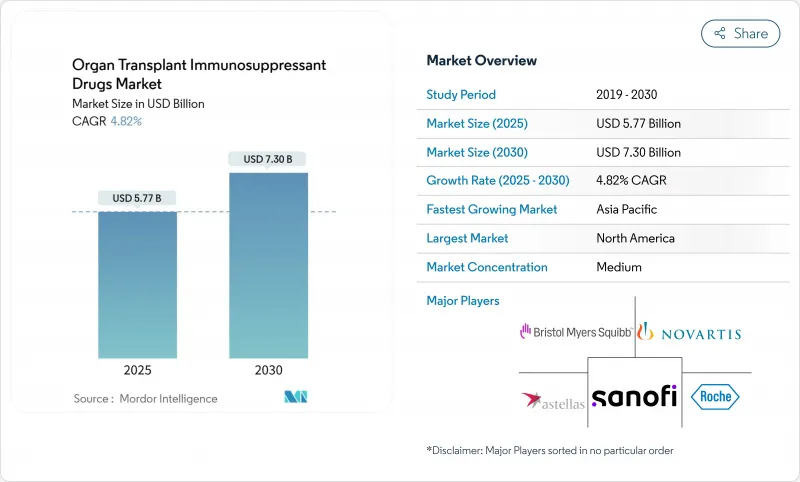

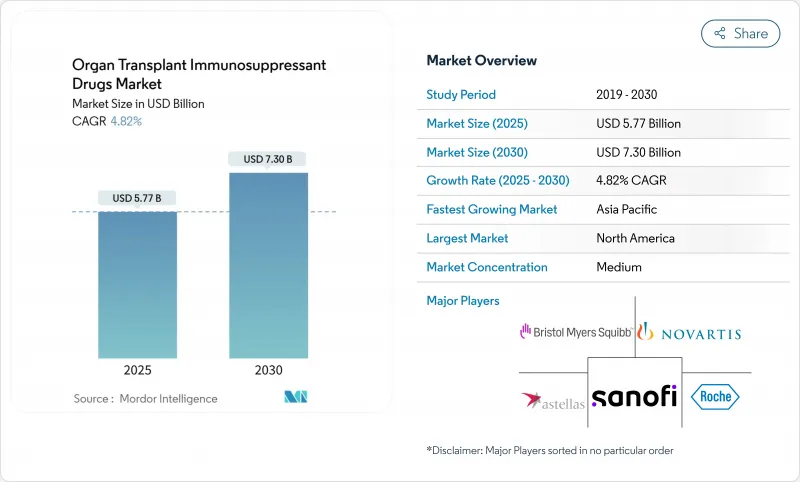

장기 이식 면역억제제 시장은 2025년에 57억 7,000만 달러로 평가되고, 2030년에는 73억 달러에 이르며, CAGR 4.82%를 나타낼 것으로 예측됩니다.

견조한 이식 건수, 기록적인 장기 제공의 이정표, 지속적인 프로토콜의 업그레이드가 확대를 지원하고 있습니다. 비용 절감이 가능한 제네릭 의약품의 승인이 가속되어 환자에 대한 접근이 확대되는 한편, 네프론 온존 요법이나 생체외 관류 기술이 임상 성과를 향상시킵니다. 디지털 제형 채널, 정밀 진단, AI 가이드 하 투여는 비용 압력과 기증자 부족의 격화에도 불구하고 수요를 더욱 강화합니다. 북미는 판매량의 리더를 유지하고 있지만, 아시아태평양의 급속한 프로그램 구축은 지리적 역학을 재정의하고 있으며, 장기 이식 면역억제제 시장을 10년을 통해 1자리대 중반의 지속적인 성장으로 끌어올리고 있습니다.

