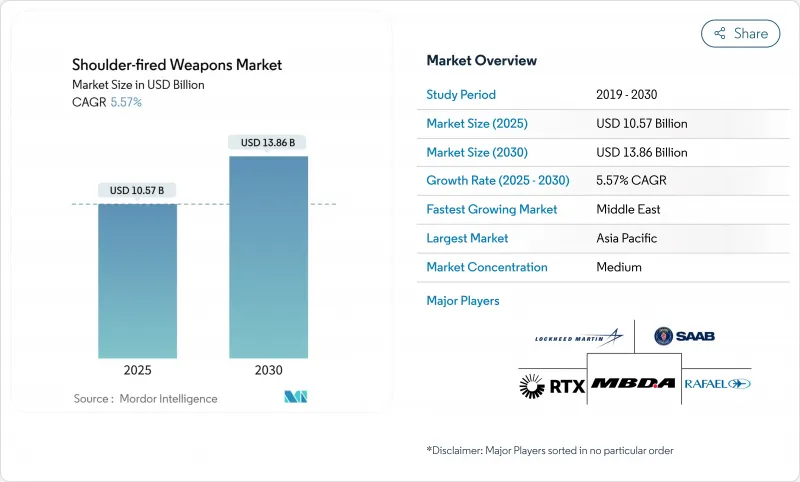

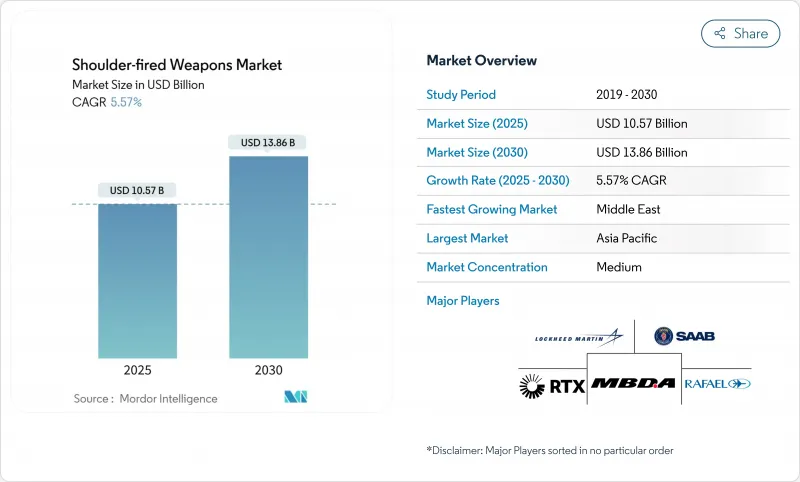

2025년 견착식 무기 시장은 105억 7,000만 달러로 평가되며, CAGR 5.57%를 나타내 2030년에는 138억 6,000만 달러에 달할 것으로 예상됩니다.

이 시장 규모의 확대를 뒷받침하는 것은 몇 가지 연동된 동향입니다. 첫째, 보병부대는 현재 인구밀집지 내의 중장갑, 무인 항공기, 요새화된 진지에 직면하고 있습니다. 휴대형 정밀 발사 장치에 의해 보병 부대는 포병이나 항공 병력을 기다리지 않고 대응할 수 있습니다. 둘째, 러시아와 우크라이나 전쟁에 의해 조달이 평시 페이스에서 급증 생산으로 이동하고 휴면 상태에 있던 미사일 라인이 재개되어 공급자는월생산량을 3배에서 4배로 하도록 촉구되었습니다. 셋째, 아시아태평양의 프로그램은 독자적인 설계와 합작 사업을 중시하고 시커 일렉트로닉스와 고도화기관제유닛의 생산량을 끌어올리고 있습니다. 넷째, 국토 안보 기관이나 국경 경비대가, 저렴한 드론에 대항하기 위해, 휴대형 방공 시스템을 채용하는 케이스가 늘어나고, 최종사용자의 밑단이 퍼지고 있습니다. 마지막으로 더 가벼운 탄소섬유 발사관과 소프트 런치 프로 팔전 스테이지가 전투 부하를 줄이고 특수 작전 부대가 장거리 순찰에 멀티 롤 런처를 휴대하도록 장려하고 있습니다.

