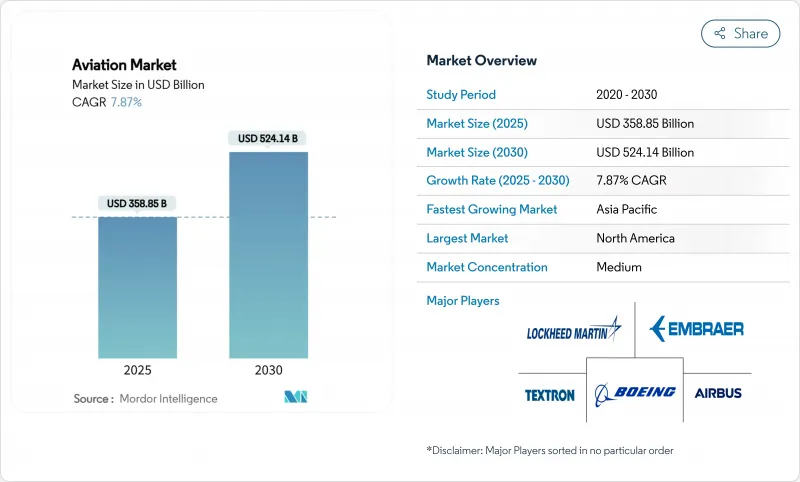

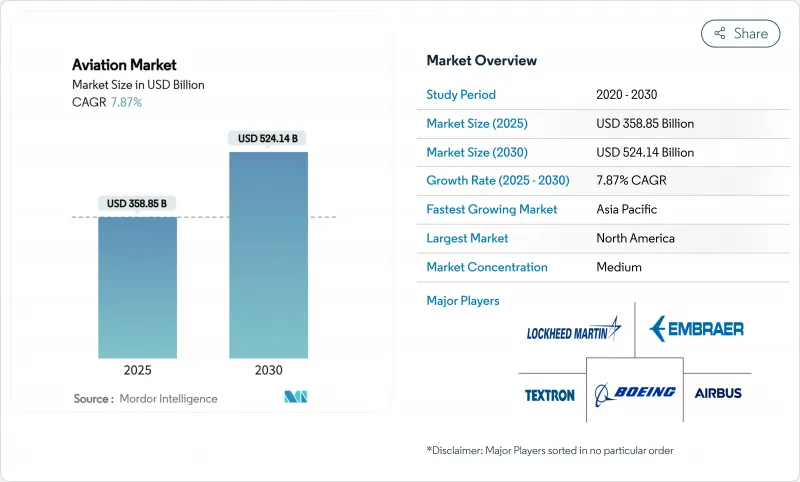

항공 시장의 2025년 시장 규모는 3,588억 5,000만 달러에 이르고, 2030년에는 5,241억 4,000만 달러로 확대되며, CAGR은 7.87%를 나타낼 전망입니다.

항공 시장은 여객 수요 회복, 항공기 현대화의 가속화, 지속 가능한 추진력에 대한 관민의 기록적 투자로부터 이익을 얻고 있습니다. 항공사와 제조업체는 연료 효율적인 항공기, 고급 디지털 유지 보수 및 배출량을 줄이고 단가를 낮추는 대체 동력원을 우선함으로써 단순한 생산 능력 확대에서 가치 최적화로 방향타를 끊고 있습니다. 항공 시장은 또한 전용화물 운송량을 증가시키는 전자상거래량의 급증, 지속가능한 항공연료(SAF) 도입에 박차를 가하는 정부의 넷제로 의무화, 전기항공기의 신규 진입에 의한 경쟁의 격화에 의해서도 형성되고 있습니다. 특히 배터리 및 수소 등 자동차 및 에너지 분야와의 기술 융합은 복잡한 인증 경로와 공급망 리스크를 관리할 수 있는 이해관계자들에게 비즈니스 기회를 더욱 확대하고 있습니다.

항공사는 차세대 내로우 바디 패밀리가 약속하는 20-30%의 연료 소비 삭감을 실현하기 위해 레거시 플릿의 교체를 예정보다 빨리 하고 있습니다. 항공 시장은 현재 제트 연료 변동에 대한 전략적 헤지로서 연비 효율을 평가했습니다. 신형기의 예지보전시스템은 예정외의 다운타임을 삭감해, 객실의 업그레이드는 좌석당의 안실러리 수입을 증가시킵니다. 저비용 캐리어와 레거시 플래그 캐리어 모두 신형 장비가 낮은 부하율로 수익성이 뛰어난 얇은 노선을 가능하게 하고 세계 네트워크 설계를 재구축하기 때문에 경쟁 압력 증가에 직면하고 있습니다.

