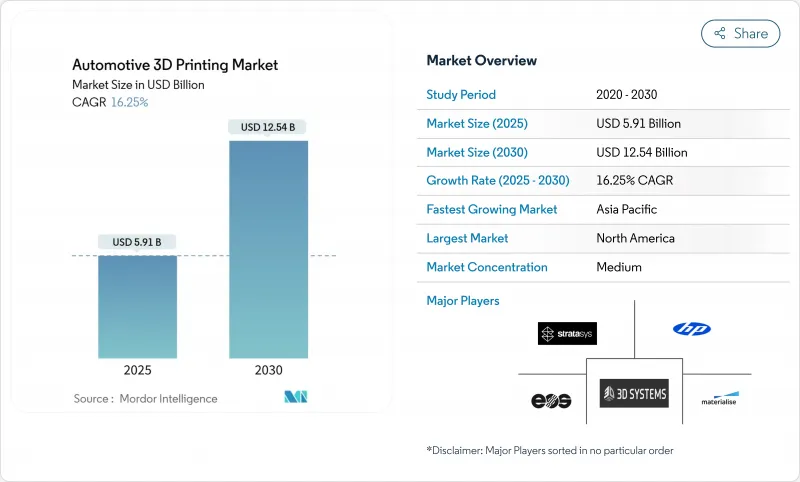

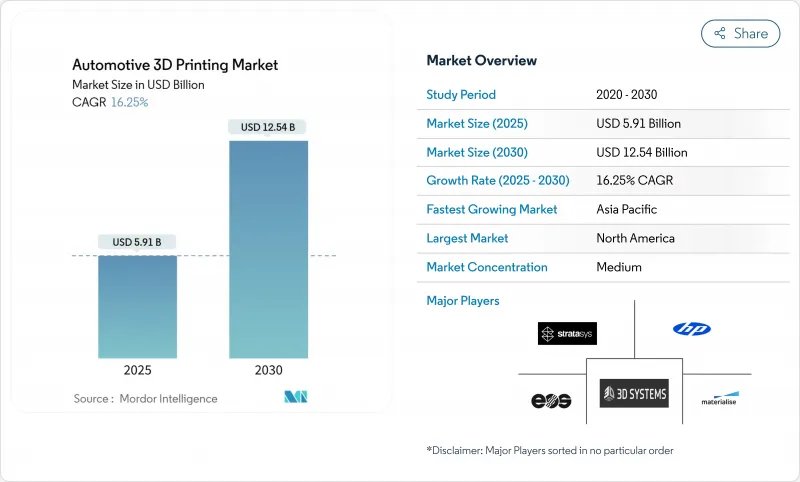

자동차 3D 프린팅 시장의 2025년 시장 규모는 59억 1,000만 달러이며, CAGR 16.25%를 반영하여 2030년에는 125억 4,000만 달러에 이를 것으로 예측됩니다.

멀티 머티리얼 가공, 디지털 공급망 오케스트레이션, 인공지능 기반 품질 관리의 혁신이 제조 경제를 재정의하는 가운데, 프로토타이핑에서 대량 생산으로의 전환이 가속화되고 있습니다. 와이어 아크 적층 가공를 통한 BMW의 27% 배기가스 배출량 감소에서 알 수 있듯이, 엄격한 배기가스 규제를 충족하는 경량화 부품에 대한 수요가 성장을 뒷받침하고 있습니다. 용융 적층 가공(FDM)와 선택적 레이저 소결(SLS) 하드웨어의 발전은 처리량을 향상시키고, 비용 효율적인 철 실리콘 분말은 전기자동차(EV) 모터 부품의 금속 응용 분야를 개척할 것입니다. 규제 압력, 온쇼어링 전략, 지속 가능한 원료의 가용성은 기존 및 신흥 경제권 전체에서 자동차 3D 프린팅 시장을 확대할 것입니다.

전기차 제조업체들은 주행거리를 늘리고 배기가스 규제를 준수하기 위해 무게의 최적화를 추구하고 있습니다. General Motors는 Cadillac Celestiq에 130개 이상의 인쇄 부품을 내장하고 있으며, 그 중에는 자동차 생산에서 가장 큰 적층 가공 알루미늄 부품도 포함되어 있습니다. 유럽의 유로 7 규제로 인해 브레이크 디스크의 코팅 및 구조 요소의 채택이 가속화되었습니다. 모래 기반 3D 프린팅은 금형 개발 주기를 단축하고, 공차 목표를 유지하면서 질량을 줄이는 주조 설계를 가능하게 합니다. 배터리 무게를 상쇄해야 하기 때문에 차량 플랫폼 전체에서 1g이라도 더 경량화하려는 경쟁이 치열해지고 있습니다.

