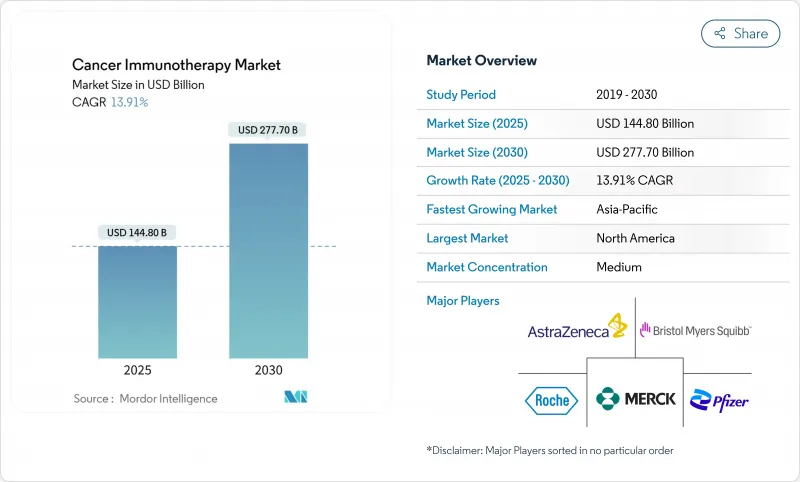

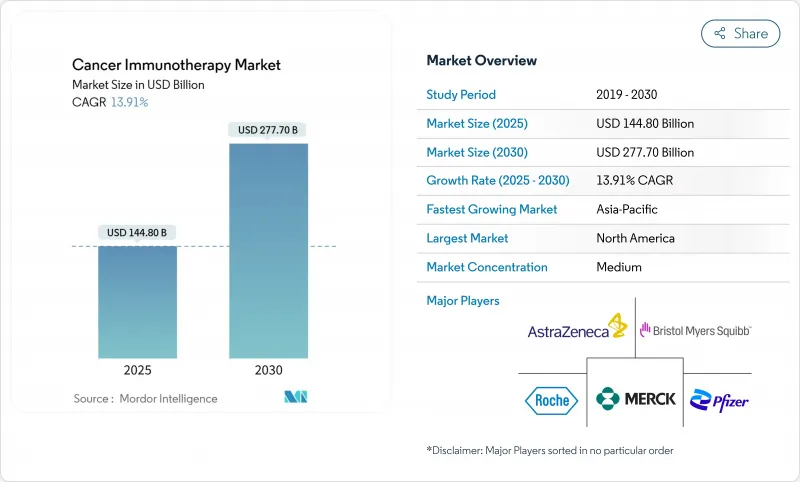

암 면역치료 시장은 2025년에는 1,448억 달러로 추정되고, 2030년에는 2,777억 달러에 이를 것으로 예측되며, CAGR 13.91%로 성장할 전망입니다.

이 성장률의 급상승은 이 치료 클래스가 실험적인 사용에서 표준 암 치료의 기둥으로 이행한 것을 반영하고 있습니다. 2024년 2월 미국 식품의약국(FDA)은 진행성 흑색종에 대한 최초의 종양 침윤 림프구(TIL) 요법인 lifileucel을 승인하는 등 주목도 높은 승인에 의해 가속화되고 있습니다. 그 기세는 대규모 제조에 대한 투자, 성과 기반 계약에 대한 지불자의 수용 확대, 생존 기간 연장 효과를 검증하는 병용 요법 시험의 결과에 의해 강화되고 있습니다. 바이러스 벡터 및 mRNA 합성에 대한 공급망이 성숙해지므로 제조 위험이 더욱 감소하고 보다 광범위한 상업 전개가 촉진됩니다. 아시아태평양의 규제 조화와 생산 능력 증강이 북미의 우위성을 균형 잡는 제2 성장 엔진이 되는 한편, 자금력이 있는 기존 기업이 차세대 치료법을 확보하기 위해 전문성이 높은 혁신자를 인수해 경쟁의 격렬함이 증가하고 있습니다.