IATA의 2025년 전망에 따르면, 여객 수송량은 2043년까지 매년 4.7% 증가하지만, APAC만으로 그 절반 이상을 견인합니다. 중국 항공사는 2043년까지 장비를 두배로 늘렸으며 인도 국내 시장은 이제 세계 3위를 차지하고 있습니다. 아프리카의 연간 성장률은 6.4%로, 인프라 제약이 작고 연비가 좋은 유형에 투자를 유도하는 가운데 1,170대의 신조기 수요가 뒷받침됩니다. 성숙한 지역은 2024년에는 1조 5,000억 달러로 회복하는 기업 출장비를 배경으로 유행 전 프리미엄 캐빈 수요를 회복했습니다.

기체와 엔진의 OEM은 주조품, 단조품, 아비오닉스 칩의 부족과 격투하고 있으며, 납기를 6-18개월 연장하고 있습니다. 보잉에 의한 스피릿 에어로시스템의 인수(47억 달러)는 중요한 동체 부분의 관리를 되찾기 위해 이용되는 수직 통합의 상징입니다. 항공사는 오래된 항공기를 길게 유지함으로써 대응하고, 유지 보수 비용을 팽창시키고, 항공 시장의 단기적인 궤도의 부족으로 생산 능력의 성장을 억제하고 있습니다.

민간항공은 세계적인 여객 수송량의 정상화와 가격 결정력을 회복시키는 목표 용량 규율에 힘입어 2024년 항공 시장에서 61.56%의 점유율을 유지했습니다. 민간 항공의 항공 시장 규모는 CAGR 6.90%로 2025년 2,210억 달러에서 2030년 3,089억 달러로 성장할 것으로 예측됩니다. 네트워크 항공사는 보다 효율적인 내로우 바디로 축발을 옮기는 한편, 저렴한 항공사는 국경을 넘은 레저 수요를 개척하기 때문에 평균 스테이지 길이를 꾸준히 끌어올리고 있습니다.

첨단 항공 모빌리티(AAM)는 업계에서 가장 파괴적인 벡터를 보여주며, 지자체가 버티포트 프레임워크를 승인하고 1세대 eVTOL 프로토타입이 의미 있는 비행 시간을 기록함에 따라 2030년까지 연평균 복합 성장률(CAGR)은 18.90%를 나타낼 전망입니다. 2026년까지 조비 서비스를 시작하는 두바이의 계획은 도시 지역의 에어 택시를 복합 교통망에 통합하려는 움직임을 보여줍니다. 현재 AAM의 수익은 극히 적지만, 높은 성장률로 인해 기존 기업은 미래의 관련성을 유지하기 위해 소수 주식과 합작 투자에 투자해야합니다.

터보 팬 엔진은 2024년 항공 시장 규모의 52.67%를 차지하며 A320neo와 B737 MAX의 활발한 프로그램에 의해 지원되었습니다. LEAP 및 GTF 엔진 제품군은 항공사가 2자리 연료 절감을 평가하는 동안 2자리 수주를 견인합니다. 그러나 전기 추진은 CAGR 15.76%로 확대되고 있으며, 배터리의 질량 트레이드 오프가 실현 가능한 200nm 미만의 지역 부문에 우선 초점을 맞추었습니다.

NASA의 전기 추진 비행 실증 프로그램은 산업계 파트너와 함께 2030년까지 상업 서비스 진출을 목표로 하고 있습니다. GE 에어로스페이스는 차세대 전기기계를 제조하는 적층조형라인에 2025년 10억 달러를 할당합니다. 하이브리드 전기 시스템은 오늘날의 항속 거리 제한을 채우는 것으로, 터보 제너레이터 세트와 배터리 팩을 결합하여 400nm 섹터에서 연료 소비를 30% 절감할 수 있습니다.

북미의 항공 시장 규모는 2025년에 1,348억 달러로, 2030년에는 CAGR 5.4%로 1,753억 달러로 확대됩니다. 미국은 B737 MAX 회복, T-7A 트레이너 방어 백로그 확대, 9,600대 등록 민간 제트기의 애프터마켓 수익을 활용하여 이 가치의 대부분을 견인합니다. 퀘벡과 온타리오에 위치한 캐나다 항공우주 허브는 특히 수소 저장 및 연료전지 시험 등 지역의 추진력 연구를 다양화하고 있습니다. 멕시코의 자유 무역 지역은 와이어 하네스와 인테리어의 Tier2 공급업체를 유치하여 공급 체인의 탄력성을 향상시킵니다.

