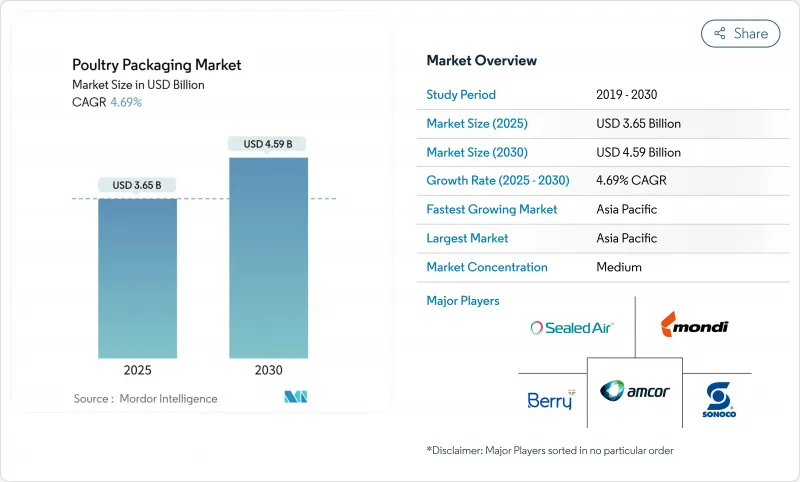

가금류 포장 시장은 2025년 36억 5,000만 달러에 이르고, 2030년에는 45억 9,000만 달러를 달성하며 CAGR 4.69%를 나타낼 것으로 예측됩니다.

케이스 레디의 가금류에 대한 수요 증가, 새로운 개선 대기 솔루션, 지속가능성 규제가이 꾸준한 성장을 지원합니다. 소매업체는 수축과 노력을 줄이는 선반 넣을 수있는 가금류 트레이를 선호합니다. 전자상거래에서는 며칠간의 운송에 견딜 수 있는 단열형이 요구되고 있습니다. 종이 기반 라미네이트로의 소재 이동은 생산자에게 처리량을 잃지 않고 장벽 층을 혁신하도록 강요합니다. 한편, 합병은 컨버터와 가공업자 간의 협상력을 변화시키고 있으며, 기술 기업은 체인의 각 링크에 온도 남용을 경고하는 센서를 내장하려고 합니다.

밀레니얼 세대와 제너레이션 Z의 쇼핑객은 벗기기 쉬운 트레이와 오븐 가능한 파우치에 들어간 빠르고 번거로운 가금류 요리를 선호합니다. 따라서 주요 소매업체는 매장 내 노력을 줄이고 제품 일관성을 향상시키는 집중 케이스 준비 프로그램을 지정합니다. 트레이 제조 업체는 현재 신선도를 며칠 연장하는 흡수 패드와 가스 플래시 밸브를 통합하고 있습니다. G. 몬디니와 같은 장비 공급업체는 정확한 물약과 낮은 필름 게이지를 결합한 모듈형 라인을 공급하여 외형의 아름다움을 희생하지 않고 재료 사용을 줄입니다. 외식 체인은 쿨러에서 그릴까지 한 단계로 이동할 수있는 미리 닦은 진공 스킨 팩을 주문하여이 변화를 반영합니다. 프리미엄 밀 키트 플랫폼은 동일한 포장을 사용하여 출하 시 보존성을 높이고 고급 필름 비용을 상쇄하는 높은 마진을 획득했습니다.

가스 치환 포장은 미생물의 성장을 늦추는 것으로 유통 기한을 향상시키지만, 초기의 고산소 배합은 지질의 산화와 색조 변화를 촉진했습니다. 컨버터는 현재 안전 우려를 높이지 않고 블룸을 안정화시키는 일산화탄소 보조제를 시도하고 있습니다. 듀로 팩과 같은 기업의 진공 스킨 필름은 퍼지를 방지하고 펑크를 견딜 수 있기 때문에 본인 컷에 매력적입니다. 포장 내에 오존을 발생시키는 플라즈마 처리 트레이는 화학제품을 사용하지 않고 캄필로박터를 90%, 살모넬라균을 60% 절단합니다. MULTIVAC과 같은 장비 제조업체는 MAP 밸브와 마이크로 천공 뚜껑을 결합하여 가공업자가 SKU별 가스 비율을 조정할 수 있도록 합니다.

