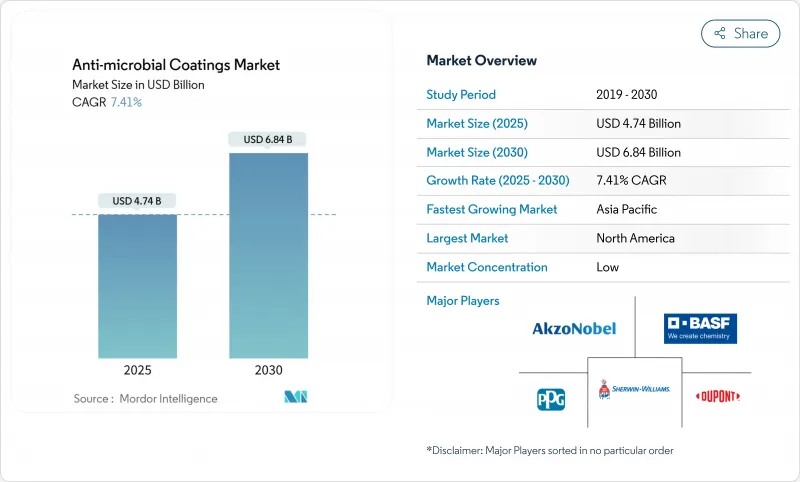

항균 코팅 시장 규모는 2025년에 47억 4,000만 달러로 추정되고, 2030년에는 68억 4,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 7.41%를 나타낼 전망입니다. 병원의 감염 관리 기준 강화, 콜드체인 물류 성장, 휘발성 유기 화합물 규제 강화가 장기 수요를 강화하고 있습니다.

은계 제제는 2024년 매출의 49%를 차지하고 우위를 유지했지만, 수계 유기 화합물은 구매자가 환경에 미치는 영향이 낮기 때문에 CAGR 9.67%를 나타낼 전망입니다. 북미는 엄격한 원내감염(HAI) 프로토콜에 힘입어 최대 지역 수요를 차지했지만, 아시아태평양은 광범위한 산업기반과 제조능력 확대를 배경으로 가장 급속히 진전하고 있습니다. 경쟁의 심각성의 중심은 가격보다는 기능적 혁신, 나노구조 활성제, 비침출성 바인더, 복합재료 및 엔지니어링 폴리머에 부착할 수 있는 멀티 프로퍼티 시스템에 있습니다. 소규모 전문 기업은 터치 인터페이스 전자기기, 냉장 물류, 고위생 건축자재에 맞는 솔루션을 제공함으로써 견인력을 늘리고 있습니다.

병원 관리자는 집중 치료실의 표면 처리로 풀 HAI가 36% 감소하고 세균량이 75-79% 감소했다는 임상 연구의 기록을 받아 표면 처리를 도입하고 있습니다. 항균 페인트는 표준 코팅보다 20-50% 높지만, 회복 시간 단축과 재입원률 저하로 인해 그 고감은 정당화됩니다. 투명한 탑코트는 미관을 바꾸지 않고 개조가 가능하며, 나노화된 유형은 정기적인 청소 도중에도 효과를 지속합니다.

온도 관리 창고가 확대되고 최종 사용자는 저온에서 균일하게 경화하고 냉장 장치의 마모를 견디는 분말 시스템을 선호합니다. ASEAN의 식품 안전 규칙이 통일되고 항균 사양이 표준화되고 있기 때문에 컨베이어 프레임, 선반, 단열 패널의 공장 설치형 솔루션이 요구되고 있습니다.

많은 신흥 국가에서 시설 관리자는 수명주기 절약에 아직 납득하지 못했으며 계약자는 종종 응용 교육을 받지 못했습니다. 유통이 끊어지기 때문에 기술 지원에 대한 액세스가 제한되고 자금이 있어도 배포가 지연됩니다. 업계 연합은 공립 병원에서 입증 프로젝트를 시험적으로 실시하고 감염 예방에 의한 건강 관리 비용 절감을 소개합니다.