특히 폐암, 대장암, 유방암에서는 생활습관과 관련된 위험 인자 증가와 고령화로 치료 가능한 환자층이 확대되고 있습니다. 종양학회는 현재 정기적인 바이오 마커 스크리닝을 권장하고 있으며, 더 많은 환자가 조기에 면역치료로 전환할 수 있습니다. 공공기관의 암 계발 캠페인은 진단률을 더욱 가속화하고, 지불기관은 뛰어난 결과를 기대할 수 있는 정밀치료제로의 상환 예산을 확대하고 있습니다. 이러한 힘을 종합하면 가격 압력이 높아지는 가운데 암 면역치료 시장의 수량 성장은 유지되고 있습니다.

CheckMate 9LA의 5년 추적 조사에서는 전이성 비소세포 폐암에서 니볼루맙과 이피리무맙의 화학요법 병용치료는 화학요법 단독 치료의 11%에 대해 18%의 전체 생존율을 달성한 것으로 확인되어 최신 치료 알고리즘을 형성하는 내구성의 우위성이 강화되었습니다. 종양학 가이드라인에서는 PD-L1 고발현 종양의 첫 회 치료에 있어서 체크포인트 억제제를 우선하는 경향이 강해지고 있으며, 주요 암 센터에서는 프로토콜의 개정이 진행되고 있습니다. 실제 임상 등록은 시험 데이터의 뒷받침이 되고, 임상의의 신뢰가 높아지며, 병원에서의 처방 확대가 촉진됩니다.

CAR-T 치료는 코스당 30만 달러를 초과하는 가격으로 판매되며, 지불자의 예산을 압박하고 미국 등 시장에서는 결과 기반 계약이 증가하고 있습니다. Iovance의 Amtagvi 정가는 51만 5,000달러이며 환자의 반응과 지불을 연결하는 협상의 방아쇠가 되었습니다. 신흥국의 단계적 가격 설정과 강제 라이선싱의 위협이 수익 궤도에 무거워지기 때문에 제조 업체는 비용 효율성을 위해 생산의 합리화를 강요하고 있습니다.

단일클론항체는 2024년 매출의 67.55%를 차지했으며, 암 면역치료 시장에서 가장 큰 점유율을 차지했습니다. 폐암, 흑색종, 신장암에서 퍼스트라인에서 지속적인 사용이 큰 볼륨을 지원하고 있으며, 이 부문의 암 면역치료 시장 규모는 2030년까지 1,742억 달러에 달할 것으로 예측되고 있습니다. 한편, 암세포 용해 바이러스는 CAGR 24.25%로 급성장하고 있으며, 후기 단계의 자산과 제조 파트너십의 확대에 의한 규모의 확대에 지지되고 있습니다.

화이자는 이그나이트 면역치료에 자본 참여함으로써 mRNA 페이로드를 따라 독자적인 바이러스 백본에 접근할 수 있게 되었습니다. 또한 브리스톨 마이어스 스퀴브와 바이오에누텍의 이중 특이성 항체에 관한 제휴는 항체 공학의 노하우와 mRNA의 능력을 융합시키는 것입니다. 치료법의 융합은 종양 특이적 면역을 강화하고 내성을 완화시키는 콤보 요법을 촉진합니다.

폐암은 2024년 매출의 25.53%를 차지했으며, 암 면역치료 시장 최대의 적응증입니다. 규제 당국이 보조제 치료를 승인하고 암 이환율이 높은 지역이 조기 진단을 촉진하는 스크리닝 프로그램을 도입하고 있기 때문에 이 분야의 우위는 흔들리지 않습니다. 혈액 악성 종양은 가장 급속한 CAGR 22.15%를 나타내며 암 면역치료 시장 규모는 2030년까지 686억 달러로 확대될 전망입니다.

다발성 골수종과 급성 림프아구성 백혈병에 대한 CAR-T의 승인은 대응 가능한 환자 수를 확대하고, 이중특이적 항체는 세포 치료가 부적격인 환자에게도 치료를 확대합니다. 중국의 데이터는 400개가 넘는 의사가 주도한 CAR-T 임상시험을 실시하고 있으며, 학술계열의 열정과 정부의 토착 기술 혁신에 대한 지원을 반영하고 있습니다. 이러한 활동은 예측 기간 동안 혈액학을 매우 중요한 수익 촉진요인으로 자리 매김하고 있습니다.

