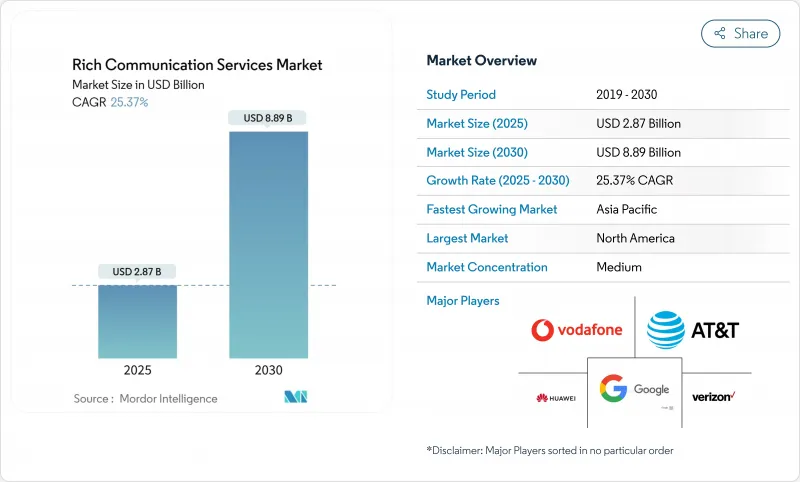

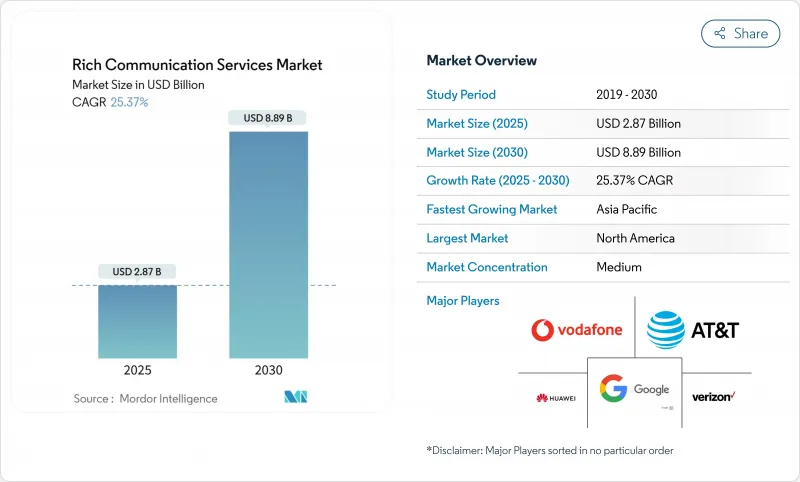

리치 커뮤니케이션 서비스(RCS) 시장은 2025년에 28억 7,000만 달러에 이르고, CAGR 25.37%를 나타내 2030년에는 88억 9,000만 달러로 성장할 것으로 예측되고 있습니다.

미디어 풍부하고 브랜드화된 고객 참여에 대한 기업의 의욕이 높아짐에 따라 기업은 단순한 SMS에서 이미지, 동영상, 액션 가능한 버튼에 대응하는 인터랙티브 메시징으로 전환하고 있습니다. 통신 사업자 지원 확대, iOS 18에 RCS 탑재, 구글에 의한 미국에서의 RCS 메시지의 하루에 10억 건 이상이라는 보고는 주류 채용의 전환점을 뒷받침하고 있습니다. 대기업이 주요 수익원이 되는 것은 아니지만, 클라우드 네이티브 CPaaS 플랫폼은 중소기업의 진입 장벽을 낮추고 있습니다. 아시아태평양의 통신 사업자가 5G 네트워크를 사용하여 리치 미디어 트래픽을 지원하기 때문에 아시아태평양의 기세는 가장 강하고 북미는 수년간 통신 사업자의 상호 운용성을 배경으로 선도하고 있습니다. 발신자 ID 인증을 향한 규제의 움직임은 고객과의 접촉에 안전하고 인증된 채널을 필요로 하는 기업에게 더욱 견인 역할을 하고 있습니다.

A2P 캠페인은 기존 SMS보다 전환율과 클릭연결율이 현저히 높으며 은행과 소매 브랜드는 이 채널에 상당한 지출을 옮겼습니다. 멀티미디어 카드와 답장 제안을 통해 마케팅 담당자는 단일 대화 대화 내에서 구매자를 인지에서 구매로 이끌 수 있으며 기본 텍스트 푸시의 6.2배 ROI를 창출합니다. CPaaS 공급업체는 로우코드 템플릿, 컴플라이언스 워크플로우, 이메일 및 앱 푸시 프로그램에 대한 리프트를 정량화하는 실시간 분석을 통합하여 대응합니다. 세계 은행과 같은 조기 채용 기업은 개인화된 대출 셀 채팅에서 10% 전환을 보고하여 수익 향상을 확인하고 있습니다. 보다 많은 기업들이 이 효과를 목격하고 있으며, A2P의 이용은 예측기간 동안 리치 커뮤니케이션 서비스(RCS) 시장 전체의 확대를 뒷받침할 것으로 보입니다.

