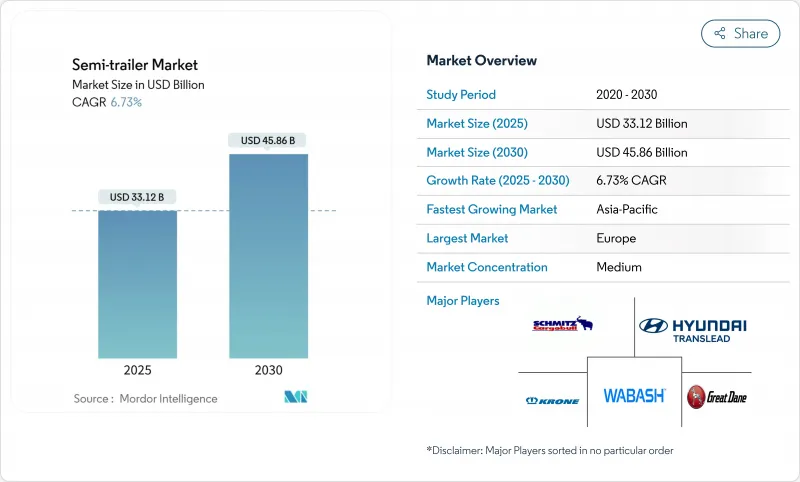

세계의 세미 트레일러 시장은 2025년에 331억 2,000만 달러로 평가되고, 2030년까지 458억 6,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 6.73%로 예상됩니다.

업계의 기세는 전자상거래에 의한 지역 유통망에 대한 끊임없는 영향, 제로 배출 화물에 대한 규제의 뒷받침, 트레일러 중심의 자동화에 대한 투자 증가에 기인하고 있습니다. 드라이 밴 유닛이 수량 리더를 유지하고 있지만, 콜드체인 활동이 확대됨에 따라 냉장 기기가 페이스를 잡고 있습니다. 전동 액슬, 첨단 텔레매틱스 및 공력 패키지가 점점 더 구매 기준을 형성하는 한편, 신흥 경제권의 인프라 정비 계획이 기준선의 차량 수요를 밀어 올리고 있습니다.

온라인 판매가 증가함에 따라 경로 밀도와 화물 규모가 변화하고 도시 중심부에서 조종하면서 지역 허브에 서비스를 제공할 수 있는 다재다능한 운전자 장비에 대한 통화율이 높아지고 있습니다. 플릿 매니저는 성수기 동안 능력을 유연하게 하기 위해 모듈형 바디를 추가하고, 텔레매틱스를 통해 승무원의 스케줄링 담당자는 밀집한 회랑에서의 트럭 지연이 대유행 전의 레벨을 넘어서 도심의 혼잡을 피할 수 있습니다. 택배 및 소포 운송업체는 내부 높이를 극대화하는 하이큐브 트레일러의 사양을 늘리는 경향이 있으며 공급업체는 강성을 희생하지 않고 용기 무게를 줄이기 위해 복합재 패널을 채택하도록 촉구하고 있습니다. 이러한 화물은 한 시점을 다투기 때문에 운송업자는 고장이 발생하기 전에 도어 씰의 마모와 휠 엔드의 발열을 알리는 예비 보전 센서가 있는 장비를 선호합니다. 이러한 변화로 인해 세미 트레일러 시장은 익일 배송에 대한 소비자의 기대 변화와 밀접하게 연동합니다.

가처분 소득 증가와 의약품 유통은 세계적인 냉장 트레일러 수요를 밀어 올리고 있습니다. 유럽의 콜드체인 생태계는 이미 8,000억 유로의 상업을 지원하고 2,900만 명 이상의 직원을 고용하고 있습니다. Carrier Transicold의 새로운 Vector HE17 냉동 유닛은 기존 시스템에 비해 연료 소비량을 30% 줄이고, 화물주는 적재량을 희생하지 않고 엄격한 배출 규제를 충족할 수 있습니다. 소매업체와 Biocoop과 같은 협동조합 식료품점은 2030년까지 리퍼 장비의 3분의 1 가까이를 전동화하고 속삭이는 소리와 같은 조용한 작업을 활용하여 야간 배송 프레임을 이용할 것을 약속하고 있습니다.