북미는 2024년 세계 매출의 48.72%를 차지했으며 주도권을 유지하고 있습니다. 미국은 FDA의 신속한 승인, 벤처 캐피탈의 왕성한 자금 유입, 프리미엄 가격을 유지하는 결과 기반 상환을 시도하는 지불자로부터 혜택을 받고 있습니다. 미국 국립암연구소(National Cancer Institute)는 71개 지정암센터에서 트랜스레이셔널리서치를 조성하여 의사주도 치험과 신규 병용요법의 파이프라인을 유지하고 있습니다. 캐나다는 연방정부에 의한 세포치료 센터 오브 엑설런스에 대한 투자를 통해 이 동향을 반영하여 국내 제조 능력을 가속화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 18.22%로 가장 빠른 성장이 전망됩니다. 중국이 이 지역 기세의 선두에 서서 400개 이상의 CAR-T 임상 프로그램을 실시하고 관민 합작 사업을 통해 바이러스 벡터의 능력을 구축하고 있습니다. 국가의약품관리국(National Medical Products Administration)의 우선 심사 패스웨이 등의 규제 개혁에 의해 획기적인 치료법에 대한 승인까지의 기간이 12개월 미만으로 단축됩니다. 의약품 의료기기 종합기구는 다른 주요 시장에 앞서 악성 흉막 중피종에 대한 니볼루맙을 승인하고 규제 당국의 민첩성을 보였습니다. 인도는 자국에서의 CAR-T 제제 제조에 주력하고 비용 효율적인 공정을 활용하여 접근을 확대하고 신흥 인근 국가의 수출 수요를 캡처합니다.

유럽은 EMA 수준의 조정에 힘입어 꾸준한 확대를 유지하고 있습니다. EU 전역을 다루는 임상시험 네트워크는 다양한 유전적 배경을 가진 환자의 효율적인 모집을 가능하게 하고 고정밀 바이오마커 검증을 위한 데이터를 충실히 합니다. 브랙시트는 규제 당국에 신청을 이중으로 하는 반면, 병행하여 이루어지는 과학적 조언에 의해 지연이 완화되어 매우 중요한 시험에 영국의 참가가 유지됩니다. 독일, 프랑스, 북유럽의 의료기술평가기관은 정가를 압박하는 비용 효과 임계값을 적용하고 결과 기반 할인 프레임워크에 인센티브를 부여하고 있습니다. 스위스와 아일랜드의 현지 바이오 제조 클러스터는 국내 시장과 수출 시장 모두에 공급 규모를 확대하고 첨단 치료 제조 허브로서 유럽의 지위를 강화하고 있습니다.

The cancer immunotherapy market stood at USD 144.80 billion in 2025 and is forecast to reach USD 277.70 billion by 2030, advancing at a 13.91% CAGR.

The growth surge mirrors the therapy class' graduation from experimental use to a pillar of standard oncology care, accelerated by high-profile approvals such as the February 2024 U.S. Food and Drug Administration (FDA) clearance of lifileucel, the first tumour-infiltrating lymphocyte (TIL) therapy for advanced melanoma. Momentum is reinforced by large-scale manufacturing investments, widening payer acceptance of outcome-based contracts, and combination-therapy trial readouts that validate durable survival benefits. Supply-chain maturity around viral vectors and mRNA synthesis further lowers production risk, encouraging broader commercial roll-outs. Asia-Pacific's regulatory harmonisation and capacity build-out add a second growth engine that balances North America's established dominance, while competitive intensity heightens as cash-rich incumbents acquire specialised innovators to secure next-generation modalities.

Rising lifestyle-related risk factors and ageing demographics enlarge the treatable patient pool, notably in lung, colorectal, and breast cancers. Oncology societies now recommend routine biomarker screening, ensuring more patients are triaged early into immunotherapy regimens. Public-sector cancer awareness campaigns further accelerate diagnosis rates, while payer agencies expand reimbursement budgets for precision drugs that promise superior outcomes. Collectively, these forces sustain volume growth in the cancer immunotherapy market even as pricing pressures mount.

Five-year follow-up from CheckMate 9LA confirmed that nivolumab plus ipilimumab with chemotherapy achieved 18% overall survival in metastatic non-small cell lung cancer against 11% for chemotherapy alone, reinforcing the durability advantage that shapes modern treatment algorithms. Oncology guidelines increasingly prioritise checkpoint inhibitors in first-line settings for PD-L1-high tumours, driving protocol revisions at major cancer centres. Real-world registries corroborate trial data, boosting clinician confidence and catalysing hospital formulary expansion.