적층 가공가 기계 가공을 대체하여 초기 단계의 설계 반복을 수행함으로써 시제품의 리드 타임을 최대 90%까지 단축하고, 단일 부품의 비용을 크게 절감할 수 있다고 보고하고 있습니다. 스테레오 리소그래피의 높은 치수 정확도는 저비용 인베스트먼트 주조를 대체할 수 있으며, AI 기반 조형 파라미터 최적화를 통해 첫 번째 성공률을 높일 수 있습니다. 3,000달러 이하의 데스크톱 SLS 프린터는 중소 공급업체의 접근성을 확대하고 아시아태평양 제조 클러스터의 혁신 주기를 단축할 수 있습니다.

산업용 SLS 프린터의 가격은 12,000-3만 3,000달러인 반면, 특수 금속 분말의 평균 가격은 1kg당 300-600달러로, 비용에 민감한 공급업체들의 채택이 제한적입니다. 헬륨 원자화 분말 생산은 가장 지속 가능한 경로를 제공하지만 자본 지출은 여전히 큽니다. 수명주기 분석에 따르면, 분말층 용융법은 복잡도가 높은 부품의 경우 경제성이 높지만 초기 투자 비용이 커서 광범위하게 도입하기 어렵습니다. 저가의 금속 필라멘트 공정은 진입장벽을 완화시키지만, 후처리의 복잡성이 증가하여 자동차 3D 프린팅 시장의 CAGR을 2.4% 낮출 것으로 예측됩니다.

보고서에서 분석된 기타 촉진 및 억제요인은 다음과 같습니다.

FDM은 낮은 시스템 비용과 다양한 재료 선택으로 2024년 자동차 3D 프린팅 시장 점유율 38.32%를 차지했습니다. SLS는 3,000달러 이하의 데스크톱형 파우더 베드 시스템이 고성능 나일론 및 복합소재 프린팅을 대중화함에 따라 2030년까지 연평균 18.53%의 성장률을 보일 것으로 예측됩니다. 나노 스케일 광중합의 발전으로 스테레오 리소그래피의 해상도는 초당 100µm으로 100nm까지 향상되었으며, 마이크로플루이딕스 및 광학 응용 분야에도 활용이 확대되고 있습니다. 디지털 라이트 프로세싱(DLP)은 점점 더 많은 보석 및 치과용 모델을 지원하고 전자빔 용해는 항공우주용 티타늄 부품에 도움이되고 있습니다. SLS 기반 부품의 자동차 3D 프린팅 시장 규모는 전기차 제조업체들이 내구성이 높은 나일론 소재의 기어와 언더후드 부품을 채택함에 따라 급성장할 것으로 예측됩니다.

적층제조와 서브트랙티브 기술을 융합한 하이브리드 제조가 부상하고 있습니다. FDM 툴 패스는 연속 섬유 강화 재료를 통합하여 2차 가공 없이 인장 강도를 향상시킵니다. 홀로그램 볼류메트릭 프린팅은 전체 레이어를 동시에 경화시켜 최대 20배의 속도 향상을 입증하여 대량 생산되는 자동차 내장 부품에 유망한 기술로 평가받고 있습니다. 공정 시뮬레이션 소프트웨어의 지속적인 개선으로 시행착오를 줄이고, SLS의 설치 기반이 증가하더라도 FDM의 관련성을 유지할 수 있습니다.

하드웨어는 2024년 매출액의 57.32%를 차지했으며, 프린터, 후처리 스테이션, 스캐너 등이 포함됩니다. 그러나 머신러닝 알고리즘이 불량률을 낮추고, 여러 공장에 대한 차량 편성을 위해 소프트웨어의 CAGR은 18.78%로 확대되고 있습니다. Baker Hughes에서 도입한 제조 운영 플랫폼은 모니터링 시간을 98% 단축하고 스크랩을 18% 줄였습니다. 자동차 제조업체가 자본 지출을 정당화할 수 없는 특수 소재나 소량 생산을 아웃소싱하는 경우, 서비스 뷰로가 활약합니다.

AI를 활용한 조형 매개변수 엔진은 엔지니어링의 노동력을 80% 절감하고, 자동차 3D 프린팅 시장에서 소프트웨어 점유율 확대에 기여하고 있습니다. 브라우저 기반의 협업 스위트는 대륙을 넘나들며 설계를 반복할 수 있고, 동시 엔지니어링과 생산에 대한 신속한 릴리스가 가능합니다. 클라우드 연결이 확대됨에 따라 구독 수익은 벤더에게 수익성 높은 연금을 제공하고 경쟁의 균형을 기계에서 디지털 생태계로 이동시킵니다.