말기 신장, 간, 심장, 폐 질환 증가로 수술 건수가 증가하고, 따라서 면역억제제의 사용량도 증가하고 있습니다. 3,700만명 이상의 미국인이 만성 신장병을 앓고 있으며, COVID-19는 간의 이환율을 악화시키고 있습니다. 노화로 인해 후보자가 늘어나고 노인 환자는 면역 회복력이 떨어지기 때문에보다 집중적인 요법이 필요합니다. 조기 진단은 장기 부전을 조기에 발견하고, 한때는 손이 닿지 않는 것으로 되어 있던 이식 파이프라인에 공급됩니다. 인공지능 매칭 시스템은 현재 98%의 정확도로 적합성을 예측하고, 거부 반응을 감소시키고, 투여 프로토콜을 최적화함으로써 수요 사이클을 강화하고 있습니다.

다수의 타크로리무스와 미코페놀산 모페틸의 제네릭 의약품을 채택하면 처방 비용이 절감되고, 자금제공 기관은 일정 예산 내에서 더 많은 수령인을 치료할 수 있습니다. 잇따르는 제네릭 의약품의 발매로 메디케어 파트 D의 주요 약제에 대한 지출은 48-67% 감소했고, 바로 사용할 수 있는 경구 현탁액은 소아에 대한 접근을 확대했습니다. 그럼에도 불구하고 FDA는 최근 어코드의 타크로리무스 1 로트를 BX로 평가하여 생물학적 동등성에 대한 경계를 강조하고 있습니다. 가격 완화는 약물 비용이 수술 후 어드히어런스의 주요 병목이 된 신흥 국가에서 특히 중요합니다.

미국 간 수혜자 1인당 연간 치료비는 3만 달러를 초과했으며, 지불자와 환자 모두에게 부담이 되고 있습니다. 메디케어 보험은 수술 후 3년 후에 만료되기 때문에 중고년 수령인의 32%는 충분한 약 보험에 가입하지 않았습니다. 합병증에 의한 입원은 의료 시스템의 비용을 더욱 부풀리게 하기 위해 공적 상환을 확대해야 한다는 목소리가 높아지고 있습니다. 저·중소득국에서는 자기부담이 많기 때문에 투여량을 절약할 수밖에 없는 경우가 많아 치료성적이 손상되어 장기 이식 면역억제제 시장의 확대가 억제되고 있습니다.

칼시뉴린 억제제는 2024년에 34.55%의 매출을 유지해 장기 이식 면역억제제 시장을 지원했습니다. 타크로리무스와 같은 입증 된 약물은 대부분의 이식편 유형에서 첫 번째 선택 약물입니다. 그러나 mTOR 억제제는 네프론 온존 효과와 심장 대사 개선 효과로 CAGR 10.25%의 궤도를 타고 있습니다. 간 이식 후 12개월 이내에 에베롤리무스로 조기 변경하여 55% 환자에서 신장 기능이 개선되었습니다. 라파마이신 기반 4가지 병용 요법은 20년 이식편 생존율 20.9%를 달성하여 타크로리무스의 벤치마크를 능가했습니다. 베라타셉트와 같은 공자극 차단제나 미코페놀산과 같은 항증식제가 치료의 골격을 이루고 있습니다.

새로운 전달 시스템이 성장을 가속합니다. 자기 조직화 라파마이신 나노입자는 혈장 농도를 유지하며, 전신 독성은 낮고, PEG화된 CD28 표적 단편(VEL-101)은 2상까지 진행하고 있습니다. 제네릭 의약품의 보급이 진행되고 특허가 끊어짐에 따라 가격 경쟁은 격화되지만, 타겟을 좁힌 제제나 국소에 특화된 제제의 기술 혁신에 의해 마진 압력은 상쇄되어 장기 이식 면역억제제 시장의 중기적인 성장 전망은 더욱 강해질 것으로 보입니다.