애플이 iOS 18에 RCS를 통합하기로 결정함으로써 트래픽을 OTT 앱으로 유도했던 역사적인 상호 운용성의 격차가 없어져 약 9억 대의 활성 iPhone이 사업자 등급의 리치 메시징을 통해 즉시 액세스할 수 있습니다. 삼성이 Galaxy 단말기에 Messages by Google을 디폴트로 채용한 것으로 세계 리치는 더욱 확대했습니다. 통합된 경험을 통해 픽셀화된 이미지, 중단된 그룹 채팅, 그린/블루 채팅의 단편화 등을 해소해 소비자의 의욕을 돋웁니다. 기업은 병렬 OTT 채널을 유지하지 않고 더 많은 주소 지정 가능한 잠재고객의 잠금을 해제하고 운영 체제 전체에서 예측 가능한 도달범위를 얻습니다. 이 네트워크 효과는 애플의 롤아웃 이후 25% 높은 참여를 기록한 테스트 캠페인에서 이미 확인되었습니다.

GSMA Universal Profile 3.0을 준수하는 통신사업자는 57개사에 머물며 국경을 넘어선 경험을 저하시키는 격차를 낳고 있습니다. 여러 지역에 캠페인을 발신하는 기업은 여분의 SMS와 OTT 채널을 유지해야 하며 비용과 운영의 복잡성을 높이고 있습니다. Google의 Jibe나 GSMA의 Interconnect 프로젝트 등의 허브는 라우팅의 합리화를 의도하고 있는 것, 구현에 편차가 있기 때문에 규모가 축소해 버립니다. 다국적 기업은 고가의 트래픽을 마이그레이션하기 전에 일관된 SLA를 계속 요구하고 있으며 RCS를 위한 수익 재구성을 늦추고 있습니다.

A2P 트래픽은 2024년 수익의 61.8%를 차지하며 리치 커뮤니케이션 서비스(RCS) 시장의 핵심을 이루었습니다. 은행, 소매업체 및 항공사는 멀티미디어 카드와 빠른 회신을 사용하여 일상적인 알림을 매출 증가를 촉진하는 대화 터치 포인트로 변환합니다. AI 채팅봇이 성숙하고 소비자가 스레드 내에서 트랜잭션을 완료하는 것에 쾌감을 느끼게 되면서 개인 대 용도의 대화는 현재는 작은 것, 매년 31.5% 확대되고 있습니다. 이러한 증가로 인해 P2A 흐름의 리치 커뮤니케이션 서비스(RCS) 시장 규모는 2030년까지 2자리 속도로 확대될 것으로 예측됩니다.

기업은 로열티 프로모션을 SMS에서 RCS로 전환할 때 전환이 8-10포인트 상승한 것을 기록하고 있습니다. 인도 사례 연구는 CPaaS 제공업체인 Gupshup이 Vertex AI 채팅봇을 통합한 후 트래픽이 358% 급증한 것으로 나타났습니다. iOS와 안드로이드의 원활한 상호 연결이 가능한 시장에서는 개인간의 이용도 증가하고 있지만, 수익화는 기업 주도가 아니라 사업자 주도로 이루어지고 있습니다. 게임 및 티켓팅과 같은 참여도가 높은 섹터는 취소 대기 및 인증을 관리하기 위해 P2A 흐름에 의존하며, 커뮤니케이션 유형 계층 내에서 믹스가 진화하고 있음을 보여줍니다.

클라우드 호스팅 플랫폼은 2024년 매출의 72.9%를 차지하며 설비 투자가 부피가 큰 On-Premise 메시징 게이트웨이를 제거하려는 보다 광범위한 기업의 움직임을 반영했습니다. 퍼블릭 클라우드 RCS는 REST API를 통해 기존 CRM, CDP, 마케팅 자동화 스택과 연계할 수 있기 때문에 다국적 브랜드가 선호하고 이용하고 있습니다.