자동차 산업의 3D 프린팅 시장 보고서는 기술 유형(선택적 레이저 소결(SLS), 스테레오리소그래피(SLA), 기타), 부품 유형(하드웨어, 소프트웨어, 서비스), 재료 유형(금속, 폴리머, 기타), 용도 유형(생산, 프로토타이핑, 기타), 지역별로 구분하여 분석하였습니다. 프로토타이핑, 기타), 지역별로 분류하고 있습니다. 시장 예측은 금액(USD)과 수량(단위)으로 제공됩니다.

북미는 2024년 38.63%의 점유율로 자동차 3D 프린팅 시장을 주도했으며, 미국의 지배적인 항공우주 및 EV 공급망에 힘입어 자동차 3D 프린팅 시장을 주도하고 있습니다. GE Aerospace의 10억 달러 규모의 적층 가공 설비 투자는 국내 생산에 대한 장기적인 자신감을 보여줍니다. 인플레이션 감소 법과 결합 된 재 단축 이니셔티브는 현지 제조에 대한 인센티브를 제공하고 자동차 산업 전반에 걸쳐 프린터 설치를 가속화할 것입니다. 캐나다와 멕시코는 국경을 초월한 무역의 틀을 활용하여 경량 트럭 부품과 항공우주용 주조 금형을 통해 기여하고 있습니다.

아시아태평양은 2030년까지 19.47%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역으로, 중국의 제조 디지털화와 인도의 신흥 바이오 프린팅 기업들에 의해 주도될 것입니다. 중국의 5개년 계획은 적층 가공를 전략적 기둥으로 삼고, 자동차 허브와 배터리 공장에 적층 가공를 도입 확대에 박차를 가하고 있습니다. 인도에서는 EOS와 Godrej의 협력으로 항공우주 응용을 가속화하고, 민관 R&D 센터가 기술 개발을 촉진합니다. 일본과 한국은 소재 혁신을 추진하여 하이브리드 전기 파워트레인에 맞는 내열성 폴리머를 개발합니다. 동남아시아의 전자 클러스터는 정부의 세제 혜택에 힘입어 금형 제작에 3D 프린팅을 채택하고 있습니다.

유럽은 대부분의 제조업체가 적층 공정을 도입한 독일을 중심으로 큰 점유율을 차지하고 있습니다. 이 지역은 AM 기업 매출의 30.6%를 연구개발에 투자하고 있으며, 금속 프린터 수출의 리더십을 강화하고 있습니다. 프랑스와 이탈리아는 슈퍼카에 복합 프린팅을 확대하고 있으며, 스칸디나비아는 자동차 내장재에 바이오 폴리머를 적용하는 방안을 모색하고 있습니다. ISO/ASTM 표준에 따른 규제 정합성은 인쇄 부품의 국경 간 인증을 지원하여 공급망 흐름을 원활하게 합니다. 남미와 중동의 신흥 지역은 다변화를 추구하고, 사우디아라비아는 금속 가공의 에너지 소비를 줄이기 위해 중소기업에 보급형 프린터를 제공합니다. 브라질은 농업 기계에 대한 적층 수리 허브를 시범적으로 설치하여 이 기술이 고소득 경제권 외의 지역에도 적용될 수 있다는 것을 입증하고 있습니다.

The Automotive 3D printing market is valued at USD 5.91 billion in 2025 and is forecast to reach USD 12.54 billion by 2030, reflecting a 16.25% CAGR.

The shift from prototyping toward full-scale production is accelerating as breakthroughs in multi-material processing, digital supply-chain orchestration, and artificial-intelligence-driven quality control redefine manufacturing economics. Demand for lightweight components that meet stringent emissions rules, illustrated by BMW's 27% emissions reduction using wire-arc additive manufacturing, underpins growth. Hardware advances in fused deposition modeling (FDM) and selective laser sintering (SLS) improve throughput, while cost-effective iron-silicon powders open metal applications for electric-vehicle (EV) motor parts. Regulatory pressure, on-shoring strategies, and the availability of sustainable feedstocks align to expand the Automotive 3D printing market across established and emerging economies.

Electric vehicle makers pursue weight optimization to extend their range and comply with emissions standards. General Motors integrates more than 130 printed parts in the Cadillac Celestiq, including the largest additively manufactured aluminum component in automotive production. Europe's Euro 7 norms accelerate adoption for brake-disc coatings and structural elements. Sand-based 3D printing shortens mold-development cycles, enabling casting designs that reduce mass while preserving tolerance targets. The need to offset battery weight intensifies competitive incentives to remove every gram across vehicle platforms.

