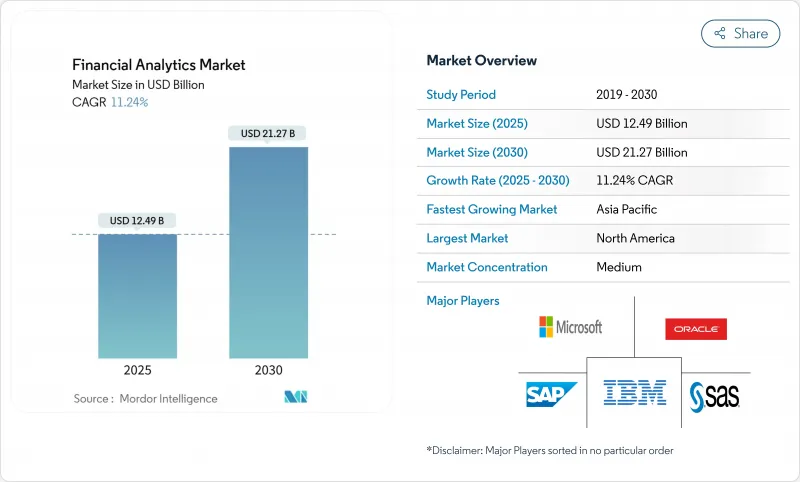

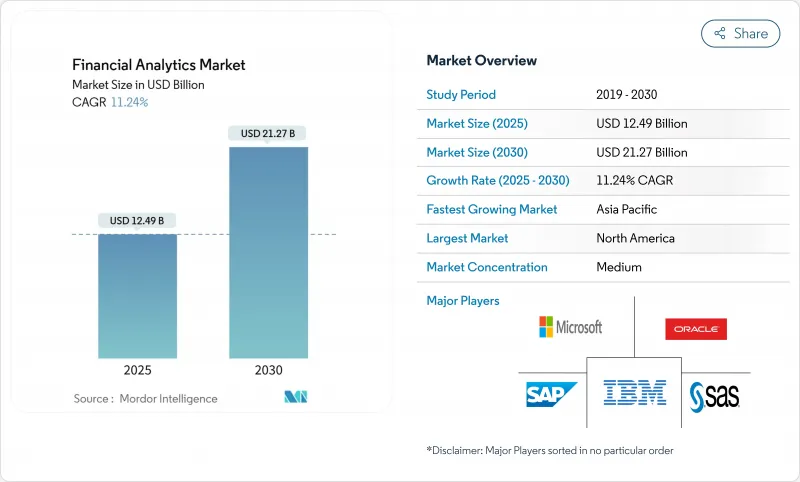

재무 분석 시장의 2025년 시장 규모는 현재 124억 9,000만 달러로 평가되었고, 2030년에 212억 7,000만 달러로 확대될 것으로 예측됩니다.

신속한 클라우드 네이티브 핵심 시스템 전환, 실시간 위험 관리 요구사항, AI 기반 의사결정 시스템이 은행, 보험, 기업 금융 부서 전반에 걸쳐 도입을 촉진하고 있습니다. 북미 기관들은 성숙한 데이터 자산을 지속적으로 최적화하는 한편, 아시아태평양 지역 은행들은 레거시 시스템에서 나노초 단위 거래 인사이트를 제공하는 클라우드 스택으로 도약하고 있습니다. 위험 회피 성향이 강한 1급 은행들 사이에서는 온프레미스 전개가 여전히 주류를 이루고 있으나, CIO들이 자본 지출을 운영 비용 지불 모델에 맞추면서 가속화되는 클라우드 마이그레이션이 벤더 전략을 재편하고 있습니다. 사이버 복원력 요구사항 강화, 수백만 달러 규모의 침해 노출 위험, 데이터 과학자 부족이 도입 속도를 저해하고 있으나, 내장형 AI에 대한 대규모 투자가 총소유비용을 낮추고 재무 분석 시장을 중소기업에 개방하고 있습니다.