아시아태평양은 2025년부터 2030년 사이에 885억 달러의 부가가치를 창출하고 주요 블록 중 가장 빠른 성장을 반영합니다. 중국의 민간 항공국은 C919의 형식 증명의 검증을 간소화하고 인도 공항 공단은 지하철 혼잡을 완화하기 위한 그린필드 개발에 118억 달러를 기록합니다. 일본의 전기 지역 항공기 벤처 및 호주 퀸즐랜드 주 SAF 허브는 항공 시장의 발자국을 더욱 확대합니다. 태국과 베트남과 같은 ASEAN 지역은 전자상거래 붐 속에서 아시아 지역의 물류 회랑에 취항하기 위해 A321의 여객기에서 화물기로의 개조를 채택하여 화물 중심 모델로 축 발을 옮깁니다.

유럽은 CAGR 6.1%와 균형 잡힌 성장 궤도를 유지하고 있으며, 와이드 바디의 A350 슬레이트 연장을 지원하는 에어버스의 함부르크와 툴루즈의 생산 증강에 지지되고 있습니다. 이 대륙은 또한 2025년에 2%의 SAF를 의무화하고 2050년까지 70%로 인상하겠다는 구속력 있는 정책을 처음으로 제안하고 지역 항공사에 장기적인 인수계약 체결을 촉구하고 있습니다. 동유럽의 저렴한 항공사는 장비를 확장하고 2선 공항에 새로운 앞치마와 정비장에 대한 투자를 촉구합니다. 보고타에서 리마까지 공항이 244억 달러의 근대화 프로젝트를 진행해 내로우 바디기의 발착 범위를 확대했습니다.

중동 및 아프리카를 합친 항공 시장 규모는 2025년 476억 달러, 2030년 702억 달러로 확대될 것으로 예상됩니다. 걸프 항공사는 유행(세계적 유행) 시대에 얻은 이익을 A350 및 B777X 주문에 재투자하고, 아프리카 항공사는 양자 간 협정을 조화시키는 단일 아프리카 항공 운송 시장의 혜택을 받습니다. 에어버스는 아프리카의 민간 항공기가 2025년 1,250대에서 2043년까지 2,650대로 급증하여 아프리카 대륙에서 가장 혼잡한 20개 지역 내 노선에서 연결성 성장이 가능할 것으로 예측했습니다.

The aviation market is valued at USD 358.85 billion in 2025 and will expand to a market size of USD 524.14 billion by 2030, reflecting a 7.87% CAGR.

The aviation market benefits from renewed passenger demand, accelerated fleet modernization, and record public- and private-sector investment in sustainable propulsion. Airlines and manufacturers are pivoting from sheer capacity growth to value optimization by prioritizing fuel-efficient aircraft, advanced digital maintenance, and alternative power sources that cut emissions and lower unit costs. The aviation market is also shaped by surging e-commerce volumes that lift dedicated cargo traffic, governmental net-zero mandates that spur sustainable aviation fuel (SAF) uptake, and intensified competition from new electric-aircraft entrants. Technology convergence with the automotive and energy sectors, particularly around batteries and hydrogen, further widens the opportunity set for stakeholders that can manage complex certification pathways and supply-chain risk.

Airlines are replacing legacy fleets earlier than planned to lock in 20-30% fuel-burn savings promised by next-generation narrow-body families. The aviation market now prices fuel efficiency as a strategic hedge against volatile jet fuel, which can equal 30% of total airline costs. Predictive maintenance suites in new aircraft reduce unplanned downtime, while cabin upgrades lift ancillary revenue per seat. Low-cost carriers and legacy flag carriers alike face rising competitive pressure as newer fleets enable profitable thin routes at lower load factors, reshaping global network design.

IATA's 2025 outlook indicates aggregate passenger traffic growing 4.7% annually through 2043, yet APAC drives more than half that increment alone. Chinese carriers will double their fleets by 2043, and India's domestic market is now the world's third-largest. Africa's annual growth rate of 6.4% underpins demand for 1,170 new aircraft even as infrastructure constraints channel investment toward smaller, fuel-efficient types. Mature regions regain pre-pandemic premium-cabin demand, with corporate travel spend rebounding to USD 1.5 trillion in 2024.