차입 비용의 상승은 갱신 사이클을 지연시킵니다. 이는 2025년 1분기 Wabash National의 매출이 26.1% 감소했으며, 수주가 선대 유지 요구를 밑돌았다는 사실이 입증되었습니다. 소규모 운송 회사에는 저렴한 신용 프레임이 없기 때문에 자본 액세스가 뛰어난 구매자가 경영난에 빠진 경쟁사를 풀어 통합을 촉구합니다. OEM은 유지보수가 있는 장기 임대에 대응하고 있지만, 잔존가치 리스크가 높아지면 총소유비용을 높여 세미 트레일러 시장의 단기적인 성장을 억제하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

드라이버 플랫폼은 보편적인 인테리어가 일반 상품, 팔레트 포장기, 포장된 소비재에 적합하기 때문에 2024년 세미 트레일러 시장에서 55.21%의 점유율을 유지했습니다. 운전자 플랫폼은 대형 소매업체와 계약 운송업체 간에 예측 가능한 교환 사이클을 지원하며 안정적인 제조율을 유지합니다. 하지만 냉장 부문은 급속한 전자상거래와 백신 물류를 통해 2030년까지 9.14%의 연평균 복합 성장률(CAGR)을 그렸습니다. Carrier Transicold의 모든 전기식 Vector eCool과 같은 장비는 직접 배출을 0으로 줄이고 운영자를 저소음 다운타운 구역에 진입시킵니다.

세미 트레일러 시장에서 플랫베드와 로우보이가 인프라 자금 조달주기를 타는 반면, 유조선 수요는 화학물질과 연료 처리량을 추적하고 규제 감독에 의해 설계가 복잡해지고 있습니다. 북미에서는 도난 억제를 위해 풀 인클로저 차체가 우선되지만, EU에서는 사이드로딩 효율을 중시해 커튼 사이더의 채용이 여전히 현저합니다. 예측 온도 경보가 있는 텔레매틱스 대응 냉동차를 제공하는 OEM은 화물 무결성이 스티커 가격을 능가하는 상황에서 차별화를 도모하고 있습니다. 그 결과, 냉장 카테고리가 세미 트레일러 시장 전체의 사양 혁신의 조타를 하고 있습니다.

25-50톤의 트레일러는 매출의 38.26%를 차지하고 특별한 허가 없이 지역을 가로지르는 레인을 가로지르는 다용도성에 힘입어 8.23%의 확대율을 유지하고 있습니다. 오퍼레이터는 3축 트랙터와 표준 고속도로 다리에 매치하는 이 유닛을 높이 평가하여 무거운 리그가 야기하는 통행료의 요금을 절감하고 있습니다. 이 클래스의 세미 트레일러 시장 규모는 2030년까지 203억 달러에 이르는 것으로 짐이 균형 잡힌 적재 효율에 기여하기 때문입니다.

더 무거운 51-100톤의 로우보이는 에너지와 건설의 메가 프로젝트에 공급되지만, 주기적인 상품 지출에 좌우됩니다. 100톤을 초과하는 모듈은 풍력 터빈 블레이드와 정제 배에 필수적이지만 여전히 틈새 시장입니다. 제로 배출 트랙을 44톤까지 끌어올리는 EU의 제안은 수요 곡선을 재구성할 수 있지만, 인프라 비용 우려가 완전한 조화를 늦출 수 있습니다. 그 결과 세미 트레일러 시장에서는 예측 기간 동안 고중량 플랫폼이 계속 대수를 지원할 것으로 보입니다.

성숙한 도로망, 밀집한 국경을 넘은 무역, 조기 배출규제가 로테이션 갱신을 자극하기 위해 유럽은 2024년 세계 수익의 35.22%를 차지했습니다. EU의 CO2 기준은 트레일러의 효율성을 2025년까지 15%, 2040년까지 90%까지 개선할 의무가 있으며, 구매자는 공기 역학적 스커트, 낮은 구름 저항 타이어, 전동 액슬로 유도됩니다. 세미 트레일러 시장은 2010년 이후 59% 확대해 국경을 넘은 체류 시간을 낮게 억제하고 있는 철도와 도로의 동기 복합 수송의 혜택을 계속 받고 있습니다. 그러나 전동 콤바인에 제안된 무게 증가는 인프라 비용 논의와 도로로의 모달 이동 가능성을 유발하고 조달 사이클에 신중한 감정을 주입하고 있습니다.

