북미의 폴리카보네이트(PC) 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

North America Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1693834

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

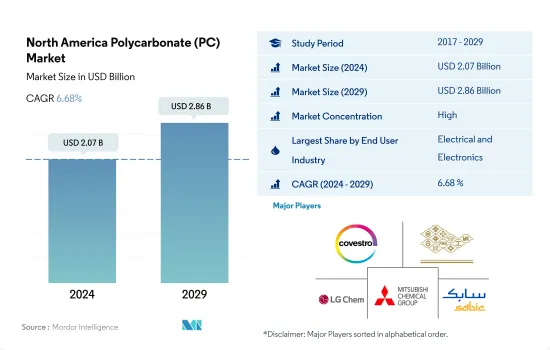

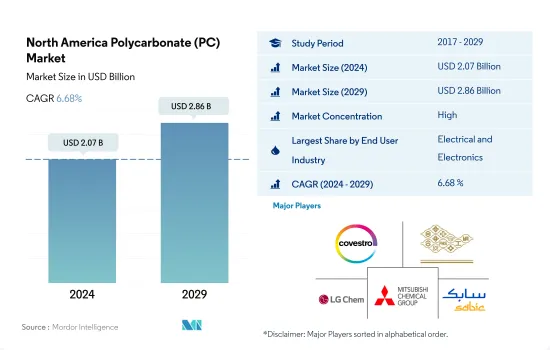

북미의 폴리카보네이트(PC) 시장 규모는 2024년에 20억 7,000만 달러에 이르렀고, 2029년에는 28억 6,000만 달러에 달할 것으로 예상되며, 예측 기간 중(2024-2029년) CAGR은 6.68%를 나타낼 전망입니다.

폴리카보네이트 제조 기술 진보가 시장 수요를 끌어올립니다.

폴리카보네이트는 높은 충격 강도, 경량, 내 자외선, 광학 변속기, 전기적 특성 및 기타 많은 특성으로 인해이 지역에서 인기가 있습니다. 폴리카보네이트는 유리와 같은 90%의 빛을 투과할 수 있습니다.

유독한 비스페놀(BPA) 대신에 탄산가스(CO2)를 원료로 하는 폴리카보네이트의 새로운 생산 기술의 동향의 고조가, 최근 시장을 견인하고 있습니다.

이 지역의 폴리카보네이트(PC) 시장은 2020년 금액 기준으로 2019년 대비 7.8% 감소했습니다. 동시기의 COVID-19 팬데믹에 의해 미국, 멕시코, 캐나다 등 여러 국가에서 전국적인 조업 정지가 발생하여 생산 설비가 3개월 가까이 정지 공급망의 혼란, 원료 부족, 지역 전체 무역 교류의 정지가 이 같은 침체를 가져왔습니다.

폴리카보네이트는 북미의 전기 및 전자 산업에서 다양한 용도로 널리 사용되고 있습니다. 고도가 북미에서의 폴리카보네이트 수지 수요를 견인할 것으로 예측됩니다. 전기 및 전자 산업은 북미에서 가장 빠르게 성장하는 최종 사용자 산업으로 예측 기간인 2023-2029년 동안 가치 기준으로 8.29%의 연평균 성장률을 나타낼 것으로 예상됩니다.

미국이 북미의 폴리카보네이트(PC) 시장을 독점, 건설 활동의 활성화와 일렉트로닉스 의료 산업의 성장에 의한

2022년의 폴리카보네이트 수지의 세계 소비량에 차지하는 북미의 비율은 금액 기준으로 10.2%였습니다.

미국은 건설, 전기 및 전자, 의료산업의 성장에 따라 국가별로는 북미에서 가장 큰 폴리카보네이트 수지 소비국입니다. 신설 바닥 면적은 2022년 58억 평방미터에서 2029년에는 74억 평방미터에 이를 것으로 예상되고 있습니다. 성장하는 건설 산업에서 폴리카보네이트 수지에 대한 수요는 예측 기간(2023-2029년) 동안 가치 기준으로 6.46%의 CAGR을 나타낼 것으로 예상됩니다.

멕시코에서는 자동차 생산과 일렉트로닉스 산업 등의 성장에 따라 폴리카보네이트 수지 수요가 대폭 증가하고 있습니다. 동국의 소비자용 전자기기 산업도 성장하고 있어, 2007년에는 220억 달러에 이르렀습니다.

