ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

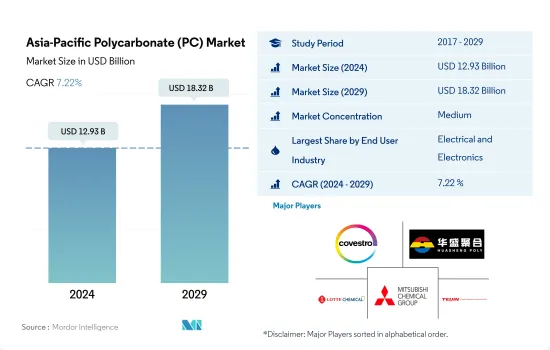

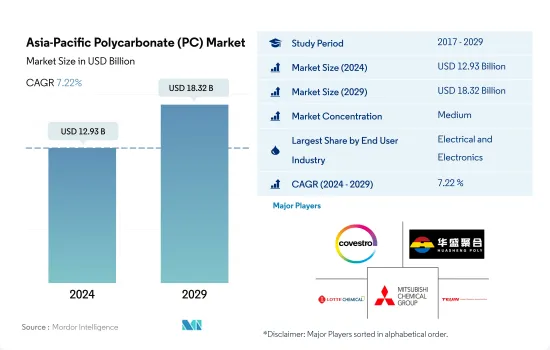

아시아태평양의 폴리카보네이트(PC) 시장 규모는 2024년에 129억 3,000만 달러에 이르렀고, 2029년에는 183억 2,000만 달러에 달할 것으로 예상되며, 예측기간 중(2024-2029년) CAGR은 7.22%를 나타낼 전망입니다.

우위성을 유지하는 전기 및 전자산업

폴리카보네이트는 범용성과 내구성이 뛰어나 다양한 산업에서 널리 이용되고 있습니다. 혈액투석막, 혈액저장소, 혈액필터 등에 응용되고 있습니다.

2017-2019년에 걸쳐 폴리카보네이트 수요는 꾸준한 성장을 이루었고 전년대비 성장률은 각각 5.14%, 3.53%였습니다.

2020년에는 COVID-19 팬데믹에 의해 조업, 여행, 무역이 제한되어 폴리카보네이트 수요는 전년 대비 3.71% 감소했습니다. 특히 영향을 받은 것은 자동차 산업과 산업기계 산업으로 올해 수량은 각각 12.52%와 16.65% 감소했습니다.

기존의 아크릴이나 유리를 폴리카보네이트로 대용하는 동향의 고조가, 예측 기간중의 동 재료 수요를 견인할 것으로 예측됩니다. 자산업이 가장 높은 성장을 이룰 것으로 예측되고 있으며, 예측기간 중 수량 기준으로 CAGR은 7.63%를 나타낼 것으로 전망됩니다. 전반적으로 폴리 카보네이트에 대한 지역 수요는 예측 기간 동안 볼륨 측면에서 5.66%, 가치 측면에서 7.22%의 연평균 성장률을 기록 할 것으로 예상됩니다.

중국은 수량이든 금액이든 우위를 유지

아시아태평양은 세계 최대의 폴리카보네이트 소비국으로 2022년에는 63.07% 이상의 점유율을 차지했습니다.

2017-2019년에 걸쳐, 폴리카보네이트 수요는 주로 중국이나 인도와 같은 나라에서의 플라스틱 포장 산업의 급성장에 의해 꾸준한 성장을 나타냈습니다. 더 산업에 심각한 영향을 미치고 이에 따라 이 지역의 폴리카보네이트 수요에 부정적인 영향을 미쳤습니다.

2021년에는 규제가 완화되었고, 폴리카보네이트 수요는 대유행 전의 수준까지 회복되었습니다. 전반적으로 아시아 태평양 지역의 폴리카보네이트 수요는 예측 기간 동안 5.60%의 연평균 성장률(볼륨 기준)을 나타낼 것으로 예상됩니다.

