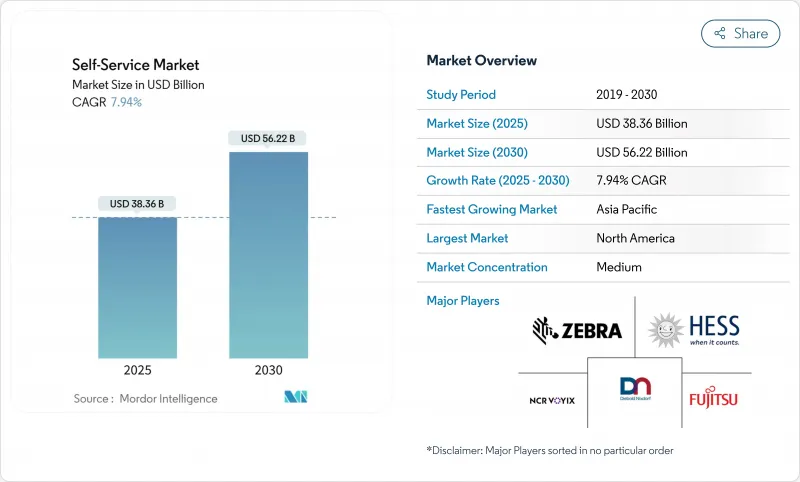

셀프 서비스 시장 규모는 2025년에 383억 6,000만 달러, 2030년에는 562억 2,000만 달러로 확대될 것으로 예측되며, 이 기간의 CAGR은 7.9%를 나타낼 전망입니다.

이 성장은 유행(세계적 유행) 이후 가속화된 비접촉식 결제로의 전환, 디지털화에 대한 기업의 의무화 강화, 디지털 지갑에 대한 일반 시민의 광범위한 친근감과 직접 연결되어 있습니다. 하드웨어 및 소프트웨어 공급업체는 대기 시간을 단축하고, 보안을 강화하고, 은행, 소매, 건강 관리, 공공 장소 등에서 새로운 이용 사례를 개척하는 AI, 컴퓨터 비전, 생체 인증 모듈을 통합하여 대응하고 있습니다. QR과 NFC로 구축된 결제 생태계는 이제 많은 도심지에서 주류가 되고 있으며, 사용자가 선호하는 모든 자격 증명을 수용할 수 있는 셀프 서비스 단말기에 대한 안정적인 수요를 지원하고 있습니다. 벤더는 또한 서비스 계약과 플랫폼 수수료를 강조했으며, 일단 하드웨어 판매가 있었던 것을 현금 흐름을 원활하게 하는 정기 수익원으로 바꾸고 있습니다. 그러나 파괴 행위, 옥외의 극단적인 날씨, 전자상거래에 의한 대안에 대한 내성은 이익을 창출하는 전개의 전제조건으로 남아 있습니다.

세계 디지털 결제 참여율은 2014년의 44%에서 2022년에는 성인의 3분의 2로 급증하여 현금없는 행동에 대한 지속적인 경사가 확인되었습니다. 유럽 조사는 위생 우려로 인해 현금을 피할 의향이 지속되고 있음을 보여주며 소규모 시장 운영자는 현금없는 모듈을 설치 한 후 수익이 증가했다고보고했습니다. 지난 10년 동안 현금 사용이 반감된 스웨덴과 같은 국가들은 정책, 상인, 소비자가 얼마나 빠르게 디지털 레일에 수렴하는지 강조하고 있습니다. 이 선호도는 생체인증 탭과 음성 프롬프트에도 확장되어 셀프 서비스 시장 구석구석까지 노터치 인증에 대응을 촉구하고 있습니다.

RFID 게이트, 컴퓨터 비전, 스마트 선반에 의존하는 무인 매장은 크게 성장할 것으로 예측됩니다. 독일에서는 최근 셀프 레지의 매장 수가 5,000개를 넘어 소매업체가 추가 가속화를 계획하고 있습니다. 미국에서는 Sam's Club과 같은 도매 체인이 몇 초 안에 장바구니를 스캔하는 AI 강화 장치를 도입하고 행렬을 줄이고 직원을 재배치하고 있습니다. 마이크로플루필먼트 허브는 통합에 고민하면서도 인구밀도가 높은 지구에 당일 보충을 약속하고, 24시간 언제든지 상품의 불출과 수취가 가능한 로커나 하이브리드 키오스크에의 끌기를 낳고 있습니다.

