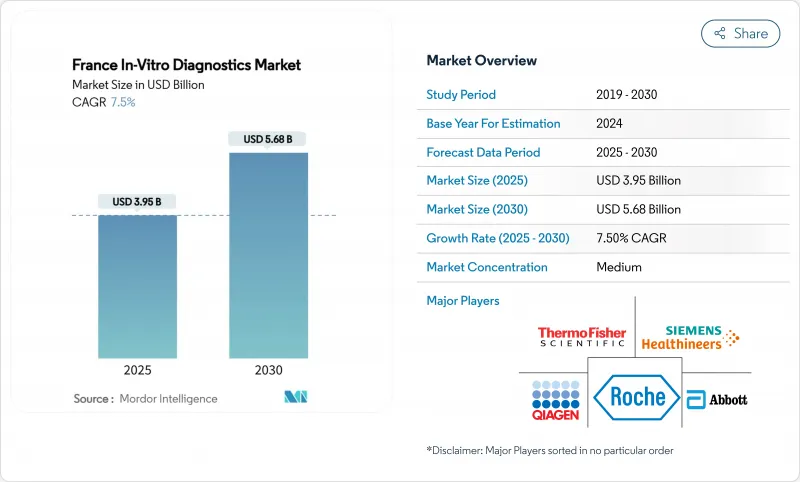

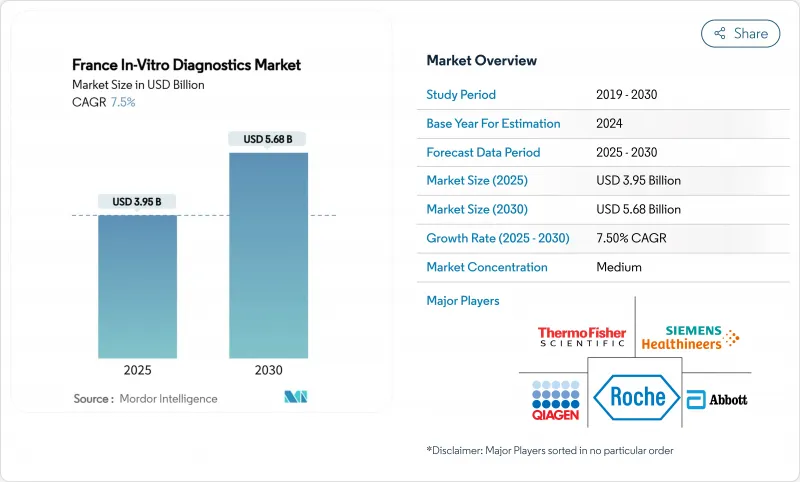

프랑스의 체외진단 시장 규모는 2025년에 39억 5,000만 달러로 평가되었고, 2030년에 56억 8,000만 달러에 이를 것으로 예측되며, 예측기간의 CAGR은 7.5%를 나타낼 전망입니다.

진단 검사는 임상 결정의 약 70%를 뒷받침하며 만성 질환 사례 증가와 예방 의료 모델 확대로 그 중요성이 지속적으로 부각되고 있습니다. 유럽연합 체외진단규정(IVDR)에 따른 규제 강화로 승인 주기는 길어지고 있으나, 가시적인 품질 향상을 이끌고 있습니다. 특히 투자자 지원 체인 간 실험실 통합은 검사량을 고처리량 허브로 집중시키는 반면, 가정용 검사 플랫폼은 환자 접근성을 확대하고 있습니다. 공급업체들이 처리 시간 단축, 정확도 향상, 데이터 통합을 추구함에 따라 기술 융합(자동화, 인공지능, 디지털 연결성)은 여전히 핵심 경쟁 요소로 자리 잡고 있습니다.

프랑스의 고령화 추세와 복합질환 증가로 인해 화학, 면역분석, 분자 패널 전반에 걸쳐 검사 항목이 확대되고 있습니다. 65세 이상 인구 비율은 2050년까지 29%에 달할 것으로 예상되어 높은 진단 수요가 지속될 전망입니다. 감염병 패널은 여전히 응용 매출의 30.2%를 차지하며, 이는 코로나19 위기 이후의 경계심을 반영합니다. 항생제 내성 감시는 병원체와 내성 표지자를 며칠이 아닌 몇 시간 내에 식별하는 신속 분자 검사의 도입을 가속화하고 있습니다. 예방적 선별 프로그램은 검사를 일상 진료 경로에 통합하여 국가 실험실 및 지역사회 환경 전반의 검사량을 추가로 증가시키고 있습니다.

