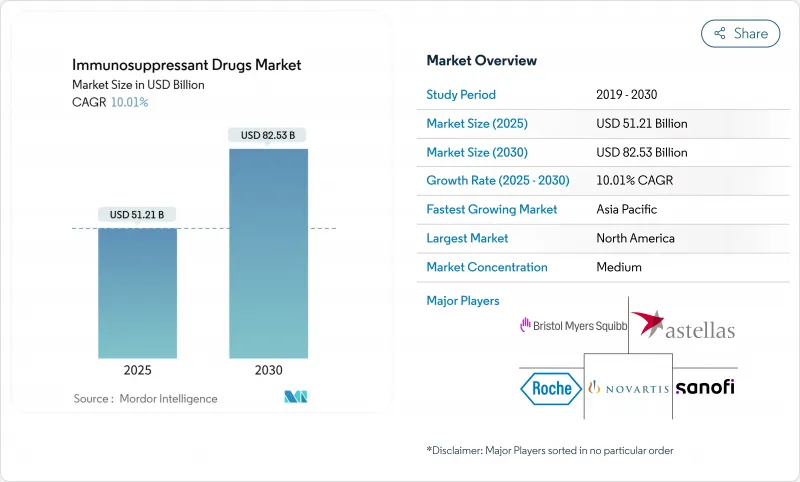

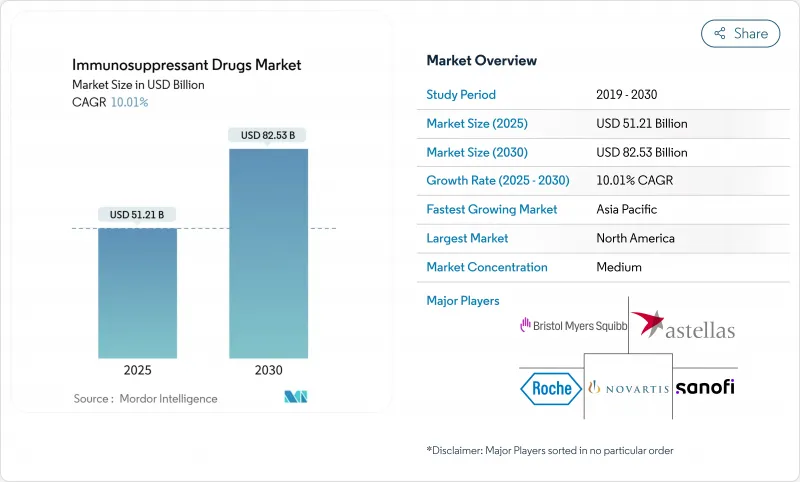

면역억제제 시장은 2025년에 512억 1,000만 달러를 창출하고, 2030년에는 825억 3,000만 달러에 이를 것으로 예상되며, CAGR은 10.01%를 나타낼 전망입니다.

자기 면역 질환 이환율의 상승, 기록적인 장기 이식 건수, 차세대 생물 제제의 급속한 보급, 메디케어의 인플레이션 억제 개혁 등이 수요를 밀어 올리는 요인이 되고 있습니다. 또한 JAK 억제제와 생물학적 제제의 피부과에서의 적응 외 사용 확대, 환자 접근을 확대하는 바이오시밀러의 침투, 투여 패턴을 개별화하는 인공지능 플랫폼 등이 기세를 늘리고 있습니다. 상업 전략은 이제 기존의 이식 센터의 틀을 훨씬 넘어, 환자 직접 판매의 디지털 유통이 약국 채널의 구조 전환을 촉진하고 있습니다. 이러한 배경에서 면역억제제 시장은 세포요법과 유전자요법의 대체품 위협과 다지역에 걸친 엄격한 규제 감시 위협에 동시에 직면하고 있으며, 경쟁은 격화의 길을 따라가고 있습니다.