브리티시 텔레콤의 데이터에 따르면, 견고한 잠금과 알람이 사건을 억제할 때까지 매년 수만 개의 공중 전화에 대한 공격이 있었습니다. 정교한 잭팟과 스키밍으로 인해 물리적 및 사이버 보안 시장은 2032년까지 324억 달러에 이를 것으로 예상됩니다. 사업자는 사기에 대항하기 때문에 지문인증, 얼굴인증, 다요소 프롬프트를 추가하고 있지만 새로운 모듈이 늘어날 때마다 단가가 올라 인증주기가 길어지고 있습니다. 경찰과의 공동 순찰과 AI 감시는 손실을 줄이지만 완전히 지울 수는 없습니다.

2024년 셀프 서비스 시장 점유율은 키오스크 단말기가 36.2%를 차지했으며, 체크인, 티켓 발권, 청구서 지불 등의 유연성이 강조되었습니다. 키오스크 단말기와 관련된 셀프 서비스 시장 규모는 언어 팩, AI 아바타 및 결제 수단 선택 사항을 추가하는 지속적인 소프트웨어 업데이트를 통해 혜택을 누리고 있습니다. 셀프 프레지는 식료품점과 종합 슈퍼가 인건비를 억제하고 금전 등록기 대기 시간을 단축하여 CAGR 8.3%를 나타낼 전망입니다. ATM은 여전히 현금 생태계를 지원하지만, 모바일 결제가 많은 저액 결제 요구를 충족하게 되었기 때문에 연간 설치 대수는 두드러지고 있습니다. 자동판매기는 스낵 과자뿐만 아니라 OTC 의약품, PPE, 일각을 다투는 백신에도 진출해 사회적 실적의 폭을 넓히고 있습니다. 스마트 로커는 최종 원 마일의 비용 절감을 촉구하고 시간외 소포 수령을 가능하게 하기 위해 물류 회사로부터 활발한 주문을 등록했습니다. 헬스케어 키오스크는 2024년 8억 달러에서 2028년 18억 1,000만 달러로 성장할 것으로 예측되며 진단, 원격 의료 및 처방전 업데이트가 컴팩트한 실적로 수렴하는 방법을 보여줍니다. 소매업체는 컴퓨터 비전을 채택하여 카메라가 자동으로 상품의 무게를 측정하여 실수나 구매자의 불만을 최소화합니다. 제품 믹스는 실시간 인사이트와 원격 서비스를 가능하게 하는 클라우드 훅과 내구성을 결합한 공급업체에 계속 보상됩니다.

키오스크 단말기 공급업체는 항균 가공, 촉각 피드백, 휠체어 대응 레이아웃 등에 투자하여 접근성 규제를 선점합니다. 셀프 레지 제조업체는 핀텍 게이트웨이와 제휴하여 결제 보안 기준을 준수하면서도 구매 및 후불을 가능하게 합니다. ATM 벤더는 비디오 텔러 머신과 암호화폐 모듈로 축 발을 옮겨 관련성을 유지합니다. Vending의 전문가들은 역동적인 냉장과 AI 플라노그램을 테스트하고 빠른 움직임 인벤토리를 처음으로 진열하여 평방인치 당 매출을 향상시킵니다. 사물함 공급자는 식료품 및 의약품 부문에 온도 관리를 추가합니다. 따라서 포트폴리오의 폭은 셀프 서비스 시장에서 소비자의 흐름과 가맹점의 경제성 변화에 대한 헤지로 계속되고 있습니다.