2024년부터 2025년까지 HPAI의 파도는 공급망에서 수백만 마리의 새를 제거하고 생산 일정을 혼란스럽게 하고 무게 등급별 트레이 수요를 변화시켰습니다. 미국 농무부는 보상에 18억 달러를 지출했지만, 축사가 재증식하는 데는 24주가 걸리고 생산량의 불안정성을 길게 하고 있습니다. 워싱턴 대학의 고속 바이오센서는 5분 안에 H5N1을 검출하여 조기 봉쇄와 표적 도태를 가능하게 했습니다. 무리주기가 짧아지면 가공업자는 더 유연한 크기를 주문하고 브랜드 믹스를 조정할 수 없게됩니다.

가금류 카테고리가 가금류 포장 시장의 65.89%를 차지하는 이유는 소비자들에게 널리 받아들여지고 탈골 라인이 합리화되고 있기 때문입니다. 처리 능력이 높기 때문에 가공업자는 필름의 비용 협상을 할 수 있어 식품 폐기물을 삭감하는 필 씰 뚜껑의 실험에 박차가 걸립니다. 오리 고기는 그 밑단의 좁음에도 불구하고, 고급 소매업체가 진공 스킨 트레이가 들어간 세련된 가슴살 물약 컨트롤을 도입함에 따라 CAGR 5.61%를 나타낼 전망입니다. 오리의 가금류 포장 시장 규모는 이국적인 단백질이 주류 냉동고로 이동함에 따라 꾸준히 상승할 것으로 예측됩니다. Amcor의 강화 장벽 가방은 유지의 전환을 방지하고 고기의 색상을 진하게 유지하며 고급 프레젠테이션 기준을 충족합니다.

오리의 상승에 따라 컨버터는 내유성 코팅을 통합하고 소매점에 호소하기 위해 투명성을 유지해야합니다. 오리 고기는 현재 자동화에 의해 중량 규격에 맞추어, 가금류와 같은 케이스 레이디의 롤아웃이 가능하게 되어 있습니다. 튀르키예는 계절 홀버드 형식으로 점유율을 유지하고 있지만, 부가가치가 높은 로스트와 슬라이스 된 델리 팩은 연중 수요를 지원합니다. 따라서 각 단백질마다 배리어성, 펑쳐 강도, 실루엣을 조정할 필요가 있고, 필름 제조업체는 SKU 수를 늘리지 않고 포트폴리오의 폭을 넓힐 필요가 있습니다.

플렉서블 구조는 2024년에 가금류 포장 시장의 62.93%를 차지해, 보다 낮은 재료 강도와 선반의 존재감을 높이는 높은 그래픽에 지지되었습니다. 모노 PET 라미네이트와 PE 라미네이트가 스토어 드롭 재활용이 가능해짐에 따라, 이 포맷은 매년 5.39%씩 성장해 성장 리더로 계속 될 것으로 보입니다. 가금류 포장 시장 규모에서 경질 트레이는 적층 안정성의 혜택을 받는 고급 오븐 대응 SKU 및 홀버드 프레젠테이션에서 그 역할을 유지합니다.

GEA의 PowerPak 1000과 같은 장비는 중간 규모 공장에서 진공, MAP 및 가죽 변형을 한 프레임으로 전환하여 전환 가동 중지 시간을 줄일 수 있습니다. 플렉서블 파우치는 현재 pH가 상승하면 색이 변하는 신선도 센서를 내장하고 포장지를 품질 모니터로 바꾸고 있습니다. 이러한 업그레이드는 비용에 민감한 단백질 카테고리의 가격대를 보호하고 수축을 줄이기 위해 코드 수명 연장을 요구하는 소매 업체를 만족시킵니다.