2024년 장기 이식 면역억제제 시장 규모는 성숙한 프로토콜과 높은 유병률을 뒷받침하며 신장이식이 계속 61.53%를 차지했습니다. 그러나 폐 이식의 CAGR은 10.15%를 나타낼 전망입니다. 상온 생체외 관류는 한계에 도달한 폐를 이식 가능한 상태로 상승시켜 순환 사후 헌체 코호트에서 1차 이식편의 기능 장애를 해소합니다. 심장 이식 프로그램에서는 급성 기능 부전 시 정맥·동맥 ECMO 백업이 활용되어 1년 생존율이 향상되고 있습니다. 간과 췌장의 이식량은 꾸준히 확대되지만 진화하는 비 수술적 질병 관리 옵션과의 경쟁에 직면하고 있습니다. 줄기세포 이식과 혈관내 복합이식편은 개별적인 면역조절을 채용하고, 보다 넓은 장기 이식 면역억제제 시장 중에서 장래에 틈새 시장에 대한 수요가 예상됩니다.

이종이식 실험이 성공하면 유지요법의 필요성이 저하되거나 인간 이식편의 한계가 계속되면 새로운 도입 틈새가 생길 수 있습니다.

북미는 4만 6,000건의 이식과 종합적인 지불자 부담을 배경으로 2024년 매출의 42.72%를 차지했습니다. 미국은 제네릭 의약품의 대체가 진행되고 있음에도 불구하고 타크로리무스 사용률이 높고 캐나다는 기계 관류를 조기에 도입했기 때문에 판매량이 더욱 증가했습니다. 유럽은 균형 잡힌 성장을 유지하고 있지만, 상환 개혁과 국경을 넘어서는 하모나이제이션의 논의가 소규모 회원국의 접근을 형성하고 있습니다.

아시아태평양은 CAGR 9.22%에서 가장 급성장하고 있습니다. 중국의 국영 이식 네트워크, 인도의 2023년 신장 수술 건수 1만 3,426건, 일본 이식 후 CMV에 대한 리브텐시티의 승인은 모두 그 기세를 나타냈습니다. 규제의 명확화, 기증자 등록의 전자화, 보험 제도의 확충은 2030년까지 장기 이식 면역억제제 시장에서 이 지역의 점유율을 높이는 구조적 변화를 보여줍니다.

남미와 중동 및 아프리카는 아직 개발 도상이지만 전략적인 지역입니다. 브라질의 확립된 간·신장 센터가 남미의 진보를 지지해, 사우디아라비아와 남아프리카가 관류 시스템 도입의 선진을 끊고 있습니다. 제한된 공여자 풀과 자금 조달의 제약이 보급을 억제하고 있지만, 겨냥한 관민 파트너십으로 인해 장기 이식 면역억제제 시장은 예측 기간 후반에 추가 기회를 잡을 수 있습니다.

The organ transplant immunosuppressant drugs market is valued at USD 5.77 billion in 2025 and is forecast to reach USD 7.30 billion by 2030, advancing at a 4.82% CAGR.

Steady transplant volumes, record organ-donation milestones, and continual protocol upgrades underpin expansion. Accelerated approvals of cost-saving generics broaden patient access, while nephron-sparing regimens and ex vivo perfusion technologies sharpen clinical outcomes. Digital dispensing channels, precision diagnostics, and AI-guided dosing further reinforce demand despite intensifying cost pressures and donor shortages. North America retains volume leadership, but Asia-Pacific's rapid program build-outs are redefining geographic dynamics, lifting the organ transplant immunosuppressant drugs market toward sustained mid-single-digit growth through the decade.

Escalating incidences of end-stage kidney, liver, heart, and lung diseases fuel surgery volumes and, by extension, immunosuppressant uptake. More than 37 million Americans live with chronic kidney disease, while COVID-19 exacerbated liver morbidity. Aging demographics deepen the candidate pool and require more intensive regimens because older patients possess diminished immune resilience. Early diagnostics flag organ failure sooner and feed transplant pipelines once deemed unreachable. Artificial-intelligence matching systems now predict compatibility with 98% accuracy, lowering rejection events and optimizing dosing protocols, thereby creating reinforcing demand cycles.

Uptake of multiple tacrolimus and mycophenolate mofetil generics slashes regimen costs, allowing funding bodies to treat more recipients within fixed budgets. Medicare Part D outlays for key drugs fell 48-67% after successive generic launches, and ready-to-use oral suspensions widened pediatric access. Nonetheless, the FDA's recent BX rating on an Accord tacrolimus lot highlights vigilance over bioequivalence. Price relief is especially pivotal in emerging economies, where drug expenditure remains the primary bottleneck to post-surgery adherence.