On-Premise 환경은 방어, 건강 관리, 정부 기관 등 데이터 거주에 관한 법률로 지역 처리가 의무화되고 있는 분야에서는 여전히 자명하지 않습니다. 이러한 환경에서 민감한 컨텐츠는 방화벽 내부에서 렌더링되며, 세계 도달범위는 퍼블릭 클라우드 상호 연결을 활용하는 하이브리드 아키텍처를 사용합니다. Twilio의 공개 베타는 SDK 뒤에 있는 경력의 복잡성을 추상화하고 개발자가 한 대시보드에서 SMS, WhatsApp, 이메일과 함께 RCS를 시작할 수 있도록 하는 공급업체의 푸시를 강조합니다.

리치 커뮤니케이션 서비스(RCS) 시장은 통신 유형별(A2P(Application-to-Person), P2P(Person-to-Person), 기타), 배포 모드별(클라우드, On-Premise), 최종 사용자 기업 규모별(대기업, 중소기업), 최종 사용자 업계별(은행, 금융서비스 및 보험(BFSI), 미디어 엔터테인먼트, 기타), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 Verizon, ATandT, T-Mobile에서 유니버설 프로파일의 조기 도입에 힘입어 2024년 매출의 38.5%를 차지했습니다. Google이 미국에서 하루 10억 건 이상의 RCS 메시지를 게시한 것은 소비자 섭취가 성숙한 것으로 나타났습니다. FCC는 현재 911 긴급 메일에 RCS를 인정하고 있으며, 시정촌과 기업이 인증 채널을 채택하는 것을 뒷받침하고 있습니다. 이 지역은 ARPU가 높기 때문에 통신 사업자는 비즈니스 메시징 요금을 통해 증수를 얻을 수 있습니다.

아시아태평양은 CAGR 30.4%로 가장 급성장하고 있는 지역으로, 스마트폰의 초고 보급과 정부의 디지털화 프로그램이 자극되고 있습니다. 인도는 단일 CPAaS 플랫폼에서 매월 5천만 건의 기업용 메시지를 기록하고 있으며, 2027년까지 트래픽량으로 북미를 추월할 것으로 예측됩니다. 일본과 한국에서는 RCS 유저 비율이 플러스 70%로 성장을 지속하고, 있어 5G의 밀도가 리치 미디어의 채용과 어떻게 상관하고 있는지를 증명하고 있습니다. 통신 사업자의 상황은 단편화하고 있는 것, GSMA Interconnect Hub와 같은 이니셔티브가 국경을 넘은 라우팅의 합리화를 목표로 하고 있어, 이 지역의 리치 커뮤니케이션 서비스(RCS) 시장을 더욱 뒷받침하고 있습니다.

유럽에서는 데이터 보호 규정과 디지털 시장법 간의 상호 운용성 규칙이 비규제 OTT 앱보다 검증된 운영자 관리 메시징에 유리하기 때문에 꾸준히 확대되고 있습니다. 독일 텔레콤의 2024년 매출액 1,158억 유로에는 RCS 대응 부가가치 서비스의 매출이 포함되었습니다. 반대로, Apple의 암호화 RCS에 대한 합법적인터셉션을 둘러싼 영국의 논의는 규제 불확실성이 도입을 일시적으로 억제할 수 있음을 보여줍니다. 라틴아메리카는 아직 초기 단계에 있지만, 특히 브라질에서는 대화형 상거래의 사용이 매우 많아, 일류 통신 사업자가 2024년 중에 최초의 대규모 캠페인을 실시했습니다.

The rich communication services market reached USD 2.87 billion in 2025 and is projected to grow to USD 8.89 billion by 2030, reflecting a 25.37% CAGR.

Growing enterprise appetite for media-rich, branded customer engagement is pushing businesses to migrate from plain SMS to interactive messaging that supports images, video, and actionable buttons. Expanded carrier support, the inclusion of RCS in iOS 18, and Google's report of more than 1 billion U.S. RCS messages per day underscore a tipping point in mainstream adoption. Large enterprises remain the principal revenue source, yet cloud-native CPaaS platforms are lowering entry barriers for small and medium businesses. Geographic momentum is strongest in Asia-Pacific as regional operators use 5G networks to support rich media traffic, while North America holds its lead on the back of long-standing carrier interoperability. Regulatory moves toward verified sender IDs are creating additional pull for enterprises that need secure, authenticated channels for customer contact.

A2P campaigns deliver markedly higher conversion and click-through rates than legacy SMS, encouraging brands in banking and retail to shift considerable spend to the channel. Multi-media cards and suggested replies let marketers guide shoppers from awareness to purchase within a single threaded conversation, generating 6.2 times the ROI of basic text pushes. CPaaS vendors have responded by embedding low-code templates, compliance workflows, and real-time analytics that quantify lift against email and app-push programs. Early adopters such as global banks report 10% conversion from personalized loan-upsell chats, validating the revenue upside. As more enterprises witness the impact, A2P usage is set to underpin overall rich communication services market expansion during the forecast window.