모놀리식 코어에서 클라우드 네이티브 아키텍처로 이전한 금융 기관들은 첫해에 운영 효율성 45% 향상과 최대 40%의 비용 절감을 기록했습니다. 이 전환은 유지보수에 소모되던 예산을 확보하고, 실시간으로 분석 엔진에 데이터를 스트리밍하는 마이크로서비스를 가능하게 합니다. 북미 1급 은행들은 하이브리드 전략을 실행 중인 반면, 인도와 인도네시아의 중견 대출 기관들은 공용 클라우드 코어로 직접 도약하고 있습니다. 공급업체 로드맵은 이제 일중 거래량에 따라 탄력적으로 확장되는 컨테이너화된 분석 모듈에 집중하고 있습니다. 규제 당국은 클라우드 그리드가 더 빠른 재해 복구와 거의 제로에 가까운 다운타임을 가능하게 함으로써 복원력 이점을 인정하고 있습니다. 이러한 추세는 재무 분석 시장의 잠재적 수요를 크게 확대합니다.

AI 엔진을 재무, 대출, 포트폴리오 관리 도구에 내장함으로써 별도의 데이터 과학 스택 구축이 불필요해집니다. AI 기반 플랫폼을 도입한 기관들은 자동화된 대조, 초정밀 현금 예측, 오경보 감소로 연간 평균 190만 달러를 절감합니다. 현대식 제품군은 ERP 및 CRM 파이프라인에서 데이터를 추출하는 예측 모델이 사전 구성되어 있어 심층 분석 인력이 부족한 지역 은행의 구현 주기를 단축합니다. AI 기반 운전 자본 최적화 같은 애플리케이션은 예측 오류를 50% 감소시켜 수익 창출 상품으로 재투입 가능한 유동성을 확보합니다. 이로 인한 총소유비용(TCO) 절감은 비용 민감 부문으로의 재무 분석 시장 침투를 가속화합니다.

은행들은 침해 사고당 평균 608만 달러의 손실을 입으며, 이는 전 산업 평균보다 약 25% 높은 수치입니다. 공격 지속 시간은 종종 5개월을 초과하여 자격 증명 및 고객 기록 도난을 가중시킵니다. 2024년 미국 주요 건강보험사를 대상으로 한 랜섬웨어 공격은 단일 침해로 2,200만 달러의 지불금이 발생할 수 있음을 보여주었습니다. 이사회는 이제 분석 업그레이드에서 보안 강화로 자본을 전환하여 리프레시 주기를 늦추고 있습니다. 사이버 보험료도 두 자릿수 상승하며 IT 예산을 더욱 압박하고 있습니다. 따라서 공급업체들은 구매자의 우려를 해소하고 재무 분석 시장의 성장을 지속하기 위해 분석 플랫폼 내부에 제로 트러스트 통제 기능을 내장해야 합니다.

2024년 온프레미스 환경은 재무 분석 시장 점유율의 61.2%를 유지하며, 데이터 거주지 및 지연 시간 관리에 대한 업계의 신중한 입장을 반영했습니다. 그러나 공공 및 사설 클라우드 전개는 연평균 13.2% 성장률로 확대되며, 규제 기관이 공동 책임 프레임워크를 공식화함에 따라 격차가 좁혀질 전망입니다. 금융 기관들은 예산 모의실험 환경과 같은 비핵심 애플리케이션부터 단계적 이전을 검토한 후 실시간 위험 엔진을 이전할 계획입니다. 공급업체들이 현지 규정 준수를 위해 주권 클라우드 지역을 구축함에 따라 클라우드 플랫폼에 기인한 재무 분석 시장 규모는 크게 증가할 것으로 전망됩니다. 은행들은 또한 비용이나 지연 시간에 따라 워크로드를 온프레미스 및 클라우드 노드 간에 전환할 수 있는 컨테이너 오케스트레이션을 도입하고 있습니다. 데이터 유출 수수료와 벤더 종속성에 대한 우려는 여전히 존재하지만, 멀티클라우드 연결 도구와 이동 가능한 라이선싱은 이러한 제약을 완화하고 더 광범위한 클라우드 채택을 촉진하는 데 도움이 됩니다.