Enterprises report up to 90% reductions in prototype lead times and sharp declines in single-part costs as additive manufacturing replaces machining for early-stage design iterations. Stereolithography's high dimensional accuracy supports low-cost investment casting alternatives, while AI-based build-parameter optimization elevates first-time-right success rates. Desktop SLS printers priced below USD 3,000 broaden access for small and midsize suppliers, compressing innovation cycles across Asia-Pacific manufacturing clusters.

Industrial SLS printers list between USD 12,000 and USD 33,000, while specialty metal powders average USD 300-600 per kg, limiting adoption among cost-sensitive suppliers. Helium-atomized powder production offers the most sustainable route, yet capital outlays remain steep. Lifecycle analyses show powder-bed fusion is economical for high-complexity components, but up-front capital still deters wide deployment. Lower-cost metal-filament processes mitigate entry barriers but add post-processing complexity, reducing the Automotive 3D printing market CAGR by 2.4 percentage points

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

FDM accounted for 38.32% of the Automotive 3D printing market share in 2024, owing to low system costs and broad material selection. SLS is projected to grow at an 18.53% CAGR through 2030 as desktop powder-bed systems below USD 3,000 democratize high-performance nylon and composite printing. Advances in nanoscale photopolymerization have pushed stereolithography resolution to 100 nm at 100 µm per second, extending its use into microfluidic and optics applications. Digital Light Processing (DLP) increasingly supports jewelry and dental models, while electron-beam melting serves aerospace titanium parts. The Automotive 3D printing market size for SLS-based parts is forecast to expand sharply as EV manufacturers adopt durable nylon gears and under-hood components.

Hybrid manufacturing that blends additive and subtractive techniques is gaining ground. FDM toolpaths integrate continuous-fiber reinforcement, improving tensile strength without secondary operations. Holographic volumetric printing demonstrates up-to-20-fold speed gains by curing entire layers simultaneously, holding promise for high-volume automotive interiors. Continual improvements in process simulation software reduce trial iterations, ensuring FDM retains relevance even as the SLS installed base rises.

Hardware captured 57.32% of 2024 revenue, encompassing printers, post-processing stations, and scanners. However, software is expanding at 18.78% CAGR as machine-learning algorithms cut defect rates and orchestrate multi-factory fleets. Manufacturing operations platforms deployed at Baker Hughes trimmed monitoring time by 98% and scrap by 18%. Service bureaus flourish when automakers outsource specialty materials or small production runs that do not justify capital spending.

AI-driven build-parameter engines reduce engineering labor by 80%, contributing to a rising software share within the Automotive 3D printing market. Browser-based collaboration suites allow design iterations across continents, enabling simultaneous engineering and rapid release to production. As cloud connectivity scales, subscription revenue offers vendors a high-margin annuity, shifting the competitive balance from machines to digital ecosystems

The 3D Printing in Automotive Industry Market Report is Segmented by Technology Type (Selective Laser Sintering (SLS), Stereo Lithography (SLA), and More ), Component Type (Hardware, Software, and Service), Material Type (Metal, Polymer, and More), Application Type (Production, Prototyping, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

North America leads the Automotive 3D printing market with a 38.63% share in 2024, supported by the United States' dominant aerospace and EV supply chains. GE Aerospace's USD 1 billion investment in additive facilities signals long-term confidence in domestic productio. Reshoring initiatives combined with the Inflation Reduction Act incentivize localized manufacturing, accelerating printer installations across automotive tiers. Canada and Mexico contribute through lightweight truck components and aerospace casting molds, leveraging cross-border trade frameworks.

Asia-Pacific is the fastest-growing region at a 19.47% CAGR through 2030, propelled by China's manufacturing digitalization and India's emerging bioprinting startups. Chinese five-year plans earmark additive manufacturing as a strategic pillar, spurring installation growth across automotive hubs and battery factories. India's collaboration between EOS and Godrej accelerates aerospace applications, while public-private R&D centers foster skill development. Japan and South Korea push materials innovation, developing heat-resistant polymers tailored to hybrid-electric powertrains. Southeast Asian electronics clusters adopt 3D printing for tooling, aided by government tax incentives.

Europe holds a significant share, anchored by Germany where majority of manufacturers deploy additive processes. The region invests 30.6% of AM company turnover back into R&D, reinforcing leadership in metal-printer exports. France and Italy expand composite printing for supercars, while Scandinavia explores bio-based polymers for vehicle interiors. Regulatory alignment through ISO/ASTM standards supports cross-border qualification of printed parts, smoothing supply-chain flows. Emerging regions in South America and the Middle East pursue diversification; Saudi Arabia outfits SMEs with entry-level printers to decrease energy consumption in metal fabrication. Brazil pilots additive repair hubs for agricultural machinery, demonstrating the technology's reach beyond high-income economies.