Airframe and engine OEMs still wrestle with shortages in castings, forgings, and avionics chips, extending delivery schedules by 6-18 months. Boeing's USD 4.7 billion purchase of Spirit AeroSystems is emblematic of vertical integration used to regain control over critical fuselage sections. Airlines respond by keeping older aircraft longer, inflating maintenance spend, and dampening capacity growth-a drag on the aviation market's near-term trajectory.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Commercial aviation retained a 61.56% share of the aviation market in 2024, supported by global passenger traffic normalization and targeted capacity discipline that restores pricing power. The aviation market size for commercial aviation is projected to grow from USD 221.0 billion in 2025 to USD 308.9 billion in 2030 at a 6.90% CAGR. Network carriers pivot toward more efficient narrow-bodies, while low-cost carriers steadily raise average stage length to tap cross-border leisure demand.

Advanced air mobility (AAM) represents the industry's most disruptive vector, clearing 18.90% CAGR through 2030 as municipalities approve vertiport frameworks and first-generation eVTOL prototypes log meaningful flight hours. Dubai's plan to launch Joby services by 2026 illustrates the push to integrate urban air taxis into multimodal transport grids. Although current AAM revenue is minimal, its high growth rate compels incumbents to invest in minority stakes or joint ventures to preserve future relevance.

Turbofan engines held 52.67% of the aviation market size in 2024, buoyed by the prolific A320neo and B737 MAX programs. LEAP and GTF engine families drive double-digit order books as airlines prize double-digit fuel savings. Yet, electric propulsion is scaling at 15.76% CAGR, focusing first on sub-200 nm regional segments where battery mass trade-offs are feasible.

NASA's Electric Propulsion Flight Demonstration program with industry partners targets commercial-service entry by 2030. GE Aerospace allocates USD 1 billion in 2025 to additive manufacturing lines that will produce next-generation electrical machines. Hybrid-electric systems bridge today's range limitations, combining turbogenerator sets with battery packs to cut fuel burn 30% on 400 nm sectors-a pathway sustains turbofan supply chains while advancing electrification.

The Aviation Market Report is Segmented by Type (Commercial Aviation, Military Aviation, General Aviation, Unmanned Aerial Systems, and Advanced Air Mobility), Propulsion Technology (Turboprop, Turbofan, Piston Engine, and More), Power Source (Conventional Fuel, Fuel Cell, and More), Fit (Line Fit, and Retrofit), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America's aviation market size was USD 134.8 billion in 2025 and will advance to USD 175.3 billion by 2030 at a 5.4% CAGR. The United States drives most of this value, leveraging B737 MAX recovery, an expanding defense backlog for the T-7A trainer, and aftermarket revenue from a fleet of 9,600 registered commercial jets. Canada's aerospace hubs in Quebec and Ontario diversify regional propulsion research, especially in hydrogen storage and fuel-cell testing. Mexico's free-trade zones attract tier-2 suppliers for wiring harnesses and interiors, improving supply-chain resilience.

Asia-Pacific adds USD 88.5 billion of incremental value between 2025 and 2030, reflecting the fastest growth among major blocs. China's Civil Aviation Administration simplifies type-certificate validation for the C919, while India's Airports Authority earmarks USD 11.8 billion in green-field developments to alleviate metro congestion. Japan's electrified regional-aircraft venture and Australia's SAF hub in Queensland further enlarge the aviation market footprint. ASEAN regionals such as Thailand and Vietnam pivot to cargo-focused models amid e-commerce booms, employing passenger-to-freighter conversions of A321s to serve intra-Asia logistics corridors.

Europe maintains a balanced growth trajectory at 6.1% CAGR, underpinned by Airbus's Hamburg and Toulouse production ramp that supports widebody A350 slate extensions. The continent is also the first to propose a binding 2% SAF mandate in 2025, rising to 70% by 2050, pressuring regional airlines to sign long-term offtake deals. Eastern European low-cost carriers enlarge their fleets, encouraging second-line airports to invest in new aprons and maintenance bays. South America rebounds as low-cost penetration exceeds 40% of passenger volumes, with airports from Bogota to Lima advancing USD 24.4 billion in modernization projects that unlock additional slots for narrowbody aircraft.

The Middle East and Africa contributed a combined aviation market size of USD 47.6 billion in 2025, climbing to USD 70.2 billion by 2030. Gulf carriers reinvest pandemic-era windfalls into A350 and B777X orders, while African carriers benefit from the Single African Air Transport Market, which harmonizes bilateral agreements. Airbus projects the African commercial fleet to surge from 1,250 aircraft in 2025 to 2,650 by 2043, enabling connectivity growth on the continent's 20 busiest intra-regional routes.