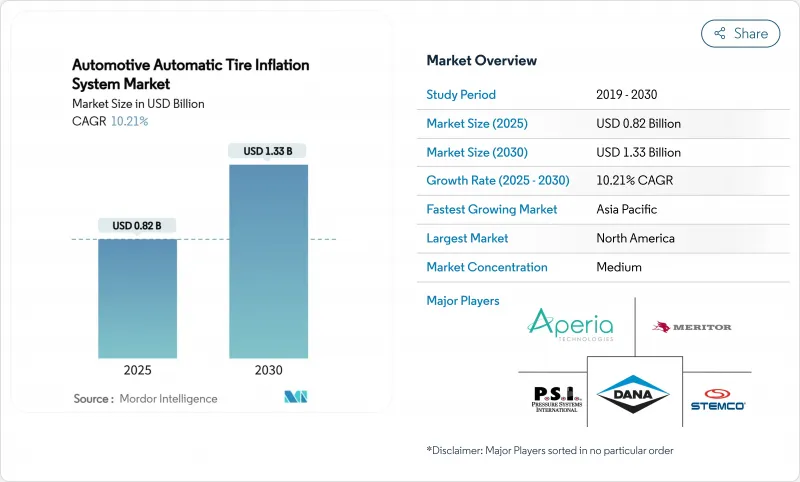

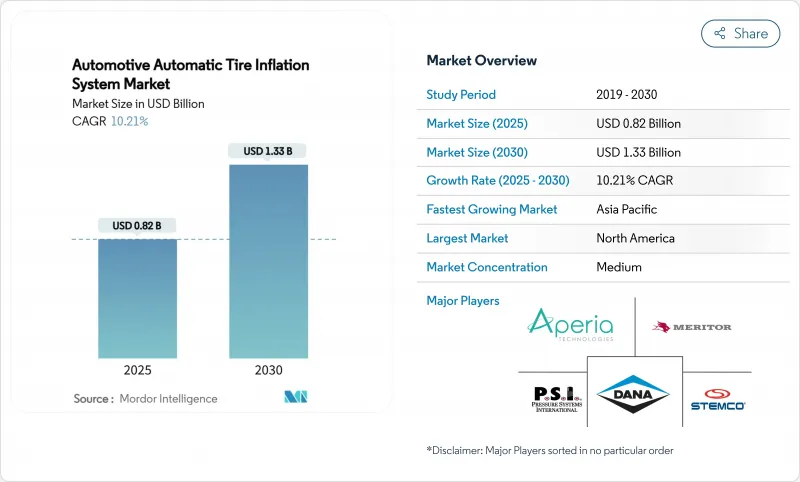

자동차용 자동 타이어 인플레이션 시스템 시장 규모는 2025년에 8억 2,000만 달러의 평가 금액을 기록하고, 2030년에는 13억 3,000만 달러에 이를 것으로 예상되며, CAGR은 10.21%를 나타낼 전망입니다.

성장은 협력적인 안전 규정, 차량 비용 절감의 필요성, 커넥티드 자동차 아키텍처와의 긴밀한 통합을 반영합니다. 북미 차량은 49 CFR 393.75의 저온 인플레이션 규칙을 준수해야 하며, 유럽 연합의 일반 안전 규칙 II는 모든 신차에 타이어 공기압 모니터링을 의무화하여 간접적으로 완전 자동 인플레이션 기능에 대한 수요가 증가하고 있습니다. 업무용 차량은 타이어가 적정 공기압으로 유지됨으로써 최대 1.4%의 연료 절감을 실현하여 자동 시스템의 투자 수익률을 높이고 있습니다. 이와 병행하여, 펜트의 바리오 그립이 주행중에 공기압을 8.7-36.3 PSI까지 변화시키는 것으로 보이는 것처럼, 농업기계나 건설기계 제조업체는 토양 보전의 의무나 정밀 농업의 요구를 충족시키기 위해 중앙 공기압 제어를 짜넣고 있습니다. 투자의 기세는 벤처기업의 자금조달에 의해 지원되고 있으며, 그 예로는 허브 탑재형 셀프 파워 인플레이터를 타겟으로 하는 Aperia Technologies의 4,500만 달러의 자금조달을 들 수 있습니다.