Apple's decision to embed RCS in iOS 18 removes the historic interoperability gap that steered traffic to OTT apps; nearly 900 million active iPhones instantly become reachable via operator-grade rich messaging. Samsung's default adoption of Messages by Google on Galaxy devices further amplifies global reach. The unified experience eliminates pixelated images, broken group chats, and green/blue chat fragmentation that deterred consumers. Enterprises gain predictable reach across operating systems, unlocking larger addressable audiences without maintaining parallel OTT channels. This network effect is already visible in pilot campaigns that recorded 25% higher engagement after Apple rollout.

Only 57 carriers have aligned with GSMA Universal Profile 3.0, creating gaps that degrade cross-border experience. Enterprises sending campaigns into multiple regions must maintain fallback SMS or OTT channels, raising cost and operational complexity. While hubs such as Google's Jibe and GSMA's Interconnect projects are intended to streamline routing, uneven implementation throttles scale. Multinationals continue to lobby for consistent SLAs before migrating high-value traffic, delaying revenue realignment toward RCS.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

A2P traffic delivered 61.8% of 2024 revenue, making it the backbone of the rich communication services market. Banks, retailers, and airlines use multimedia cards and quick replies to convert routine notifications into conversational touchpoints that drive incremental sales. Person-to-Application conversations, though currently smaller, are expanding 31.5% annually as AI chatbots mature and consumers grow comfortable completing transactions inside a thread. This uptick will increase the rich communication services market size for P2A flows at a double-digit clip through 2030.

Enterprises are documenting conversion jumps of 8-10 percentage points when migrating loyalty promotions from SMS to RCS. Case studies in India show a 358% traffic surge for CPaaS provider Gupshup after integrating Vertex AI chatbots. Person-to-Person usage also climbs in markets with seamless iOS-Android interconnect, though monetization is operator-driven rather than enterprise-driven. High-engagement sectors such as gaming and ticketing rely on P2A flows to manage waitlists and authentication, signaling an evolving mix within the communication-type hierarchy.

Cloud-hosted platforms generated 72.9% of 2024 revenue, mirroring broader enterprise moves to eliminate cap-ex-heavy, on-premise messaging gateways. Multinational brands favor public-cloud RCS because it dovetails with existing CRM, CDP, and marketing-automation stacks via REST APIs.

On-premise environments remain non-trivial in sectors such as defense, healthcare, and government where data-residency laws require local processing. Those deployments stand to benefit from hybrid architectures in which sensitive content is rendered behind the firewall while global reach rides public-cloud interconnects. Twilio's public beta underscores the vendor push to abstract carrier complexity behind SDKs, letting developers spin up RCS alongside SMS, WhatsApp, and email within one dashboard.

Rich Communication Services Market is Segmented by Communication Type (A2P (Application-To-Person), P2P (Person-To-Person), and More), Deployment Mode (Cloud and On-Premise), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Media and Entertainment and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 38.5% of 2024 revenue, underpinned by early universal profile adoption across Verizon, ATandT, and T-Mobile. Google's disclosure of more than 1 billion daily RCS messages in the U.S. illustrates mature consumer uptake. Regulatory clarity also helps: the FCC now recognizes RCS for emergency 911 texts, encouraging municipalities and enterprises alike to adopt authenticated channel. The region's high ARPU lets carriers capture incremental revenue through business messaging fees.

Asia-Pacific is the fastest-growing geography at a 30.4% CAGR, stimulated by ultra-high smartphone penetration and government digitization programs. India records 50 million monthly enterprise messages on a single CPaaS platform and is projected to eclipse North America in traffic volume by 2027. Japan and South Korea exhibit plus-70% RCS user ratios, proving how 5G density correlates with rich-media adoption. Despite fragmented operator landscapes, initiatives such as the GSMA Interconnect Hub aim to streamline cross-border routing, further boosting the rich communication services market in the region.

Europe posts steady expansion as data-protection regulations and Digital Markets Act interoperability rules favor verified, operator-controlled messaging over unregulated OTT apps. Deutsche Telekom's EUR 115.8 billion 2024 revenue includes a growing slice from RCS-enabled value-added services. Conversely, the UK debate over lawful interception vis-a-vis Apple's encrypted RCS shows that regulatory uncertainty can temporarily dampen deployment, yet enterprises continue pilot projects to gauge engagement lift. Latin America remains early-stage but is notable for outsized conversational commerce usage, especially in Brazil where tier-one carriers completed their first large-scale campaigns during 2024.