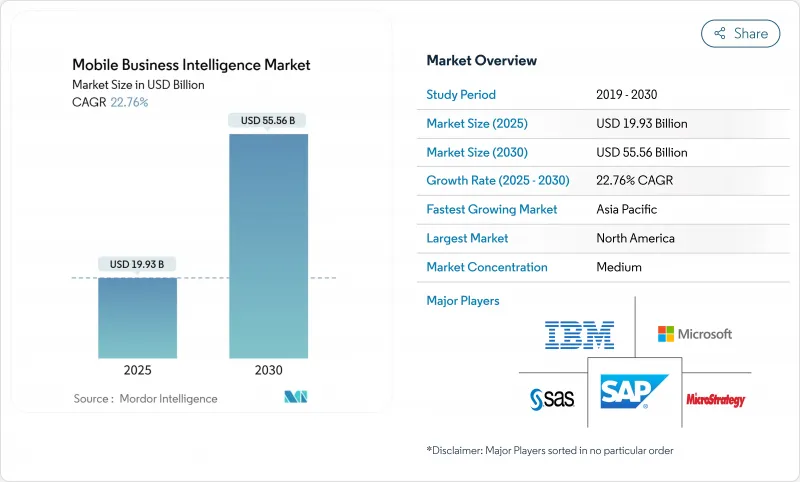

모바일 비즈니스 인텔리전스 시장 규모는 2025년 199억 3,000만 달러에 이르고, 2030년에는 555억 6,000만 달러로 확대될 것으로 예측됩니다.

이러한 성장은 분산된 직원이 실시간으로 인사이트를 바탕으로 행동할 수 있도록 고정 데스크톱 이외의 데이터 액세스를 민주화하는 긴급성을 반영합니다. 강력한 돌풍에는 대기 시간을 단축하는 5G의 성숙, 데이터 소스 근처에서 처리하는 엣지 컴퓨팅의 보급, 기술자가 아닌 사용자라도 쿼리 작성을 간소화할 수 있는 제네레이티브 AI의 도입 등이 있습니다. 소프트웨어 솔루션은 여전히 서비스를 능가하지만 기업이 복잡한 클라우드, AI 및 보안 요구 사항을 극복하면서 구현 및 관리 제공 제품에 대한 수요가 급속히 확대되고 있습니다. 북미는 모빌리티 프레임워크가 성숙하고 있기 때문에 주도권을 유지하고 있지만, 아시아태평양은 모바일 퍼스트의 지령 하에 현지 기업이 디지털 변혁을 가속화하고 있기 때문에 가장 상승 여지가 큽니다.

대기업은 On-Premise 스택을 클라우드 네이티브 모바일 BI로 전환하여 세계 직원들이 VPN을 통하지 않고 대시보드에 액세스할 수 있도록 합니다. 52,000개 이상의 기업이 Microsoft Power BI를 적극적으로 활용하고 Microsoft 365 워크스트림에 애널리틱스를 통합하고 있습니다. 이 마이그레이션은 서버 유지 관리가 필요 없으며 사용량이 많을 때 탄력적인 리소스를 확장하여 총 소유 비용을 절감합니다. SAP Analytics Cloud는 엄격한 ID 관리를 유지하면서 라이브 트랜잭션 데이터와 모바일 시각화를 연결합니다. 이 모델이 보급됨에 따라 모바일 비즈니스 인텔리전스 시장의 침투는 한때 클라우드 마이그레이션에 저항했던 규제 부문 전체에 퍼져 있습니다.

현재 아시아태평양 7개국에서 독립형 5G 네트워크가 운영되고 있으며 8,800억 달러에 이르는 아시아태평양의 모바일 경제를 지원하고 있습니다. 엣지 컴퓨팅은 처리를 로컬 게이트웨이로 옮기므로 모바일 대시보드는 밀리초 단위로 업데이트됩니다. 도쿄의 금융 트레이딩 데스크는 이미 핸드 헬드 장치에서 파생 상품 가격을 결정하기 위해 밀리 초 이하의 피드를 사용하고 있습니다. 이러한 예는 모바일 비즈니스 인텔리전스 시장에서 5G와 에지의 조합이 어떻게 사용 강도를 높이는 방법을 보여줍니다.