비정규군, 도시민병, 소규모 원정소대는 좁은 도로나 험한 골짜기에서 주력전차와 대치하는 경우가 늘고 있습니다. 2024년 이후 차세대 대전차 미사일의 세계적 획득은 37% 증가했고, 그 필두는 서브의 NLAW 생산량의 4배 증가와 록히드 마틴의 자벨린 출하량의 2.5배 증가했습니다. 프로그램 가능한 탠덤 탄두, 최소 사거리의 단축된 퓨즈, 소프트 런치 모터로 하차한 분대는 백블라스트에 몸을 노출시키지 않고 반응 장갑을 깨뜨릴 수 있습니다. 따라서 견착식 무기 시장은 중편대보다 보병에 의존하는 모든 전선으로부터 혜택을 받습니다.

주권에 대한 우려가 높아짐에 따라 즉각적인 화력에 많은 자본 예산을 할당하도록 의회가 움직이고 있습니다. 아시아태평양의 방위비는 2023년에는 4,110억 달러에 이르렀고, 일본은 2025년 납품을 목표로 칼 구스타프 런처를 300기 조달해 인도는 인간 휴대형 ATM을 완성시킵니다. 핀란드와 스웨덴이 북극 여단을 개편하는 북유럽과 경량 런처가 미사일 실드를 보완하는 걸프 지역에서도 비슷한 궤도가 그려져 있습니다. 장기적인 산업계획은 시커 생산과 국내 최종 조립을 통합하여 전자기기 기업을 견착식 무기 시장으로 끌어들이는 동시에 공급망을 최종 사용자 가까이에 고정시킵니다.

미군수품 목록과 미사일 기술관리제도는 숄더링 미사일과 시커전자기기 수출을 제한하고 있습니다. 수출자는 최종 사용자 증명서를 확보해야 하며 리드 타임을 늦추고 컴플라이언스 비용을 상승시킵니다. NATO와 제휴하지 않은 구매자는 중국 공급업체로 옮기거나 보다 단순한 무반동 소총을 선택하는 경우가 많으며, 견착식 무기 시장의 기준선 성장에서 0.7% 포인트 깎여 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

유도 솔루션은 2025년 중 71억 9,000만 달러의 수익을 올리고 견착식 무기 시장의 69.45%를 차지할 것으로 예상됩니다. 한때 대형 미사일 전용이었던 소형 이미지 시커와 관성 항법 칩의 통합으로 보병은 응사 범위 밖에서 이동하는 장갑을 격파할 수 있게 되었습니다. 무유도 시스템의 견착식 무기 시장 규모는 CAGR 7.89%를 나타낼 전망입니다. 한국의 Raybolt 블록 업그레이드는 광섬유 데이터 링크와 5km의 스탠드오프가 가능한 모터를 융합시킨 것으로, 국산 R&D가 어떻게 기술 격차를 줄이고 있는지를 보여줍니다. 무유도 로켓은 비용보다 정확도가 우선하는 경우 여전히 매력적입니다. 그러나 새로운 부드러운 점심 디자인과 프로그래밍 가능한 퓨즈는 유도탄이 좁은 도시의 골목에서도 더 안전해지고 반응 장갑에 더 유리해지기 때문에 점유율이 해마다 축소되고 있습니다.

군인이 장착하는 서멀 사이트의 채용률이 상승함에 따라 조달은 더욱 유도탄에 기울어지고 있습니다. 클라우드 기반 교육 지원 도구를 통해 운영자 자격 취득이 몇 달이 아닌 며칠로 단축되어 신병이 첫 번째 배치 사이클에서 고급 미사일을 효과적으로 발사할 수 있습니다. 생산량이 증가하고 단가가 감소함에 따라 전환이 가속화됩니다. 전반적으로 경쟁 차별화는 추진 하드웨어에서 소프트웨어 정의 시커로 이동하여 견착식 무기 시장에 진입하는 소규모 전기 광학 기업에 비옥 한 토양을 공급합니다.

