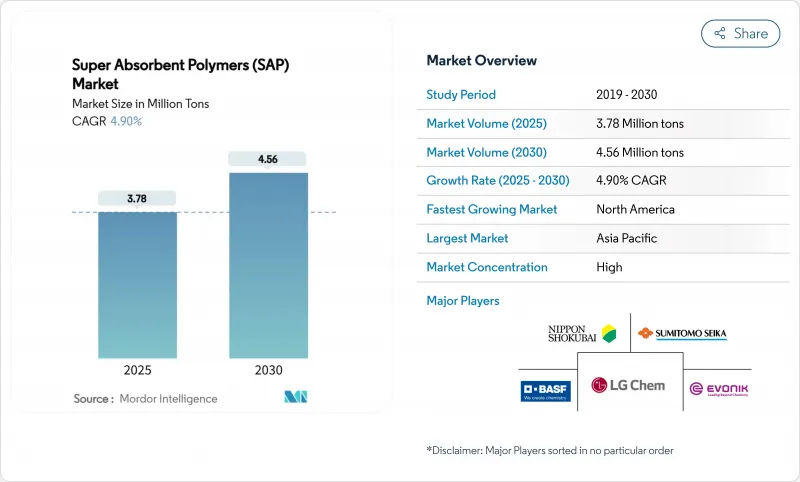

고흡수성 수지(SAP) 시장 규모는 2025년 378만 톤으로 평가되었고, 예측기간(2025-2030년)의 CAGR은 4.90%를 나타낼 것으로 예측되며 2030년에 456만톤에 이를 전망입니다.

유아용 기저귀 수요 확대, SAP 성인용 요실금 패드의 급속한 보급, 산업 및 농업 분야의 응용 범위 확대가 이러한 꾸준한 성장의 핵심 동력입니다. 바이오 기반 화학 물질을 장려하는 유럽의 강화된 규제와 중국 및 인도의 1인당 기저귀 소비 증가가 제품 포트폴리오를 프리미엄 고성능 등급으로 재편하고 있습니다. 제조업체들은 아크릴산 가격 변동 완화를 위해 에너지 효율성 향상 및 수직 통합을 위한 공장 업그레이드를 지속하고 있습니다. 동시에 소비자 직구 구독 모델과 전자상거래 기반 콜드체인 포장은 표준 위생용품 부문의 마진 압박을 상쇄하는 고마진 틈새시장을 개척하고 있습니다. 셀룰로오스 및 전분 유래 대체재에 대한 투자 증가로 지속가능성이 이제 고흡수성 수지 시장에서 브랜드 가치와 공정 혁신을 동시에 주도하고 있음을 시사합니다.

중국 도시 가구는 대가족 지원 정책 변화와 가처분 소득 증가에 힘입어 2022년 이후 평균 기저귀 지출을 15% 늘렸습니다. 인도에서는 2 및 3선 도시 유통망 확대로 보급률이 상승하며 초보 구매자들도 고급 기저귀 제품을 접할 수 있게 되었습니다. 프리미엄 SKU에는 고용량 SAP 등급이 포함되고 젤 차단 기능이 개선되어 고흡수성 수지 시장 전반에 걸쳐 단위 소비량과 가치 성장을 가속화하고 있습니다. 현지 변환업체들은 품질 확보 및 운송 위험 완화를 위해 장기 공급 계약을 통해 공급을 점차 확보하고 있습니다.

일본, 한국, 독일, 이탈리아의 인구 고령화로 성인 요실금 유병률이 높아진 반면, 사회적 수용 캠페인을 통해 낙인이 줄어들고 있습니다. 신제품 패드는 최대 40% 더 많은 SAP를 통합하여 일반 속옷과 유사한 얇은 프로필을 구현하고 주간 사용을 장려합니다. 구독형 전자상거래 채널이 성장하며, 비밀 배송, 누출 보증, 이동성 특화 SKU를 패키지로 제공합니다. 제조사들은 하중 하에서 흡수력을 높이는 차별화된 코어-쉘 입자 형태로 대응하며, 고흡수성 수지 시장 내 고마진 하위 부문를 창출하고 있습니다.

아크릴산은 생산 비용의 최대 70%를 차지하며, 분기별 25%에 달하는 가격 변동은 조달 예산을 불안정하게 합니다. 창홍 폴리머의 16억 달러 규모 프로판-아크릴산 공장이 2026년 가동되면 가변 비용 곡선을 낮추고 기존 서구 공급업체 간 가격 균형을 흔들 수 있습니다. 이사회가 원료 안보를 최우선 과제로 삼으면서 바이오 공정 및 수직 통합에 대한 관심이 높아지고 있습니다.