대형 트럭의 운행 예산의 15-20%는 타이어의 지출이며, 공압 부족은 거리에서의 타이어 고장의 95%에 해당합니다. Pressure Systems International은 자동 공기 공급을 설치할 때 평균 1.4%의 연비 향상과 10%의 타이어 수명 연장을 정량화합니다. 데이터가 풍부한 플랫폼은 공압, 온도 및 적재 정보를 실시간으로 제공하여 배달 담당자가 속도 프로파일과 유지보수 창을 최적화할 수 있도록 합니다. 장거리 운송업체는 트랙터 1대당 연간 주행거리가 12만 마일을 넘으면 증가하는 절약 효과가 복합적으로 작용하기 때문에 절대적인 이익을 가장 크게 즐길 수 있습니다. 그 결과, 조달 팀은 트랙터와 트레일러의 교환 주기에 자동 공기 흡입을 선호하는 총 소유 비용 모델을 통합합니다.

세계적인 법규제가 타이어 유지보수 규율을 높이고 있습니다. 2024년 7월에 발효된 EU 일반 안전 규칙 II는 M1을 제외한 모든 신규 호모로게이션 차량 범주에 타이어 공압 모니터링을 의무화했으며 자동 공압 업그레이드를 장려하는 보편적인 기준선을 만들어 냈습니다. 보완적인 유로 7 규칙은 타이어 마모의 상한이 설정되고 2032년이 준수 기한이 되었습니다. 미국에서는 연방자동차 운송안전국의 검사관이 노상검사에서 타이어공압의 하한을 강제하고 있기 때문에 대규모 플릿은 단속을 피하기 위해 자동 시스템을 도입하고 있습니다. 유사한 규정은 수출 지향 OEM이 EU 기준과 조화를 이루는 가운데 남미와 동남아시아에도 파급되고 있습니다. 그 결과, 함대 매니저는 자동차용 자동 타이어 인플레이션 시스템 시장 도입이 컴플라이언스에 필요한 것으로, 운영상의 절약이 될 수 있다고 인식하고 있습니다.

시스템 패키지는 1대당 1,500달러에서 5,000달러입니다. 레트로핏 프로젝트는 근무 시간과 잠재적인 가동 중지 시간을 추가하기 때문에 많은 소규모 운송 회사는 흡수할 수 없습니다. 상업용 타이어 딜러는 예산에 제약이 있는 운영자가 손익 분기점 분석을 통해 18개월 이내에 투자를 회수할 수 있음에도 불구하고 설비 투자 주기가 완성될 때까지 업그레이드를 늦추고 있다고 지적합니다. 기술자 교육, 센서 교정, 기존 전자 제어 장치와의 소프트웨어 무결성 등이 가격에 민감한 지역에서의 채용을 더욱 늦추고 있습니다.

2024년 자동차용 자동 타이어 인플레이션 시스템 시장 매출액의 66.82%를 중형·대형 상용차가 차지해 이 분야가 자동차용 자동 타이어 인플레이션 시스템 시장에 큰 영향을 미친 것으로 나타났습니다. 연간 주행 거리 증가, 다차축 구성, 연료 소비에 대한 감도의 높이 등이 자동 타이어 인플레이션에 대한 설득력 있는 투자 케이스를 만들어 내고 있습니다. 원격 진단 및 공압 교정을 통해 배차 담당자는 로드 사이드 서비스 통화를 최소화하고 배송 일정을 보호할 수 있습니다. OEM이 모델 라인 전체에서 공기 주입 포트와 데이터 프로토콜을 표준화함에 따라 지역 운송 트럭과 최종 마일 트럭에도 채택이 확산되고 있습니다.