대전차 유도탄 발사기는 견착식 무기 시장 점유율의 35.51%를 차지하고 있습니다. 그 지속적인 매력은 우크라이나처럼 장갑 부대에 대한 살상력이 입증되었기 때문입니다. 이 범주에서는 지속적으로 블록 업그레이드가 진행되고 있습니다. 자벨린의 경량 CLU와 탄두는 2025년까지 미국 편대에 착탄합니다. 2025년에는 규모가 작아지며, MANPADS는 무인 항공기 위협과 전방 기지 주변의 비용 효과적인 돔 방어의 필요성에 힘입어 8.72%의 가장 높은 부문 CAGR을 나타낼 전망입니다. 에스토니아의 대규모 Piorun 프레임 워크 계약은 현대 어깨 쏘는 방공 도구에 대한 유럽의 의지를 보여줍니다.

무반동 소총은 신형 탄환이 조약에 저촉되지 않고 대구조물의 펀치를 주기 때문에 새로운 관심을 모으고 있습니다. 미국 육군이 1,600만 달러를 던져 칼 구스타프 M4를 주문한 것은 이 동향을 뒷받침하는 것입니다. RPG와 SLAW의 범주는 예산에 제약이 있는 군에서는 관련성을 유지하고 있지만, 보다 스마트한 시스템에 상대적인 성장을 빼앗기고 있습니다. 그러므로 견착식 무기 시장은 단일 발사 장비 제품군에서 멀티미션 페이로드, 모듈러 발사관, 전자 퓨즈 프로그래밍에 기울고 있습니다.

아시아태평양의 매출은 27억 달러로, 2025년 세계 매출의 32.47%에 해당하며, 견착식 무기 시장에서 가장 규모가 큰 지역 슬라이스를 유지하고 있습니다. 남중국해와 히말라야 산맥의 변경에서의 영토분쟁이 각국 정부를 보병에 신뢰할 수 있는 대무기 억제력을 장비하도록 촉구하고 있습니다. 일본의 2025년 칼 구스타프 발주는 40년 이상 전에 실전 배치된 재고를 근대화하는 것입니다. 필리핀은 자벨린을 추구하는 반면, 그레이존으로의 침공을 막기 위해 브라흐 모스의 육상 미사일을 통합합니다. 인도의 MPATGM 시험 비행은 주야간에 관계없이 이미징과 최고 공격 프로파일을 특징으로하며 국내 공급망의 성숙을 시사합니다. 이러한 사건은 휴대용 정밀 무기에 대한 지속적인 요구를 시사하고 지역 공동 생산 거래의 파이프라인을 유지하는 것입니다.

북미는 강력한 수요를 유지하고 있지만 진화하고 있습니다. 우크라이나로의 대규모 이전 이후 미국은 자베린, 스팅거, 튜브 발사 시스템을 록히드 마틴, RTX, 노스롭 그라만과의 다년간 계약을 지지하는 의무화된 준비 수준으로 회복시켜야 합니다. 새로운 자벨린 경량 런처는 2025년에 취역해 북극부대의 한랭지에서의 신뢰성을 향상시킵니다. 캐나다는 NATO의 탄약 호환성 목표에 맞추기 위해 칼 구스타프 보유 무기의 증강을 계획하고 있습니다. 그 결과, 북미의 견착식 무기 시장은 보충과 근대화 모두에서 혜택을 받게 됩니다.

유럽 시장의 양상은 2024년 2월 이후 가장 변화했습니다. NATO 국가들은 분쟁 초기에 재고를 비우고 긴급한 작전 요구를 내렸습니다. 라인 메탈은 MBDA와 제휴하여 레이저 대 드론 포드를 개발하여 중층 방어 생태계를 제안했습니다. 영국의 자벨린 대체 프로그램은 탱크의 활성 보호 시스템을 우회하는 차세대 라운드를 추구합니다. 폴란드는 자베린을 추가로 조달하고 공급 리스크를 헤지하기 위해 국산 필라테 ATM을 추구하고 있습니다. 따라서 유럽은 대량 구매 국가이자 기술 인큐베이터이기도합니다.

중동 및 아프리카의 견착식 무기 시장은 2030년까지 연평균 복합 성장률(CAGR) 9.61%를 나타낼 전망입니다. 이스라엘이 아이언 돔, 다윗 슬링, 아이언 빔을 52억 달러로 포괄 계약한 것은 이 지역의 중층 방공에 대한 투자 의욕을 뒷받침합니다. 튀르키예의 로케샹은 카라오크 미사일의 50m 급하강 킬 프로파일을 시연해 국내의 기술 혁신 능력을 증명하는 동시에 걸프 국가 고객에게 수출을 뒷받침했습니다. 아프리카 수요는 다양하며 기존 공급업체가 수출 규제 지연에 직면하는 반면 중국 기업은 서아프리카에 쇼룸을 설치하고 장갑차에 QN-202 런처를 번들하고 있습니다. 이러한 움직임은 남쪽 호의 지속적인 성장을 시사합니다.