2024년 수익의 54.0%는 하드웨어가 차지했지만, 소프트웨어는 매년 9.0%씩 증가하고 있으며, 평생 수익화의 열쇠를 잡고 있습니다. 벤더는 컨테이너화된 운영 체제를 도입하여 현장 방문 없이 안전한 업데이트가 가능하므로 새로운 기능 시장 투입까지의 시간이 단축됩니다. 클라우드 대시보드는 사용량이 급증하면서 스포트라이트를 제공하므로 소매업체는 트래픽이 요청할 때만 직원에게 사전 부하를 가할 수 있습니다. 다이볼드 닉스도르프의 DN Vynamic Suite는 23만 개 이상의 엔드포인트를 연결하여 예정되지 않은 다운타임을 줄이는 예보 유지 보수 경고를 푸시합니다. AI 엔진은 가장자리에 배치되며 몇 밀리초 이내에 의심스러운 서랍 패턴에 플래그를 지정하여 즉시 잠금을 지원합니다. 또한 로열티 플랫폼과의 통합을 통해 화면에서 업셀을 사용할 수 있습니다.

서비스는 설치, 철거, 소프트웨어 패치 적용, 컴플라이언스 감사 등 구성 요소 플레이를 마무리합니다. 정기 계약이 확대됨에 따라 서비스 마진은 하드웨어 출하 마진을 능가할 수 있습니다. 내게 필요한 옵션 컨설턴트는 연방 관보에 규정된 촉각, 음성 및 시각 표준의 준수를 보장합니다. ERP 및 POS 데이터를 키오스크 단말기의 원격 측정과 결합하는 기업은 SKU, 이동 및 위치별 매출 증가를 보여주는 폐쇄 루프 분석을 가능하게 합니다. 이 가시성은 셀프 서비스 시장 내 얇은 자본투자주기로 세계에 키오스크를 전개하는 대규모 체인에서의 조달 결정의 중심이 되고 있습니다.

셀프 서비스 시장 보고서는 제품 유형(키오스크, ATM 등), 구성요소(하드웨어, 소프트웨어, 서비스), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 소매, 퀵 서비스 레스토랑 등), 기술(바이오메트릭 대응, NFC/비접촉, AI 구동, 컴퓨터 비전 등), 배치 장소(실내, 실외), 지역별로 분류하고 있습니다.

북미는 2024년 매출액의 39.4%를 차지했는데, 이는 오랜 세월에 걸쳐 현금 자동 예금기 기술의 채용, 폭넓은 소매점에의 전개, 개인정보보호규제의 지지를 반영했습니다. 결제 카드의 보급은 거의 세계적이며 디지털 월렛이 주류이기 때문에 가맹점은 칩, 탭, 모바일 자격 증명을 다루는 기기를 선호합니다. 연방 정부 기관은 광대역 및 디지털 거버먼트 포털에 경기 자극책 예산을 투입하여 공공 서비스의 키오스크 단말기에서 일관된 사용자 경험을 키웁니다. AI, 클라우드, 사이버 보안에 대한 기업의 의욕은 예산 주기마다 높아져 기존 하드웨어 위에 올리는 소프트웨어 중심 업그레이드에 대한 수요가 강해집니다.

유럽은 지속가능성과 포함의 균형을 잡는다. 유럽 위원회는 에코 디자인과 투명한 공급망을 촉구하고 제조업체에게 장기 수명화와 탄소 발자국의 공표를 촉구합니다. 접근성 방법은 촉각 키패드, 음성 프롬프트, 조정 가능한 글꼴 크기를 강제하며, 이는 BOM 및 펌웨어 설계에 영향을 미칩니다. 독일의 EHI 이니셔티브는 수천 개의 셀프 레지 레인을 세는 것으로 상업적 의욕을 보이는 반면,이 지역에서는 키오스크 및 ATM과 원활하게 연결할 수있는 디지털 유로에 대한 최상의 형식을 논의했습니다. 운영자는 원격 원격 측정을 도입하여 서비스 밴의 주행 거리를 줄이고 기후 변화 목표에 부합합니다.