진보된 진단 기술은 지금까지 발견되지 않았던 장기적인 약물 억제를 필요로 하는 환자 그룹을 발견하고, 자가면역 질환의 인지도를 증가시킵니다. 미국에서는 2024년에 4만 8,000건 이상의 장기 이식이 실시되었고 2023년 대비 3.3% 증가하여 평생 유지 요법의 새로운 수요 기준선이 설정되었습니다. 장기 보존 기술의 향상과 기증자 기준의 확대로 이식 건수가 더욱 증가하고 2026년까지 연간 6만 건의 이식을 실시하는 OPTN의 목표는 면역억제제의 지속적인 필요성을 강조하고 있습니다. 신흥경제국에서는 고령화가 진행되고, 치료계획이 복잡해지고, 환자 1인당 투여량이 증가하고, 총 지출이 증가합니다. 이러한 요인은 면역억제제 시장의 성장 궤도를 지원합니다.

유전자 편집 돼지의 장기가 개념 증명에서 조기 임상 평가로 진전하여 기증자 장기 부족을 완화하고 면역학적 프로토콜을 재정의할 수 있는 패러다임 변화를 나타냅니다. FDA의 틀은 현재 이종이식 신청에 대한 기대를 상세하게 설명하고 있으며, 미국을 차세대 이식의료의 최전선에 자리잡고 있습니다. 동시에 생체적합성 스캐폴드나 3D 바이오프린트 구조체 등의 조직공학적 혁신은 면역원성을 저하시켜 생물제제와 나노입자 기반의 전달을 융합시킨 새로운 면역억제 요법을 촉진하고 있습니다. 이러한 변화에 맞추어 연구개발 파이프라인을 정비하는 제약기업은 확대하는 면역억제제 시장에서의 방어력을 강화합니다.

규제의 다양화로 인해 기업은 서로 다른 승인 일정, 안전 요건 및 실제 세계 증거의 의무에 대응해야 했습니다. FDA의 조사는 이제 태내 노출시험까지 및 임상 프로그램을 장기화시켜 비용을 상승시키고 있습니다. 대서양을 넘어서는 하모나이제이션의 노력으로 무결성이 개선되었고, 지역 특유의 약물감시는 여전히 커스텀 인프라를 의무화하고 있으며 경쟁 우위는 견고한 컴플라이언스 자원을 가진 기존 기업에 기울고 있습니다. 전체적으로 이러한 복잡성은 이익을 압박하고 면역억제제 시장의 확대를 억제하고 있습니다.

칼시뉴린 억제제는 오랫동안 임상적 친숙함과 광범위한 가이드라인 승인을 통해 2024년 면역억제제 시장 점유율의 44.23%를 유지했습니다. 그러나 신독성이 우려되는 mTOR 억제제에는 여백이 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 10.78%로 가장 빠른 성장률을 보이고 있습니다. mTOR 억제제를 기반으로 하는 프로토콜의 면역억제제 시장 규모는 간 및 신장 수령인의 양호한 신기능 결과에 도움이 되며, 급격한 속도로 확대될 것으로 예측됩니다. 타크로리무스와 시클로스포린은 계속 이식 후 조기 투여의 주류가 되지만, 베라타셉트와 에베롤리무스는 집학적 이식팀에 어필하는 스테로이드 온존 접근법을 추진합니다.

칼시뉴린 억제제와 저용량 mTOR 억제제의 조합은 거부반응 위험과 부작용 프로파일의 균형을 맞추는 치료제 모니터링 플랫폼이 등장하여 정밀병용요법에 대한 기운이 가속화되고 있습니다. 미코페놀산 모페틸과 같은 항증식제와 새로운 비용 자극 차단제가 칵테일 요법을 완성하여 여러 작용기전을 가진 혁신적인 제약 기업을 위한 하이모트 포트폴리오를 형성하고 있습니다. 타크로리무스의 바이오시밀러 의약품의 보급에 의해 단가가 저하되는 가운데, 면역억제제 시장의 프랜차이즈 경제를 지키기 위해, 이노베이터는 차별화된 딜리버리 기술(나노입자 캡슐화, 주 1회 패치)에 경주하고 있습니다.