워크로드가 전환되면 운영 모델도 변화합니다. 사이트 신뢰성 엔지니어(SRE)가 하드웨어 팀을 대체하고, 사용량 기반 가격 책정이 IT 지출을 거래량과 연계시킵니다. 중소 금융기관들은 종량제 모델을 활용해 글로벌 은행에만 제한되었던 머신러닝 라이브러리에 접근합니다. 클라우드 플랫폼은 테넌트 간 네트워크 트래픽을 모니터링하는 위협 분석 기능을 통합해 사이버 복원력을 강화합니다. 확장 가능한 컴퓨팅은 대규모 고정 투자 없이 포트폴리오 위험를 위한 몬테카를로 시뮬레이션을 가능케 합니다. 이로 인한 민첩성은 여전히 메인프레임에 의존하는 기존 기업들에 추가 압박을 가하며, 클라우드 기반 재무 분석 시장 솔루션으로의 예산 재배분을 가속화합니다.

분석 및 보고 제품군이 2024년 시장 점유율 33.6%로 선두를 달렸는데, 재무팀이 더 빠른 결산 주기를 위해 통합 대시보드를 요구했기 때문입니다. 다중 법인 기업이 복잡한 IFRS 및 GAAP 의무를 충족하기 위해 단일 진실 원본 장부를 필요로 함에 따라 재무 통합 제품군은 12.7%의 연평균 성장률(CAGR)을 보입니다. 이러한 모듈은 통화 변환 및 계열사 간 제거를 자동화하여 수기 분개 입력을 70% 줄입니다. 공급업체들은 그룹 결산 과정에서 이상 변동을 감지하고 시정 조치를 권고하는 AI를 내장하여 보고 일정을 며칠 단축합니다. 기후 및 세금 투명성에 대한 규제 기관의 공시 요구가 강화됨에 따라 통합과 관련된 재무 분석 시장 규모는 크게 확대될 전망입니다.

데이터베이스 관리 및 계획 도구는 분석 엔진이 실행되는 기반을 형성하는 반면, 위험 및 규정 준수 모듈은 시나리오 모델링을 규제 분류 체계와 통합합니다. ESG 점수 분석 및 양자 준비형 파생상품 플랫폼은 신흥 ‘기타 솔루션’ 영역을 차지합니다. 기업들이 종단간 재무 변혁을 추구함에 따라 공급업체들은 계정 조정 및 공시 관리와 같은 인접 기능을 대규모 플랫폼에 통합합니다. 이러한 융합 추세는 공급업체들이 풀스택 커버리지를 제공하기 위해 경쟁하면서 인수합병을 촉진하고, 재무 분석 시장 내 경쟁을 가속화합니다.

재무 분석 시장 보고서는 분석 시장 보고서는 전개 유형(온프레미스 및 클라우드), 솔루션 유형(데이터베이스 관리 및 계획, 분석 및 보고 등), 적용 분야(위험 관리, 예산 및 예측 등), 분석 유형(기술적 분석 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(금융·보험·증권, 헬스케어 등), 지역별로 분류됩니다.

2024년 북미 지역은 38.7%의 매출 점유율로 선두를 차지했습니다. 자본력이 풍부한 은행들이 AI 핵심 기술, 클라우드 복원력, 통합 규정 준수 워크벤치에 조기 투자했기 때문입니다. 미국 규제 당국은 모델 위험 관리에 대한 명확한 지침을 제공하여 기관들이 잘 정의된 가이드레일 내에서 실험할 수 있도록 합니다. 캐나다 은행들은 풍부한 거래 데이터를 제3자 분석 레이어로 스트리밍하는 오픈뱅킹 API를 선도적으로 도입했습니다. 뉴욕과 토론토의 자본 시장 기업들은 파생상품을 마이크로초 단위로 가격 책정하는 저지연 그리드를 구축했습니다. 하이퍼스케일 클라우드 지역의 존재는 데이터 주권 마찰을 줄여 해당 지역 전반에 걸쳐 재무 분석 시장의 우위를 유지합니다.