CAR-T therapies price above USD 300,000 per course, stretching payer budgets and prompting the rise of outcome-based contracts in markets such as the United States. Iovance's Amtagvi lists at USD 515,000, triggering negotiations that link payment to patient response. Tiered pricing and compulsory-licensing threats in emerging economies weigh on revenue trajectories, pressing manufacturers to streamline production for cost efficiencies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Monoclonal antibodies retained 67.55% of revenue in 2024, giving them the largest cancer immunotherapy market share among modalities. Continued first-line use in lung, melanoma, and renal cancers supports sizable volumes, and the segment's cancer immunotherapy market size is projected to reach USD 174.2 billion by 2030. In contrast, oncolytic viruses are growing fastest at a 24.25% CAGR, underpinned by rising late-phase assets and manufacturing partnerships that unlock scale.

Investment patterns confirm strategic re-weighting; Pfizer's equity stake in Ignite Immunotherapy provides access to proprietary viral backbones aligned with mRNA payloads. Parallelly, Bristol Myers Squibb's alliance with BioNTech on bispecific antibodies merges antibody engineering know-how with mRNA capabilities. Convergence of modalities fosters combo regimens that enhance tumour-specific immunity and mitigate resistance.

Lung cancer contributed 25.53% of 2024 sales, representing the single largest indication within the cancer immunotherapy market. The segment's dominance persists as regulators approve adjuvant uses and high-burden geographies roll out screening programmes that drive earlier diagnosis. Hematologic malignancies exhibit the most rapid 22.15% CAGR, elevating their cancer immunotherapy market size to USD 68.6 billion by 2030.

CAR-T approvals for multiple myeloma and acute lymphoblastic leukaemia expand addressable patient pools, while bispecific antibodies extend therapy to those ineligible for cell therapy. Data from China show over 400 investigator-led CAR-T trials, reflecting academic enthusiasm and government support for indigenous innovation. Such activity positions hematology as a pivotal revenue accelerator over the forecast horizon.

The Cancer Immunotherapy Market Report is Segmented by Therapy Type (Monoclonal Antibodies, Immunomodulators, and More), Cancer Type (Prostate Cancer, Breast Cancer, Lung Cancer, and More), End Users (Hospitals and Clinics, Cancer Research Centers, and More), Route of Administration (Intravenous and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America preserved leadership with 48.72% of global revenue in 2024. The United States benefits from rapid FDA approvals, robust venture capital inflows, and payers experimenting with outcome-based reimbursement that sustains premium pricing. National Cancer Institute funding underwrites translational research across 71 designated cancer centres, maintaining a pipeline of investigator-initiated trials and novel combination studies. Canada mirrors the trend through federal investments in cell-therapy centres of excellence, accelerating domestic manufacturing capability.

Asia-Pacific delivers the fastest 18.22% CAGR through 2030. China spearheads regional momentum, hosting more than 400 CAR-T clinical programmes and building viral-vector capacity via public-private joint ventures. Regulatory reforms, such as the National Medical Products Administration's priority-review pathway, compress approval timelines to under 12 months for breakthrough therapies. Japan extends leadership in early adoption; the Pharmaceuticals and Medical Devices Agency approved nivolumab for malignant pleural mesothelioma ahead of other major markets, signalling regulatory agility. India focuses on indigenous CAR-T manufacturing, leveraging cost-efficient processes to widen access and capture export demand in emerging neighbouring nations.

Europe maintains steady expansion underpinned by EMA-level coordination. Pan-EU clinical-trial networks enable efficient patient recruitment across diverse genetic backgrounds, enriching data for precision biomarker validation. While Brexit imposes dual regulatory submissions, parallel scientific advice mitigates delays, sustaining UK participation in pivotal studies. Health Technology Assessment bodies across Germany, France, and the Nordics apply cost-effectiveness thresholds that pressure list prices, incentivising outcome-based discount frameworks. Local biomanufacturing clusters in Switzerland and Ireland scale supply for both domestic and export markets, reinforcing Europe's status as an advanced-therapy manufacturing hub.