라틴아메리카는 비즈니스 기회로서는 작지만, 국경의 긴장과 반범죄 작전에 힘입어 일시적인 급성장을 나타내고 있습니다. 칠레는 산악 보병을 위해 Spike SR 탄을 평가하고 브라질은 Astros II MLRS를 Alacran 일회용 대 구조물 발사기로 보완합니다. 예산의 역풍이 대규모 인수를 억제하고 있지만, 군비의 합리화 계획에서는 비축되고 있는 레거시 RPG를 신형의 무반동 라이플총으로 전환할 가능성이 있습니다.

The shoulder-fired weapons market is valued at USD 10.57 billion in 2025 and is projected to reach USD 13.86 billion by 2030, reflecting a 5.57% CAGR.

Several interlocking trends sustain this expansion in market size. First, infantry units now face heavy armor, drones, and fortified positions inside densely populated areas; portable precision launchers let them respond without waiting for artillery or airpower. Second, the Russia-Ukraine war shifted procurement from peacetime pacing to surge production, reopening dormant missile lines and prompting suppliers to triple or quadruple monthly output. Third, Asia-Pacific programs emphasize indigenous design and joint ventures, lifting volumes for seeker electronics and advanced fire-control units. Fourth, homeland-security agencies and border guards increasingly adopt man-portable air-defense systems to counter cheap drones, widening the end-user base. Finally, lighter carbon-fiber launch tubes and soft-launch propulsion stages cut combat loads, encouraging special-operations forces to carry multi-role launchers on long-range patrols.

Irregular forces, urban militias, and small expeditionary platoons increasingly face main battle tanks inside narrow streets and rugged valleys. Since 2024, global acquisitions of next-generation anti-tank missiles rose 37%, spearheaded by Saab's fourfold boost to NLAW output and Lockheed Martin's 2.5-times increase in Javelin shipments. Programmable tandem warheads, reduced minimum-range fuzes, and soft-launch motors allow dismounted squads to defeat reactive armor without exposing themselves to backblast. The shoulder-fired weapons market, therefore, benefits from every frontline that relies on infantry over heavy formations.

Rising sovereignty concerns move parliaments to allocate larger capital budgets for quick-reaction firepower. Asia-Pacific defense outlays climbed to USD 411 billion in 2023, with Japan procuring 300 Carl-Gustaf launchers for 2025 delivery and India perfecting its man-portable ATGM. Similar trajectories appear in Northern Europe, where Finland and Sweden revamp Arctic brigades, and in the Gulf, where lightweight launchers complement layered missile shields. Long-term industrial plans bundle seeker production with domestic final assembly, pulling electronics firms into the shoulder-fired weapons market while anchoring supply chains close to end-users.

The US Munitions List and the Missile Technology Control Regime restrict the transfer of shoulder-launched missiles and seeker electronics. Exporters must secure end-user certificates, delay lead times, and raise compliance costs. Buyers not aligned with NATO often shift toward suppliers in China or opt for simpler recoilless rifles, shaving 0.7 percentage points from baseline growth in the shoulder-fired weapons market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Guided solutions generated USD 7.19 billion in revenue during 2025, representing 69.45% of the shoulder-fired weapons market. Integration of compact imaging seekers and inertial navigation chips, once exclusive to larger missiles, allows infantry to defeat moving armor from outside return-fire range. The shoulder-fired weapons market size for unguided systems will grow at a 7.89% CAGR trajectory. South Korea's Raybolt block upgrade blends a fiber-optic data-link with a motor capable of 5 km standoffs, showing how indigenous R&D narrows technology gaps. Unguided rockets still appeal where cost trumps accuracy. Yet, their share shrinks yearly because new soft-launch designs and programmable fuzes make guided rounds safer in tight urban alleys and better against reactive armor.