아시아태평양은 2024년 가금류 포장 시장의 38.71%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR) 5.24%를 나타낼 것으로 예측됩니다. 중국과 인도의 급속한 도시 이동과 가처분 소득 상승은 냉동 가금류 수요를 밀어 올리고 태국은 수출 지위를 강화합니다. 국가의 서큘러 이코노미 규칙이 재활용 가능한 라미네이트 채택에 박차를 가하고 현지 가공업자는 수출 위생 기준을 충족하기 위해 세계 기계 제조업체와 제휴합니다. 인도네시아와 베트남에 진출하는 다국적 소매업체는 사례 준비 프로그램을 지정하고 지역 컨버터에 새로운 비즈니스를 제공합니다.

북미는 금액 기준으로 2위입니다. 연방 정부의 규제는 여전히 안정적이지만, 캘리포니아와 오레곤과 같은 국가는 생산자 책임 수수료를 추가하고 단일 소재 형식에 보상을 제공합니다. 소비자는 항생제를 사용하지 않고 지속가능성 인증 팩에 지불할 강한 의지를 보여주며, 각 브랜드가 퇴비화 가능한 트레이를 시험적으로 도입하도록 격려하고 있습니다. 캐나다의 '플라스틱 폐기물 제로' 의제의 업데이트는 EU의 목표에 부응하여 종이와 폴리머의 하이브리드로의 전환을 더욱 가속화합니다. 지능형 라벨은 대형 상점이 추적성을 위한 온팩 QR 코드를 테스트하고 있으며 조기 보급을 볼 수 있습니다.

유럽에서는 헤드라인의 성장이 낮지만 혁신의 밀도는 높습니다. 규칙 2025/40은 2030년까지 100%의 재활용 가능성을 강제하고 PFAS를 금지하기 때문에 컨버터는 신속한 재료 대체를 강요합니다. 소매업체는 공급업체와 협력하여 가금류의 신선도를 21일 동안 유지하는 완전 섬유 트레이를 확인합니다. 독일에서는 스마트 센서의 테스트 운용이 시간과 온도의 남용을 추적하고 폐기를 억제하기 위한 역동적인 할인에 도움이 되는 데이터를 제공합니다.

The poultry packaging market reached USD 3.65 billion in 2025 and is expected to achieve USD 4.59 billion by 2030, advancing at a 4.69% CAGR.

Rising demand for case-ready poultry, new modified-atmosphere solutions, and sustainability regulations underpin this steady growth. Retailers prefer shelf-stable chicken trays that reduce shrink and labor. E-commerce adds volume for insulated formats that survive multi-day transit. Material shifts toward paper-based laminates press producers to innovate barrier layers without losing throughput. Meanwhile, merger activity is altering bargaining power between converters and processors, and technology firms are embedding sensors that warn of temperature abuse at every link in the chain.

Millennial and Generation Z shoppers favor quick, no-mess poultry meals that arrive in easy-peel trays or ovenable pouches. Large retailers therefore specify centralized case-ready programs that cut in-store labor and improve product consistency. Tray producers now integrate absorbent pads and gas-flush valves that extend freshness by several days. Equipment vendors such as G.Mondini supply modular lines that blend precise portioning with lower film gauge, trimming material use without sacrificing visual appeal. Foodservice chains mirror this shift by ordering pre-marinated, vacuum-skin packs that move from cooler to grill in one step. Premium meal-kit platforms exploit the same packaging to boost shelf life during shipping, capturing higher margins that offset advanced film costs.

Modified-atmosphere packaging improves shelf life by slowing microbial growth, yet early high-oxygen blends accelerated lipid oxidation and color shifts. Converters now trial carbon-monoxide adjuncts that stabilize bloom without raising safety concerns. Vacuum-skin films from firms like Duropac prevent purge and withstand puncture, making them attractive for bone-in cuts. Plasma-treated trays that create in-pack ozone cut Campylobacter by 90% and Salmonella by 60% without chemicals. Equipment makers such as MULTIVAC pair MAP valves with micro-perforated lids so processors can tune gas ratios to each SKU.