아시아태평양은 CAGR 7.68%로 두드러지며, 중국의 지속적인 고속도로 건설과 인도의 화물 운송 코리도 전개에 추진되고 있습니다. CIMC Vehicles는 2024년 상반기에 107억 위안 매출을 기록했으며 Starlink 최적화 프로그램 하에서 세미 트레일러 매출이 24.67% 증가했습니다. 인도의 트럭에 중점을 둔 국가 물류 정책은 물류 비용을 GDP의 10% 미만으로 압축하는 것을 목표로 하고 있으며, 이 변화는 아대륙에서의 자산 회전율을 높여 지역 세미 트레일러 시장을 확대할 것으로 예측됩니다. 일본에서는 Hino와 Mitsubishi Fuso의 OEM 통합이 추진되어 경쟁상의 긴장이 높아집니다.

북미는 2025년 클래스 8 트랙터 판매 대수가 25만-28만대로 예측됨과 함께 2030년까지 제로 배출 상용차 판매 대수의 30%를 목표로 하는 정책의 청사진에 힘입어 견조한 기반을 유지합니다. PACCAR는 애프터마켓 부품의 매출이 66억 7,000만 달러로 과거 최고를 기록했다고 보고하고 노후화된 트레일러 풀의 이용이 호조를 보이고 있습니다. 그러나 수입 트럭에 대한 25% 관세가 예정되어 트레일러 가격이 9% 상승하고 수요가 17% 감소할 수 있습니다. 남미는 도로화물에 크게 의존하고 있으며, 브라질은 화물의 65%를 트럭으로 운송하고 있습니다. 한편 중동 및 아프리카 시장은 개발은행이 운송회랑에 자본을 주입함에 따라 기세를 늘리고 있으며, 세계 각지역의 세미 트레일러 시장의 미묘한 전망을 형성하고 있습니다.

The semi-trailer market size is valued at USD 33.12 billion in 2025 and is forecast to reach USD 45.86 billion by 2030, translating into a 6.73% CAGR over the period.

Industry momentum stems from e-commerce's relentless pull on regional distribution networks, regulatory pushes for zero-emission freight, and rising investments in trailer-centric automation. Dry van units uphold volume leadership, yet refrigerated equipment sets the pace as cold-chain activity broadens. Electrified axles, advanced telematics, and aerodynamic packages increasingly shape purchase criteria, while infrastructure programs across emerging economies lift baseline fleet demand.

Online sales growth reshapes route density and shipment size, intensifying call-off rates for versatile dry-van equipment that can service regional hubs while maneuvering in urban cores. Fleet managers add modular bodies to flex capacity for peak seasons, and telematics enable crew schedulers to avoid city-center congestion as truck delays in dense corridors exceed pre-pandemic levels . Courier and parcel operators increasingly spec high-cube trailers that maximize internal height, prompting suppliers to adopt composite panels to trim tare weight without sacrificing stiffness. Because this freight is time-critical, carriers favor equipment with predictive-maintenance sensors that flag door seal wear and wheel-end heat before failures occur. Together, these changes keep the semi-trailer market in close alignment with shifting consumer expectations for next-day delivery.

Rising disposable incomes and pharmaceutical distribution push refrigerated trailer demand worldwide. Europe's cold-chain ecosystem already supports EUR 800 billion in commerce and employs over 29 million people, underscoring the structural scale of temperature-controlled freight . New Vector HE 17 refrigeration units from Carrier Transicold cut fuel burn by 30% relative to legacy systems, letting shippers meet tightening emission ceilings without sacrificing payload. Retailers and cooperative grocers such as Biocoop have pledged to electrify nearly one-third of reefer equipment by 2030, leveraging whisper-quiet operations to access night-time delivery slots.