Rising adoption of soldier-worn thermal sights has further tilted procurement toward guided profiles. Cloud-based training aides now shorten operator qualification to days, not months, enabling conscripts to fire advanced missiles effectively during their first deployment cycles. The switchover accelerates as production volumes rise and unit prices fall. Overall, competitive differentiation moves from propulsion hardware to software-defined seekers, supplying fertile ground for smaller electro-optics firms to enter the shoulder-fired weapons market.

Anti-tank guided missile launchers represented 35.51% of the shoulder-fired weapons market share. Their sustained appeal stems from proven lethality against armored columns, as in Ukraine. The category receives continuous block upgrades: Javelin's lightweight CLU and warhead refresh land in US formations by 2025, breakingdefense.com. Though smaller in 2025, MANPADS will post the highest segment CAGR of 8.72%, buoyed by drone threats and the need for cost-effective dome defenses around forward bases. Estonia's large Piorun framework deal underlines European appetite for modern shoulder-fired air-defense tools.

Recoilless rifles enjoy renewed interest because new rounds give them anti-structure punch without breaching treaties. The US Army's USD 16 million Carl-Gustaf M4 order validates this trend. RPGs and SLAW categories maintain relevance in budget-constrained forces but lose relative growth to smarter systems. The shoulder-fired weapons market, therefore, tilts toward multi-mission payloads, modular launch tubes, and electronic fuze programming within a single family of launchers.

The Shoulder-Fired Weapons Market Report is Segmented by Technology (Guided and Unguided), Weapon Type (Recoilless Rifles, and More), Range (Short, Medium, and Long), Projectile (Launcher/Tube, Projectile/Missile, and Fire-Control and Sighting Systems), End-User (Army, Navy, Air Force, Special Operations Forces, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated USD 2.70 billion, equal to 32.47% of 2025 global revenue, and remains the largest regional slice of the shoulder-fired weapons market. Territorial disputes in the South China Sea and the Himalayan frontier push governments to equip infantry with credible anti-armor deterrents. Japan's 2025 Carl-Gustaf order modernizes an inventory fielded over four decades ago. The Philippines seeks Javelins while integrating BrahMos shore-based missiles to discourage gray-zone incursions. India's MPATGM test flights, featuring day/night imaging and top-attack profiles, signal a maturing domestic supply chain. These events suggest a durable requirement for portable precision weapons and sustain a pipeline of regional co-production deals.

North America maintains a strong but evolving demand. After large transfers to Ukraine, the United States must restore Javelin, Stinger, and tube-launched systems to mandated readiness levels, underpinning multi-year contracts with Lockheed Martin, RTX, and Northrop Grumman. A new Javelin lightweight launcher enters service in 2025, improving cold-weather reliability for Arctic units. Canada plans to augment its Carl-Gustaf holdings to align with NATO munition interchangeability goals. Consequently, the shoulder-fired weapons market in North America benefits from both replenishment and modernization.

Europe's market complexion shifted the most after February 2024. NATO states emptied inventories early in the conflict, then issued urgent operational requirements. Saab reacted by scaling NLAW output; Rheinmetall partnered with MBDA to develop laser counter-drone pods, hinting at a layered defense ecosystem. The UK's replacement program for Javelin seeks a next-generation round to bypass tank active-protection systems. Poland procured additional Javelins and pursues its home-grown Pirat ATGM to hedge supply risk. Europe, therefore, acts as both a volume buyer and a technology incubator.

The Middle East and Africa shoulder-fired weapons market will rise at a 9.61% CAGR to 2030. Israel's USD 5.2 billion umbrella contract for Iron Dome, David's Sling, and Iron Beam underscores regional willingness to invest in layered air defense. Turkey's Roketsan demonstrated the Karaok missile's 50 m "dive" kill profile, proving domestic innovation capacity and supporting export pitches to Gulf clients. African demand is varied: while established suppliers face export-control delays, Chinese firms establish showrooms in West Africa, bundling armored vehicles with QN-202 launchers. These dynamics suggest sustained growth on the southern arc.

Latin America represents a smaller opportunity but shows episodic spikes, driven by border tensions and anti-crime operations. Chile evaluated Spike SR rounds for mountain infantry, while Brazil's army complements its Astros II MLRS with Alacran disposable anti-structure launchers. Budget headwinds temper large acquisitions, yet fleet rationalization plans could convert stockpiled legacy RPGs to newer recoilless rifles.