정책 입안자들은 명확한 임상적 유용성을 제공하는 검사에 보상을 제공하는 ‘증거 기반 보장’ 제도로 전환하고 있습니다. 동반진단(CDx)이 가장 먼저 혜택을 보며, 표적 치료 시작 전 바이오마커 확인이 필요한 정밀 암 치료 요법과 연계됩니다. 정부 보험 적용은 선별된 디지털 진단까지 확대되어 검사 플랫폼과 전자건강기록 간의 상호운용성을 촉진합니다. 이러한 환경은 혁신을 장려하는 동시에 공급업체가 실제 임상 결과 개선을 입증하도록 유도합니다.

IVDR은 위험 기반 기기 분류와 강력한 임상 증거 서류를 요구하여 혁신적 검사의 승인 주기를 연장합니다. 2024년 7월 개정안은 공급 부족 시 의무적 통보 및 단계적 Eudamed 등록을 추가하여 행정적 부담을 더욱 가중시켰습니다. 제조업체의 70% 이상이 규제 기능에 자원을 재배치하면서 제품 출시가 지연되고 전환 기간 동안 검사 가용성이 제한될 가능성이 있습니다.

면역 진단은 일상적인 호르몬, 자가면역 및 감염성 질환 패널에서의 역할에 힘입어 2024년 프랑스 체외 진단 시장 점유율의 28%를 차지했습니다. 대규모 설치된 분석기 기반과 시약 연계로 안정적인 수요가 보장됩니다. 분자 진단 시장은 2025년부터 2030년까지 연평균 9.5% 성장률(CAGR)을 기록할 전망이며, 종양학, 감염성 질환, 유전성 질환 관리 분야로 점차 확대되고 있습니다. 플랫폼 트렌드는 다중 PCR 및 차세대 시퀀싱을 선호하여 결과 도출 시간을 며칠에서 몇 시간으로 단축시키고 있습니다. BIOFIRE SPOTFIRE와 같은 통합 장치는 여러 호흡기 표적 검사를 단일 카트리지로 통합하여 증후군 패널로의 전환을 강조합니다. 임상 화학, 혈액학 및 응고 검사는 여전히 병원의 핵심 지표를 제공하지만, 상품화된 가격 정책으로 인해 분자 검사 대비 수익 성장률은 뒤처진다. 현장진단용 카트리지는 분산된 수요를 해결하며 응급 및 외래 환경에서의 접근성을 확대합니다.

정밀의학에 대한 강조가 증가함에 따라 실행 가능한 유전체 변이를 식별하는 동반진단(CDI)이 추진되고 있습니다. 실험실들은 자동화 추출 및 라이브러리 준비 스테이션을 도입하여 인력 증가 없이 증가하는 검체 수를 처리하고 있습니다. 이러한 도입은 면역분석법이나 현미경 검사로 관찰되던 질환까지 포함해 분자 검사의 주류화 추세를 공고히 합니다. 결과적으로 프랑스 체외진단 시장은 분자진단학이 전체 지출에서 점유율을 점차 확대하며 수익 구성의 재조정이 예상됩니다.

2024년 프랑스 체외진단 시장에서 시약 및 키트는 65.5%를 차지했으며, 이는 임상 검사의 소모품 기반 경제성을 반영합니다. 민감도 개선이 입증된 독점적 화학 기술은 특히 바이러스 부하 및 종양학 패널 분야에서 프리미엄 가격을 유지합니다. 기기는 낮은 점유율을 보이지만 장기적인 고객 확보의 기반이 되며, 분석기 선택이 향후 시약 공급망을 결정하기 때문입니다. 2030년까지 연평균 12.1% 성장할 것으로 예상되는 소프트웨어 및 서비스는 실험실에 분석, 품질 관리 대시보드, AI 기반 의사 결정 지원을 제공합니다. 의료 네트워크는 분석기 출력과 병원 정보 시스템을 연결하는 상호운용성 미들웨어에 자본을 배분하여 물리적 하드웨어 공급을 넘어 공급업체 관계를 강화합니다.

서비스 계약은 이제 원격 모니터링, 예측 유지보수, 워크플로우 최적화 컨설팅을 묶어 제공합니다. 이러한 변화로 솔루션 공급업체는 단순한 장비 공급업체가 아닌 비용 절감 및 규제 준수 분야의 파트너로 자리매김합니다. 결과적으로 소프트웨어 수익은 주기적인 자본 지출을 완충하여 공급업체의 현금 흐름을 안정화하고 프랑스 체외진단 시장에서 고객 생애가치를 전반적으로 높입니다.