Elevated borrowing costs delay replacement cycles, evidenced by Wabash National's 26.1% revenue drop in Q1 2025 as orders fell below fleet sustainment needs. Smaller carriers lack inexpensive credit facilities, prompting consolidation as buyers with superior capital access scoop distressed competitors. OEMs respond with extended-term leases bundled with maintenance, though higher residual-value risk inflates the overall cost of ownership, tempering near-term semi-trailer market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Dry van platforms kept a 55.21% share of the semi-trailer market in 2024 as their universal interior fits general merchandise, palletized machinery, and packaged consumer goods. They anchor predictable replacement cycles among big-box retailers and contract carriers, sustaining steady build rates. Nevertheless, the refrigerated segment is charting a 9.14% CAGR to 2030, catalyzed by rapid grocery e-commerce and vaccine logistics. Equipment such as Carrier Transicold's all-electric Vector eCool cuts direct emissions to zero, letting operators enter low-noise downtown zones.

The semi-trailer market also sees flatbeds and lowboys ride infrastructure funding cycles, whereas tanker demand tracks chemical and fuel throughput, with regulatory oversight adding design complexity. Curtain-sider adoption remains pronounced in the EU for side-loading efficiency, though North America prioritizes full-enclosure bodies for theft deterrence. OEMs that deliver telematics-ready reefers with predictive temperature alerts differentiate in a landscape where load integrity trumps sticker price. As a result, the refrigerated category steers overall specification innovation within the semi-trailer market.

Trailers rated 25-50 ton hold 38.26% of revenues and maintain an 8.23% expansion rate, underpinned by versatility across cross-regional lanes without special permits. Operators prize these units for matching three-axle tractors and standard highway bridges, cutting toll surcharges that heavier rigs attract. The semi-trailer market size for this class is set to reach USD 20.3 billion by 2030 as shippers gravitate toward balanced payload efficiency.

Heavier 51-100 ton lowboys serve energy and construction megaprojects but hinge on cyclic commodity spending. Above-100-tonne modules remain niche, albeit critical for wind-turbine blades and refinery vessels. EU proposals to lift zero-emission truck combos to 44 tonnes could reshape demand curves, yet infrastructure cost concerns may delay full harmonization. Consequently, mid-weight platforms will continue to anchor volume in the semi-trailer market through the forecast horizon.

The Semi-Trailer Market Report is Segmented by Vehicle Type (Flat Bed, Dry Van, and More), Tonnage (Below 25 Ton, 25 Ton - 50 Ton, and More), Foot Length (28-45 Ft and Above 45 Ft), End-Use Industry (Transportation and Logistics, Food and Beverage, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Europe anchored 35.22% of global revenue in 2024 as mature road networks, dense cross-border trade, and early emissions legislation stimulate rotational renewals. EU CO2 standards mandate trailer efficiency improvements of 15% by 2025 and up to 90% by 2040, channeling buyers toward aerodynamic skirts, low-rolling-resistance tires, and electrified axles. The semi-trailer market continues to benefit from synchronized rail-road combined transport, which has expanded 59% since 2010, keeping cross-border dwell times low. However, weight increases proposed for electric combinations trigger infrastructure cost debates and potential modal shifts back toward road, injecting cautious sentiment into procurement cycles.

Asia-Pacific stands out with a 7.68% CAGR, propelled by China's sustained highway build-out and India's freight-corridor rollouts. CIMC Vehicles booked 10.7 billion RMB revenue in H1 2024 and logged a 24.67% lift in semi-trailer sales under its Starlink optimization program, underscoring local production agility. India's truck-focused National Logistics Policy aims to compress logistics costs to under 10% of GDP-a change expected to swell the regional semi-trailer market by lifting asset turnover on the subcontinent. Japan's push for OEM consolidation between Hino and Mitsubishi Fuso adds competitive tension.

North America retains a solid base, buoyed by 250,000-280,000 projected Class 8 tractor sales in 2025 and a policy blueprint that targets 30% zero-emission commercial vehicle sales by 2030. PACCAR reports record USD 6.67 billion aftermarket parts turnover, signaling strong utilization of aging trailer pools. Yet prospective 25% tariffs on imported trucks could drive trailer price inflations of 9% and dent demand by 17%. South America relies heavily on road freight-Brazil moves 65% of goods by truck-while Middle East and Africa markets gain momentum as development banks funnel capital into transport corridors, altogether shaping a nuanced outlook for the semi-trailer market across global regions.