2024년 고흡수성 수지(SAP) 시장 점유율에서 아크릴계 제품이 72%를 차지했으며, 이는 유아용 기저귀에서의 검증된 신뢰성에 기반합니다. 안전성 인식을 강화하기 위해 프리미엄 브랜드들은 자유 단량체 수준이 낮은 고순도 아크릴계 SAP를 지정합니다. 동시에 폴리아크릴아미드 등급은 건조 농업 및 산업용 밀봉 분야에서 우수한 수분 보유력으로 인해 연평균 6.6% 성장률을 보이며 확대되고 있습니다. 고흡수성 수지 시장 규모 측면에서, 폴리아크릴아미드 물량은 2025년부터 2030년 사이에 125킬로톤 증가할 것으로 예상되며, 이는 아크릴 등급으로부터 점유율을 점진적으로 확보하는 것을 의미합니다.

제품 개발자들은 비용과 분해성을 조화시키기 위해 아크릴과 다당류 골격을 혼합한 하이브리드 네트워크를 추구하고 있습니다. 일본쇼쿠바이의 인도네시아 생산 할랄 인증 바이오매스 유래 SAP 라인은 이러한 교차 화학 혁신의 사례입니다. 현재 투자 초점은 일관된 중합체 구조를 보장하는 바이오매스 조달 물류, 불순물 제어, 확장 가능한 연속 반응기 설계로 이동 중입니다.

겔 중합은 2024년 매출 점유율 60%를 유지했으며, 고처리량과 균일한 가교 밀도를 위해 반응기 트레인이 최적화되었습니다. 에너지 회수 루프와 연속 단량체 재활용이 점진적 비용 경쟁력을 주도합니다. 용액 중합은 분자량 분포가 좁고 에너지 부하가 감소된 소량 특수 등급 생산을 가능하게 하여 지속가능성 목표와 부합하므로 연평균 5% 성장률을 기록 중입니다.

현탁 중합 및 역현탁 중합 공정은 의료용 유체 관리용 코어-쉘 미세구체와 같이 독특한 입자 형태가 필요한 틈새 시장에서 지속됩니다. 공정 엔지니어들은 정밀한 가교제 공급 제어와 인라인 분광법을 통해 부하 하에서의 흡수율을 조정하는 데 주력하며, 고흡수성 수지 시장 내 공급을 더욱 세분화하고 있습니다.

고흡수성 수지(SAP) 시장은 제품 유형(폴리아크릴아미드, 아크릴산 기반, 기타), 중합 공정(용액 중합 등), 응용 분야(아기 기저귀, 성인 요실금 제품 등), 최종 사용자 산업(퍼스널케어 제조사, 농업 투입재 공급업체 등), 지역(아시아태평양, 북미, 유럽 등)별로 세분화됩니다. 지역별 분석

아시아태평양 지역은 2024년 고흡수성 수지 시장의 42%를 차지했으며, 이는 원료 물류를 최소화하는 중국의 아크릴산-SAP 통합 클러스터에 힘입은 결과입니다. 특히 장쑤성과 산둥성의 정부 인센티브는 생산 능력 병목 현상 해소 및 수출 지향적 확장을 지원합니다. 인도는 기저귀 보급률 확대를 통해 물량 증가에 기여하는 반면, 일본은 특수 등급 및 바이오매스 유래 등급 분야에서 기술 리더십 틈새 시장을 유지하고 있습니다.

북미는 2030년까지 5.50%의 가장 빠른 연평균 성장률(CAGR은)을 기록할 것으로 전망됩니다. 고가 기저귀 SKU, 고령화 베이비붐 세대의 고흡수성 성인용 요실금 제품 채택 증가, 수압파쇄용 물 차단제 및 콜드체인 패드 등 특수 산업용 수요가 성장 동력입니다. 국립 농업대학과의 연구 컨소시엄은 셀룰로오스 및 단백질 기반 네트워크를 선도하며 기업의 지속가능성 약속과 규제 동향을 연계하고 있습니다. 또한 이 지역은 원예 분야에서 대마 기반 SAP의 초기 현장 적용 사례를 기록하며 고흡수성 수지 시장 내 순환 경제 논리를 강화하고 있습니다.

유럽의 엄격한 정책 환경은 바이오 기반 제품 채택과 포장재 재활용성을 가속화합니다. 독일은 생산량에서 선두를 달리는 반면, 북유럽 국가들은 퇴비화 가능 기저귀 코어에 대한 소비자 선호도를 주도합니다. 규정 준수 비용은 폴리머 공급업체와 폐기물 관리 기업 간의 동맹을 촉진하여 폐쇄형 순환 회수 방안을 시범 운영하게 합니다. EU 기준은 수출 제품 구성에 점점 더 큰 영향을 미치며, 글로벌 생산자들이 제품 안전성과 라벨링을 조화시키도록 강제하고 있습니다.

The Super Absorbent Polymers Market size is estimated at 3.78 Million tons in 2025, and is expected to reach 4.56 Million tons by 2030, at a CAGR of 4.90% during the forecast period (2025-2030).