Annual therapy expenses exceeding USD 30,000 per U.S. liver recipient strain payers and patients alike. Medicare coverage lapses three years post-surgery, leaving 32% of middle-aged recipients without adequate drug insurance. Complication-driven hospitalizations further inflate health-system costs, prompting calls to extend public reimbursement, which economic models show would yield both savings and quality-of-life gains. In low- and middle-income countries, out-of-pocket exposure often forces dose skimping, undermining outcomes and constraining organ transplant immunosuppressant drugs market expansion.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Calcineurin inhibitors retained 34.55% revenue in 2024, anchoring the organ transplant immunosuppressant drugs market. Proven agents such as tacrolimus remain first-line for most graft types. Yet mTOR inhibitors are on a 10.25% CAGR trajectory due to nephron-sparing and cardiometabolic benefits. Early conversion to everolimus within 12 months post-liver transplant improved renal function in 55% of patients. Rapamycin-based quadruple therapy delivered 20-year graft survival of 20.9%, eclipsing tacrolimus benchmarks. Co-stimulation blockers like belatacept and antiproliferatives such as mycophenolic acids round out therapeutic backbones, while antibody induction remains situational for high-risk recipients.

Novel delivery systems catalyze growth. Self-assembled rapamycin nanoparticles sustain plasma concentrations with lower systemic toxicity, and pegylated CD28-targeting fragments (VEL-101) progress through Phase 2. As generic penetration rises and patents sunset, price competition will intensify, but innovation in targeted or localized formulations should offset margin pressures, reinforcing the organ transplant immunosuppressant drugs market's mid-term growth outlook.

Kidney grafts continued to dominate 61.53% of the organ transplant immunosuppressant drugs market size in 2024, supported by mature protocols and high disease prevalence. Lung transplants, however, register the briskest 10.15% CAGR. Normothermic ex vivo perfusion elevates marginal lungs to transplantable status, eliminating primary graft dysfunction in donation-after-circulatory-death cohorts. Heart graft programs leverage veno-arterial ECMO back-up during acute dysfunction, boosting one-year survival. Liver and pancreas volumes expand steadily but face competition from evolving non-surgical disease-management options. Stem-cell transplants and vascularized composite allografts adopt tailored immunomodulation, indicating future niche demand pockets within the broader organ transplant immunosuppressant drugs market.

Growth in lung and emerging composite procedures will keep overall therapy volumes rising despite xenotransplantation experiments, whose success could either dampen maintenance-drug need or create new induction niches if human graft limitations persist.

The Organ Transplant Immunosuppressant Drugs Market Report is Segmented by Drug Class (Calcineurin Inhibitors, Antiproliferative Agents, MTOR Inhibitor, and More), Transplant Type (Heart, Kidney, Liver, Lung, and More), Route of Administration (Oral, Intravenous, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 42.72% of 2024 sales on the back of 46,000 transplants and comprehensive payer coverage. The United States posts high tacrolimus utilization despite rising generic substitution, and Canada's early adoption of machine perfusion further amps volumes. Europe maintains balanced growth, though reimbursement reforms and cross-border harmonization debates shape access in smaller member states.

Asia-Pacific is the fastest-growing contributor at 9.22% CAGR. China's state-sponsored transplant network, India's 13,426 kidney operations in 2023, and Japan's approval of LIVTENCITY for post-transplant CMV all illustrate momentum. Improvements in regulatory clarity, donor-registry digitization, and insurance expansion underline a structural shift that will raise the region's share of the organ transplant immunosuppressant drugs market through 2030.

South America and the Middle East & Africa remain nascent yet strategic. Brazil's established liver and kidney centers anchor South American progress, while Saudi Arabia and South Africa spearhead regional adoption of perfusion systems. Limited donor pools and funding constraints temper uptake, but targeted public-private partnerships could unlock incremental opportunity for the organ transplant immunosuppressant drugs market in the later forecast window.