기업의 60%는 영업 성적 향상이 분명함에도 불구하고 보다 광범위한 BI 도입의 주요 장벽으로 모바일 보안을 꼽고 있습니다. BYOD 정책은 소비자와 기업의 앱이 혼합되어 있기 때문에 Apple의 새로운 개인정보 보호 매니페스트에서 부분적으로만 완화되는 정보 유출 위험이 증가하고 있습니다. 은행이나 병원에서는 모바일 BI를 회사 지급 휴대전화로 제한하는 경우가 많으며, 암호화나 생체인증 로그인이 개선되어도 고가치 분야에서의 보급이 늦어지고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년에 66.5%의 점유율을 획득한 시각화 도구, 쿼리 엔진 및 거버넌스 레이어를 제공하는 소프트웨어는 여전히 수익이 필요합니다. 이 제품은 대부분의 기업 분석 스택을 지원하며 ID 제품군, 데이터 웨어하우스, 로우코드 플랫폼과 통합됩니다. 그럼에도 불구하고 구현, 커스터마이즈, 관리 운영에 대한 수요가 급증하고 있기 때문에 서비스 제공업체는 라이선스 공급업체보다 빠르게 계약을 맺고 있습니다. 많은 고객은 대규모 언어 모델, 에지 배포 스크립트 및 제로 트러스트 제어의 미세 조정을 아웃소싱합니다. 모바일 비즈니스 인텔리전스 시장 규모는 기업이 순수한 소프트웨어 투자에서 성과 기반 계약으로 전환함에 따라 2030년까지 2자리 높은 CAGR을 나타낼 것으로 예측됩니다.

컨설팅 회사는 데이터 엔지니어링, 사용자 교육 및 배포 2일째 최적화를 번들로 제공하여 고객이 배포 직후에 가치를 끌어낼 수 있도록 합니다. 매니지드 서비스 파트너는 모바일 앱 패치 적용, 사용 현황 모니터링, 시맨틱 레이어 개선을 위해 여러 해 계약을 체결하여 비즈니스 부서는 플랫폼 관리가 아닌 인사이트 소비에 집중할 수 있습니다. MicroStrategy가 Google Cloud Marketplace에 게재된 것은 이 트렌드를 이야기합니다. 자동 프로비저닝은 도입 기간을 단축하고 인증 파트너가 지속적인 거버넌스를 제공합니다. 이러한 패턴은 셀프 서비스 툴이 개선되어도 서비스 풍부한 성장 호가 계속 될 가능성을 강화하고 있습니다.

대기업은 세계 비즈니스 배포, 풍부한 IT 직원 및 견고한 모바일 BI 제품군을 지원하는 컴플라이언스 의무를 갖고 있기 때문에 2024년 매출의 75.1%를 차지했습니다. 대기업은 ERP 및 CRM 워크플로우에 분석 그래프를 통합하여 수천 명의 직원이 현장에서 KPI를 추적할 수 있도록 합니다. 멀티테넌트 거버넌스, 싱글 사인온, 세분화된 역할 관리는 금융, 헬스케어, 공공 부문의 감사인을 만족시킵니다. 이러한 우위에도 불구하고, 턴키 SaaS가 진입 장벽을 낮추고 있기 때문에 현재 중소기업 분야가 가장 빠르게 확대되고 있습니다.

중소기업은 종량 과금 구독, 자동 스케일링 및 익숙한 생산성 제품군에 표시되는 마법사 기반 보고서 작성기를 높이 평가합니다. 중소기업용 모바일 비즈니스 인텔리전스 시장 규모는 비싼 온프레임 데이터베이스를 시작하지 않고도 현금 흐름, 재고 및 고객 감정을 즉시 시각화해야 하는 창업자의 요구에 따라 급증할 것으로 예측됩니다. 크로아티아의 조사 데이터에 의하면, 도입의 성패는 경영 톱에 의한 스폰서십과 명확한 실적 목표에 상관하고 있습니다. 앱 스토어가 Shopify, QuickBooks, Stripe에 빌드된 커넥터로 넘쳐나는 가운데 중소기업은 데이터 사이언스자를 고용하지 않고 데이터 중심의 문화에 참여할 수 있으며, 이 코호트가 모바일 비즈니스 인텔리전스 업계 전체를 능가하는 이유를 뒷받침하고 있습니다.