북미는 견고한 이식 생태계, 종합적인 메디케어 적용, 신규 투여 알고리즘 가이드라인의 신속한 채용을 배경으로 2024년 시장 점유율 40.87%를 유지했습니다. 임상연구 네트워크는 후기 개발품의 실용화까지의 시간을 단축하여 연구개발자에게 수익의 확실성을 높입니다. 캐나다의 각 주 포뮬러리와 멕시코의 Seguro Popular 업그레이드는 그 적용 범위를 넓히고 있지만, 가격 차이는 국경을 넘어서는 조달 전략을 복잡하게 하고 있으며, 면역억제제 시장 전체에서 무역 컴플라이언스에 대한 신중한 모니터링이 필요한 요인이 되고 있습니다.

아시아태평양은 중국과 인도가 이식능력을 확대하고 일본의 고령화가 자가면역질환 환자수를 증가시키기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 10.84%를 나타낼 전망입니다. 지역기관이 획기적인 생물학적 제제의 심사를 가속시키고, 상시까지의 기간이 과거의 전례에 비해 개선됩니다. 바이오시밀러 의약품의 현지 제조는 취득 비용을 절감하고, 2급 도시에서도 폭넓은 사용을 촉진합니다. 호주와 한국이 AI를 활용한 TDM 플랫폼의 도입을 선도하고, 면역억제제 시장에서의 환자 관리의 틀이 더욱 충실합니다.

유럽은 국민 모두 보험제도와 견고한 약물감시 체제에 힘입어 견조한 성장을 보이지만 의료기술평가가격 캡이 고액 진입기업의 톱라인 성장을 억제하고 있습니다. 독일, 영국, 프랑스는 이식제 판매량의 선두 주자이며, 남유럽 국가들은 자가면역 질환의 처방으로 능가하고 있습니다. FDA와의 규제 수렴으로 여러 지역에서의 신청 부담은 경감되지만, 브렉짓 후의 이중 신청은 범유럽 공급망을 운영하는 제조업체에게는 마찰이 됩니다. 중동 및 아프리카와 남미는 아직 발전도상이지만, 각각 이식시설의 인정과 제네릭 의약품 제조에 다액의 투자를 실시하고 있어, 세계의 면역억제제 시장에 장래적으로 관련성이 있음을 나타내고 있습니다.

The immunosuppressant drugs market generated USD 51.21 billion in 2025 and is forecast to reach USD 82.53 billion by 2030, progressing at a 10.01% CAGR.

Rising autoimmune-disease incidence, record organ-transplant volumes, rapid uptake of next-generation biologics, and Medicare inflation-rebate reforms combine to pull demand upward . Additional momentum comes from wider off-label dermatology use of JAK inhibitors and biologics, biosimilar penetration that broadens patient access, and artificial-intelligence platforms that individualize dosing patterns. Commercial strategies now extend far beyond traditional transplant centers, with direct-to-patient digital distribution driving a structural shift in pharmacy channels. Against this backdrop, the immunosuppressant drugs market faces simultaneous threats from cell- and gene-therapy substitutes and from stringent multi-regional regulatory surveillance, keeping competitive stakes high.

Autoimmune-disease recognition intensifies as advanced diagnostics uncover previously undetected patient pools requiring long-term pharmacologic suppression. The United States performed more than 48,000 organ transplants in 2024, a 3.3% rise over 2023, setting a new demand baseline for lifelong maintenance therapy . Enhanced organ-preservation technologies and expanded donor criteria raise procedure volumes further, while the OPTN target of 60,000 annual transplants by 2026 underscores sustained need for immunosuppressants. Aging demographics in developed economies add complexity to care plans, enlarging per-patient dosing and boosting aggregate spending. Collectively, these forces anchor the upward trajectory of the immunosuppressant drugs market.