은은 광역 스펙트럼 효능과 규제 당국에 익숙한 깊이로 2024년 항균 코팅 시장의 49%를 차지했습니다. 은 나노입자는 박테리아의 호흡과 효소 활성을 저해하고, 내성균의 발생을 저지하고, 위험이 높은 환경에서의 채용을 지원합니다. 생물 유래의 은 시스템의 진보는 항균 보호와 동시에 항산화의 이점도 제공하게 되어 식품에 접촉하는 이용 사례가 확산되고 있습니다.

천연 항균제에 뿌리를 둔 유기화학물질은 CAGR 9.67%를 나타낼 것으로 예측됩니다. 중금속이 없는 라벨과 사용된 프로파일을 개선하려는 브랜드에 매력적입니다. 구리는 지속적인 선택이지만, 칠레 광산의 노동 파업으로 인해 공급이 불안정 해지고 마진이 압박되어 리드 타임이 연장됩니다. 고분자 활성제는 유연성, 투명성, 엘라스토머와의 적합성 등이 최대한의 살균력보다 우선되는 틈새 역할을 담당하고 있습니다.

은은 고가이기 때문에 지금까지 헬스케어 분야 이외에서의 사용은 한정되어 있었지만, 나노화에 의해 표면적이 확대되어, 투여량의 역치가 낮아진 것으로, 현재는 HVAC의 핀, 엘리베이터의 버튼, 소비자용 전기 제품 등에 비용 효율적인 전개가 가능하게 되고 있습니다. 4급 암모늄, 키토산 또는 식물 유래 추출물을 기반으로 하는 유기 시스템은 알레르겐의 안전 임계값을 충족하면서 높은 살충률을 보이며 학교, 사무실 및 주거용 코팅의 잠재력을 넓히고 있습니다. 배합자가 분산을 최적화하고 기존의 아크릴에 필적하는 막의 투명성과 경도를 유지함으로써 채용이 가속화되고 있습니다.

북미는 2024년 항균 코팅 시장 매출의 45%를 차지했습니다. 엄격한 HAI 기준이 병원 개보수를 촉구하고 연방 정부의 인프라 지출에는 위생적인 공공시설용 재료에 대한 할당이 포함되어 있습니다. 아시아태평양의 2030년까지의 CAGR은 8.98%를 나타낼 것으로 예측됩니다. 중국은 첨단 제조업의 규모를 확대하고 인도의 '메이크 인 인디아'는 기능성 첨가제의 국내 생산을 가속화하고 ASEAN의 냉장 물류에 대한 설비 투자는 분체 도장 수주를 밀어 올립니다.

유럽은 화학 안전법에 의해 지원되며 큰 점유율을 차지합니다. 이 지역의 REACH 프레임워크는 금속이 없는 시스템으로의 축발을 앞당기고 바이오기반 활성제의 연구개발세제 우대조치를 뒷받침합니다.

중동 및 아프리카와 남미에서는 아직 막 시작되었지만 수요가 높아지고 있습니다. 걸프 협력 회의 회원국의 병원은 의료 관광 증가에 따라 감염 방지 대책에 투자하고, 브라질의 식육 가공 공장은 수출 기준을 충족시키기 위해 냉장실을 개수합니다. 또한 브라질 식육 가공 공장에서는 수출 기준을 충족하기 위해 냉장실을 개조하고 있습니다.

The Anti-microbial Coatings Market size is estimated at USD 4.74 billion in 2025, and is expected to reach USD 6.84 billion by 2030, at a CAGR of 7.41% during the forecast period (2025-2030).Heightened infection-control standards in hospitals, cold-chain logistics growth, and tighter volatile-organic-compound rules are reinforcing long-term demand.