또한 기존의 재료와 비슷한 강도를 가지며 경량이기 때문에 첨단 재료의 사용도 증가하고 있습니다.

북미의 폴리카보네이트(PC) 시장 동향

기술 혁신의 강력한 성장이 산업 전체의 성장을 뒷받침

북미의 전기 및 전자기기 생산은 스마트 TV, 냉장고, 에어컨 등의 소비자용 전자기기 제품 수요 증가와 기술의 진보가 더해져 2017-2019년에 걸쳐 1.4% 이상의 CAGR을 나타냈습니다.

북미의 전자기기 매출은 생산시설의 운영 정지, 공급망의 혼란 등 다양한 제약으로 인해 COVID-19의 영향으로 2020년에는 2019년 대비 약 9% 감소했습니다. 그 결과, 이 지역의 전기 및 전자기기 생산에 의한 수익은 2020년에 전년 대비 4.7% 감소했습니다.

2021년에는 이 지역의 소비자용 전자기기 매출액이 약 1,130억 달러에 달했으며 2020년보다 4% 증가했습니다. 그 결과 북미의 전기 및 전자기기 생산은 2021년 전년 대비 13.8% 증가했습니다.

2027년에는 북미는 전기 및 전자기기 생산에서 제3위의 지역이 되어 세계 시장의 약 10.5%의 점유율을 차지할 것으로 예측되고 있습니다. 효율성과 저비용을 실현하기 위해 가상현실, IoT 솔루션, 로봇공학 등의 선진기술이 소비자용 전자기기 제품에 등장한 것이 소비자용 전자기기 산업에 큰 이점을 가져왔습니다. 이 지역의 소비자용 전자기기 산업은 2023년 1,276억 달러에서 2027년에는 약 1,618억 달러 규모에 이를 것으로 예측됩니다. 그 결과, 이 지역의 전기 및 전자제품 수요는 증가할 것으로 예측됩니다.

북미의 폴리카보네이트(PC) 산업 개요

북미의 폴리카보네이트(PC) 시장은 상당히 통합되어 상위 5개사가 100%를 차지하고 있습니다. 이 시장의 주요 기업은 Covestro AG, Formosa Plastics Group, LG Chem, Mitsubishi Chemical Corporation, SABIC 등입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

전기 및 전자

포장

수출입 동향

폴리카보네이트(PC) 무역

가격 동향

형태 동향

재활용 개요

폴리카보네이트(PC) 재활용 동향

규제 프레임워크

캐나다

멕시코

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

전기 및 전자

산업 및 기계

포장

기타

국가명

캐나다

멕시코

미국

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

CHIMEI

Covestro AG

Formosa Plastics Group

LG Chem

Lotte Chemical

Luxi Group

Mitsubishi Chemical Corporation

SABIC

Teijin Limited

Trinseo

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The North America Polycarbonate (PC) Market size is estimated at 2.07 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 6.68% during the forecast period (2024-2029).

Technological advancements in the manufacturing of polycarbonate to boost market demand

Polycarbonate is popular in the region for its high impact strength, lightweight, UV resistance, optical transmission, electrical, and many other properties. The impact strength of the polycarbonate sheet is 200 times more than common glass. Polycarbonate can transmit 90% of light through it, the same as glass. The demand for polycarbonate in the region is expected to grow by 7.93%, by value, in 2023 compared to 2022.

The rising trend of new production technology of polycarbonate from carbon dioxide gas (CO2) instead of bisphenol (BPA), which is toxic in nature, has driven the market over recent years.

The polycarbonate market in the region declined by 7.8% in terms of value in 2020 compared to 2019. The COVID-19 pandemic during the same period halted production facilities for nearly three months because of nationwide lockdowns in several countries, including the United States, Mexico, and Canada. The supply chain disruptions, raw material shortages, and stoppage of trade exchanges across the region resulted in such a decline. However, the demand regained in 2021 with a growth rate of 18.24% compared to 2020, owing to the resumption of production facilities to its annual capacity output.