Enlarging demand in baby diapers, rapid uptake of high-SAP adult incontinence pads, and a widening set of industrial and agricultural applications are the core forces behind this steady expansion. Tightening European regulations that reward bio-based chemistries, together with higher per-capita diaper spend in China and India, are reshaping product portfolios toward premium, high-performance grades. Manufacturers continue to upgrade plants for energy efficiency and vertical integration to buffer acrylic acid price swings. At the same time, direct-to-consumer subscription models and e-commerce-driven cold-chain packaging unlock high-margin niches that compensate for margin pressure in standard hygiene volumes. Rising investment in cellulosic and starch-derived alternatives signals that sustainability now drives both brand value and process innovation in the super absorbent polymers market.

Urban households in China lifted their average diaper outlay by 15% since 2022, aided by policy changes that support larger families and rising disposable income. In India, distribution build-out in tier-2 and tier-3 cities raised penetration, bringing advanced diaper formats within reach of first-time buyers. Premium SKUs contain higher-capacity SAP grades and reduced gel blocking, accelerating unit consumption and value growth across the super absorbent polymers market. Local converters increasingly lock supply via long-term offtake deals to secure quality and mitigate freight risks.

Demographic aging in Japan, South Korea, Germany, and Italy has elevated adult incontinence prevalence, while social acceptance campaigns reduce stigma. New pads integrate up to 40% more SAP, enabling thinner profiles that resemble regular underwear and encourage daytime use. Subscription e-commerce channels are growing, bundling discrete delivery, leakage guarantees, and mobility-specific SKUs. Producers respond with differentiated core-shell particle morphologies that boost absorption under load, creating a high-margin sub-segment within the super absorbent polymers market.

Acrylic acid constitutes up to 70% of production cost, and quarterly swings as wide as 25% destabilize procurement budgets. Changhong Polymer's USD 1.6 billion propane-to-acrylic-acid plant, due in 2026, could lower variable cost curves and unsettle pricing parity among established Western suppliers. Interest in bio-routes and vertical integration rises as boards prioritize feedstock security.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The acrylic fraction represented 72% of the super absorbent polymers market share in 2024, anchored by its proven reliability in baby diapers. To bolster safety perception, premium brands specify higher-purity acrylic SAPs with lower free monomer levels. In parallel, polyacrylamide grades are expanding at a 6.6% CAGR, propelled by their superior water retention in arid agriculture and industrial sealing. Within the super absorbent polymers market size context, polyacrylamide volumes are forecast to add 125 kilotons between 2025 and 2030, capturing incremental share from acrylic grades.

Product developers pursue hybrid networks that mix acrylic and polysaccharide backbones to marry cost and degradability. Nippon Shokubai's biomass-derived SAP line, certified Halal and produced in Indonesia, exemplifies such cross-chemistry innovation. Investment emphasis now tilts toward biomass sourcing logistics, impurity control, and scalable continuous reactor designs that ensure consistent polymer architecture.

Gel polymerization kept a 60% revenue share in 2024, with its reactor trains optimized for high throughput and uniform cross-link density. Energy recovery loops and continuous monomer recycling drive incremental cost competitiveness. Solution polymerization grows at 5% CAGR because it enables small-lot, specialty grades with tight molecular weight distribution and reduced energy load, aligning with sustainability targets.

Suspension and inverse-suspension routes persist in niche roles that require unique particle morphologies, such as core-shell microspheres for medical fluid management. Process engineers focus on precise cross-linker feed control and in-line spectroscopy to tune absorption under load, further segmenting supply within the super absorbent polymers market.

The Super Absorbent Polymer (SAP) Market Segments the Industry by Product Type (Polyacrylamide, Acrylic Acid Based, and Others), Polymerization Process (Solution Polymerization, and More), Application (Baby Diapers, Adult Incontinence Products, and More), End-User Industry (Personal Care and Hygiene Manufacturers, Agriculture Input Suppliers, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Asia-Pacific held 42% of the super absorbent polymers market in 2024, powered by China's integrated acrylic acid-SAP clusters that minimize feedstock logistics. Government incentives, notably in Jiangsu and Shandong, support capacity debottlenecking and export-oriented expansions. India contributes volume growth through broader diaper penetration, while Japan retains a technology leadership niche in specialty and biomass-derived grades.

North America is projected to post the fastest 5.50% CAGR through 2030. Growth arises from premium diaper SKUs, high-SAP adult incontinence adoption among aging baby boomers, and specialized industrial uses such as fracking water blockers and cold-chain pads. Research consortia with land-grant universities pioneer cellulosic and protein-based networks, aligning corporate sustainability pledges with regulatory trends. The region also records early field use of hemp-based SAP in horticulture, reinforcing circular economy narratives within the superabsorbent polymers market.

Europe's stringent policy climate accelerates bio-based uptake and packaging recyclability. Germany leads production volume, whereas Nordic countries drive consumer preference for compostable diaper cores. Compliance costs spur alliances between polymer suppliers and waste-management firms to pilot closed-loop recovery schemes. EU standards increasingly influence export formulations, compelling global producers to harmonize product safety and labeling.