오프 하이웨이 장비는 2030년까지 연평균 복합 성장률(CAGR)이 11.84%로 가장 날카로운 궤도를 나타낼 전망입니다. 정밀 농업에서는 수율을 보호하기 위해 부드러운 토양 부하가 요구되고 건설 차량과 군용 차량은 아스팔트, 자갈 및 진흙 사이에서 신속한 조정이 요구됩니다. 펜트의 캡슐인 VarioGrip은 몇 초 안에 압력을 전환하고 견인 효율을 높이고 체결을 줄입니다. 존디어와 CNH 산업은 비슷한 제품을 제공하고 압력 제어를 통합한 업계로의 전환을 시사합니다. 경상용 밴과 승용차의 매출은 겸손하지만, EU 안전 규칙과 고급 운전 지원 기능에 대한 소비자의 선호도는 OEM 각 회사에 소형 자동 공압 모듈을 통합하도록 촉구하고 있습니다.

온로드 타이어는 2024년 자동차용 자동 타이어 인플레이션 시스템 시장 매출의 72.41%를 차지하며, 고속도로의 주행 거리마다 공압 부족이 연비를 악화시키는 대륙 횡단 트럭 수송이 그 중심이 되었습니다. 자동 공기 흡입 시스템은 기존의 주 1회 검사 루틴에서 만성 공기압 부족으로 이어질 수 있는 주변 변동에 관계없이 냉간 공기 흡입 수준을 지속적으로 조정합니다. 함대 텔레매틱스 대시보드는 운행 시간 표시와 함께 공압 KPI를 통합하고 관리자는 디젤 소비량과 직접 관련된 컴플라이언스 비율로 저장소를 벤치마킹합니다.

오프로드 타이어는 채석, 임업 및 농업을 위한 스마트 기계에 대한 투자를 반영하여 CAGR 12.29%를 나타낼 전망입니다. 미슐랭 중앙 시스템은 토양 유형에 맞게 공기압을 조정하여 생산성을 최대 4% 향상시키고 연료를 10% 절약합니다. 연구에 의하면 적절한 압력으로 토양의 체결 깊이를 3분의 1까지 줄일 수 있어 경작지를 보존하고 경작 에너지를 삭감할 수 있습니다. 마찬가지로, 휠 로더의 운전자는 측벽의 핀치 피해가 발생하기 전에 경고를 발하는 폐쇄 루프 공압을 도입하여 타이어 관련 다운타임이 감소했다고 보고했습니다. 이러한 장점은 소규모 계약자에게 선행가격이 장벽이 되더라도 미래 수요를 확고히 합니다.

북미는 2024년에 자동차용 자동 타이어 인플레이션 시스템 시장에서 39.81%의 매출을 확보해, 명확한 규제 틀과 성숙한 텔레매틱스의 보급에 지지되었습니다. 연방 정부가 타이어 공압 규칙을 시행함에 따라 운송 회사는 거리 벌금에 대한 보험으로 자동 솔루션을 채택했습니다. 대규모 하이어 플릿은 1-3%의 디젤 절약과 15-20%의 타이어 수명 향상을 꼽으며, 이사회 수준의 지속가능성 서약을 강화하는 성과입니다. 이 지역은 또한 드라이버리스 화물 운송 경로의 대규모 파일럿 테스트를 실시하고 있으며, 자율 주행 개발자는 드라이버를 유지 보수 루프에서 제거하는 중복 타이어 건강 시스템이 필요합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 12.19%로 가장 빠르게 상승할 것으로 예상됩니다. 전자상거래의 폭발적인 출하량, 대규모 고속도로 건설, 전동 파워트레인의 추진은 자동 인플레이션의 경제적 근거를 선명하게 합니다. 인도의 물류 개혁은 운송 비용에 연결된 GDP의 12-14% 유출을 줄이려고 하며, 타이어 공압의 시정은 눈에 띄는 테코입니다. 제일기차나 Sinotruk 등 중국의 OEM은 배터리의 항속 거리를 연장하기 위해 신에너지 트럭에 공압 밸브를 통합하여 자동차용 자동 타이어 인플레이션 시스템 시장을 표준 효율 대책으로 자리잡고 있습니다.