Silver-based formulations retained primacy with 49% of 2024 revenue, yet waterborne organic chemistries are accelerating on a 9.67% CAGR as buyers prioritize lower environmental impact. North America accounted for the largest regional demand, supported by strict hospital-acquired infection (HAI) protocols, whereas Asia-Pacific is advancing fastest on a broad industrial base and expanding manufacturing capacity. Competitive intensity centers on functional innovation, nanostructured actives, non-leaching binders, and multi-property systems capable of bonding to composites and engineered polymers, rather than on price. Smaller specialists are gaining traction by tailoring solutions to touch-interface electronics, refrigerated logistics, and high-hygiene construction materials.

Hospital administrators are installing surface treatments after clinical studies recorded 36% lower pooled HAIs and 75-79% bacterial load reductions on treated intensive-care surfaces. Although antimicrobial paints cost 20-50% more than standard coatings, shorter recovery times and lower readmission rates justify the premium. Transparent top-coats enable retrofits without altering aesthetics; nano-enabled variants sustain efficacy between routine cleanings.

Temperature-controlled warehousing is expanding, and end users prefer powder systems that cure uniformly at lower temperatures and resist abrasion inside refrigeration units. Harmonized ASEAN food-safety rules are standardizing antimicrobial specifications, prompting factory-installed solutions for conveyer frames, shelving, and insulated panels.

Facility managers in many developing countries remain unconvinced of life-cycle savings, and contractors often lack application training. Fragmented distribution limits access to technical support, slowing uptake even where financing exists. Industry coalitions are piloting demonstration projects in public hospitals to showcase healthcare cost reductions from infection prevention.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Silver commanded 49% of the anti-microbial coatings market in 2024 thanks to broad-spectrum efficacy and regulatory familiarity. Silver nanoparticles disrupt bacterial respiration and enzyme activity, stalling resistance development and supporting adoption in high-risk settings. Advances in biogenic silver systems now deliver antioxidant benefits alongside antimicrobial protection, widening food-contact use cases.

Organic chemistries, rooted in natural antimicrobials, are forecast to rise at 9.67% CAGR. They appeal to brands seeking heavy-metal-free labels and improved end-of-life profiles. Copper remains a durable option, yet supply volatility-intensified by labor strikes at Chilean mines-tightens margins and extends lead times. Polymeric actives occupy niche roles where flexibility, clarity, or compatibility with elastomers outweigh maximum microbicidal strength.

Silver's premium pricing historically limited use outside healthcare, but nano-enabled surface area gains and lower dosage thresholds now support cost-effective deployment in HVAC fins, elevator buttons, and consumer appliances. Organic systems based on quaternary ammonium, chitosan, or plant-derived extracts demonstrate high kill rates while meeting allergen-safety thresholds, unlocking school, office, and residential coatings. Adoption accelerates as formulators optimize dispersion to preserve film clarity and hardness comparable to conventional acrylics.

The Antimicrobial Coatings Market Report Segments the Industry by Material (Silver, Copper, Polymeric, Organic, and Other Materials), Coating Form (Powder, Liquid, and Others), Application (Building and Construction, Food Processing, Textiles, Home Appliances, Healthcare, Marine, and Other Applications) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

North America represented 45% of the anti-microbial coatings market revenue in 2024. Stringent HAI standards drive hospital retrofits, and federal infrastructure spending includes allocations for hygienic public-facility materials. Asia-Pacific is forecast to post an 8.98% CAGR through 2030. China scales advanced manufacturing, India's "Make in India" accelerates domestic output of functional additives, and ASEAN capital spending on refrigerated logistics boosts powder-coating orders.

Europe holds a sizeable share, underpinned by chemical-safety legislation. The region's REACH framework hastens the pivot to metal-free systems and drives research and development tax incentives for bio-based actives.

The Middle East and Africa, and South America show nascent but rising demand. Gulf Cooperation Council hospitals invest in infection-control measures as medical tourism grows, while Brazilian meat-processing plants retrofit cold rooms to meet export standards. Limited local manufacturing capacity opens partnership opportunities for global suppliers.