아시아태평양 지역은 적극적인 디지털화, 지원 정책, 금융 서비스에 대한 중산층 수요 확대로 2030년까지 연평균 12.5% 성장률을 기록할 전망입니다. 중국 대형 은행들은 수십억 달러 규모의 클라우드 예산을 투입하는 한편, 인도 국영 은행들은 신용 평가를 위한 신규 데이터 세트를 확보하는 계좌 통합 네트워크에 참여합니다. 일본 금융 대기업들은 금리 변동성 완화를 위해 양자 컴퓨팅 컨소시엄을 모색 중입니다. 동남아시아 핀테크 기업들은 은행 계좌가 없는 계층의 신용 접근성을 확대하며 실시간 분석 워크로드를 엣지로 이동시키고 있습니다. 지역 AI 지출은 2028년까지 1,100억 달러에 달할 것으로 전망되어 장기적 성장 동력을 강화할 전망입니다.

유럽은 선진적인 ESG 보고 기준과 정교한 도매 시장으로 상당한 영향력을 유지합니다. 프랑스 은행들은 탄소 회계를 신용 모델에 통합하고, 독일 보험사들은 기후 위험을 반영하는 보험 수리 엔진을 도입합니다. EU 데이터법은 개인정보 보호 준수를 강화하여 보안 엔클레이브 같은 프라이버시 보호 분석 기술의 광범위한 채택을 촉진합니다. 한편 유럽중앙은행이 결제 시스템을 보호하기 위해 양자 암호화 이후 기술을 탐색한 이후 양자 대비가 주목받기 시작했습니다. 남미, 중동, 아프리카는 현재 비중은 작지만 모바일 머니, 디지털 ID, 오픈 뱅킹 이니셔티브가 성숙함에 따라 두 자릿수 성장을 기록하고 있습니다.

The financial analytics market is currently valued at USD 12.49 billion in 2025 and is forecast to rise to USD 21.27 billion by 2030, reflecting an 11.2% CAGR during the period.

Rapid cloud-native core conversions, real-time risk mandates, and AI-enabled decision systems are pushing adoption across banking, insurance, and corporate finance teams. North American institutions continue to optimize mature data estates, while Asia-Pacific banks leap from legacy systems to cloud stacks that deliver nanosecond transaction insights. On-premise deployments remain prevalent among risk-averse tier-1 banks, yet accelerating cloud migrations are reshaping vendor strategies as CIOs align capital outlays with operational pay-as-you-go models. Intensifying cyber resiliency requirements, multimillion-dollar breach exposures, and a shortage of data scientists are restraining the pace, but heavy investment in embedded AI is lowering the total cost of ownership and opening the financial analytics market to small and midsize enterprises.

Financial institutions that migrate from monolithic cores to cloud-native architectures record 45% jumps in operational efficiency and up to 40% cost savings within the first year. The shift frees budgets historically consumed by maintenance and enables microservices that stream data into analytics engines in real time. North American tier-1 banks are executing hybrid moves, while mid-tier lenders in India and Indonesia leap directly to public cloud cores. Vendor roadmaps now center on containerized analytics modules that scale elastically with intraday transaction volumes. Regulators acknowledge the resilience benefit because cloud grids allow faster disaster recovery and near-zero downtime. This momentum greatly enlarges addressable demand in the financial analytics market.

Embedding AI engines inside treasury, lending, and portfolio tools removes the need for separate data science stacks. Institutions deploying AI-infused platforms save an average of USD 1.9 million annually through automated reconciliations, hyper-accurate cash forecasts, and fewer false-positive alerts. Modern suites come pre-configured with predictive models that pull data from ERP and CRM pipes, shrinking implementation cycles for regional banks lacking deep analytics talent. Applications such as AI-guided working capital optimization reduce forecast errors by 50%, unlocking liquidity that can be redeployed into revenue-generating products. The resulting lower total cost of ownership accelerates penetration of the financial analytics market into cost-sensitive segments.

Banks average USD 6.08 million in loss per breach, nearly 25% above cross-sector norms. Attack dwell time often exceeds five months, amplifying theft of credentials and customer records. The 2024 ransomware strike on a leading U.S. health insurer showed how a single breach can trigger USD 22 million in payouts. Boards now divert capital from analytics upgrades to security hardening, slowing refresh cycles. Cyber insurance premiums also rise by double digits, squeezing IT budgets further. Vendors must therefore embed zero-trust controls inside analytics platforms to assuage buyer concerns and sustain growth in the financial analytics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

On-premise setups retained 61.2% of the financial analytics market share in 2024, underscoring the sector's cautious stance on data residency and latency control. However, public and private cloud deployments are advancing at 13.2% CAGR and will narrow the gap as regulators formalize shared-responsibility frameworks. Institutions weigh staged migrations beginning with non-core applications, such as budgeting sandboxes, before moving real-time risk engines. The financial analytics market size attributed to cloud platforms is forecast to climb markedly as vendors build sovereign cloud regions to satisfy local compliance. Banks also adopt container orchestration that allows workloads to swing between on-premise and cloud nodes based on cost or latency. Although data-egress fees and vendor lock-in fears linger, multicloud connectivity tools and portable licensing help alleviate these restraints and propel broader cloud adoption.