The 2024-2025 HPAI wave removed millions of birds from supply chains, unsettling production schedules and altering tray demand by weight class. USDA spent USD 1.8 billion on indemnities, but barns need up to 24 weeks to repopulate, prolonging volume instability. Rapid biosensors from Washington University now detect H5N1 in five minutes, enabling earlier lockdowns and targeted culls. Shorter flock cycles force processors to order more flexible sizes and adjust brand mix, which in turn influences run-length planning for converters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The chicken category owns 65.89% of the poultry packaging market, thanks to broad consumer acceptance and streamlined deboning lines. High throughput lets processors negotiate film cost and spur experimentation with peel-reseal lids that cut food waste. Duck, despite its modest base, grows at a 5.61% CAGR as upscale retailers introduce portion-controlled breasts in sleek vacuum-skin trays. Here, the poultry packaging market size for duck is forecast to climb steadily as exotic proteins move into mainstream freezers. Enhanced barrier bags from Amcor prevent grease migration and preserve dark-meat color, meeting premium presentation standards.

Duck's rise compels converters to integrate oil-resistant coatings while keeping clarity for retail appeal. Automation now portions duck to weight specs, enabling case-ready rollouts similar to chicken. Turkey holds share through seasonal whole-bird formats, yet value-added roasts and sliced deli packs sustain year-round demand. Each protein therefore demands tailored barrier, puncture strength, and silhouette, nudging film suppliers to broaden portfolios without inflating SKU count.

Flexible structures delivered 62.93% of the poultry packaging market in 2024, supported by lower material intensity and high graphics that elevate shelf presence. The format will remain the growth leader, advancing 5.39% each year as mono-PET and PE laminates become store-drop recyclable. Within the poultry packaging market size, rigid trays retain roles in premium oven-ready SKUs and whole-bird presentations that benefit from stacking stability.

Equipment such as GEA's PowerPak 1000 lets mid-scale plants swing between vacuum, MAP, and skin variants on a single frame, cutting change-over downtime . Flexible pouches now embed freshness sensors that change color when pH rises, turning the wrapper into a quality monitor. These upgrades defend price points in a cost-sensitive protein category and satisfy retailers that push for longer coded life to lower shrink.

The Poultry Packaging Market Report is Segmented by Meat Type (Chicken, Turkey, Duck), Packaging Format (Fixed/Rigid, Flexible), Packaging Material (Plastics, Paper and Paperboard, Metals), Packaging Technology (Modified Atmosphere Packaging, Vacuum Skin Packaging, and More), Distribution Channel (Retail, Foodservice/HORECA, Industrial and Institutional), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 38.71% of the poultry packaging market in 2024 and is projected to expand at a 5.24% CAGR to 2030. Rapid urban migration and rising disposable income in China and India lift chilled-poultry demand, while Thailand strengthens its export position. National circular-economy rules spur adoption of recyclable laminates, and local processors engage global machinery firms to meet export hygiene codes. Multinational retailers entering Indonesia and Vietnam specify case-ready programs, unlocking new business for regional converters.

North America ranks second in value. Federal regulation remains stable, but states such as California and Oregon add producer-responsibility fees that reward mono-material formats . Consumers display strong willingness to pay for antibiotic-free and sustainability-certified packs, encouraging brands to pilot compostable trays. Canada's updated Zero Plastic Waste agenda echoes EU targets, further accelerating the shift to paper-polymer hybrids. Intelligent labels see early uptake as big-box stores test on-pack QR codes for traceability.

Europe shows low headline growth yet high innovation density. Regulation 2025/40 enforces 100% recyclability by 2030 and bans PFAS, forcing converters into rapid material substitution. Retailers collaborate with suppliers to validate fully fiber trays that keep poultry fresh for 21 days, exemplified by Coveris' new BarrierFresh line. Smart-sensor pilots in Germany track time-temperature abuse, delivering data that informs dynamic discounting to curb waste.