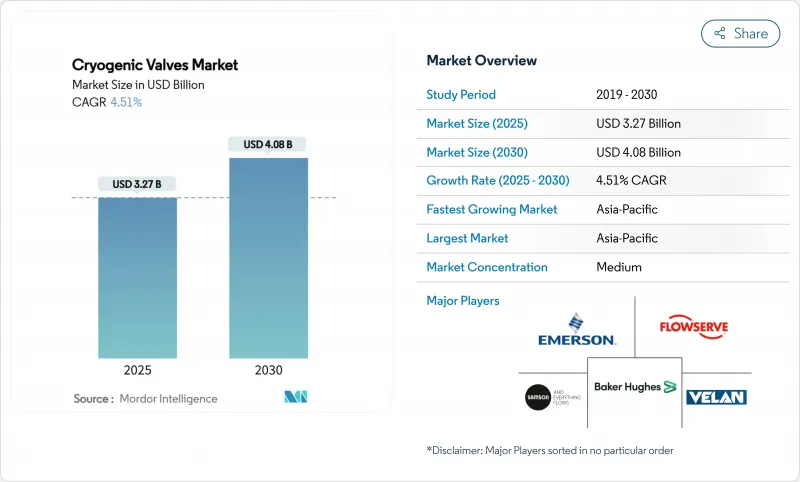

극저온 밸브 시장 규모는 2025년에 32억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 4.51%로, 2030년에는 40억 8,000만 달러에 이를 것으로 예상되고 있습니다.

액화 천연가스(LNG) 터미널, 그린 수소 프로젝트, 석유화학 확장에 대한 투자 증가가 이 꾸준한 궤도를 지원하고 있습니다. 대규모 시설에서는 -150°C 이하의 온도에서 밀봉 가능한 밸브가 각각 수백 개 필요하며, 소유자는 여러 표준에 대응하는 제품을 신속하게 인증할 수 있는 공급자를 선호하고 있습니다. 아시아태평양은 여전히 장비의 가장 큰 구매자이며 북미는 수소 조종사 플랜트와 연관된 가치있는 기회를 제공합니다. 최종 사용자가 장기적인 신뢰성과 빠른 턴 라운드 유지 보수를 요구하기 때문에 극저온 엔지니어링과 애프터 서비스를 결합할 수 있는 제조업체는 프리미엄 계약 상을 받았습니다.

2024년부터 2028년 사이에 예정된 확장 공사로 세계 LNG 액화 능력은 40% 상승하고 미국이 카타르를 빼고 수출의 주도국이 되는 한편 아시아태평양이 증가한 화물의 대부분을 구입하게 됩니다. 베이커 퓨즈는 루이지애나의 2계열 LNG 설비에서 56억 달러의 수주를 획득했으며, 초저 누설 성능을 보장할 수 있는 현장에서 입증된 밸브 파트너에 대한 계약자의 의욕을 보여주고 있습니다. 해상 벙커 수요는 2030년까지 연간 1,600만 톤을 초과할 것으로 예상되며, 항만은 긴급 차단 밸브를 통합한 자동 저온 이송 어셈블리를 지정하도록 촉구하고 있습니다. 엔터프라이즈 프로덕츠 파트너스는 휴스턴쉽 채널의 냉동능력을 30만 배럴/일 확대해, -162℃까지의 트리플 오프셋 스톱 밸브의 신규 수주를 창출합니다. 사우디 알람코의 파딜리 업그레이드는 77억 달러로, 스위트 가스 처리를 1.3Bcf/d 추가하는 것으로, 각 트레인에는 혼합 냉매를 취급하기 위한 리던던트 극저온 플로우 패스가 장비됩니다.

텍사스에 위치한 에어 리퀴드의 4개의 모듈식 공기 분리 유닛은 엑손 모빌의 저탄소 수소 복합체에 9,000톤/일의 산소를 공급하여 대륙 최대의 아르곤 스트림을 생성합니다. 헬스케어의 확대에 의해 액체 산소의 소비량은 증가의 일도를 따르고 있으며, 병원은 환자용 회로에서의 입자 유출을 막는 밸브 설계를 의무화하고 있습니다. 식품 가공업자는 급속 냉동을 위한 액체 질소 터널을 선호하고 있으며 위생적인 마무리를 유지하면서 -196℃까지의 급속한 열 사이클을 견디는 밸브를 사용합니다. 신재생에너지에 의한 공기분리 플랜트에서는 운전자가 변동하는 송전망의 요금에 맞추어 출력을 조정할 수 있도록 고속응답제어 트림이 필요합니다.