The France in vitro diagnostics market size stands at USD 3.95 billion in 2025 and is projected to reach USD 5.68 billion by 2030, translating to a 7.5% CAGR over the forecast period.

Diagnostic testing underpins roughly 70% of clinical decisions and continues to gain relevance as chronic disease cases rise and preventive-care models expand. Regulatory tightening under the European Union's In Vitro Diagnostic Regulation (IVDR) is lengthening approval cycles yet driving demonstrable quality gains. Laboratory consolidation, especially among investor-backed chains, is steering volumes toward high-throughput hubs while home-based testing platforms widen patient access. Technology convergence-automation, artificial intelligence, and digital connectivity-remains the pivotal competitive lever as suppliers look to improve turnaround time, accuracy, and data integration.

France's aging profile and rising multimorbidity are enlarging test menus across chemistry, immunoassay, and molecular panels. The share of citizens aged >=65 is projected to reach 29% by 2050, sustaining high diagnostic demand. Infectious disease panels still represent 30.2% of application revenues, reflecting vigilance after the COVID-19 crisis. Antimicrobial-resistance surveillance is accelerating the uptake of rapid molecular assays that identify pathogens and resistance markers in hours rather than days. Preventive screening programs embed testing into routine care pathways, further lifting volumes across national laboratories and community settings.

Policy makers are moving toward 'coverage-with-evidence' schemes that reward assays delivering clear clinical utility. Companion diagnostics benefit first, aligning with precision oncology regimens that require biomarker confirmation before targeted therapy initiation. Government reimbursement also extends to select digital diagnostics, incentivizing interoperability between test platforms and electronic health records. This environment encourages innovation while nudging suppliers to prove real-world outcome gains.

The IVDR imposes a risk-based device classification and robust clinical-evidence dossier, stretching approval cycles for innovative assays. July 2024 amendments added mandatory supply-shortage notifications and phased Eudamed registration, further intensifying administrative load. More than 70% of manufacturers have redirected resources to regulatory functions, delaying product launches and potentially limiting test availability during the transition period.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Immuno Diagnostics secured 28% of the France in vitro diagnostics market share in 2024, supported by its role in routine hormone, autoimmune, and infectious-disease panels. Large installed analyzer bases and reagent tie-ins ensure stable demand. Molecular Diagnostics, projected to expand at a 9.5% CAGR between 2025 and 2030, increasingly permeates oncology, infectious disease, and hereditary-disease management. Platform trends favor multiplex PCR and next-generation sequencing, shrinking turnaround time from days to hours. Integrated devices such as BIOFIRE SPOTFIRE consolidate multiple respiratory targets into a single cartridge, underscoring the shift toward syndromic panels. Clinical Chemistry, Hematology, and Coagulation continue to provide core hospital metrics, though revenue growth trails molecular assays because of commoditized pricing. Point-of-care cartridges address decentralized needs, broadening access in emergency and outpatient contexts.

Growing emphasis on precision medicine propels companion diagnostics that identify actionable genomic alterations. Laboratories adopt automated extraction and library-prep stations to handle rising sample numbers without proportionate staff increases. This adoption cements molecular testing's trajectory toward mainstream use, even for conditions historically monitored by immunoassay or microscopy. As a result, the France in vitro diagnostics market expects a rebalanced revenue mix, with molecular diagnostics capturing a progressively larger slice of overall spending.

Reagents & Kits captured 65.5% of the France in vitro diagnostics market in 2024, reflecting the consumables-based economics of clinical testing. Proprietary chemistries with demonstrated sensitivity improvements preserve premium pricing, especially in viral-load and oncology panels. Instruments deliver lower share yet underpin long-term customer lock-in, as analyzer selection dictates future reagent pipelines. Software & Services, growing at 12.1% CAGR to 2030, provide laboratories with analytics, quality-control dashboards, and AI-driven decision support. Healthcare networks allocate capital toward interoperable middleware that bridges analyzer outputs and hospital information systems, reinforcing vendor relationships beyond physical hardware supply.

Service contracts now bundle remote monitoring, predictive maintenance, and workflow optimization consulting. This shift positions solution providers as partners in cost containment and regulatory compliance rather than mere equipment vendors. Consequently, software revenues buffer cyclical capital spending, smoothing supplier cash flows and elevating overall customer lifetime value within the France in vitro diagnostics market.

The France In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, and More), Product & Service (Instrument, and More), Specimen (Blood, Urine, and More), Test Setting (Centralised Laboratory Testing, and More), Application (Infectious Disease, Diabetes and More), and End-Users (Independent Diagnostic Laboratories, and More). The Market Forecasts are Provided in Terms of Value (USD).