Gene-edited pig organs progress from proof-of-concept to early clinical evaluation, signaling a paradigm shift that could alleviate donor-organ scarcity and redefine immunologic protocols. FDA frameworks now detail expectations for xenograft submissions, positioning the United States at the forefront of next-generation transplant medicine. Concurrently, tissue-engineering innovations-such as biocompatible scaffolds and 3-D bioprinted constructs-lower immunogenicity, prompting novel immunosuppression regimens that blend biologics with nanoparticle-based delivery. Pharmaceutical companies that align R&D pipelines with these changes strengthen defensibility in an expanding immunosuppressant drugs market.

Regulatory divergence forces companies to navigate disparate approval timelines, safety requirements, and real-world-evidence obligations. FDA scrutiny now extends to in-utero exposure studies, lengthening clinical programs and escalating costs. Although trans-Atlantic harmonization efforts improve alignment, region-specific pharmacovigilance still mandates custom infrastructures, tilting competitive advantage toward incumbents with robust compliance resources. In aggregate, these complexities compress margins and temper expansion across the immunosuppressant drugs market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Calcineurin inhibitors retained 44.23% immunosuppressant drugs market share in 2024 owing to long-standing clinical familiarity and broad guideline endorsement. Yet nephrotoxicity worries open white space for mTOR inhibitors, whose 10.78% CAGR marks the fastest segment growth to 2030. The immunosuppressant drugs market size for mTOR-based protocols is projected to expand at a notably brisk clip, helped by favorable renal-function outcomes among liver and kidney recipients. Tacrolimus and cyclosporine will continue to dominate early-post-transplant dosing, but belatacept and everolimus drive steroid-sparing approaches that appeal to multidisciplinary transplant teams.

Momentum toward precision combinations accelerates as therapeutic-drug-monitoring platforms pair calcineurin inhibitors with low-dose mTOR inhibitors to balance rejection risk and adverse-event profiles. Antiproliferative agents such as mycophenolate mofetil and emerging costimulation blockers round out cocktail regimens, creating high-moat portfolios for innovators that own multiple mechanisms of action. As biosimilar tacrolimus diffusion lowers unit prices, innovators lean on differentiated delivery technologies-nanoparticle encapsulation, once-weekly patches-to protect franchise economics inside the immunosuppressant drugs market.

The Immunosuppressant Drugs Market is Segmented by Drug Class (Calcineurin Inhibitors, Antiproliferative Agents, MTOR Inhibitors, Steroids, Other Classes), Application (Autoimmune Diseases, Organ Transplant, Other Applications), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America maintained 40.87% market share in 2024 grounded in robust transplant ecosystems, comprehensive Medicare coverage, and rapid guideline adoption for novel dosing algorithms. Clinical research networks speed time-to-practice for late-stage products, raising revenue certainty for developers. Canada's provincial formularies and Mexico's Seguro Popular upgrades extend reach, yet pricing differentials complicate cross-border procurement strategies, a factor requiring vigilant trade-compliance oversight across the immunosuppressant drugs market.

Asia-Pacific exhibits the most rapid 10.84% CAGR to 2030 as China and India scale transplant capacity and as Japan's aging demographics swell autoimmune caseloads. Regional agencies craft accelerated review pathways for breakthrough biologics, which improves launch windows relative to historic precedents. Local biosimilar manufacturing cuts acquisition costs, spurring broader usage even in secondary-tier cities. Australia and South Korea lead uptake of AI-enabled TDM platforms, further enriching patient-management frameworks within the immunosuppressant drugs market.

Europe posts steady gains aided by universal coverage and strong pharmacovigilance structures, but health-technology-assessment price caps curb top-line growth for high-ticket entrants. Germany, United Kingdom, and France represent transplant volume leaders, while Southern European nations outpace on autoimmune prescriptions. Regulatory convergence with FDA eases multi-regional filing burdens; however, post-Brexit dual submissions add friction for manufacturers operating pan-European supply chains. Middle East & Africa and South America remain nascent but invest heavily in transplant-center accreditation and generic manufacturing respectively, signaling future relevance to the worldwide immunosuppressant drugs market.