ASME B31.3은 -425°F 이하의 충격 시험된 재료를 의무화합니다. 호환되는 밸브는 샤르피 시험에서 입증된 오스테나이트계 스테인리스 또는 알루미늄 합금을 사용합니다. 2025년 ASME VIII 업데이트에서는 새로운 극저온 사례 연구가 도입되었으며 설계자는 새로운 규칙을 충족하기 위해 두꺼운 보닛과 벨로우즈 씰을 추가해야 합니다. MSS SP-158-2021은 고압 가스 시험을 의무화하고 개발 비용을 상승시키지만 유틸리티 기업은 정전 위험을 줄이기 위해 인증 취득을 요구하고 있습니다. 미국 코드 49CFR은 밸브에 탱크 시험 압력을 침투시키지 않고 유지하고 기계적 손상에 대한 견고한 가드를 포함해야 하며 트레일러 레이아웃 옵션을 형성합니다. 안전 밸브의 5년 재인증 사이클은 경상적인 서비스 수입을 창출하지만 소규모 사업자에게는 소유 비용을 상승시킵니다. 소규모 제조업체는 여러 관할 구역에 걸친 코드 작업을 따라잡는 데 어려움을 겪고 있으며 기존 브랜드의 경쟁력이 떨어지고 있습니다.

2024년 극저온 밸브 시장 점유율은 볼 밸브가 34.18%를 차지했습니다. 제조업체 각 회사는 끓는 액화 가스에서 밸브 시트를 격리하고 얼음 축적과 밸브 시트 손상을 방지하는 확장 스템 디자인을 제공합니다. 에머슨의 Fisher HP 시리즈는 스프링으로 작동하는 PTFE 링을 사용하여 -198 ° C에서 클래스 VI의 셧오프를 유지합니다. 글로브 밸브는 설치 베이스에서는 작지만, 수소 액화 프로젝트에서는 그 조리개 정밀도가 선호되기 때문에 CAGR 5.41%를 나타낼 전망입니다. 글로브 밸브의 극저온 밸브 시장 규모는 8-10t/h의 액체 수소를 생산하는 파일럿 플랜트에서 현저하게 확대될 것으로 예상되며, 각 플랜트에서는 오르소파라 변환열을 관리하기 위한 가변 유량 제어가 요구되고 있습니다.

기술 강화는 두 제품 라인에서 계속됩니다. 볼 밸브 제조업체는 ESG 크레딧을 요구하는 운영자에게 중요한 요소인 초저 퓨지티브 방출을 위한 ISO 15848-1 클래스 A에 인증된 흑연 보닛 씰을 추가합니다. 글로브 밸브의 OEM은 등비 특성을 실현하는 윤곽이 있는 플러그를 채용하여 다단식 익스팬더 공정의 안정성을 높이고 있습니다. 게이트 밸브와 체크 밸브는 틈새 응용을 유지합니다. 게이트 밸브는 최대 42인치 풀 보어 LNG 로딩 라인을 지원하며, 듀얼 플레이트 극저온 체크 밸브는 보일 오프 가스 재순환 루프에서 역 서지를 방지합니다. 특수 버터플라이 밸브와 플러그 밸브는 초저 토크가 필수적인 초저밀도 헬륨 서비스 등의 갭을 메웁니다.

수동 기어와 핸드 휠 운영자는 2024년 극저온 밸브 시장의 59.82%를 차지하며, 단순성과 전원 손실 시의 본질적인 페일 세이프 기능이 중점을 두었습니다. LNG 수출 터미널은 버스 측 긴급 상황에서화물 라인을 확보하기 위해 수동 격리 밸브에 의존합니다. 그러나 시설 소유자가 인력 감소를 위한 원격조작에 주목하고 있기 때문에 이 부문의 성장은 완만합니다. 공압 액추에이션은 2030년까지 연평균 복합 성장률(CAGR) 5.57%를 나타내 페일 클로즈드 로직 하에서 플랜트의 공기나 질소를 활용하여 신속한 스트로크 시간을 실현합니다. 수소 제조 시설에서는 전기 모터와 관련된 발화 위험을 피하기 위해 공압 구동이 선호됩니다.