북미는 유비쿼터스 LTE-Advanced의 커버리지, 신속한 5G 배포, 모바일 보안 프레임워크에 대한 기업의 익숙함에 의해 2024년 세계 매출의 36.7%를 유지했습니다. 실리콘 밸리 벤더는 음성 쿼리 및 카메라 기반 데이터 캡처와 같은 새로운 기능을 세계 출시 전에 국내에서 시험적으로 도입하고 있으며, 이 지역의 생산성을 조기에 향상시키고 있습니다. Microsoft Entra ID와 Okta와의 긴밀한 통합은 데스크톱에서 휴대폰으로의 ID 전달을 간소화하고 활성 사용자 수를 증가시킵니다. 인건비가 높기 때문에 기업이 분석 주도의 효율성을 추구하는 동기 부여가 되어 모바일 비즈니스 인텔리전스 시장의 업그레이드를 위한 지속적인 예산 배분을 보장하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 23.2%를 나타낼 것으로 예측되어 눈에 띕니다. 이는 각국 정부가 5G 주파수 대역에 보조금을 내고 국경 내의 클라우드 지역에 유리한 데이터 현지화를 의무화하고 있기 때문입니다. 중국의 주요 전자상거래는 페타바이트 규모의 원격 측정을 실시간 대시보드로 전송하여 플래시 세일을 몇 분 안에 최적화합니다. 인도의 Unified Payments Interface는 매일 수십억 개의 트랜잭션을 분석 클라우드에 푸시하여 은행이 농촌 에이전트가 휴대하는 스마트폰으로 사기 모델을 개선할 수 있도록 합니다. ASEAN 제조업체의 대부분은 레거시 MES 시스템을 건너뛰고 모바일 대시보드를 먼저 채택하고 모바일 비즈니스 인텔리전스 시장 규모를 다른 어느 지역보다 빠르게 확장하는 리프플로그 효과를 보여줍니다.

유럽은 GDPR(EU 개인정보보호규정), 지속가능성 목표, 산업 5.0 전략의 중압 하에서 꾸준한 확대를 기록하고 있습니다. 유틸리티자는 모바일 BI를 이용해 재생에너지 발전을 감시하고, 자동차 제조업체는 핸드헬드 분석을 이용해 저스트 인 시퀀싱의 배송을 조정하고 있습니다. 엄격한 프라이버시 규칙은 가명화와 장치의 암호화를 촉구하고 개발의 복잡성을 높이지만 컴플라이언스 감사를 통과하는 공급업체의 차별화가 되었습니다. 한편, 라틴아메리카와 중동, 아프리카에서는 새로운 영역이 확산되고 있습니다. 브라질 PIX 즉시 결제 네트워크는 모바일 인사이트에 굶주린 핀테크에 행동 데이터를 제공합니다. 멕시코 걸프의 통신사는 기업용 데이터 플랜에 분석 대시보드를 번들하여 유전 운영자, 병원, 스마트 시티 관리자에게 원스톱 이동성 및 인텔리전스를 판매합니다.

The mobile business intelligence market size reached USD 19.93 billion in 2025 and will advance to USD 55.56 billion by 2030, translating to a 22.8% CAGR and confirming a rapid scale-up in enterprise spending on mobile analytics platforms.

This growth reflects the urgency to democratize data access beyond fixed desktops so that distributed employees can act on insights in real time. Strong tailwinds include 5G maturation that lowers latency, the spread of edge computing that keeps processing close to data sources, and the injection of generative AI that simplifies query creation for non-technical users. Software solutions continue to outsell services, yet demand for implementation and managed offerings expands quickly as firms wrestle with complex cloud, AI, and security requirements. North America retains leadership because of mature mobility frameworks, but Asia-Pacific offers the highest upside as local enterprises accelerate digital transformation under mobile-first mandates.

Large corporations are swapping on-premises stacks for cloud-native mobile BI so global staff can reach dashboards without VPN friction. More than 52,000 companies actively use Microsoft Power BI, embedding analytics into Microsoft 365 work streams. The shift lowers total cost of ownership because server upkeep disappears and elastic resources scale during peak usage. SAP Analytics Cloud similarly links live transactional data with mobile visualizations while preserving strict identity controls. As this model proliferates, mobile business intelligence market penetration deepens across regulated sectors that once resisted cloud migration.

Standalone 5G networks now run in seven Asia-Pacific countries, undergirding a USD 880 billion regional mobile economy that prizes responsive analytics. Edge computing moves processing to local gateways so mobile dashboards refresh in milliseconds, a necessity for factory predictive-maintenance alerts and retail shelf-stocking decisions. Financial-trading desks in Tokyo already exploit sub-millisecond feeds to price derivatives on handheld devices. These examples illustrate how 5G plus edge collectively raise usage intensity inside the mobile business intelligence market.