아시아태평양의 폴리카보네이트(PC) 시장 동향

ASEAN 국가의 급성장은 전자 생산을 촉진

아시아태평양에서는 2020-2021년에 걸쳐 전기 및 전자기기의 생산수입이 13.9% 증가했습니다. 전자 부문은 대부분의 아시아 국가의 수출 총액의 20-50%를 차지했습니다. 텔레비전, 라디오, 컴퓨터, 휴대전화 등의 소비자용 전자기기 제품의 대부분은 아세안 지역에서 생산되고 있습니다.

ASEAN은 하드디스크 드라이브 생산을 선도하고 있으며 하드디스크 드라이브의 80% 이상이 ASEAN 지역 내에서 생산되고 있습니다. 전반적으로 ASEAN의 전기 및 전자(E&E) 산업은 다른 산업보다 외국의 투입물과 기술에 의존하고 있으며, E&E 수출의 53%는 ASEAN의 E&E 수출에 내장된 외국 부가가치(FVA) 또는 외국에서의 투입물에 의한 것입니다.

태국과 말레이시아 같은 국가들은 지역 내 전자 생산을 선도하고 있습니다. 동남아시아 최대급 전자기기 조립기지를 보유한 태국은 하드 드라이브, 집적회로, 반도체 생산에 선도하고 있습니다. 에어컨 제조에서는 2위, 세계 냉장고 시장에서는 4위입니다.

전자 산업은 중국과 일본과 같은 아시아 경제 대국과 무역 개선을 촉진하는 ASEAN의 통합 생산 네트워크로부터 큰 혜택을 누리고 있습니다.

중국은 전기 제품의 세계 수출로 11.2%의 점유율을 차지했으며, 2019-2020년에 걸쳐 디지털 제품의 수출로 5.8%의 성장을 기록했습니다. 아시아개발은행에 따르면 중국은 이 지역의 전자기기에 큰 시장을 제공합니다. 태국, 일본, 중국, 말레이시아, 인도, 필리핀 등의 국가들은 전자 생산에서 계속 이 지역을 선도하고 있습니다.

아시아태평양의 폴리카보네이트(PC) 산업 개요

아시아태평양의 폴리카보네이트(PC) 시장은 적당히 통합되어 있으며 상위 5개 기업에서 59.21%를 차지하고 있습니다.

The Asia-Pacific Polycarbonate (PC) Market size is estimated at 12.93 billion USD in 2024, and is expected to reach 18.32 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Electrical and electronics industry to maintain its dominance

Polycarbonates are widely utilized in various industries due to their versatile and durable nature. They find applications in refrigerators, agricultural houses, industrial and public buildings, facades, surgical instruments, drug delivery systems, hemodialysis membranes, blood reservoirs, and blood filters. The electrical and electronics industry has been the largest consumer of polycarbonate in the region, and it accounted for over 45% of the market share in 2022.

Between 2017 and 2019, polycarbonate demand experienced steady growth, with Y-o-Y rates of 5.14% and 3.53%, respectively. The increasing production in the electronics industry primarily drove this growth.

In 2020, the COVID-19 pandemic led to operational, travel, and trade restrictions, resulting in a decline in the demand for polycarbonates by 3.71% compared to the previous year. The automotive and industrial machinery industries were particularly affected, experiencing declines of 12.52% and 16.65% in their 2019 volumes, respectively. However, as the restrictions eased, the demand for polycarbonates gradually recovered, with China and India playing a significant role in driving the growth.

The growing trend of substituting traditional acrylics and glass with polycarbonates is expected to drive the demand for the material in the forecast period. Among all end-user industries in the Asia-Pacific region, the electrical and electronics industry in India is projected to witness the highest growth, with a CAGR of 7.63% in terms of volume during the forecast period. Overall, the regional demand for polycarbonates is expected to record a CAGR of 5.66% in volume terms and 7.22% in value terms throughout the forecast period.

China to maintain its dominance both in terms of volume and value

The Asia-Pacific region is the largest consumer of polycarbonates globally, occupying a share of over 63.07% in 2022. In the Asia-Pacific region, polycarbonates find various applications in the electrical and electronics, automotive, aerospace components manufacturing, and healthcare devices manufacturing industries.