전동 액추에이터는 제품의 질감을 유지하기 위해 유량을 미세 조정하는 디지털 방식으로 관리되는 질소 동결 터널과 같이 데이터가 풍부한 위치 피드백이 필수적인 경우 틈새 지지를 얻습니다. 공압 드라이브에 디클러치 가능한 기어 박스를 볼트로 고정하는 하이브리드 솔루션은 수동 오버라이드와 자동화된 속도를 결합하여 듀얼 사용 설비에 대한 수요를 획득하고 있습니다. OEM은 스템의 마찰과 사이클 카운트를 측정하는 스마트 포지셔너를 통합하는 것이 증가하고 있으며, 누출이 발생하기 전에 서비스 작업 지시를 내리는 플랜트 히스토리에 공급하고 있습니다. 이 예측 유지 보수 모델은 애프터마켓과의 연결을 강화하고 설치된 밸브의 평생 수익을 향상시킵니다.

아시아태평양은 2024년에 극저온 밸브 시장의 26.55%를 차지했고, 2030년까지의 CAGR은 5.72%로 확대될 것으로 예측되고 있습니다. 중국의 가스 투 파워 정책의 전환과 인도의 열파에 의한 수요가 수입의 성장을 부활시키는 한편, 일본과 한국은 미국으로부터의 화물을 재배치하는 리로딩 허브에 투자하고 있습니다. 호주에서는 노후화된 액화 트레인이 리노베이션 사이클에 들어가 애프터마켓 밸브 서비스를 뒷받침하고 있습니다. 중국, 한국, 호주 정부의 수소 로드맵은 파일럿 액화 시설에서 고압 장갑 밸브의 입찰을 증가시킵니다.

북미는 미국이 세계 최대의 LNG 수출국이 된 것과 수소 허브에 대한 연방 정부의 적극적인 자금 원조로부터 혜택을 받습니다. 멕시코 걸프의 브라운필드 액화 프로젝트에서는 북미 밸브 공업회의 회원이 되도록 규정되어 있으며, 현지에 재고가 있는 국내 공급자가 유리합니다. 에어 리퀴드의 베이 타운에 대한 투자와 여러 중형 액체 산소 제조 사업은 산업용 가스 밸브의 안정적인 수요를 유지합니다. 2027년 브리티시컬럼비아주에서 캐나다 최초의 LNG 출하가 예정되어 서반구 수요가 증가하고 있습니다.

유럽은 2024년 LNG 수입 감소에도 불구하고 수소에 적극적으로 참여했습니다. 독일에서 계획된 1,000만kW의 전해조 용량은 액화 및 지하 저장 계획에 연결되어 있으며 각각은 초저 누설 격리 밸브를 지정합니다. 호라이즌 유럽은 스페인과 네덜란드 사이의 이동식 LH2 탱크 시험에 자금을 제공하여 특수 카고 핸들링 밸브 주문을 생성합니다. 북유럽의 항만은 녹색 회랑 항로의 제휴를 지원하는 LNG 벙커링의 전개를 가속화하고 있습니다.

중동 및 아프리카에서는 대규모 가스 처리의 녹색 분야를 볼 수 있습니다. 사우디 알람코의 Fadhili 확장 공사, 카타르의 North Field South, 오만의 여러 석유화학 콤비나트는 사워가스 화합물에 내성이 있는 내구성이 있는 저온 야금이 필요합니다. 아부다비는 LNG 트레인에서 밸브 패키지까지 설계 사상을 도입하는 블루 암모니아를 모색하고 있습니다. 아프리카에서는 모잠비크의 육상 LNG 플랜트 건설이 연기되고 있지만, 안보가 안정되면 밸브 조달의 새로운 사이클을 기대할 수 있습니다.