Once workloads shift, operating models change. Site-reliability engineers replace hardware teams, and consumption pricing aligns IT spend with transaction volumes. Smaller lenders exploit the pay-as-you-go model to access machine-learning libraries previously limited to global banks. Cloud platforms integrate threat analytics that monitor network traffic across tenants, strengthening cyber resilience. Scalable compute further enables Monte Carlo simulations for portfolio risk without large fixed investments. The resulting agility places added pressure on incumbents still anchored to mainframes, encouraging an accelerated reallocation of budgets toward cloud-based financial analytics market solutions.

Analysis and reporting suites led the 2024 landscape with 33.6% revenue share as finance teams demanded unified dashboards for faster close cycles. Financial consolidation suites exhibit 12.7% CAGR because multi-entity corporations require single-version-of-truth ledgers to meet complex IFRS and GAAP obligations. These modules automate currency translation and intercompany eliminations, reducing manual journal entries by 70%. Vendors embed AI that flags anomalous variances during group close and recommends corrective actions, shaving days off reporting timelines. The financial analytics market size associated with consolidation is projected to expand significantly as regulators intensify disclosure demands for climate and tax transparency.

Database management and planning tools form the substrate on which analytical engines run, while risk and compliance modules integrate scenario modeling with regulatory taxonomy. ESG-score analytics and quantum-ready derivatives platforms occupy the emerging "other solutions" niche. As corporations seek end-to-end financial transformation, vendors bundle adjacent capabilities such as account reconciliation and disclosure management into larger platforms. The convergence trend fuels mergers and acquisitions as providers race to offer full-stack coverage, amplifying competition within the financial analytics market.

The Financial Analytics Market Report is Segmented by Deployment Mode (On-Premise and Cloud), Solution Type (Database Management and Planning, Analysis and Reporting, and More), Application (Risk Management, Budgeting and Forecasting, and More), Analytics Type (Descriptive Analytics, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare, and More), and Geography.

North America led with 38.7% revenue share in 2024 as well-capitalized banks invested early in AI cores, cloud resilience, and integrated compliance workbenches. U.S. regulators provide clear guidance on model risk management, allowing institutions to experiment within well-defined guardrails. Canadian banks pioneer open-banking APIs that stream enriched transaction data into third-party analytics layers. Capital markets firms in New York and Toronto deploy low-latency grids that price derivatives in microseconds. The presence of hyperscale cloud regions reduces data-sovereignty friction, sustaining dominance of the financial analytics market across the region.

Asia-Pacific is expected to post a 12.5% CAGR through 2030 on the back of aggressive digitization, supportive policy, and expanding middle-class demand for financial services. China's megabanks commit multi-billion-dollar cloud budgets, while India's public-sector banks join account-aggregator networks that unleash new data sets for credit scoring. Japan's financial giants explore quantum computing consortiums to mitigate interest-rate volatility. Southeast Asian fintechs unlock credit access for the unbanked, pushing real-time analytics workloads to the edge. Regional AI spend is forecast to hit USD 110 billion by 2028, reinforcing long-term momentum.

Europe maintains a sizeable footprint with advanced ESG reporting norms and sophisticated wholesale markets. French banks integrate carbon accounting into credit models, while German insurers deploy actuarial engines that factor climate risk. The EU Data Act elevates privacy compliance, prompting wider adoption of privacy-preserving analytics such as secure enclaves. Meanwhile, quantum readiness gains traction after the European Central Bank explored post-quantum cryptography to safeguard payment rails. South America, and Middle East, and Africa contribute smaller shares today but register double-digit growth as mobile money, digital ID, and open banking initiatives mature.