유럽은 유럽연합(EU) 전체의 안전·환경지령에 인도되어 일관성을 유지하고 있습니다. 규제 II는 모든 신차에 TPMS를 의무화하고 Euro 7은 최적의 공기압에 크게 의존하는 마모 제한을 도입했습니다. 독일과 프랑스 사업자는 고객의 Scope 3 공개 요구 사항을 충족하기 위해 인플레이션 데이터와 탄소 보고서를 결합합니다. 중동 및 아프리카는 전반적인 보급률로 지연을 겪고 있지만, 석유 수출국은 인프라 자금을 직업용 차량 업그레이드에 쏟고 있으며 서비스 센터의 밀도가 늦어도 기본적인 수요가 높아지고 있습니다.

The automotive automatic tire inflation system market size registers a valuation of USD 0.82 billion in 2025 and is forecast to reach USD 1.33 billion by 2030, advancing at a 10.21% CAGR.

Growth reflects coordinated safety regulations, fleet cost-reduction imperatives, and tighter integration with connected-vehicle architectures. North American fleets must comply with 49 CFR 393.75 cold-inflation rules, while the European Union's General Safety Regulation II requires tire-pressure monitoring across all new vehicles, indirectly cementing demand for fully automatic inflation capabilities. Commercial fleets realize up to 1.4% fuel savings when tires remain at correct pressure, sharpening return on investment for automatic systems . In parallel, agricultural and construction equipment makers embed central pressure control to meet soil-conservation mandates and precision-farming needs, as seen in Fendt's VarioGrip that varies pressure from 8.7 to 36.3 PSI while in motion. Investment momentum is buoyed by venture funding, illustrated by Aperia Technologies' USD 45 million raise that targets hub-mounted self-powered inflators.

Tire expenditures represent 15-20% of heavy-truck operating budgets, and under-inflation generates up to 95% of roadside tire failures. Pressure Systems International quantifies 1.4% mean fuel gains and 10% tire-life extension when automatic inflation is installed . Data-rich platforms deliver live pressure, temperature, and load information, letting dispatchers optimize speed profiles and maintenance windows. Long-haul carriers accrue the greatest absolute benefit because incremental savings compound across annual mileages that exceed 120,000 miles per tractor. Consequently, procurement teams embed total cost-of-ownership models that prioritize automatic inflation during tractor and trailer replacement cycles.

Worldwide statutes are elevating tire-maintenance discipline. The EU General Safety Regulation II, effective July 2024, mandates tire-pressure monitoring on every newly homologated vehicle category except M1, creating a universal baseline that encourages automatic inflation upgrades. Complementary Euro 7 rules set tire-abrasion caps with 2032 compliance deadlines . In the United States, Federal Motor Carrier Safety Administration inspectors enforce cold-inflation minimums during roadside checks, prompting large fleets to deploy automated systems to avoid citations. Similar provisions are cascading into South America and Southeast Asia as export-oriented OEMs harmonize with EU standards. As a result, fleet managers perceive automotive automatic tire inflation system market adoption as a compliance necessity that also unlocks operational savings.