남미는 아직 막 시작되었지만 유망합니다. 브라질은 계절적 가스 부족을 관리하기 위해 부유식 저장 및 재기화 장치를 검토하고 있으며 소형 극저온 밸브 스키드가 필요합니다. 아르헨티나의 바카 무에르타 셰일은 LNG 수출 바지 프로젝트에 궁극적으로 공급될 수 있지만, 시기의 불확실성은 당분간 수요를 억제하고 있습니다. 칠레의 광업 부문은 공정 효율성을 위해 액체 산소를 연구하고 있으며 소규모이지만 이익률이 높은 밸브 전망을 보여줍니다.

The Cryogenic Valves Market size is estimated at USD 3.27 billion in 2025, and is expected to reach USD 4.08 billion by 2030, at a CAGR of 4.51% during the forecast period (2025-2030).

Rising investment in liquefied natural gas (LNG) terminals, green-hydrogen projects, and petro-chemical expansions underpins this steady trajectory. Large-scale facilities each require hundreds of valves capable of sealing at temperatures below -150 °C, and owners favour suppliers able to certify products quickly for multiple codes. Asia-Pacific remains the largest regional buyer of equipment, while North America delivers high-value opportunities tied to hydrogen pilot plants. Producers able to combine cryogenic engineering depth with aftermarket services are attracting premium contract awards, as end-users seek long-term reliability and fast turn-round maintenance.

Expansions slated between 2024-2028 will lift global LNG liquefaction capacity by 40%, with the United States overtaking Qatar as lead exporter while Asia-Pacific purchases the bulk of incremental cargoes. Baker Hughes secured USD 5.6 billion of LNG equipment awards for two Louisiana trains, illustrating contractor appetite for field-proven valve partners able to guarantee ultra-low-leak performance. Marine bunkering demand is forecast to exceed 16 million t annually by 2030, prompting ports to specify automated cryogenic transfer assemblies that integrate emergency shut-off valves. Enterprise Products Partners is expanding Houston Ship Channel refrigeration capacity by 300,000 bbl/d, creating new orders for triple-offset stop-valves rated down to -162 °C. Saudi Aramco's USD 7.7 billion Fadhili upgrade will add 1.3 Bcf/d of sweet-gas processing, each train fitted with redundant cryogenic flow-paths to handle mixed refrigerants.

Air Liquide's four modular air-separation units in Texas will deliver 9,000 t/d of oxygen to ExxonMobil's low-carbon hydrogen complex and generate the continent's largest argon stream, placing long-cycle demand on valve makers able to certify for oxygen service. Healthcare expansion keeps liquid-oxygen consumption rising, and hospitals mandate valve designs that prevent particle shedding in patient circuits. Food processors favour liquid nitrogen tunnels for flash-freezing, with valves that tolerate rapid thermal cycling down to -196 °C while maintaining hygienic finishes. Renewable-powered air-separation plants require fast-response control trim so operators can throttle output to match fluctuating grid tariffs.

ASME B31.3 mandates impact-tested materials below -425 °F; complying valves use austenitic stainless or aluminium alloys proven by Charpy testing. The 2025 ASME VIII update introduces fresh cryogenic case studies, prompting designers to add thicker bonnets or bellows seals to satisfy the new rules. MSS SP-158-2021 requires high-pressure gas tests that inflate development costs, yet utilities increasingly insist on the certification to reduce outage risk. U.S. Code 49 CFR obliges valves to hold tank test pressure without seepage and to include robust guards against mechanical damage, shaping layout choices on trailers. Five-year recertification cycles for safety valves generate recurring service revenue but raise ownership costs for small operators. Smaller fabricators struggle to keep pace with multi-jurisdiction code work, giving established brands a competitive edge.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ball valves held a dominant 34.18% cryogenic valves market share in 2024, owing to proven tight shut-off and straightforward maintenance. Manufacturers supply extended-stem designs that isolate the seat from boiling liquefied gases, cutting ice buildup and seat damage. Emerson's Fisher HP series uses spring-energised PTFE rings to hold Class VI shut-off at -198 °C. Globe valves, though smaller in installed base, are expected to grow at 5.41% CAGR as hydrogen liquefaction projects favour their throttling precision. The cryogenic valves market size for globe valves is anticipated to widen notably in pilot plants producing 8-10 t/h of liquid hydrogen, each calling for variable-flow control to manage ortho-para conversion heat.