아시아태평양은 CAGR 8.5%로 성장하고 있으며, 디지털화 추진령과 스마트폰 연동 QR 결제의 폭발적 증가의 혜택을 받고 있습니다. 인도에서는 UPI에 의한 송금이 매월 수십억 건 행해져 농촌의 키오스크에서도 QR탭이 상태화하고 있습니다. 중국은 중앙 은행의 디지털 통화를 시험적으로 도입하고 있으며, 이 디지털 통화는 교통 및 자동판매기 네트워크에 통합될 가능성이 높으며, 사업자에게는 펌웨어의 신속한 업데이트가 요구되고 있습니다. ASEAN 각국 정부는 우체국의 전자정부 로비에 자금을 제공하고 원격지 시민들이 동등한 서비스를 받을 수 있도록 하는 동시에 번거로운 절차를 줄이고 있습니다. 남미와 중동은 그 후 먼지를 숭배하고 있지만, 통신사업자가 모바일 머니를 추진하고, 관광업이 다언어 대응의 발권소에 대한 관심을 부활시키면서 가속하고 있습니다.

The self-service market size stood at USD 38.36 billion in 2025 and is forecast to advance to USD 56.22 billion by 2030, reflecting a 7.9% CAGR over the period.

This growth links directly to the shift toward contactless engagement that gathered pace after the pandemic, tighter corporate mandates for digitization, and broad public familiarity with digital wallets. Hardware and software suppliers are responding by embedding AI, computer vision, and biometric modules that cut wait times, strengthen security, and open new use-cases across banking, retail, healthcare, and public venues. Payment ecosystems built on QR and NFC are now mainstream in many urban centers, and they underpin steady demand for self-service terminals able to accept any credential the user prefers. Vendors also highlight service contracts and platform fees, turning what was once a one-off hardware sale into a recurring revenue stream that smooths cash flow. However, resilience against vandalism, outdoor weather extremes, and e-commerce substitution remains a prerequisite for profitable roll-outs.

Global digital payment participation jumped from 44% in 2014 to two-thirds of adults in 2022, confirming a permanent tilt toward cashless behaviors. European research shows sustained intentions to avoid cash because of hygiene concerns, and operators of micro-markets report higher revenues after installing cashless modules. Countries like Sweden, where cash use halved in the past decade, underscore how rapidly policy, merchants, and consumers converge on digital rails. This preference extends to biometric taps and voice prompts, driving every corner of the self-service market to support no-touch authentication.

Autonomous stores relying on RFID gates, computer vision, and smart shelving are projected to grow significantly. Germany counted more than 5,000 self-checkout outlets recently, and retailers plan further acceleration. In the United States, wholesale chains such as Sam's Club deployed AI-enhanced devices that scan carts in seconds, shrinking queues and redeploying staff. Micro-fulfilment hubs, despite integration headaches, promise same-hour replenishment for densely populated districts, creating a pull for lockers and hybrid kiosks able to dispense and accept goods around the clock.

Data from British Telecom revealed tens of thousands of attacks on pay-phones each year until ruggedized locks and alarms curbed incidents. Sophisticated jackpotting and skimming drives a physical and cyber security market forecast to reach USD 32.4 billion by 2032. Operators add fingerprint, facial recognition and multi-factor prompts to counter fraud, yet every new module raises cost per unit and elongates certification cycles. Collaborative patrols with police and AI-driven surveillance mitigate losses but cannot erase them entirely.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Kiosks controlled 36.2% self-service market share in 2024, highlighting their flexibility across check-in, ticketing, and bill payment. The self-service market size tied to kiosks benefits from continuous software refreshes that add language packs, AI avatars, and payment choices. Self-checkout lanes are growing at an 8.3% CAGR as grocers and general merchandisers curb labor expenses and speed the line. ATMs still anchor cash ecosystems, yet annual installations are plateauing because mobile transfers now satisfy many low-value needs. Vending machines move beyond snacks into OTC medicines, PPE, and time-sensitive vaccines, which widens their social footprint. Smart lockers registered brisk orders from logistics firms under pressure to cut last-mile costs and allow after-hours parcel pick-up. Healthcare kiosks, projected to ramp from USD 0.8 billion in 2024 to USD 1.81 billion by 2028, illustrate how diagnosis, telehealth, and prescription renewal can converge in compact footprints. Retailers adopt computer vision so cameras automatically weigh produce, minimizing errors and shopper frustration. The product mix will continue to reward vendors who merge durability with cloud hooks that unlock real-time insights and remote service.