System packages range from USD 1,500 to USD 5,000 per vehicle. Retrofit projects add labor hours and potential downtime that many small carriers cannot absorb. Commercial tire dealers note budget-constrained operators delaying upgrades until capex cycles align, even though break-even analysis often shows payback inside 18 months. Training technicians, calibrating sensors, and harmonizing software with legacy electronic control units further slow adoption in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Medium and heavy commercial vehicles accounted for 66.82% of the automotive automatic tire inflation system market revenue in 2024, underscoring the sector's outsized influence on the automotive automatic tire inflation system market. Elevated annual mileage, multi-axle configurations, and fuel-spend sensitivity combine to produce compelling investment cases for automatic inflation. Remote diagnostics and over-the-air pressure calibration let dispatchers minimize roadside service calls and preserve delivery schedules. Adoption is now filtering into regional haul and final-mile trucks as OEMs standardize inflation ports and data protocols across model lines.

Off-highway equipment exhibits the sharpest trajectory at an 11.84% CAGR through 2030. Precision agriculture mandates gentle soil loading to protect yield, while construction and military vehicles require fast adjustments between asphalt, gravel, and mud. Fendt's in-cab VarioGrip toggles pressure inside seconds, boosting tractive efficiency and cutting compaction, and similar offerings from John Deere and CNH Industrial signal an industry shift toward embedded pressure control. Light commercial vans and passenger cars participate more modestly, yet EU safety rules and consumer preference for advanced driver-assistance features are nudging OEMs to incorporate scaled-down automatic inflation modules.

On-road tires secured 72.41% of the automotive automatic tire inflation system market revenue in 2024, anchored by cross-continental trucking, where under-inflation steals fuel economy on every highway mile. Automated systems continuously regulate cold-inflation levels regardless of ambient swings that might lead to chronic under-pressure in conventional weekly-check routines. Fleet telematics dashboards integrate pressure KPIs alongside hours-of-service readouts, and managers benchmark depots on compliance percentages that correlate directly with diesel spend.

Off-road tires are climbing at a 12.29% CAGR, reflecting investment in smart machinery for quarrying, forestry, and agriculture. Michelin's central system posts up to 4% productivity lifts and 10% fuel savings by tailoring pressure to soil type. Studies show that correct pressure can trim soil compaction depth by one-third, preserving arable land and reducing tillage energy. Similarly, wheel-loader operators report lower tire-related downtime after installing closed-loop inflation that alerts them before sidewall pinch damage occurs. These benefits cement future demand even as upfront pricing remains a barrier for smaller contractors.

The Automotive Automatic Tire Inflation System Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (On-The-Road Tires and Off-The-Road Tires), Sales Channel (OEM and Aftermarket), Product Type (Central Tire Inflation Systems (CTIS), Continuous/Wheel-End Inflators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America secured 39.81% revenue of the automotive automatic tire inflation system market in 2024, buoyed by well-defined regulatory frameworks and mature telematics penetration. Federal enforcement of tire-pressure rules prompts carriers to adopt automatic solutions as insurance against roadside fines. Large for-hire fleets cite 1-3% diesel savings and 15-20% tire-life gains, outcomes that reinforce board-level sustainability pledges. The region also hosts expansive pilots for driverless freight corridors, and autonomous developers require redundant tire-health systems that remove the driver from the maintenance loop.

Asia-Pacific posts the quickest ascent at 12.19% CAGR through 2030. Explosive e-commerce shipping volumes, extensive highway build-outs, and the push for electrified powertrains sharpen the economic rationale for automatic inflation. India's logistics overhaul seeks to trim the 12-14% GDP drain tied to freight costs, and correcting tire pressure is a visible lever. Chinese OEMs such as FAW and Sinotruk integrate inflation valves on new energy trucks to extend battery range, positioning the automotive automatic tire inflation system market as a standard efficiency measure.

Europe remains consistent, guided by Union-wide safety and environmental directives. Regulation II obliges TPMS on every new vehicle, and Euro 7 introduces abrasion limits that depend heavily on optimum pressure. Operators in Germany and France combine inflation data with carbon reporting to satisfy customer Scope 3 disclosure requests. The Middle East and Africa trail in overall penetration, yet oil-exporting economies funnel infrastructure funds into vocational fleet upgrades, which lifts baseline demand even if service-center density lags.