During 2017-2019, the demand for polycarbonates witnessed steady growth, mainly driven by the rapid growth in the plastic packaging industry in countries like China and India. In 2020, various restraining factors, like worker unavailability and raw material shortages caused by operational and trade restrictions during the pandemic, severely affected various end-user industries, thereby negatively affecting the polycarbonate demand in the region. Among all countries, the polycarbonate demand in Australia was affected severely. In 2020, the country's Y-o-Y demand volume declined by 40.96%, whereas the regional Y-o-Y decline was 3.71%.

In 2021, as the restrictions eased, the polycarbonate demand rose back to its pre-pandemic level. This growth was majorly driven by the rapid growth in industrial activities in countries like India. This growth trend is expected to continue throughout the forecast period, with India witnessing the highest growth in polycarbonate demand among all countries. Overall, the polycarbonate demand in the Asia-Pacific region is expected to record a CAGR of 5.60% (in volume) during the forecast period.

Asia-Pacific Polycarbonate (PC) Market Trends

Rapid growth in ASEAN countries to foster electronics production

The Asia-Pacific region saw an increase in electrical and electronics production revenue by 13.9% from 2020 to 2021. The electronics sector accounts for 20-50% of the total value of most Asian countries' exports. Consumer electronics such as televisions, radios, computers, and cellular phones are largely manufactured in the ASEAN region.

ASEAN leads the production of hard drives, with over 80% of hard drives being manufactured in the region. Overall, the electrical and electronics (E&E) industry in ASEAN relies more on foreign inputs and technology than other industries, with 53% of E&E exports arising from foreign value added (FVA) or foreign inputs integrated into ASEAN's E&E exports.

Countries like Thailand and Malaysia lead in the production of electronics in the region. Thailand, home to one of the largest electronics assembly bases in Southeast Asia, leads in the production of hard drives, integrated circuits, and semiconductors. It ranks second in manufacturing air conditioning units and fourth in the global refrigerators market.

The electronics industry has greatly benefitted from ASEAN's integrated production networks, which foster improved trade with larger Asian economies like China and Japan.

China held an 11.2% share of global exports in electrical products and registered a growth of 5.8% in the export of digital products from 2019 to 2020. According to the Asian Development Bank, China provides a large market for electronics in the region. Countries such as Thailand, Japan, China, Malaysia, India, and the Philippines continue to lead the region in the production of electronics.

Asia-Pacific Polycarbonate (PC) Industry Overview

The Asia-Pacific Polycarbonate (PC) Market is moderately consolidated, with the top five companies occupying 59.21%. The major players in this market are Covestro AG, Hainan Huasheng New Material Technology Co., Ltd., Lotte Chemical, Mitsubishi Chemical Corporation and Teijin Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Electrical and Electronics

4.1.5 Packaging

4.2 Import And Export Trends

4.2.1 Polycarbonate (PC) Trade

4.3 Price Trends

4.4 Form Trends

4.5 Recycling Overview

4.5.1 Polycarbonate (PC) Recycling Trends

4.6 Regulatory Framework

4.6.1 Australia

4.6.2 China

4.6.3 India

4.6.4 Japan

4.6.5 Malaysia

4.6.6 South Korea

4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Electrical and Electronics

5.1.5 Industrial and Machinery

5.1.6 Packaging

5.1.7 Other End-user Industries

5.2 Country

5.2.1 Australia

5.2.2 China

5.2.3 India

5.2.4 Japan

5.2.5 Malaysia

5.2.6 South Korea

5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 CHIMEI

6.4.2 Covestro AG

6.4.3 Formosa Plastics Group

6.4.4 Hainan Huasheng New Material Technology Co., Ltd.

6.4.5 LG Chem

6.4.6 Lotte Chemical

6.4.7 Mitsubishi Chemical Corporation

6.4.8 Sinochem

6.4.9 Sinopec SABIC Tianjin Petrochemical Company (SSTPC)

6.4.10 Teijin Limited

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)