Sixty percent of enterprises cite mobile security as the main barrier to broader BI rollout despite clear sales-performance gains. BYOD policies mingle consumer and corporate apps, raising leakage risks that new Apple privacy manifests only partly mitigate. Banks and hospitals often restrict mobile BI to company-issued phones, slowing penetration in high-value verticals even as encryption and biometric log-ins improve.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software remains the revenue cornerstone, supplying visualization tools, query engines and governance layers that earned a 66.5% share in 2024. These offerings anchor most enterprise analytics stacks and integrate with identity suites, data warehouses and low-code platforms. Still, surging demand for implementation, customization and managed operations means service providers are booking faster contracts than license vendors. Many clients now outsource fine-tuning of large language models, edge-deployment scripts and zero-trust controls because internal teams lack bandwidth. The mobile business intelligence market size for services is projected to expand at high double-digit CAGR through 2030 as organizations shift from pure software spend toward outcome-based engagements.

Consulting firms bundle data engineering, user-training and day-two optimization so clients can unlock value soon after go-live. Managed-services partners sign multiyear agreements to keep mobile apps patched, monitor usage and refine semantic layers, freeing business units to focus on insight consumption instead of platform care. MicroStrategy's listing on Google Cloud Marketplace illustrates the trend: automated provisioning trims deployment timelines, while certified partners step in for ongoing governance. These patterns reinforce a service-rich growth arc likely to continue even as self-service tooling improves.

Large enterprises controlled 75.1% revenue in 2024 because they possess global operations, ample IT staff, and compliance obligations that favor robust mobile BI suites. They embed analytic graphs into ERP and CRM workflows so thousands of employees can track KPIs in the field. Multi-tenant governance, single sign-on, and fine-grained role controls satisfy auditors in finance, healthcare, and public-sector domains. Despite this dominance, the small-business segment now logs the briskest expansion as turnkey SaaS lowers entry barriers.

SMEs appreciate pay-as-you-go subscriptions, automated scaling, and wizard-based report builders that appear within familiar productivity suites. The mobile business intelligence market size for SMEs is forecast to climb steeply as founders seek instant visibility into cash flow, inventory, and customer sentiment without spinning up expensive on-prem databases. Croatian survey data shows that adoption success correlates with top-management sponsorship and clear performance targets. As app stores flood with pre-built connectors to Shopify, QuickBooks, and Stripe, smaller firms can join data-driven cultures without hiring data scientists, underscoring why this cohort will keep outpacing the overall mobile business intelligence industry.

The Mobile Business Intelligence Market Report is Segmented by Solution (Software and Services), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Application (Sales and Marketing Analytics, Finance and Risk Analytics, and More), End-User Vertical (BFSI, IT and Telecommunications, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America kept 36.7% of global revenue in 2024, anchored by ubiquitous LTE-Advanced coverage, swift 5G roll-outs, and enterprise familiarity with mobile security frameworks. Silicon Valley vendors pilot novel features-voice query, camera-based data capture-domestically before global releases, giving the region early productivity gains. Tight integrations with Microsoft Entra ID and Okta simplify identity propagation from desktop to phone, boosting active-user counts. High labor costs also motivate firms to chase analytics-driven efficiency, ensuring continued budget allocation for upgrades in the mobile business intelligence market.

Asia-Pacific stands out with a projected 23.2% CAGR through 2030 as governments subsidize 5G spectrum and mandate data-localization that favors cloud regions inside national borders. China's e-commerce giants stream petabyte-scale telemetry into real-time dashboards that optimize flash sales in minutes. India's Unified Payments Interface pushes billions of daily transactions into analytics clouds, letting banks refine fraud models on smartphones carried by rural agents. Many ASEAN manufacturers skip legacy MES systems and adopt mobile dashboards first, illustrating a leapfrog effect that expands the mobile business intelligence market size faster than any other region.

Europe posts steady expansion under the weight of GDPR, sustainability targets, and Industry 5.0 strategies. Utilities use mobile BI to monitor renewable generation, while carmakers rely on handheld analytics to coordinate just-in-sequence deliveries. Strict privacy rules encourage pseudonymization and on-device encryption, raising development complexity but also differentiating vendors that pass compliance audits. Meanwhile, Latin America and the Middle East and Africa open fresh territory. Brazil's PIX instant-payment network feeds behavioral data to fintechs hungry for mobile insights. Gulf telcos bundle analytics dashboards with enterprise data plans, selling one-stop mobility plus intelligence to oil-field operators, hospitals, and smart-city managers.