Polycarbonate is widely used in the electrical and electronics industry for various applications in North America. The industry consumed nearly 126 thousand tons of polycarbonate resin in North America. The rising trend of high-strength and lightweight material in consumer electronics is expected to drive the demand for polycarbonate resins in North America. The electrical and electronics industry is expected to be the fastest-growing end-user industry in North America, registering a CAGR of 8.29%, by value, during the forecast period, 2023-2029.

The United States to dominate the North American polycarbonate market owing to rising construction activities and growth in the electronics and medical industries

North America accounted for 10.2% by value of the global consumption of polycarbonate resins in 2022. Polycarbonate is a key polymer in North America for various industries, including automotive, building and construction, electrical and electronics, and medical.

The United States is the largest country-wise consumer of polycarbonate resin in the North American region, owing to growth in its construction, electrical and electronics, and medical industries. The country's construction industry, one of the largest end-user industries of polycarbonate, accounted for consumption of nearly 76,000 tons in 2022. The new floor area is expected to reach 7.4 billion square footage by 2029 from 5.8 billion square footage in 2022. The demand for polycarbonate resin in the growing construction industry is expected to register a CAGR of 6.46% by value during the forecast period (2023-2029).

The demand for polycarbonate resin is increasing significantly in Mexico owing to growth in vehicle production and electronics, among other industries. Mexico is the second-largest vehicle producer in North America. It produced 3.78 million units in 2022, a 7.67% increase over 2021. The country's consumer electronics industry is also growing, expected to reach USD 22 billion by 2027. These factors are expected to drive the demand for polycarbonate resins in Mexico during the forecast period.

The use of advanced materials is also growing, as they provide strength similar to existing ones and are lightweight. Such trends are expected to drive the demand for polycarbonate in North America over the forecast period. Polycarbonate is widely replacing glass in many applications because it is six times lighter and two times cheaper than glass.

North America Polycarbonate (PC) Market Trends

Strong growth of technological innovations to augment the overall growth of the industry

Electrical and electronics production in North America witnessed a CAGR of over 1.4% between 2017 and 2019 owing to the advancement of technology, coupled with the increasing demand for consumer electronics products, such as smart TVs, refrigerators, air conditioners, and other products. The rapid pace of electronic technological innovation is driving the demand for newer and faster electronic products. As a result, it has also increased the electrical and electronics production in the region.

Electronic device sales in North America fell by around 9% in 2020 compared to 2019, owing to the COVID-19 impact, because of the production facility shutdowns, supply chain disruptions, and various other constraints. As a result, revenue from electrical and electronics production in the region decreased by 4.7% in 2020 compared to the previous year.

In 2021, the sales of consumer electronics in the region reached around USD 113 billion, 4% higher than in 2020. As a result, North America's electrical and electronics production grew by 13.8% in 2021 in terms of revenue compared to the previous year.

By 2027, North America is projected to be the third-largest region for electrical and electronics production and account for a share of around 10.5% of the global market. The emergence of advanced technologies such as virtual reality, IoT solutions, and robotics into consumer electronic products to achieve efficiency and low cost has provided a significant advantage to the consumer electronics industry. The consumer electronics industry in the region is projected to reach a market volume of around USD 161.8 billion by 2027 from USD 127.6 billion in 2023. As a result, the demand for electrical and electronic products in the region is projected to increase.

North America Polycarbonate (PC) Industry Overview

The North America Polycarbonate (PC) Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Covestro AG, Formosa Plastics Group, LG Chem, Mitsubishi Chemical Corporation and SABIC (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Electrical and Electronics

4.1.5 Packaging

4.2 Import And Export Trends

4.2.1 Polycarbonate (PC) Trade

4.3 Price Trends

4.4 Form Trends

4.5 Recycling Overview

4.5.1 Polycarbonate (PC) Recycling Trends

4.6 Regulatory Framework

4.6.1 Canada

4.6.2 Mexico

4.6.3 United States

4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Electrical and Electronics

5.1.5 Industrial and Machinery

5.1.6 Packaging

5.1.7 Other End-user Industries

5.2 Country

5.2.1 Canada

5.2.2 Mexico

5.2.3 United States

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 CHIMEI

6.4.2 Covestro AG

6.4.3 Formosa Plastics Group

6.4.4 LG Chem

6.4.5 Lotte Chemical

6.4.6 Luxi Group

6.4.7 Mitsubishi Chemical Corporation

6.4.8 SABIC

6.4.9 Teijin Limited

6.4.10 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)