Kiosk suppliers invest in antimicrobial surfaces, haptic feedback, and wheelchair-friendly layouts to stay ahead of accessibility rules. Self-checkout makers partner with fintech gateways to switch on buy-now-pay-later while still conforming to payment security standards. ATM vendors pivot toward Video Teller Machines and cryptocurrency modules to preserve relevance. Vending specialists test dynamic refrigeration and AI planograms to display fast-moving inventory first, which uplifts sales per square inch. Locker providers add temperature control for the grocery and pharmaceutical segments. Portfolio breadth, therefore, remains a hedge against shifts in consumer flow and merchant economics within the self-service market.

Hardware was responsible for 54.0% of revenue in 2024, yet software is advancing 9.0% each year and is the key to lifetime monetization. Vendors deploy containerized operating systems that permit secure updates without field visits, shortening mean-time-to-market for new features. Cloud dashboards spotlight usage spikes, allowing retailers to preload staff only when traffic demands. Diebold Nixdorf's DN Vynamic suite connects more than 230,000 endpoints and pushes predictive maintenance alerts that reduce unscheduled downtime. AI engines sit at the edge, flagging suspicious withdrawal patterns within milliseconds and supporting instant lockouts. Integrations with loyalty platforms also open upsell moments right on the screen.

Services round out the component play, spanning installation, decommissioning, software patching, and compliance audits. As recurring contracts expand, service margins may eclipse those of hardware shipments. Accessibility consultants ensure adherence to tactile, speech, and visual standards laid out in the Federal Register. Firms that couple ERP and point-of-sale data with kiosk telemetry enable closed-loop analytics showing sales uplift by SKU, shift, and location. This visibility is central to procurement decisions at large chains that roll kiosks worldwide on thin capex cycles within the self-service market.

The Self-Service Market Report is Segmented by Product Type (Kiosk, ATM, and More), Component (Hardware, Software, and Services), End-User Industry (BFSI, Retail and Quick-Service Restaurant, and More), Technology (Biometric-Enabled, NFC / Contactless, AI-Driven and Computer-Vision, and More), Deployment Location (Indoor and Outdoor), and Geography.

North America held 39.4% of revenue in 2024, reflecting long-standing adoption of automated teller technology, wide retail deployment, and supportive privacy regulations. Payment card penetration is nearly universal, and digital wallets are mainstream, so merchants prioritize terminals that handle chip, tap, and mobile credentials. Federal agencies devote stimulus budgets to broadband and digital government portals, fostering a consistent user experience in public service kiosks. Corporate appetite for AI, cloud, and cybersecurity rises each budget cycle, reinforcing demand for software-centric upgrades that sit atop existing hardware.

Europe balances sustainability and inclusion. The European Commission urges eco-design and transparent supply chains, pushing manufacturers to lengthen device lifespans and publish carbon footprints. Accessibility law compels tactile keypads, audio prompts, and adjustable font sizes, which influence BOM and firmware design. Germany's EHI initiative demonstrates commercial appetite by counting thousands of self-checkout lanes, while the region debates best formats for a digital euro that could seamlessly link to kiosks and ATMs. Operators retrofit remote telemetry to trim service van miles, aligning with climate targets.

Asia-Pacific, advancing at an 8.5% CAGR, benefits from pro-digitization edicts and an explosion of smartphone-linked QR payments. India stages billions of UPI transfers each month, normalizing QR taps even in rural kiosks. China pilots a central bank digital currency that will likely integrate into transit and vending networks, placing pressure on operators to update firmware fast. Governments in ASEAN fund e-government lobbies inside post offices, reducing red tape while ensuring remote citizens receive equal service. South America and the Middle East trail but accelerate as telcos push mobile money and as tourism revives interest in multi-language ticketing stations.