Technical enhancements continue across both lines. Ball-valve makers are adding graphite bonnet seals certified to ISO 15848-1 Class A for ultra-low fugitive emissions, an important factor for operators seeking ESG credits. Globe-valve OEMs are deploying contoured plugs that deliver equal-percentage characteristics, enhancing process stability in multi-stage expanders. Gate and check valves retain niche uses: gate valves accommodate full-bore LNG loading lines up to 42 in, while dual-plate cryogenic check valves prevent reverse surge in boil-off gas recirculation loops. Specialty butterfly and plug valves fill gaps such as helium service at ultra-low density where very low torque is essential.

Manual gear and hand-wheel operators represented 59.82% of the cryogenic valves market in 2024, prized for simplicity and intrinsic fail-safe capability during power loss. LNG export terminals rely on manual isolation valves to secure cargo lines during berth-side emergencies. The segment, however, grows slowly as facility owners look to remote operation to cut staffing. Pneumatic actuation will expand at 5.57% CAGR to 2030, leveraging plant air or nitrogen to deliver quick stroke times under fail-closed logic. Hydrogen sites favour pneumatic drives to avoid ignition risks linked to electric motors.

Electric actuators achieve niche uptake where data-rich position feedback is essential, such as in digitally managed nitrogen freezing tunnels that fine-tune flow to maintain product texture. Hybrid solutions that bolt a declutchable gearbox onto a pneumatic drive combine manual override with automated speed, capturing demand in dual-use installations. OEMs increasingly embed smart positioners measuring stem friction and cycle count, feeding plant historians that trigger service work orders before leakage occurs. This predictive-maintenance model strengthens aftermarket ties and lifts lifetime revenue per installed valve.

The Cryogenic Valves Market Report is Segmented by Product Type (Ball Valve, Gate Valve, Globe Valve, Check Valve, Other Product Types), Actuation (Manual, Pneumatic, Electric), Gas (Liquid Nitrogen, Liquid Natural Gas, and More), End-User Industry (Oil and Gas, Energy and Power, Chemicals, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 26.55% of the cryogenic valves market in 2024 and is projected to expand by a 5.72% CAGR through 2030. China's gas-to-power policy reversal and India's heat-wave-driven demand are reviving import growth, while Japan and South Korea invest in re-loading hubs that reposition cargoes from the United States. Australia's ageing liquefaction trains enter refurbishment cycles, pushing aftermarket valve services. Government hydrogen roadmaps in China, South Korea and Australia create incremental bids for high-pressure globe valves at pilot liquefier sites.

North America benefits from the United States becoming the world's largest LNG exporter and from aggressive federal funding for hydrogen hubs. Gulf Coast brownfield liquefaction projects stipulate North American Valve Manufacturers Association membership, favouring domestic suppliers with local inventories. Air Liquide's Baytown investment plus multiple mid-scale liquid-oxygen build-owns maintain steady industrial-gas valve uptake. Canada's first LNG shipment slated for 2027 from British Columbia will add western-hemisphere demand.

Europe, despite softer LNG imports in 2024, commits heavily to hydrogen. Germany's planned 10 GW of electrolyser capacity links to liquefaction and underground storage schemes, each specifying ultra-low-leak isolation valves. Horizon Europe funds mobile LH2 tank trials between Spain and the Netherlands, generating specialty cargo-handling valve orders. Nordic ports accelerate LNG bunkering roll-outs supporting green-corridor shipping alliances.

The Middle East and Africa witness sizeable greenfield gas processing. Saudi Aramco's Fadhili expansion, Qatar's North Field South and multiple Omani petro-chem complexes need durable cryogenic metallurgy that resists sour-gas compounds. Abu Dhabi is exploring blue-ammonia, which will import design philosophies from LNG trains to valve packages. In Africa, Mozambique's postponed onshore LNG plant, once security stabilises, promises a fresh cycle of valve procurement.

South America remains nascent yet promising. Brazil eyes floating storage and regasification units to manage seasonal gas deficits, requiring compact cryogenic valve skids. Argentina's Vaca Muerta shale may eventually feed LNG export barge projects, though timetable uncertainty tempers near-term demand. Chile's mining sector investigates liquid oxygen for process efficiency, presenting small but high-margin valve prospects.